sankai/E+ via Getty Images

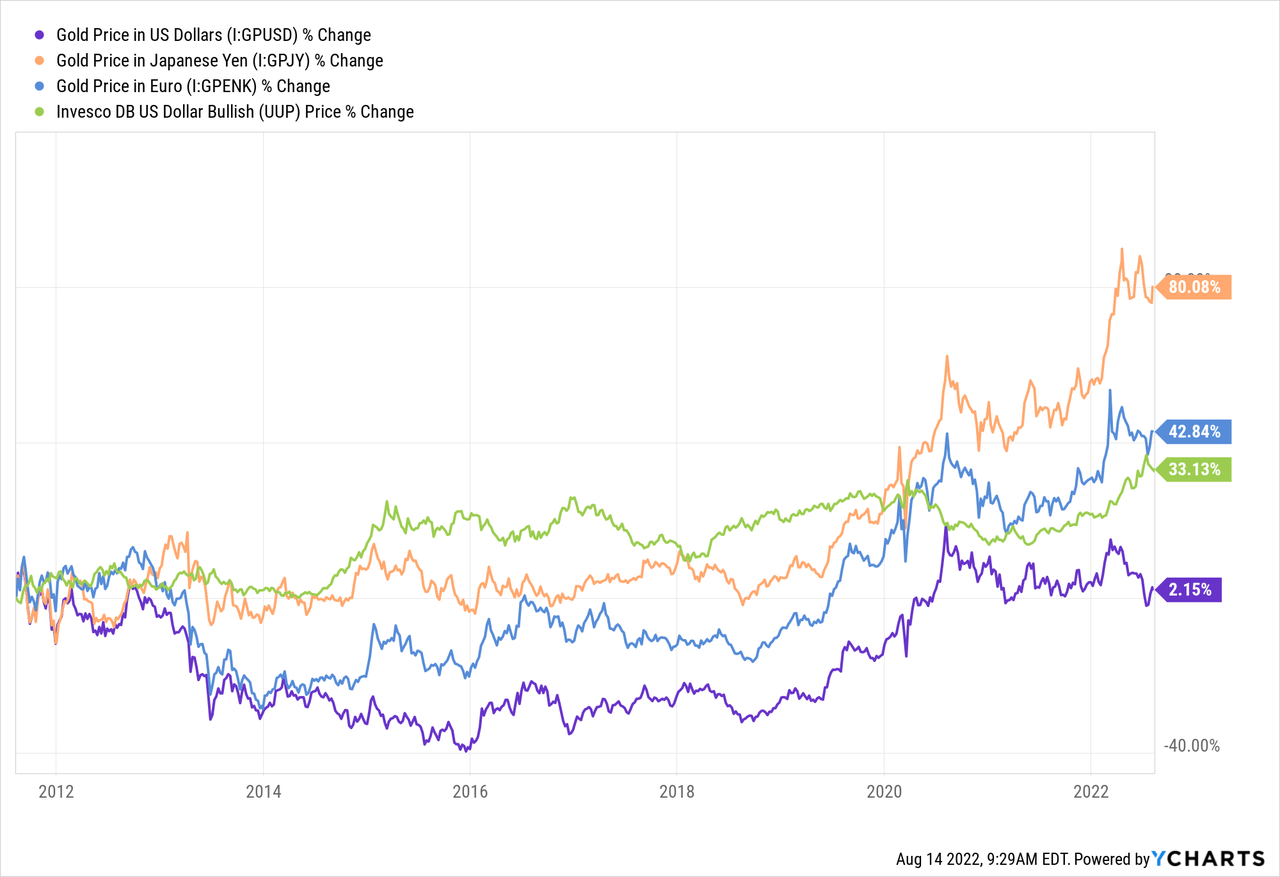

The price of gold has been held in a trading range for over two years. Gold fluctuated around the same range from 2011 to 2013 before it entered a bear market. With interest rates rising and inflation starting to slow, there is some reason to believe gold may repeat its historical pattern. However, inflation is high not only in the U.S. but also in the rest of the world. In many currencies, such as the Japanese Yen and the Euro, gold has broken firmly higher since 2022 began. Indeed, gold’s weakness in 2022 is attributable primarily to the relative strength of the U.S. dollar against foreign currencies. See below:

Gold is currently near an all-time-high in Japan and Europe, but is at a range-low in the U.S. due to the appreciation of the dollar against these currencies. Notably, most currencies in the developed world trade in prominent long-term trading ranges and rarely appreciate each other for too long. Economically, this attribute stems from inflation spreading across trading partners, forcing central banks to hike interest rates in tandem.

Despite high inflation in most developed economies, the U.S. is one of the only to pursue more significant interest rate hikes. Japan’s BOJ has thus far avoided interest rate hikes, while Europe’s ECB recently hiked rates to zero. The U.K., Canada, and Australia have been a bit more steady, but the U.S. remains the leader in higher interest rates among developed economies. This factor has contributed significantly to the U.S. dollar’s strength as others, such as the Yen, crumble toward nearly unseen lows. The dollar’s relative strength has lowered domestic inflation expectations and will likely cause inflation to be exported toward weakened currencies such as Japan.

With the inflation outlook slowing, the Federal Reserve is already looking to end interest rate hikes soon, meaning the U.S. dollar’s strength may quickly reverse, potentially causing gold to rise to a new all-time high. Ironically, we are in a situation where lower inflation benefits gold due to its impact on interest rates. More specifically, lower interest rates and higher inflation are ideal for gold, but the interest rate factor is more critical with the dollar so strong. I believe the gold ETF (NYSEARCA:GLD) may be a good trade over the coming months as the U.S. dollar’s relative strength unwinds.

Gold, Real Interest Rates, And Crude Oil

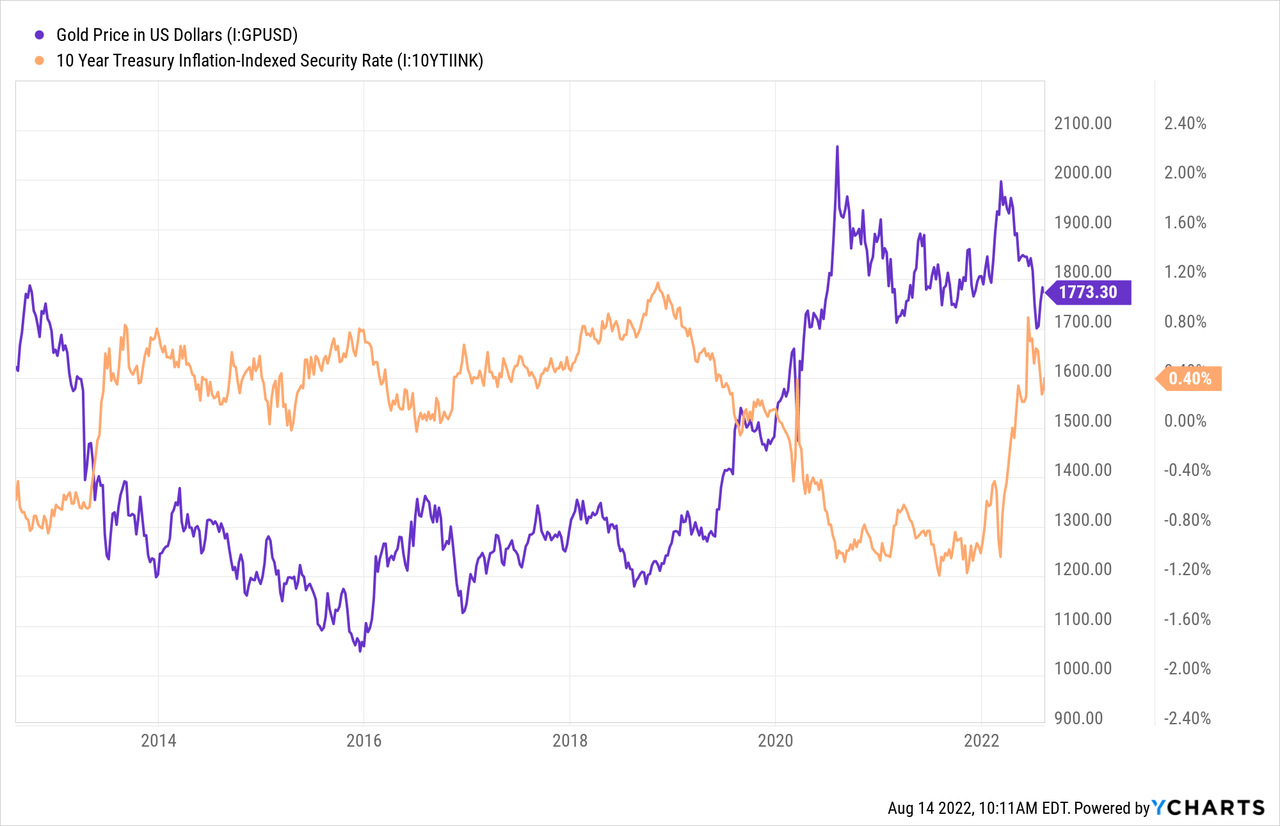

The primary driver of the U.S. price of gold is the long-term real interest rate. This rate can be measured directly by yields on inflation-indexed U.S. Treasury bonds. When real interest rates decline, gold’s comparative value to bonds increases, since it does not decay with inflation. When real interest rates rise, the bond’s relative value to gold increases since gold does not have a yield, this relationship makes for a strong inverse correlation between gold and real interest rates. See below:

Real interest rates were at extreme all-time lows before 2022, with 10-year inflation-indexed bonds paying ~-1.2% after the inflation adjustment. Real rates have risen dramatically this year as the drastic inflation spike triggered the end of the ultra-low interest rate era. Today, long-term investors in inflation Treasury bonds, such as those in the ETF (TIP), can earn a positive yield after whatever CPI inflation may be over the coming years (since they are indexed). However, with the economy slowing, I expect real interest rates will begin to climb back down toward negative levels as more investors consider low-risk assets. This factor has already benefited gold indirectly, as seen in the recent slight rise from $1700 to ~$1775 combined with a 40 bps decline in real interest rates.

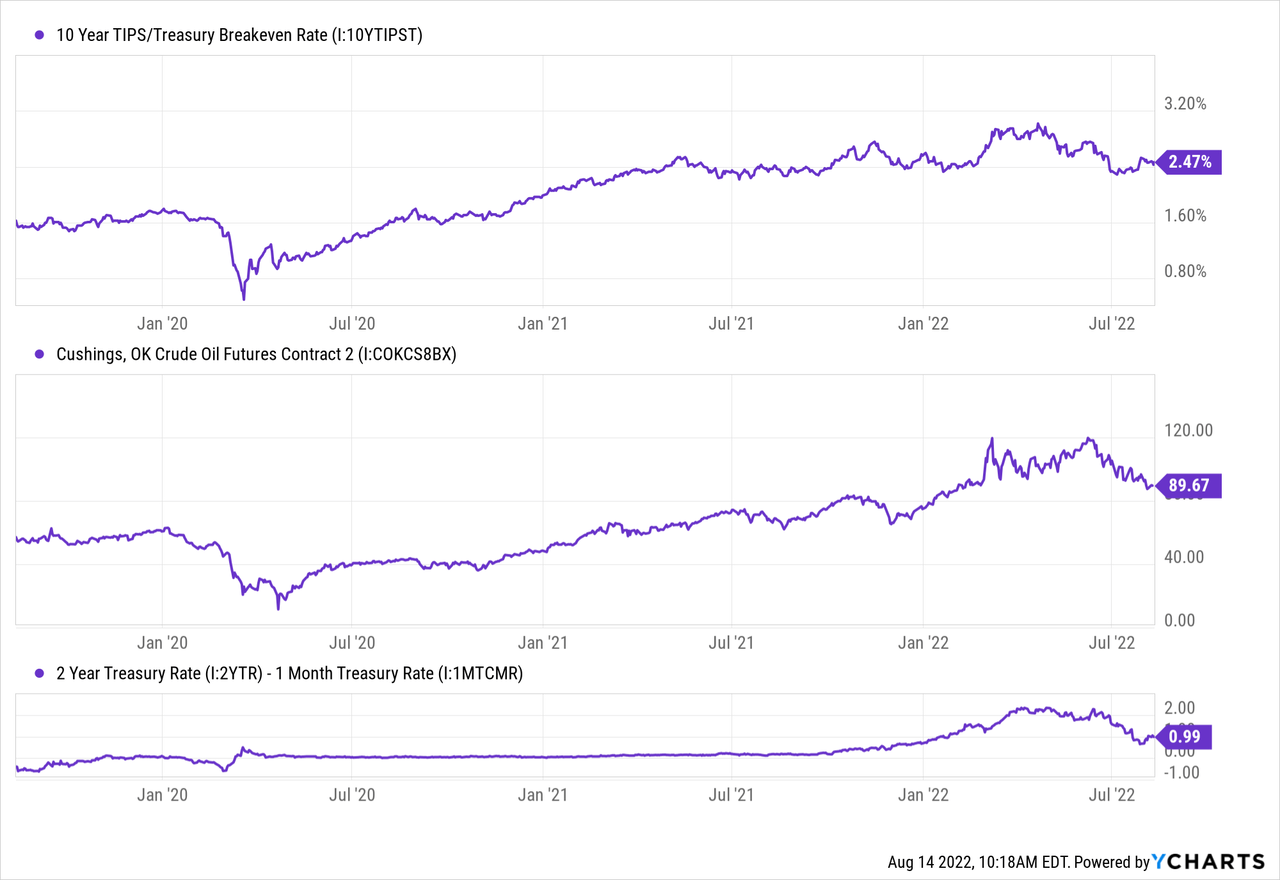

While last month saw a moderate slowdown in inflation, the long-term inflation rate may not have peaked. The bond market’s expectation of 10-year average inflation has slipped from around 3% to about 2.5% since May, coinciding with a moderate crude oil price decline. The Federal Reserve watches this figure closely and aims to create a policy outlook that holds this measure near 2%. As the inflation outlook has declined, so has the expected interest rate hike outlook (measured by the 2-year Treasury to 1-month spread). See below:

The bond market now expects a 1% total hike in interest rates to be sufficient to keep the long-term inflation average at 2.5% or below. Of course, this view is contingent on crude oil, arguably the primary inflation driver, remaining at current levels. In my opinion, it is unlikely crude oil will stay below $100 and is more likely to rise to a new all-time high by the end of 2023 due to ongoing declines in crude oil inventories and stagnating production growth. Indeed, evidence suggests the recent declines in crude oil are primarily attributable to immense SPR releases, which cannot be sustained. SPR withdrawal will end by next year, and, without significant production growth, crude oil may rise much higher and trigger another wave of inflation.

Euro And Yen Trends To Benefit U.S. Gold

Depending on the state of the economy, another rise in inflation may cause the Federal Reserve to pursue more substantial interest rate hikes. However, the inflation issue is likely worse in Europe and Japan due to their lower interest rates and lack of domestic commodity production. Europe and Japan are both heavily dependent on imports for energy products, so a rise in energy prices is likely to boost their inflation rates more than the U.S. The potential for “stickier” inflation in these regions will soon force the ECB and BOJ to hike interest rates aggressively.

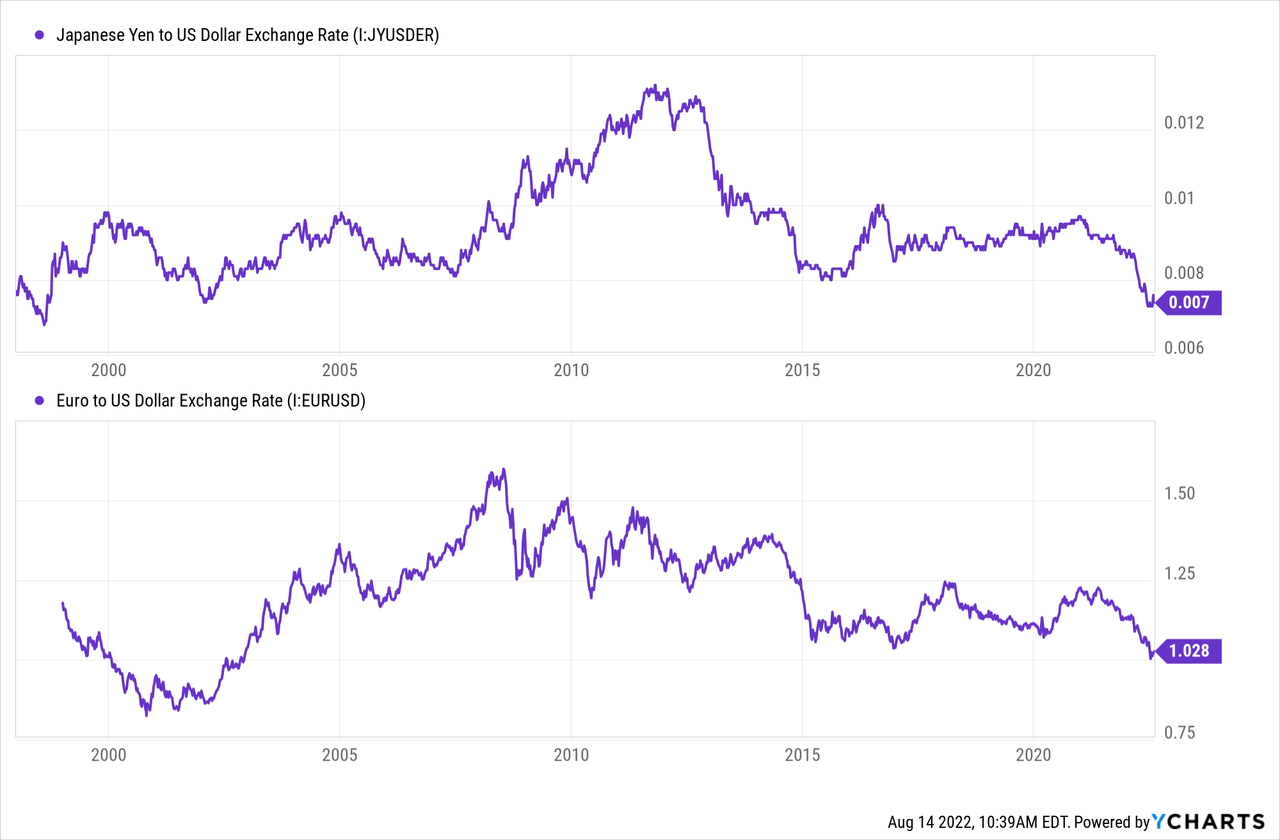

The JPY/USD and EUR/USD exchange rates are also both near extreme historical lows, supporting a reversal as their central banks become more hawkish than the Federal Reserve:

I believe this situation supports a solid bearish reversal for the US dollar. The US dollar may move at a swift pace lower over the coming months due to growing volatility associated with higher interest rates and inflation. The Japanese Yen has tumbled rapidly this year, so it may rally at an equally quick rate once its interest rate outlook adjusts. Given that gold is trending higher in Japan and Europe, a dollar weakening should cause it to trend higher in the US.

A Trade Opportunity In GLD

My view regarding the ETF GLD is not based on a hyperinflation outlook or any black-swan risks. In the case of an immense inflation shock, the ETF GLD may not be the best due to its counterparty risks, with physical metal likely being a better long-term alternative. However, in the short term, GLD appears to be an excellent bet since it is far more liquid, has essentially no premium (40 bps expense ratio), and closely tracks the future price of gold. I view GLD as a suitable way to bet on short-term directional moves on gold, and not as a hedge against hyperinflation or banking risks.

The core bullish catalysts for gold are a decline in the US dollar and a decline in US real interest rates. Gold may also benefit from another wave higher in crude oil. Still, I do not expect oil to rise until Biden’s administration ends SPR withdrawals – potentially in November. Of course, GLD carries the risk that real interest rates reverse higher or the US dollar continues to strengthen. I believe this is mitigated by the Federal Reserve’s slightly dovish shift, but the dollar’s trend has not yet broken entirely. Overall, I think this situation sets a strongly bullish trade for GLD. My current price target for GLD is $200-$220, equating to a gold target of ~$2100-$2300 by next spring.

Be the first to comment