Editor’s note: Seeking Alpha is proud to welcome UFD Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

George Frey

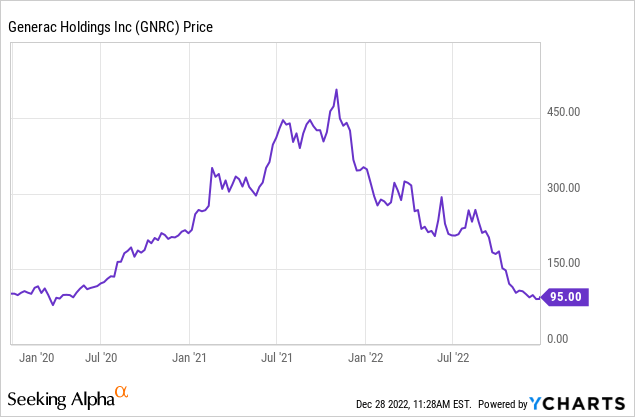

Shares of Generac Holdings (NYSE:GNRC) have seen a YTD decline of over 70%. This decline is partially due to macroeconomic factors and partially due to weakness in their home generator business. To make matters worse, the solar company Pink Energy has also sued Generac alleging that Generac sold them defective parts and failed to properly communicate with Pink Energy.

We began to take a closer look at Generac after it declined 25% on October 19, 2022, its worst one-day selloff since going public in 2010. They missed estimates on the top and bottom lines and lowered their full-year outlook, citing pressure on residential sales. Generac showed investors a problematic inventory build and that they have had difficulty installing their generators due to a labor shortage. Many investors finally threw in the towel after the company reported this disappointing quarter, while analysts were quick to cut their price targets.

We believe that this capitulation in the shares of Generac presents a buying opportunity; however, there are many risks to the thesis and investors should understand what they are getting themselves into.

The Company

Generac designs and manufactures a wide range of products for the generation of electricity. They are known for their generators, which are used to provide power in a variety of settings, including homes, businesses, and industrial facilities. Their generators are available in a range of sizes and styles, including portable, standby, and industrial models. In addition to generators, they also produce a variety of other products related to the generation and distribution of electricity, including transfer switches, power management systems, and load banks. Their products are designed to be reliable, efficient, and easy to use.

They are also involved in the solar industry. Their solar products include solar panels, inverters, and battery storage systems that can be used to generate and store electricity from the sun. These products are designed to be reliable, efficient, and easy to use, and can be integrated into a variety of different solar power systems, including grid-tied, off-grid, and hybrid systems. In addition to its solar products, Generac also offers a range of services related to the design, installation, and maintenance of solar power systems, including technical support and training.

An overview of Generac’s product portfolio

Generators: Generac offers a range of generators for various applications, including portable, standby, and industrial models. These generators can be powered by gasoline, diesel, natural gas, or propane, and are designed to provide reliable backup power for homes, businesses, and other facilities in the event of a power outage.

Transfer switches: Generac’s transfer switches allow users to safely and easily switch between different sources of power, such as utility power and a backup generator. The company offers a range of transfer switches in different sizes and configurations, including manual, automatic, and load-shedding models.

Power management systems: Generac’s power management systems are designed to help users optimize their energy usage and reduce their energy costs. These systems can be used to monitor and control the flow of electricity in a home or business, and can be configured to support a variety of different energy sources, including solar, wind, and hydroelectric power.

Load banks: Generac’s load banks are used to test and maintain the performance of generators and other electrical systems. These load banks can be used to simulate different types of loads, such as resistive, inductive, or capacitive loads, and can help users ensure that their generators are operating at optimal efficiency.

Other products: In addition to the products listed above, Generac also offers a variety of other products and services related to the generation and distribution of electricity, including solar power systems, fuel cells, and backup power systems for critical infrastructure.

They also produce pressure washers.

The Backdrop

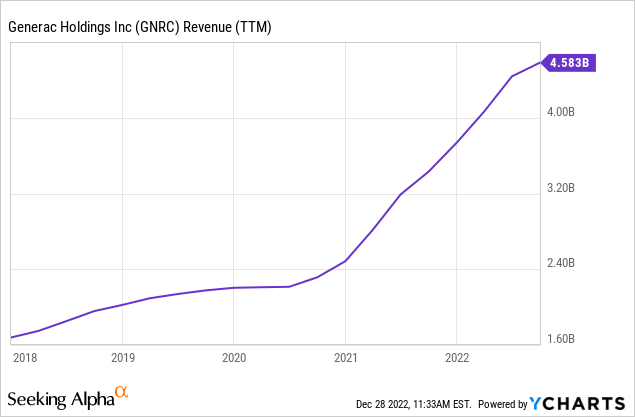

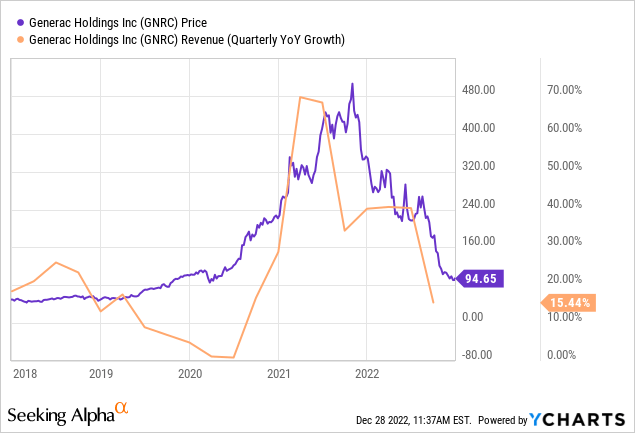

Generac saw accelerating sales growth over the previous two years, with year-over-year revenue up 13% in 2020 and 50% in 2021.

With this sales growth came hype from analysts and investors, and this hype carried shares of Generac up to an all-time high closing price of $505.80 on November 01, 2021. Their remarkable sales growth began to decelerate and the fundamentals were unable to support this lofty valuation, with shares plummeting to just $94.65 as of this writing.

Investor pessimism has steadily increased over the past 12 months, reaching a crescendo after Generac reported Q3 results that did not live up to expectations, as well as making a disappointing cut to their guidance.

Just as stocks often overshoot to the upside, they can also overshoot to the downside. We believe the selloff in Generac stock has finally become overdone, presenting an attractive buying opportunity.

Positives

The long-term fundamental tailwinds for Generac remain intact, and many of the issues that worry investors are short term in nature.

The Q3 report that sent shares tumbling wasn’t even that bad when looking at the absolute numbers. Much of the decline in earnings was due to one time charges related to the Pink Energy bankruptcy. Investors and analysts were disappointed that the numbers were lower than their expectations. Taking a step back, 15% revenue growth and $1.75 in adjusted earnings is still good, especially in a tough macro environment.

The forward guidance is what caused many investors and analysts to be concerned, but Generac is still guiding to grow revenue 22-24% year over year despite headwinds. It is likely that demand will pick up in the back half of 2023 and that Generac will be able to increase their installation capacity by then, resulting in the potential to outperform expectations.

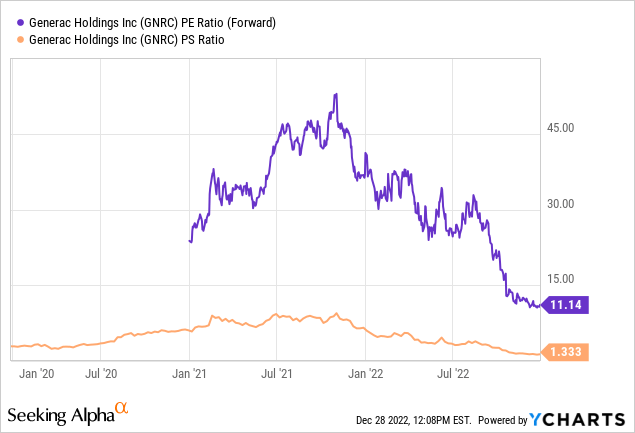

The valuation looks attractive here at 11.21 forward earnings, especially if Generac is able to beat growth estimates going forward. Generac has the potential to beat these estimates which would likely drive upward revisions and renewed positive sentiment.

The inventory build is a short-term headwind and Generac should be able to unwind this inventory in 2023. They will likely be more proficient at handling inventory in the future and this can serve as a learning experience for the company.

The Pink Energy lawsuit could see a resolution in 2023, with a favorable outcome heavily de-risking the stock.

Labor and input cost headwinds could abate and Generac could see material improvement in their operating margins.

Their business is becoming more diversified away from just home generators and could be viewed as an ESG play in the future.

A higher frequency of climate events could increase the demand for home generators.

Generac Valuation

We mentioned earlier how Generac looked attractive on a PE basis at 11.21 forward earnings. This is relatively cheap compared to recent history, though it is worth noting that investors had unrealistic growth expectations a year ago. On a price to sales basis Generac is back to trading around pre-COVID levels, despite having a notable increase in installed base since then.

Generac is a component of the S&P 500 and is classified as a member of the GICS® industrials sector. Below are the fundamentals for the S&P 500 industrial sector as of November 30, 2022.

Fundamental Valuation Multiples for the S&P 500 Industrial Sector (S&P Global)

We compared the above data to Generac’s trailing P/E of 13.73, forward P/E of 11.21, P/B of 2.49, and P/S of 1.23. On the surface it appears that Generac is trading at a steep discount when compared to their sector (except for dividend yield, they do not pay a dividend).

The industrial sector has seen a boost this year from aerospace and defense companies due to geopolitical conflicts, so a broad sector comparison should be taken with a grain of salt.

Generac is a generator pure play with some solar business upside. Most of their competitors on the generator side that are public companies are also much more diversified. Their competitors in the solar market are typically solar pure plays. This makes finding valuation comparisons difficult.

On a company-specific level, Generac’s closest competitor is Honeywell International (HON). Honeywell is a much more diversified company and are going to be more resistant to macro headwinds in the generator market. Keeping this in mind, when comparing the valuations of these businesses we see a sharp contrast.

Generac vs Honeywell Valuation Multiples (Data from Generac and Honeywell earnings reports)

Solar companies are typically given a higher multiple by the market than traditional industrial companies. Generac has the potential to capture a higher multiple if their solar business grows larger. While it is certainly unlikely to be awarded a forward earnings multiple of 30+ like Enphase Energy (ENPH) or First Solar (FSLR), even a small increase in valuation multiple given by the market can lead to a large amount of upside for the shares given where they trade today.

We believe that this discount to the industrial sector and their closest public market peer is unwarranted and that Generac should trade more in line with the industrial sector as a whole. Generac has many tailwinds that remain intact and a lower debt load than many industrial companies, thus reducing risk. Generac has further valuation upside if their solar business can grow. A lot of bad news has already been priced into the stock.

Our personal outlook for revenue growth and net margins can be found below. We note that these estimates are conservative and Generac has the potential to meaningfully exceed our expectations, resulting in asymmetric upside.

UFD Capital

Negatives/Risks

The Pink Energy lawsuit could result in Generac being liable for damages. We are not lawyers so we won’t give an opinion on the merits of the lawsuit or what percentage chance each potential outcome has. From the standpoint of an investor seeking to mitigate risk, this lawsuit could have large financial implications for Generac with the potential for damages in the billions of dollars. In addition to these stiff financial penalties, an adverse outcome would also result in a large amount of reputational damage to their solar business.

The value of Generac is more skewed to their generator business than their solar business. For this reason, if the litigation results in an outcome that is bad for Generac it is likely that they will still be able to continue operating over the long term. That being said, this is a material risk and could send shares sharply lower if the outcome of this lawsuit is unfavorable. Investors in the name must understand that this legal risk could end up being substantial with Generac potentially liable for billions in damages, and that there is a non-zero probability that Generac could go bankrupt.

Some other potential risks for Generac include:

- The demand for generators could never pick back up, leading to Generac seeing stagnating or declining sales.

- Input and labor costs could remain high or even increase, further eating into Generac’s profit margins.

- The increased prevalence of electric vehicle bidirectional charging could cut into Generac’s sales.

- The solar business could never take off, resulting in a reduced multiple and a less diversified business.

Final Thoughts

In conclusion, investors should understand that an investment in Generac comes with baggage and risk. That being said, we believe the risk reward is favorable here, with a large amount of bad news priced into the stock and investor/analyst sentiment being highly pessimistic. Our intrinsic value estimate for Generac is 17.64x forward earnings to bring it more in line with the S&P 500 industrial sector. This $148.92 a share value represents a 57% increase from these levels.

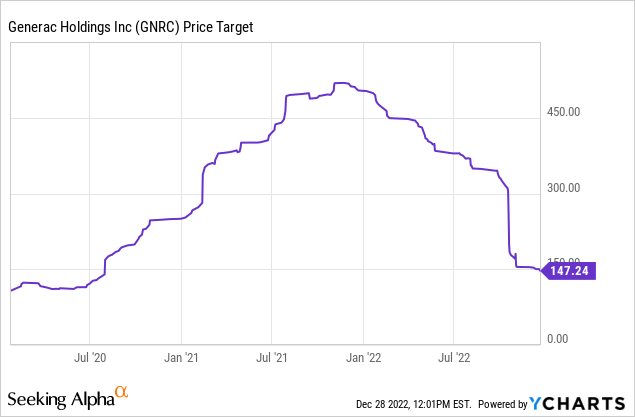

Analysts have an average price target of $147.24; however, many of these same analysts had price targets much higher a mere 12 months ago, so that doesn’t give us much comfort.

It appears the selloff in Generac has become overdone and we believe investors should take a look at the fundamentals and risks and come to their own conclusion. Negative sentiment and massive selloffs can result in great opportunities. It’s generally worth taking a closer look at these opportunities once the dust finally settles.

Be the first to comment