Black_Kira/iStock via Getty Images

Following a slew of major deals over the last month, FREYR Battery (NYSE:FREY), a development stage company in the midst of building out a lithium-ion battery manufacturing footprint globally, now boasts an impressive >130GWh order book focused on automotive mobility and energy storage. Near-term funding hurdles have also been cleared, with the recent share offering completed despite challenging market conditions. While the equity raise is near-term dilutive to existing shareholders, the stock price performance post-raise indicates investors are happy to underwrite the upside potential from FREY’s ambitious strategy.

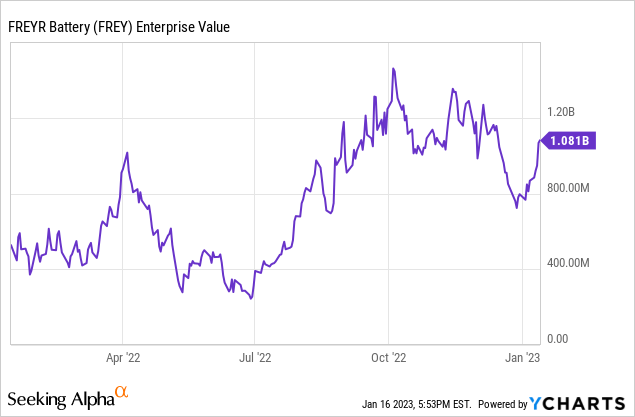

I agree with the optimistic view – there’s risk here, but FREY is attractively positioned, given its cost competitiveness in a high-growth battery market, to become a major lithium iron phosphate (LFP) battery producer. Relative to the >$1bn of revenue once its fully funded capacity is built out by FY24, as well as the potential to turn gross margin positive (helped by the inflation reduction act (IRA) subsidies) the following year, the current >$1bn enterprise value doesn’t seem that pricey. From here, the onus is on FREY’s execution, as production is due to ramp up at its Norway-based customer qualification plant [CQP] this quarter.

JP Research

Making Inroads into Mobility with First Offtake Agreement

Just last week, FREY announced a landmark offtake deal with commercial mobility player Impact Clean Power Technology for 10-14GWh of LFP battery cells. The supply agreement will cover Impact’s commercial vehicle, rail, and traditional power generation products over the FY25-FY30 period. Given its limited presence in mobility thus far, this is an important deal for FREY, marking the start of the company building out a major presence beyond the storage space. More importantly, it validates what management has been saying for a while now – that its LFP cells can penetrate the massive mobility addressable market as well. Building on FREY’s success in the storage space, this early success in the mobility segment points to more upside for the pace of LFP battery uptake, adding impetus to the long-term growth story.

Nidec JV Adds to the Upside Potential in Storage

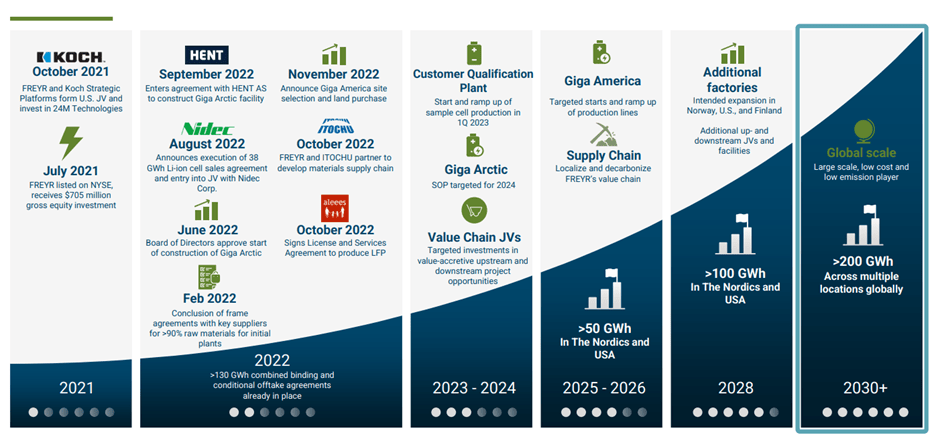

The offtake announcement comes on the heels of FREY forming a downstream joint venture for low environmental impact battery energy storage systems (BESS) with Japanese electric motor manufacturer Nidec (OTCPK:NJDCY). Per the initial terms, the JV ownership will comprise 66.7% for Nidec and 33.3% for FREY. By storing power generated from renewable energy sources in batteries to compensate for surpluses and shortages, BESS will play a crucial role in stabilizing supply on renewable power grids. The current target for JV production kickoff is FY25, with >8GWh of generation per year in FY27 and a further ramp-up to 12GWh of generation per year by FY30.

The deal economics is hard to gauge at this point, but given the battery module production will be integrated into FREYR’s Giga Arctic facility (scheduled to kick off in FY24), the capex outlay should be manageable. With target production amounts also tied to FREY’s Giga Arctic cell production, the planned >$127m investment by FY30 seems reasonable. Depending on whether the JV operates out of the future USA plant, which would grant it $10/kWh of battery module credits in addition to the $35/kWh for battery cell manufacturers (per the IRA), there could be even more savings in the long run as well. On the P&L side, building scale in BESS should be accretive to future margins – not only because of the outsized benefits from IRA grants but also the significantly higher retail pricing relative to plain battery cells.

Well-Capitalized After the Latest Share Offering

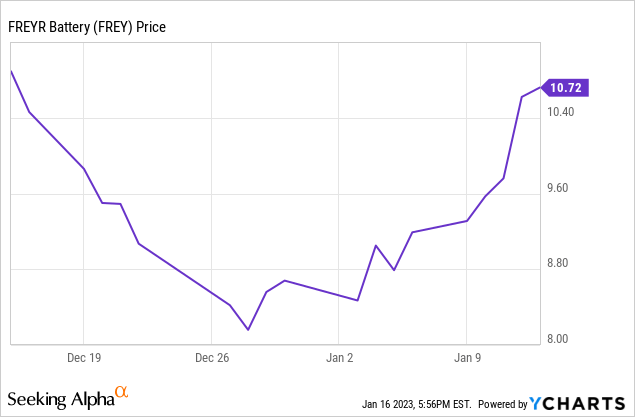

At this stage, dilution risks are limited – at least for another year or two. FREY has completed an equity raise, raising gross proceeds of $264.5m (net ~$251m after fees) for constructing its Giga Arctic production site and developing the US-based Giga Americans. As the ~23m share issuance entails ~20% of dilution to existing shareholders, the November selloff wasn’t surprising. The subsequent rally in the last month or so, however, indicates investor willingness to fund the ambitious long-term strategy – a key factor to the company hitting its LFP battery production targets of >50GWh by FY25 and >200GWh by FY30.

For new investors, the removal of the capital raise overhang presents a compelling entry point into the FREY growth story ahead of CQP production this quarter. From here, execution will be key to validating the viability of partner 24M’s battery technology and FREY’s competitiveness in LFP battery cell production.

FREYR Battery

Encouraging Progress on the Path to Cell Production

With the FREY order book now at new highs following the announcement of a first commercial offtake agreement with commercial mobility player Impact Clean Power, the company looks poised to emerge as a gigawatt-scale LFP battery producer over time. Given the addressable market opportunity of the battery market is massive, particularly in the automotive and storage space, investors seem open to funding FREY’s growth ambitions as well. The recent share offering is a case in point – despite the dilution, the stock has rallied over the last month or so, reflecting the upside potential offered by a well-capitalized FREY.

Going forward, the focus will shift to execution, with the company on track to ramp up production at its CQP this quarter; more details on the CQP progress should be available during the upcoming results next month. While FREY won’t be cash flow positive for a while, the FY24 capacity buildout is set to kickstart >$1bn of revenue generation, and helped by IRA subsidies, positive gross margins shouldn’t be far off. Relative to the growth potential, the current >$1bn enterprise value (>$600 net cash post-raise) seems very reasonable.

Be the first to comment