FeelPic

Freeport-McMoRan Inc. (NYSE:FCX) reported its Q4 earnings results recently, but its upward momentum has continued to stall at its January highs.

The company reported a double beat on revenue and adjusted EPS. However, buyers were unmoved, as they likely anticipated more from management.

Management is confident that the long-term secular drivers sustaining the physical demand for copper remain valid. Therefore, it should continue to spur buying support for FCX, as previous headwinds (forex, macro outlook, energy costs, inflation) that hampered its advance have weakened further.

Despite that, management highlighted that it expects higher average unit costs of $1.60 per pound for copper production in FY23, up from FY22’s $1.50 average. Moreover, it’s higher than FQ4’s $1.53 average, suggesting that Freeport-McMoRan continues to be impacted by inflationary pressures on its production base.

Management indicated several persistent cost challenges, such as: “higher electricity and coal costs, power requirements, equipment components, supply costs, and labor costs.”

Furthermore, management stressed that tight labor supply dynamics remain a concern in the US. The US accounted for 35% of Freeport-McMoRan’s FY22 copper production, coming in behind Indonesia’s 37% production base. As such, the structural challenges could persist in the medium term. Consequently, Freeport-McMoRan doesn’t expect to lift its FY23 production above FY22 levels.

Hence, FCX likely needs underlying copper futures (HG1:COM) prices to perform well in 2023 to sustain its revenue growth moving ahead.

Wall Street analysts’ estimates suggest that Freeport-McMoRan could report flattish revenue growth in FY23 (-0.1%), with adjusted EBITDA expected to rise by 1.2%.

Therefore, we believe that analysts have based their average forecasts in line with management’s outlook in 2023. As such, investors need to glean the price action in the futures market to assess whether there’s potential for outperformance.

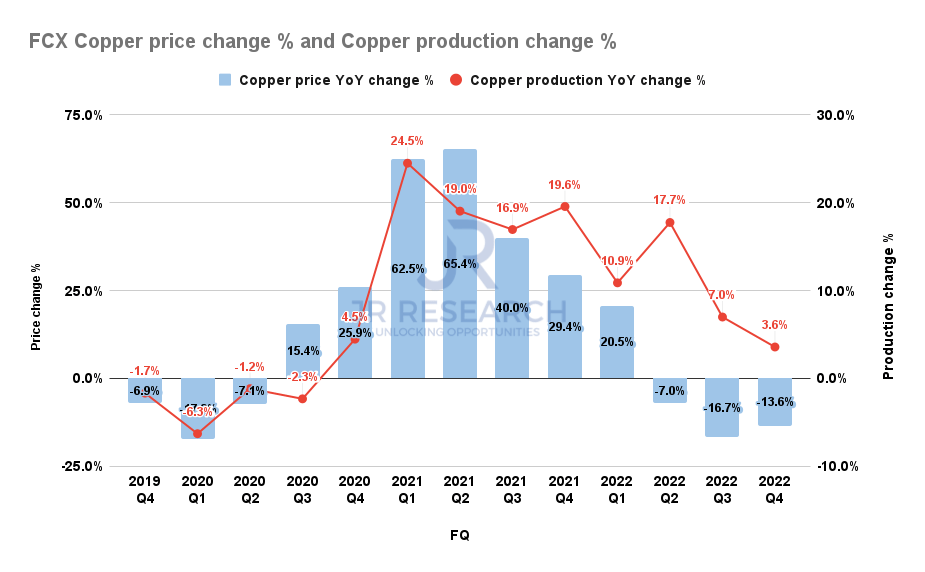

FCX copper price change % and production change % (Company filings)

As seen above, Freeport-McMoRan’s average realized price decline seems to have bottomed in Q3’22, even though average prices still fell 13.6% in Q4. However, the recovery in underlying futures prices helped FCX to lift its operating performance, bolstering its double beat in FQ4, as discussed earlier.

Could there be an opportunity for Freeport-McMoRan to lift its production outlook in the medium term? Possibly.

Management suggests that it’s still “taking advantage of technology advancements and opportunities to expand production from leaching at [a] low incremental cost.” As such, investors shouldn’t rule out the potential for production ramp as FCX tests out newer technologies to meet the world’s secular demand for copper as we continue to decarbonize.

Bloomberg reported that a record-breaking $1T was invested in decarbonizing energy in 2022, marking a significant increase of over $250B from the previous year. Hence, the critical underpinnings for Freeport-McMoRan as the US’ most significant copper producer are alive and well.

But, the critical question is whether the near- and medium-term upside has been captured relative to the production outlook telegraphed by management.

We gleaned that market sentiment over copper has switched from bearish to bullish, suggesting buyers have already piled into FCX. Moreover, China’s rapid reopening from its COVID lockdowns has also added to the recent bullish sentiments, spurring strategists to be increasingly optimistic.

So, we believe investors need to demonstrate patience now and not chase the recent surge.

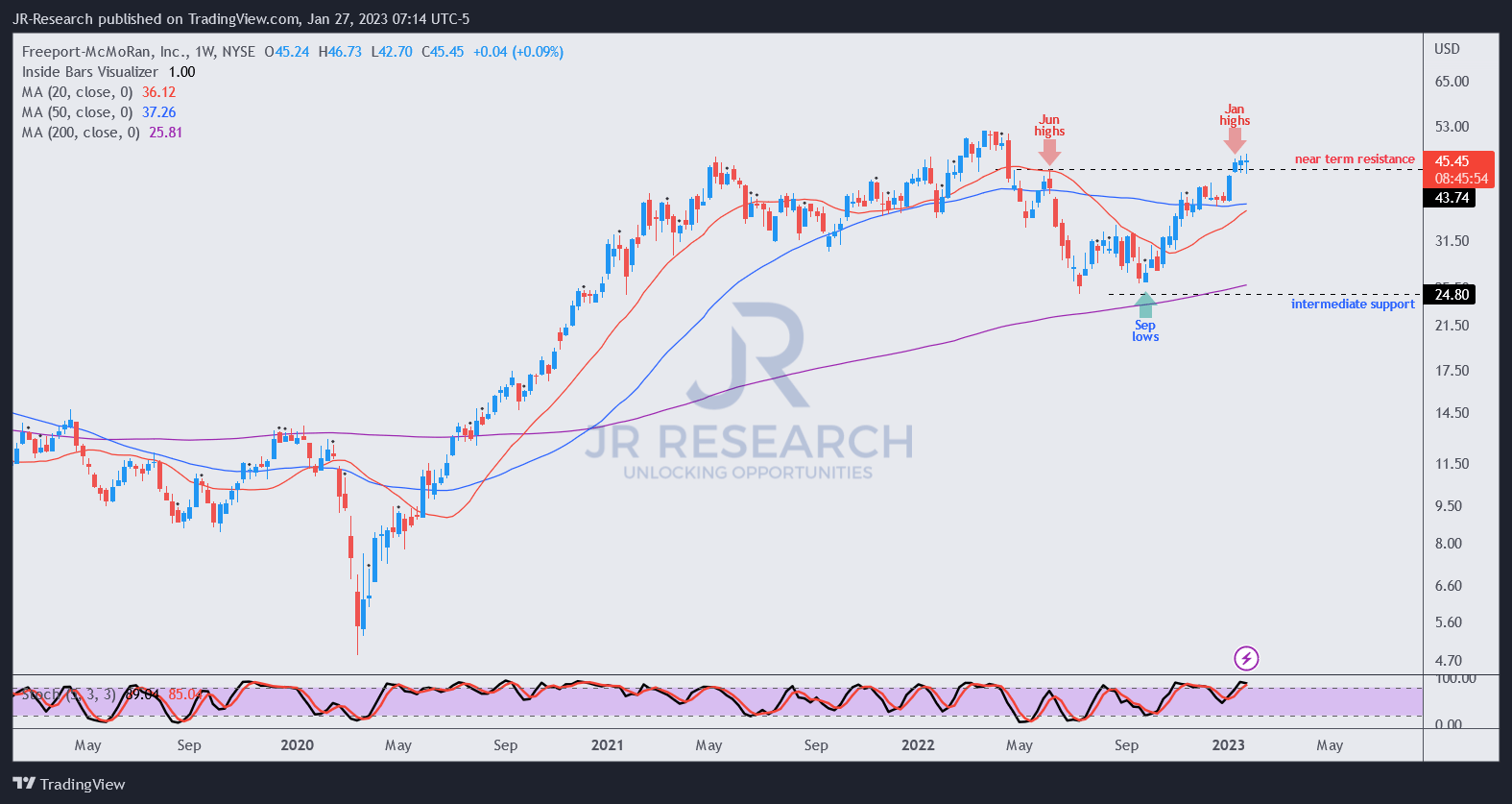

FCX price chart (weekly) (TradingView)

As seen above, FCX continues to hover around its January highs, predicated against the June 2022 top.

Does it mean it would not move higher to re-test its 2022 highs? Of course not. It could continue to grind up if greedy buyers continue to pile in to lift its momentum higher.

However, investor discipline is important, knowing that momentum and breadth indicators are already overbought. Sentiment has also turned strongly bullish, indicating caution should be heeded.

But, we are confident that FCX’s July and September 2022 lows will not likely be retaken if its price action can consolidate and stay above its 50-week moving average (blue line).

A deeper pullback would be constructive for investors still biding their time.

Rating: Hold (Reiterated, but on the watch for a rating change).

Be the first to comment