Araya Doheny

Logitech (NASDAQ:LOGI) is a leading hardware based technology company, which is well known for its range of webcams, and gaming accessories. The company recently reported pretty poor results for the third quarter of fiscal year 2023, as its revenue and earnings declined year over year. Although this may seem terrible, I believe this is mainly due to the cyclical demand in the gaming/PC market and thus it will not be the start of a long term trend. In addition, its stock is undervalued according to my valuation model and thus may be worth holding onto despite the poor news. In this post I’m going to break down its recent earnings release and dive into my valuation model, before reviewing the company risks. Let’s dive in.

Third Quarter Financials

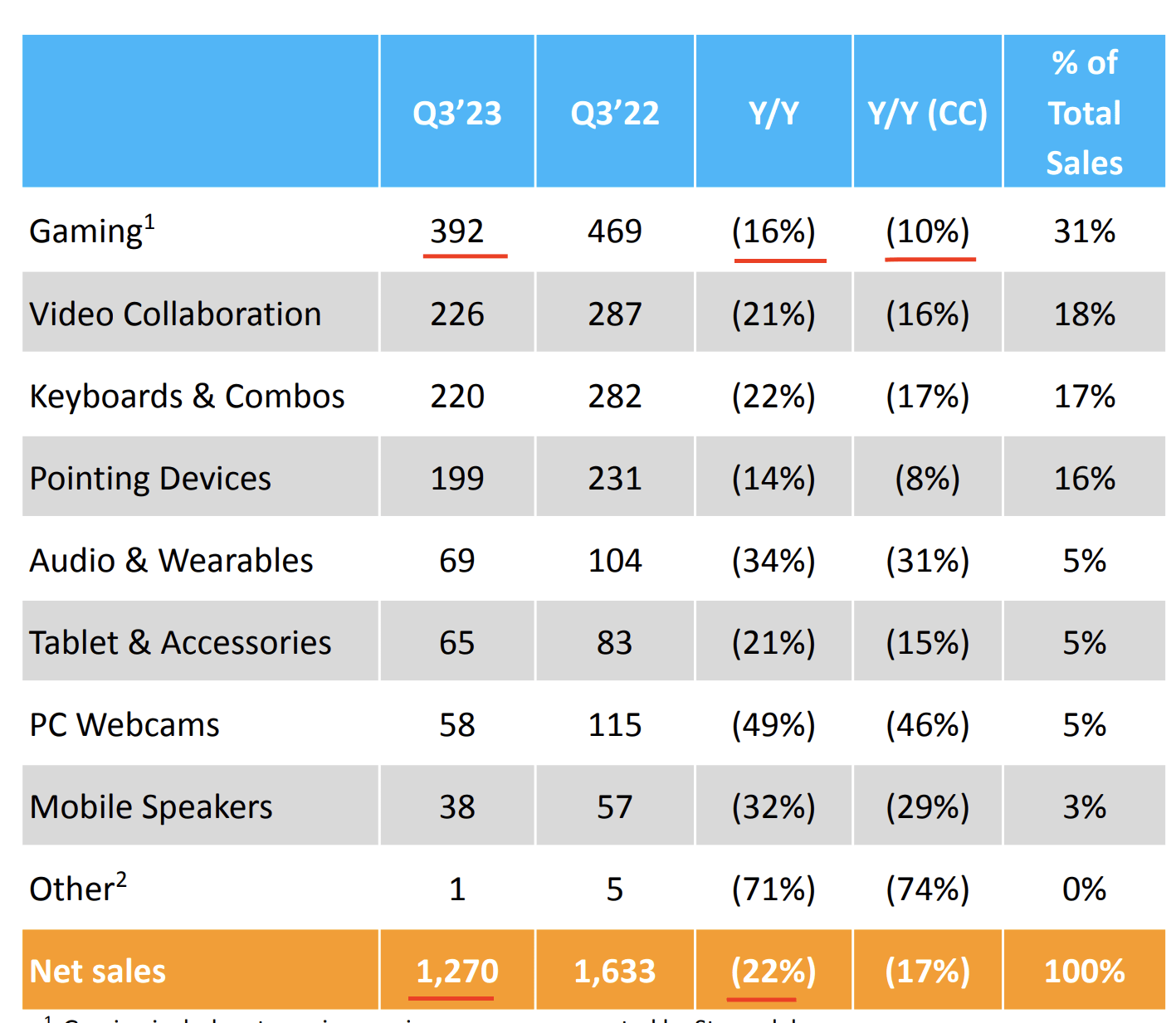

Logitech reported pretty poor financial results for the third quarter of the fiscal year 2023. Net sales was $1.27 billion, which missed analyst estimates by $50 million and declined by 22% year over year. Its international revenue was impacted by a strong U.S dollar, which caused foreign exchange headwinds. Therefore on a constant currency basis, net sales declined 17% year over year. Breaking revenue down by segment, Gaming products makes up the majority (31%) of total sales and reported a 16% revenue decline to $392 million. The gaming industry boomed in 2020, during the lockdown. However, since the “reopening” of the economy this market has suffered from suppressed demand. In my other posts on Microsoft and Nvidia, I reported similar dynamics in their gaming segments (Xbox and GPU’s), thus this is an industry wide dynamic. The positive for Logitech is that the gaming industry was valued at $195.65 billion in 2021 and is forecast to growth at a rapid 12.9% compounded annual growth rate [CAGR]. Therefore, long term I forecast this segment to grow again for Logitech, as a rising tide should effectively lift most boats.

Logitech stock (Q3,FY23 report)

Moving onto the other segments, Video Collaboration is the second largest segment (18% of sales) and reported sales of $226 million, down 21% year over year. A positive for this segment is quarter over quarter it achieved growth of 7%. Video conference room cameras and peripherals, also increased by close to 30% year over year. This was offset slightly by webcams, which were down by 30% year over year, despite being three times greater than pre pandemic levels. Since the lockdown of 2020, there has been an industry wide shift towards remote working and remote friendly conference rooms. This of course caused major purchases for webcams in 2020. However, logically speaking as many people will have now purchased a webcam, the demand will likely less, this is a simple correction in demand. The positive is Logitech is still considered to be a leader on many review websites, which rank Logitech as number one for its classic C920 webcam. In addition, the company looks to have the greatest range of webcams relative to competitors. Its alternative camera models, also appear in the number two spot, six, nine and ten.

Moving onto Logitech’s third largest business segment (Keyboards & Combos). This segment reported $220 million in net sales which declined by 17% on a constant currency basis. I again checked out multiple review websites and discovered Logitech is a highly rated player in this market. It has the number one spot on Tech Radar, and has a models rated as the “best upper mid range” and best “cheap” keyboards on another review website. Therefore I would deem that this segment is also experiencing some cyclical demand headwinds. However, I would caveat this with a disclaimer that they keyboard industry is more competitive and more of a commodity product in my eyes. I will discuss this more in the “Risks” section. Logitech’s other segments which included Pointing devices, to accessories also showed a similar dynamic.

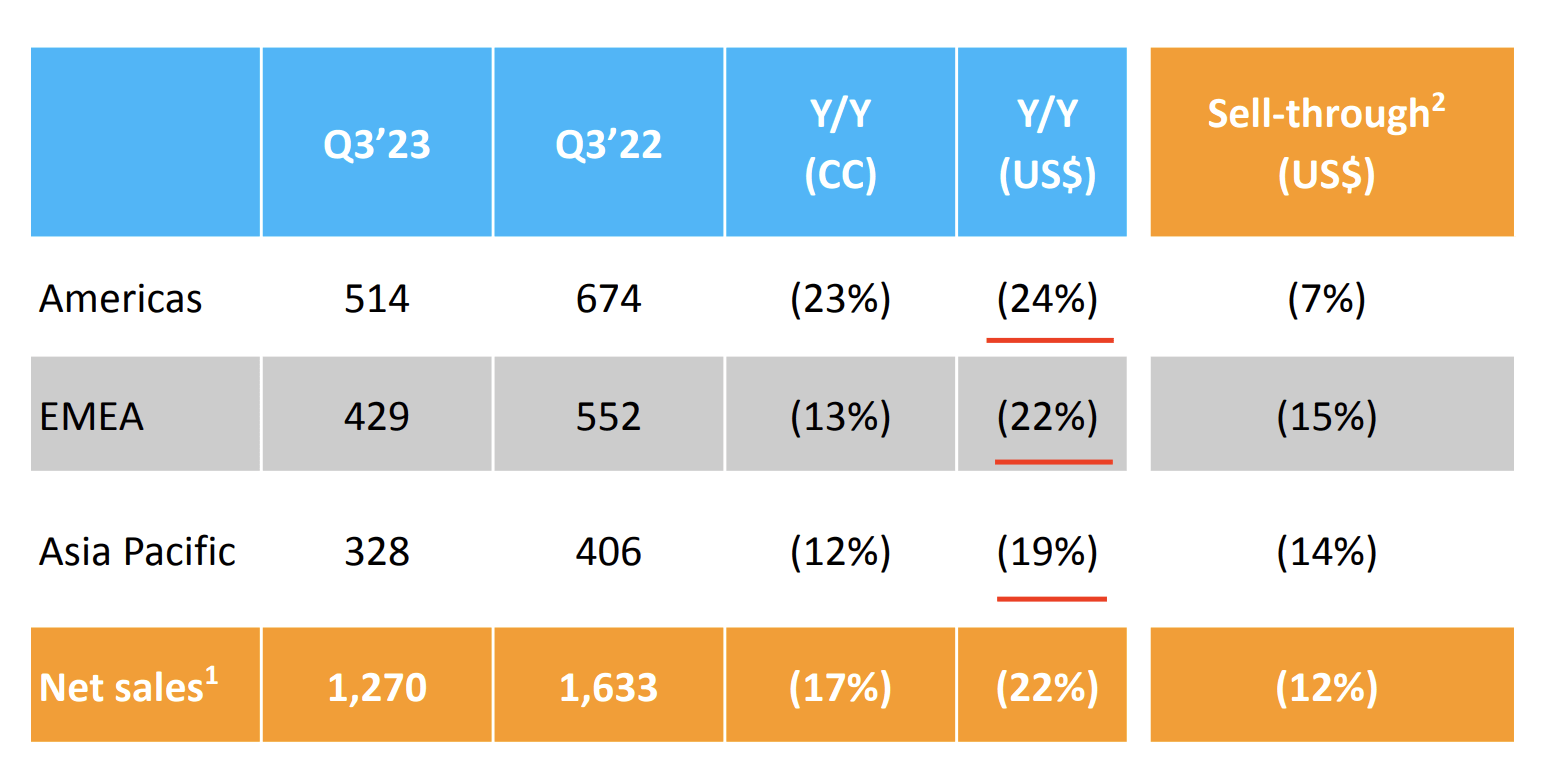

Analysing the sales by region, the Americas reported $514 million in revenue which declined by 24% year over year. EMEA also reported a decline of 13% year over year, on a constant currency basis. As did the Asia Pacific region, which declined by 19% year over year to $328 million. A positive for Logitech is its revenue is highly diversified internationally, which makes the company less prone to a downturn in a specific market. In this case, it is clear the demand adjustment is a global issue.

Logitech by region (Q3,FY23 report)

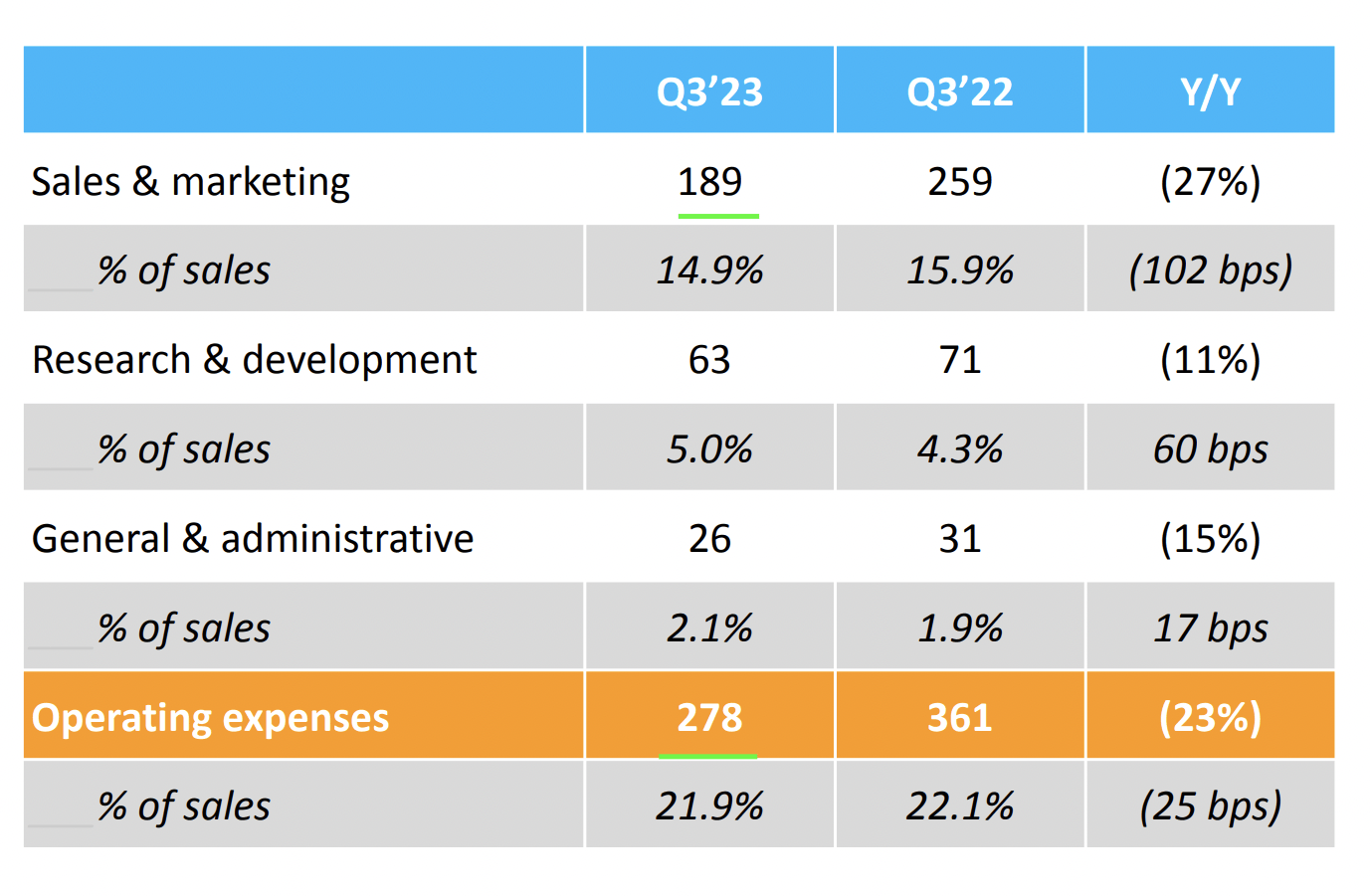

Moving onto profitability, Logitech reported a gross margin of 37.9%, which was down slightly year over year. This was driven by foreign exchange rate headwinds, as-well as a “promotional environment” and cost inflation which squeezed margins. The positive is Logitech has reduced its Sales & Marketing expenses by 27% year over year to $189 million, in order to adjust to the market which has lower demand. The business also scaled back its R&D expenses by 11%. While its G&A expenses naturally fell with lower sales.

Logitech (Q3,FY23)

The business reported operating income of $204 million, which declined by 32% year over year. Moving forward the company has stated a tepid outlook for the full fiscal year of 2023, with negative 13% to 15% expected, on a constant currency basis.

The company has a solid balance sheet with $1.036 billion in cash and short term investments. In addition, to minimal debt of ~$79.9 million. Management bought back $90 million worth of shares in the quarter which was a positive sign.

Advanced Valuation

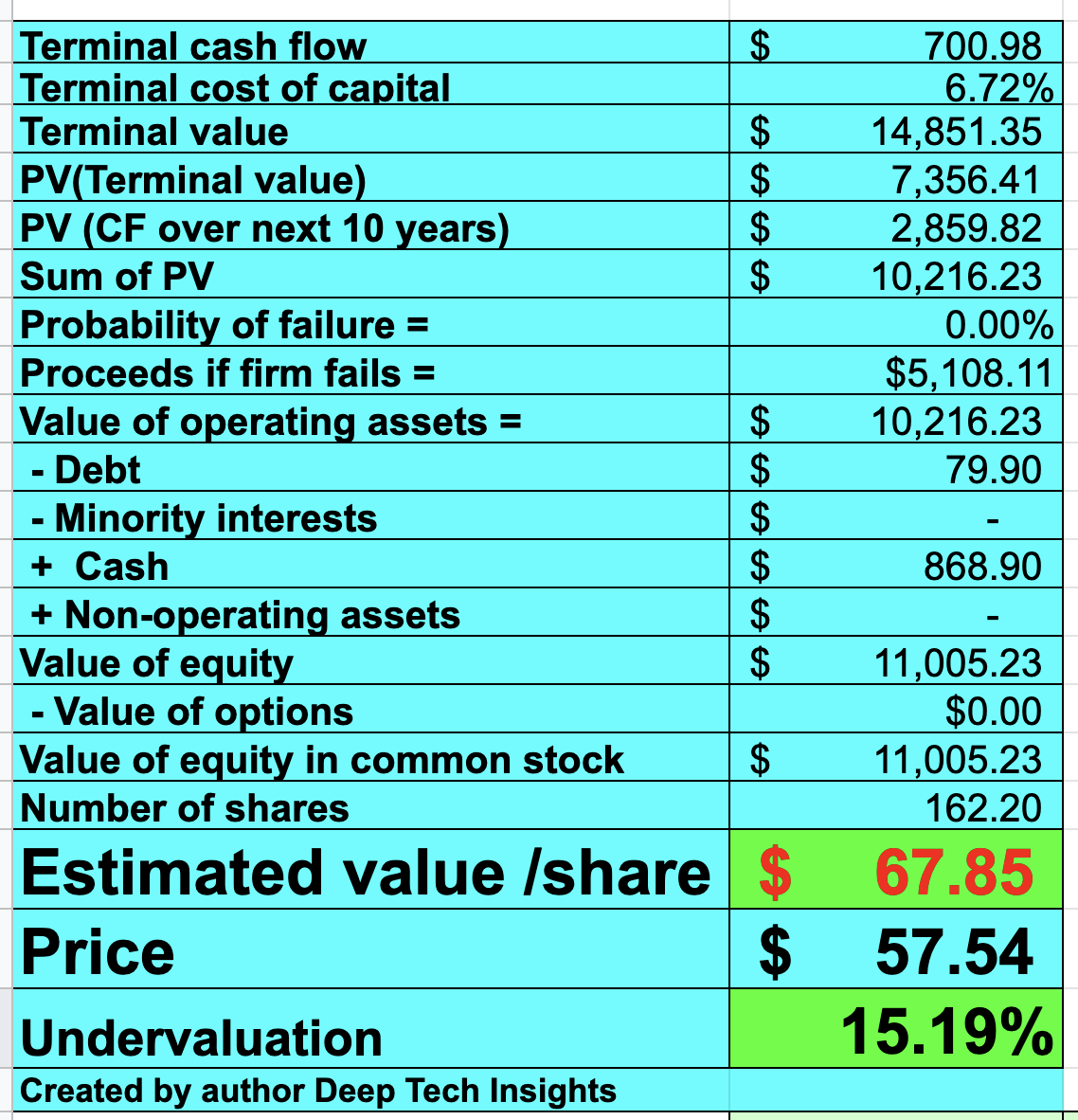

In order to value Logitech I have plugged its latest financials into my discounted cash flow valuation model. I have forecast negative 10% growth for “next year”, which I expect to be driven by continued lower demand and the forecasted recession. However, in years 2 to 5, I have forecast a cyclical rebound in demand, due to the underlying secular growth forecasted in industries such as gaming. In addition, to the continued adoption of remote and hybrid working strategies.

Logitech stock valuation 1 (created by author Deep Tech Insights)

To increase the accuracy of the valuation model, I have capitalised R&D expenses which has lifted net income. In addition, I have forecast a pre tax operating margin of 16% over the next 8 years.

Logitech stock valuation 2 (created by author Deep Tech Insights)

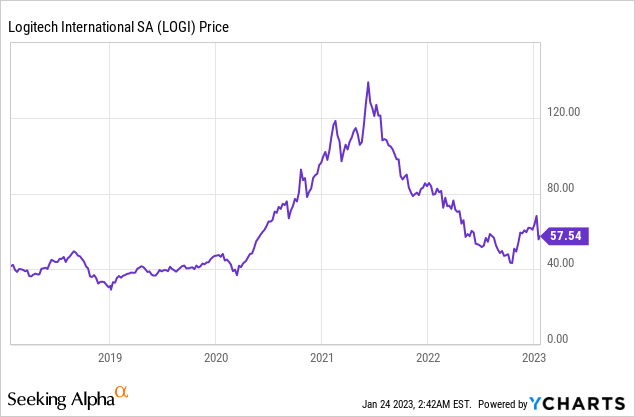

Given these factors I model a fair value of $67/share. With the stock trading at ~$57/share I estimate a 15% undervaluation..

As an extra datapoint, Logitech trades at a price to earnings ratio = 22x, which is 13% cheaper than its 5 year average.

Risks

Recession/Competition

Many analysts have forecast a recession for 2023, therefore I will expect continued lower demand for Logitech’s products. In addition, I don’t believe the company has a strong moat around its business as there are many companies which offer similar products. In gaming, we have companies such as Corsair (CRSR) and then in webcams we have El Gato, Sony, etc.

Final Thoughts

Logitech is a leading provider of electronic devices which have benefited from the market shift in demand since the pandemic. The world has become more “digitised” and Logitech is poised to benefit from these long term trends. Its business is facing a number of industry headwinds, which has impacted sales considerably. The positive is the stock is undervalued and thus for existing investors I will label the stock as a “hold”. In my personal investment strategy I like to invest into businesses with a strong competitive advantage. In this case, I believe Logitech’s products are close to a commodity and thus this could be an issue long term.

Be the first to comment