hapabapa

Beginning in 2020, the effects of the pandemic caused significant shortages of semiconductor chips which affected companies like Foxconn Technology Co. (OTCPK:FXCOF), a Taiwanese manufacturer of chips. A surge in demand for laptops and PCs in 2020 coupled with the growing electronic vehicle market added to the crunch, and East Asian manufacturers simply couldn’t keep up with the demand, especially in light of their own logistical issues such as periodic shutdowns and quarantines. Predictably, the chip shortage caused a surge in used car prices and other electronics, as the supply of new products with semiconductor chips became stressed.

Global economic conditions were unstable between 2020 and 2021, as regulations and measures meant to combat Covid alternated between lockdowns and re-openings. As lockdowns occurred, economic activity slowed worldwide, and as lockdowns were lifted, a surge in spending stimulated the economy. This trend alternated throughout 2020 and 2021, and again in 2022. Although economic growth has resumed due to the ease of lockdowns combined with fiscal and monetary policy and stimuli from world governments, the global economic forecast for computer chips is less clear. Trade relations between the US and China, the Fed’s downsizing of its balance sheet, and high oil prices will continue to determine economic trends going forward, but Foxconn is in a position to continue its trajectory of growth in 2023.

Taiwan benefited from conditions set forth by a world engrossed in the pandemic. Strong demand for semiconductor chips allowed the country to achieve high levels of exports, while its domestic demand remained high throughout the pandemic.

Current Production Outlets

Foxconn is heavily involved in the production and distribution of consumer electronics and has a dominant market position in several economic spheres. Taiwanese manufacturers currently dominate the market for notebooks, with some Japanese and American firms having a minority market share. Taiwanese manufacturers also have roughly 60% market share in the production of smartphones, followed by about 15% US manufacturers, and then the remainder going to China and others. Lastly, Taiwan dominates the production of tablets, with very little market share going to US or Chinese makers.

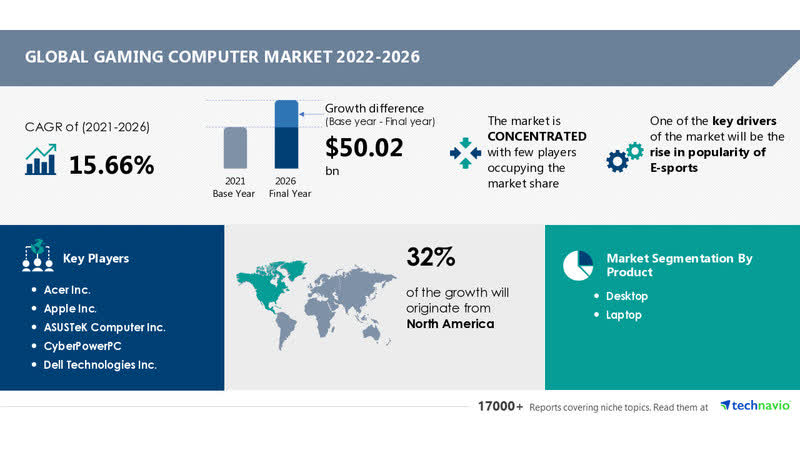

Consumer demand for these products is consistently high and received a huge boost due to the Covid pandemic. The market for gaming PCs, for example, remains particularly strong:

prnewswire.com

There also remains a robust demand for Apple (AAPL) products, particularly the latest iPhone model. According to UBS analysis, lead time for the iPhone 14 is increasing, indicating that demand far exceeds apple’s ability to supply the market. The lead time measures how many days it requires for a particular product to reach the consumer. Higher lead times indicate stronger demand (barring issues related to material inputs) while lower lead times occur when demand for a product falters. The lead time for Apple’s latest iPhone14 is increasing as the company sells more units than expected, with the iPhone14 eclipsing the iPhone 13 in year-over-year sales.

Recent Difficulties

China’s “zero-Covid” policy created troubles for Foxconn, as an increasing number of Covid cases in China prompted mass lockdowns and quarantines. Foxconn has many manufacturing centers located in mainland China, including the one located in Zhengzhou, a leading assembly plant for Apple products. The company reported US $18 billion in revenue for the month of November, down significantly from October. The company has posted month-over-month revenue growth consistently for more than a decade until November of last year. Harsh lockdowns and backlash from ordinary Chinese citizens, including workers at the plant, caused a dramatic decrease in output. The company is confident though, that the worst is behind it.

Due to popular backlash, China relaxed its “zero-Covid” policies, and production in Foxconn’s facilities is returning to normal levels. To address its staffing issues, Foxconn offered cash bonuses to workers and new hires, and it seems to have had the desired effect. December output reached about 90% of the company’s goal, and they are expecting full production to resume this month. With the difficulties behind them, it is time to begin reviewing Foxconn’s segments of growth by looking into their new development initiatives.

Electric Vehicles

Foxconn has long dominated the production of Apple’s iPhones, as well as supplied electronics for gaming PCs and medical devices, but the company is also looking to expand into the market for electric vehicles. In 2023, Foxconn is going to embark on a new initiative to greatly expand into the production of electric vehicles, an underexploited market segment that has seen tremendous growth in recent years. All of the major car manufacturers are shifting resources to boost production in electric vehicles, and Foxconn stands to gain from this market shift.

Deloitte

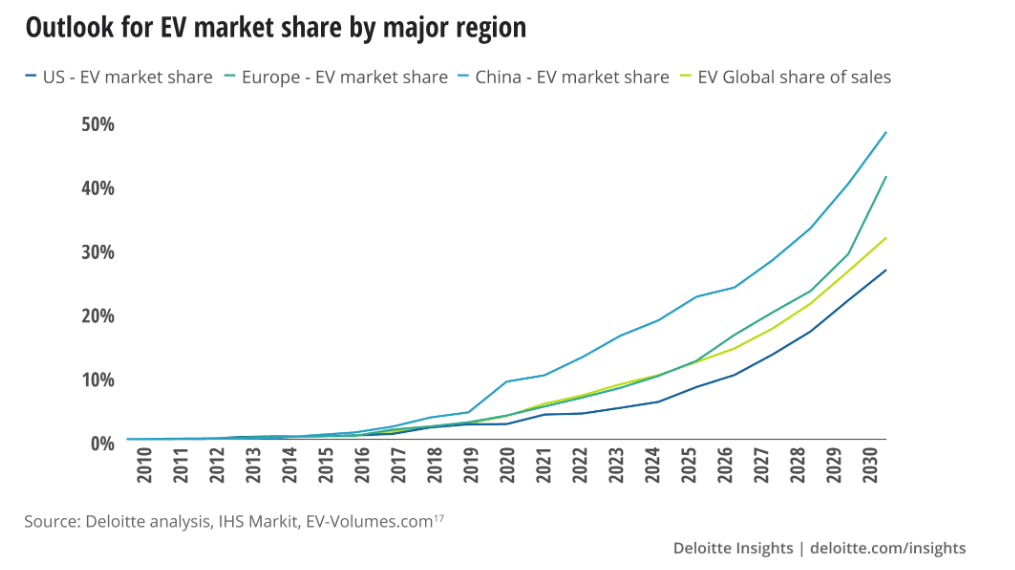

Electronic vehicle sales have surged over the last three years, and the trend is expected to continue. Foxconn is preparing itself to enter this market sector by devising new strategic partnerships that will allow it to produce and supply electric cars with the chips and batteries they require.

Foxconn chairman Liu Young-way is optimistic that this is the right path for the company, and he expects to vigorously pursue growth in this field. He expects partnerships with leading automakers to produce computer chips in Indonesia, Thailand, Saudi Arabia, the US, and elsewhere. Liu’s forecasts are ambitious, as he wants to capture at least 5% of the global electric vehicle market to generate up to USD 32.6 billion in revenue on an annual basis, representing approximately 15% of Foxconn’s forecasted top line.

The transition will not be easy, but it will be necessary for Foxconn to achieve the growth rates that make the stock an attractive investment at its current levels. Foxconn’s current business model of smartphone production relies on the industrial centers it owns in mainland China, but the logistical ease of producing and transporting smartphones and other small electronics will need to be revisited in order to shift towards electric vehicle production. Foxconn will have to reinvent itself through strategic partnerships in order to achieve its electric vehicle goals. Fortunately, some of those partnerships are already in place.

The company has already partnered with firms in Thailand to handle the Southeast Asia market, and it has also partnered with Lordstown Motors (RIDE) in the United States, which produces electric pickup trucks. The company has additional ambitions to partner with Tesla (TSLA), though it remains to be seen if anything substantial occurs.

Foxconn has already made great strides in the electric vehicle space, having already unveiled a few prototype vehicles in October of last year, and there are talks of additional partnerships with Volkswagen to build a new electric SUV.

Aside from some of the larger players, Foxconn intends to partner with smaller startup firms that are in the business of making electric vehicles but do not yet have the capital or the infrastructure in place for mass production, and Foxconn is looking into ways of partnering with those firms to provide that infrastructure.

Conclusion

The future is looking good for Foxconn. Having recently overcome the difficulties associated with strict Covid lockdowns in China, production of iPhone units will resume at full capacity. And while Foxconn’s production of iPhones gives it a lucrative cash stream, the true growth is going to come from electric vehicles. The current business model of producing consumer electronics will equip Foxconn with the cash necessary to sustain itself while it makes the necessary transitions, and the strategic partnerships that are both already in place as well as the ones that are currently being negotiated will ensure that Foxconn has plenty to do in the coming years as it pertains to electric vehicles.

Foxconn’s stock price currently represents the company’s capacity to produce iPhones and other electronics. The explosive growth the company will experience over the next 2-3 years is not priced in, and the company is a solid buy at these levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment