cagkansayin

Highlights

- Fixed income funds realized a return of positive 2.82% on average during the fourth quarter of 2022. This was the first positive quarterly performance for fixed income funds of the year and the largest quarterly return since Q2 2020.

- Taxable bond funds (+2.65%) underperformed tax-exempt bond funds (+3.31%) in quarterly performance for the second time in the last three quarters.

- Of the 51 Lipper fixed income classifications, 49 ended the quarter with plus-side quarterly returns. In each of the first two quarters of 2022, all 51 classifications realized sub-zero performance. In the third quarter, 48 posted a loss.

- Our top three Lipper classifications over the quarter were Emerging Markets Local Currency Debt Funds (+8.57%), Emerging Markets Hard Currency Debt Funds (+8.47%), and International Income Funds (+5.55%).

- The worst-performing classifications on average were Alternative Currency Strategies Funds (-1.33%), General U.S. Treasury Funds (-0.14%), and Short U.S. Government Funds (+0.55%.)

Fixed Income Funds Suffer Worst Year on Record, Despite a Strong Fourth Quarter

Executive Summary

Fixed income funds realized a return of positive 2.82% on average during the fourth quarter of 2022. This was the first positive quarterly performance for fixed income funds of the year and the largest quarterly return since Q2 2020.

Taxable bond funds (+2.65%) underperformed tax-exempt bond funds (+3.31%) in quarterly performance for the second time in the last three quarters.

The fourth quarter of 2022 saw fixed income performance rebound from what has been one of the worst-performing years on record. The Bloomberg U.S. Aggregate Bond Index (+1.87%), Bloomberg U.S. Corporate IG Grade TR Index (+3.63%), Bloomberg Municipal Bond TR Index (+4.10%), and Bloomberg U.S. Corporate HY TR Index (+4.93%) all realized strong gains during Q4 while ending three straight quarters of sub-zero returns.

A nice end to the year still cannot hide the abysmal first three quarters. Looking back at returns dating back to 1976, the Bbg U.S. Aggregate Bond Index (-13.01%) and Bbg U.S. Corporate IG Grade Index (-15.76%) both set records in 2022 for worst-performing calendar years. The Bbg Municipal Bond Index (-8.53%) fell by its largest percentage since 1981, while the Bbg U.S. Corporate HY Index (-10.26%) realized its lowest return since 2008.

Why the poor performance? Well, the simple answer is when interest rates rise, bond prices fall. During 2022, the Federal Reserve raised rates a total of seven times, including four straight increases of 75 basis points (bps), moving the interest rate range from 0% to 0.25% up to 4.25% to 4.50%-a 15-year high. Fed officials are not expected to stop there, the majority of members still have interest rates forecasted over 5.0% in 2023.

Federal Reserve President of Minneapolis Neel Kashkari wrote, “Wherever that end point is, we won’t immediately know if it is high enough to bring inflation back down to 2% in a reasonable period of time…Any sign of slow progress that keeps inflation elevated for longer will warrant, in my view, taking the policy rate potentially much higher.”

Market consensus is now factoring in a recession starting in 2023, which has caused market volatility and uncertainty. Money market funds have seen more inflows during December (+$54.1 billion) than any other month this year. Some of that may be for tax loss harvesting reasons, but even so, December’s 2022 intake would be the fourth largest monthly inflow over the last 31 months. The Fed’s primary concern right now is slowing inflation and has repeatedly noted it will attempt to do so no matter the collateral economic damage.

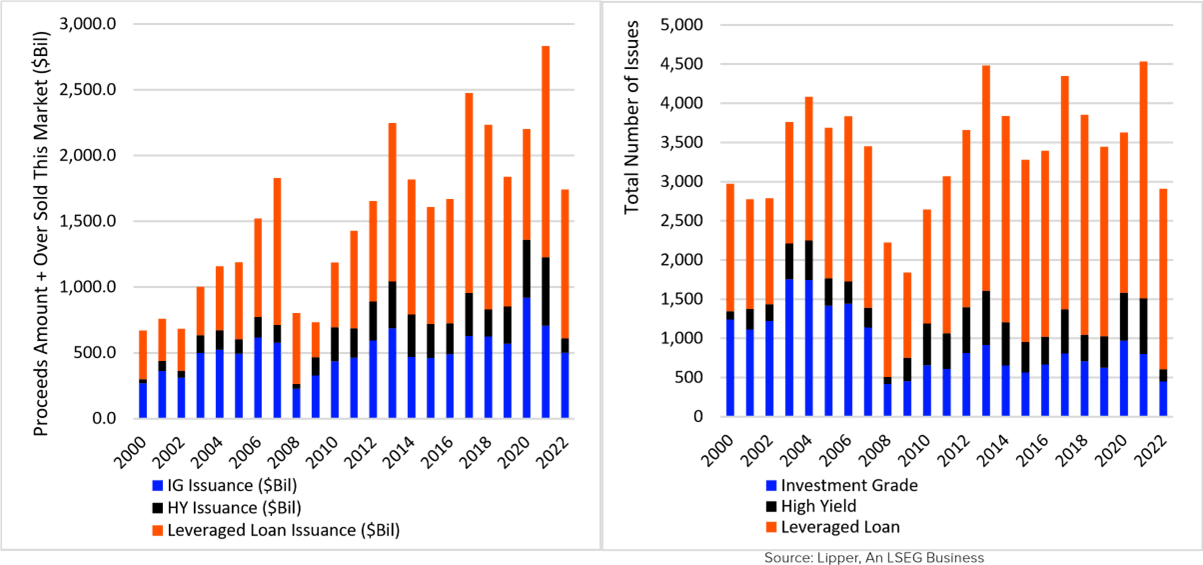

Forecasts aside, what does the data tell us? In terms of debt issuance in 2022, U.S. high yield debt was issued at the lowest volume ($109.3 billion) since 2009 and the lowest total issue amount (156) since 2008. Investment Grade Debt issuance in the U.S. fell to around 2016 levels, $501.7 billion, but the total number of issues (451) was the lowest level since 2008. It’s no surprise that with interest rates rising, firms are holding back on raising capital. With firms cutting back on capital expenditures paired with the recent layoffs brought on by technology and finance companies, economic activity is inevitably going to slow next year, if not already.

As the newly issued debt market dries up and future interest rate hikes expect to slow, fixed income investors look towards debt already in circulation-debt that has seen prices fall due to the 2022 interest rate increases.

Figure 1: Proceeds Amount and Total Debt Issuance per Year

Inflation is and has always been the arch-nemesis of fixed income securities. Those believing inflation has already been tamed by the actions of the Fed have bought back into both credit and long-duration risk. Looking at Q4 flows, Lipper Core Bond funds saw $18.4 billion of inflows in Q4 after posting $27.4 billion of outflows in the first half. Lipper High Yield funds (+$7.8 billion) and Lipper Corporate Debt BBB-Rated funds (+$7.1 billion) both recorded their largest inflows of the year in the fourth quarter. Lipper High Yield funds suffered $50.5 billion in outflows throughout the first three quarters of 2022. Investors in Lipper High Yield funds were rewarded as the classification reported the seventh-largest quarterly performance of all fixed income classifications.

Of the 51 Lipper fixed income classifications, 49 ended the quarter with plus-side quarterly returns. In each of the first two quarters of 2022, all 51 classifications realized sub-zero performance. In the third quarter, 48 posted a loss. All 51 classifications improved on their quarterly returns in the final quarter of 2022.

The top performing Lipper classifications over the course of Q4 were Emerging Markets Local Currency Debt Funds (+8.57%), Emerging Markets Hard Currency Debt Funds (+8.47%), International Income Funds (+5.55%), Global High Yield Funds (+4.58%), and California Municipal Debt Funds (+4.21%).

Alternative Currency Strategies Funds (-1.33%), General U.S. Treasury Funds (-0.14%), Short U.S. Government Funds (+0.55%), General U.S. Government Funds (+0.62%), and Short-Intermediate U.S. Government Funds (+0.66%) closed the quarter as the worst-performing classifications.

Lipper’s 51 fixed income classifications each fall under one of the eight fixed income macro groups. All eight macro-groups reported gains during the quarter for the first time since Q1 2021. The top three macro-groups during Q4 were World Taxable Fixed Income Funds (+6.08%), Short-Term/ Intermediate Corporate Fixed Income Funds (+3.69%), and Single State Municipal Debt Funds (+3.39%).

World Fixed Income Funds Summary

World Fixed Income Funds also rebounded in Q4 2022. Their gain of 6.08% led them to be the top-performing macro-groups while ending a five-quarter skid of negative returns. The last time World Fixed Income Funds outperformed the other seven macro-groups was in Q4 2020.

The top four gainers of all fixed income Lipper classifications fell under this macro-group: Emerging Markets Local Currency Debt Funds (+8.57%), Emerging Markets Hard Currency Debt Funds (+8.47%), International Income Funds (+5.55%), and Global High Yield Funds (+4.58%). This was the largest quarterly return for both the local and hard currency debt funds since Q4 and Q2 of 2020, respectively. International Income Funds ended a five-quarter stretch of negative returns while realizing their largest quarterly gain since Q3 2010.

The only other classification under this macro-group is Global Income Funds (+3.60%), which still finished fifteenth out of the 51 fixed income classifications. Global Income Funds also ended five straight quarters of negative returns while logging their largest gain since Q4 2020.

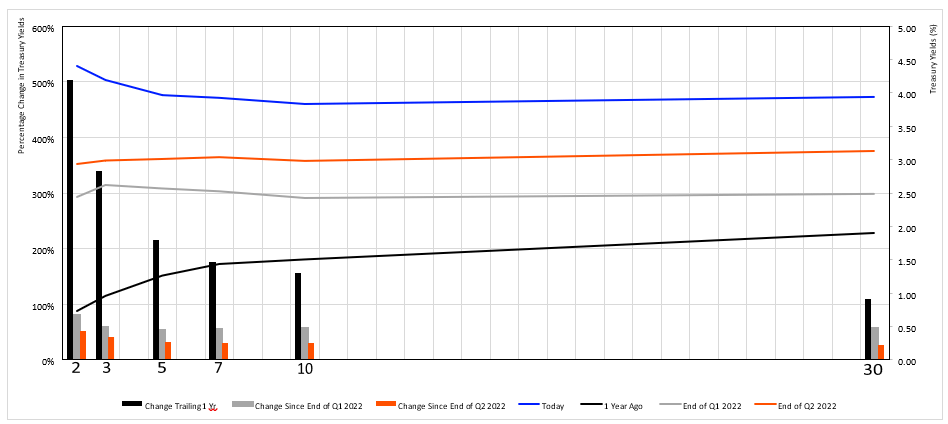

Figure 2: Treasury Yield Curve: Movement Over the Past Year

Source: Lipper, An LSEG Business

Government/Treasury Funds Summary

The treasury yield curve ended the year with an inverted 10-two yield spread in 129 straight daily sessions. During the past three months, both the two- and 30-year treasury yields increased by more than 4.60%, while the five- and seven-year yields fell 1.91% and 0.56%, respectively. The 10-two treasury yield spread fell from positive 0.05 to negative 0.57 since the end of the second quarter. Over the past year, the two-year treasury yield increased 501.50% while the 30-year only rose 108.47%.

The government/treasury funds macro-group posted a positive 1.16% return on average over the quarter, marking the first quarter in the black this year and the thirteenth positive quarterly performance over the previous 17 quarters. Q4 2022 was this macro-group’s best-performing quarter since q2 2021. government/treasury funds were the worst-performing macro-group for the second straight quarter.

The top three Lipper classifications under government/treasury funds were inflation protected bond funds (+1.97%), GNMA Funds (+1.36%), and U.S. Mortgage Funds (+1.19%). Inflation Protected Bond Funds ended three straight quarters of negative returns, while GNMA posted their first positive gain in seven quarters and the largest since the first quarter of 2020.

The worst-performing classifications under this macro-group were general U.S. Treasury Funds (-0.14%), short U.S. government funds (+0.55%), and general U.S. Government Funds (+0.62%). General U.S. Treasury Funds have been the worst-performing classification under the macro group each quarter this year. On a positive note, the classification realized the largest quarter-over-quarter improvement (+6.70%). short U.S.

Government funds have ended a streak of seven quarters of negative performance as they recorded their largest quarterly gain since Q2 2020.

General Domestic Taxable Bond Funds Summary

As a macro-group, General Domestic Taxable Fixed Income Bond Funds finished the quarter returning a positive 2.86%, which ends their streak of three straight quarters in the red. Q4 was the largest gain since the fourth quarter of 2020 for the macro-group.

Lipper High Yield Funds (+3.93%), Corporate Debt BBB-Rated Funds (+2.85%), and Multi-Sector Income Funds (+2.54%) were the leading classifications under General Domestic Taxable Bond Funds. Both High Yield Funds and Corporate Debt BBB-Rated Funds reported their first gain this year, while the last positive quarterly return for Multi-Sector Income Funds was in Q3 2021. The last time Lipper High Yield Funds led the macro-group was in Q4 2020.

Lipper Specialty Fixed Income Funds (+0.78%), Flexible Income Funds (+1.98%), and General Bond Funds (+2.00%) were the lowest-performing classifications of the macro-group. Despite being the laggard of the group, Specialty Fixed Income Funds are the breadwinner for the year (+2.23%) under this macro-group and still realized their largest quarterly performance since Q1 2021. The last time each classification in the macro-group posted positive gains was in Q2 2021.

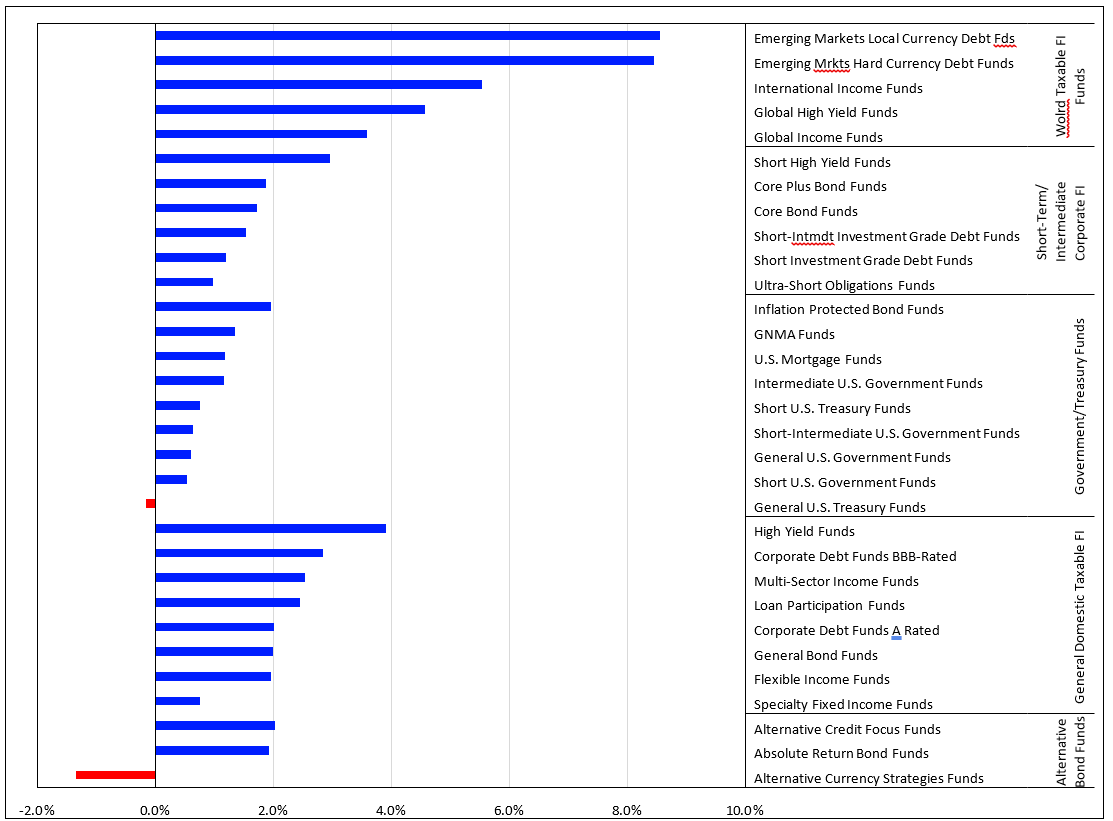

Figure 3: Q4 2022 Taxable Fixed Income Performance (%)

Source: Lipper, An LSEG Business

Short-Term Intermediate Corporate Bond Funds Summary

Short-Term Intermediate Corporate Bond funds finished the fourth quarter with positive quarterly performance (+1.60%), their first gain in the last five quarters. Despite being the third lowest returning macro-group, Short-Term Intermediate Corporate Bond Funds realized their largest quarterly return since Q2 2021. Each Lipper classification under the macro-group witnessed plus-side returns over the last three months, marking the first time since Q3 2021.

The top performing Lipper classification in this macro-group was Short High Yield Funds (+2.98%), realizing their largest quarterly return since Q4 2020. This classification was only one of two to record gains in Q3 as well. Short High Yield Funds recorded the second largest year-to-date return under this macro group (-4.61%). Following Short High Yield Funds are Core Plus Bonds (+1.89%) and Core Bond Funds (+1.74%). These latter two classifications were the two worst-performing classifications just last quarter, possibly signaling a shift in investor preference toward corporate credit.

At the bottom of this macro-group during Q4 were Ultra-Short Obligations Funds (+0.99%), Short Investment Grade Debt Funds (+1.22%), and Short-Intermediate Investment Grade Debt Funds (+1.54%). Both Short and Short-Intermediate Investment Grade Debt Funds have not posted a gain since Q3 2021. Short Investment Grade Debt Funds (-4.32%) led the macro-group in year-to-date performance as investors started the year favoring shorter-duration funds, signaling another shift toward longer-dated debt. Ultra-Short Obligations Funds reported their back-to-back quarters in the black and their largest return since Q2 2020.

Municipal Debt Funds Summary

Municipal debt funds recorded an average gain of 3.39% in the fourth quarter of 2022-marking their first quarterly gain of the year. All 21 municipal debt funds Lipper classifications reported positive quarterly performance for the first time since Q2 2021.

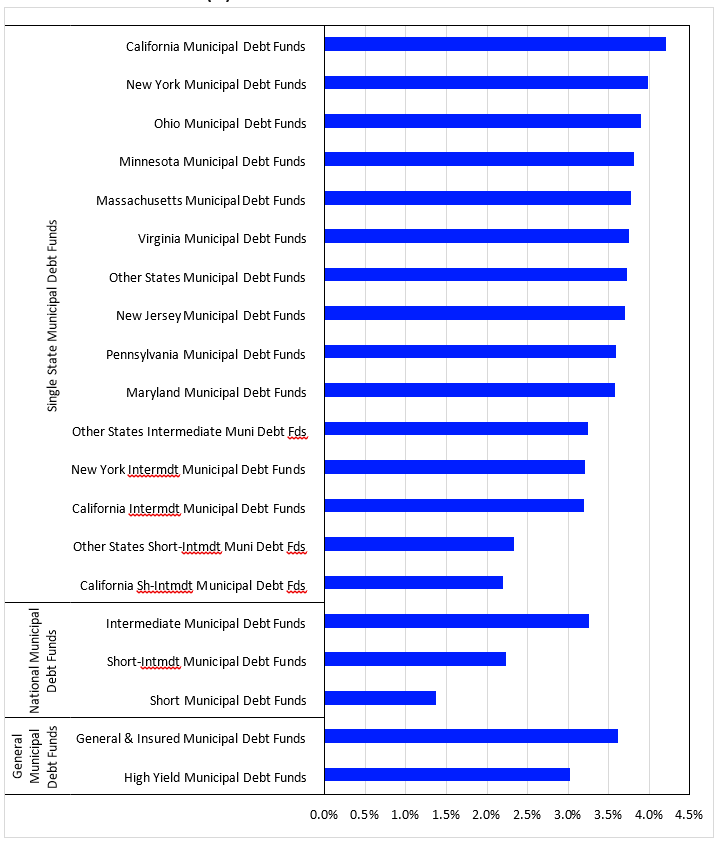

The macro-groups under Municipal Debt Funds all fared rather well to end the calendar year-Single State Municipal Debt Funds (+3.69%), General Municipal Debt Funds (+3.39%), and National Municipal Debt Funds (+2.49%). Each of these macro-groups ended a stretch of three straight negatively performing quarters. Q4 marked the largest quarterly gain for Single State Municipal Debt Funds since Q2 2011. The two top-performing non-single state tax-exempt Lipper classifications were General & Insured Municipal Debt Funds (+3.62%) and Intermediate Municipal Debt Funds (+3.26%).

The top three performing classifications under Single State Municipal Debt Funds were California Municipal Debt Funds (+4.21%), New York Municipal Debt Funds (+3.98%), and Ohio Municipal Debt Funds (+3.90%). Each of these three classifications snapped a three-quarter streak of negative returns.

Figure 4: Q4 2022 Tax-Exempt Fixed Income Performance (%)

Source: Lipper, An LSEG Business

|

© Refinitiv 2022. All Rights Reserved. Lipper FundMarket Insight Reports are for informational purposes only, and do not constitute investment advice or an offer to sell or the solicitation of an offer to buy any security of any entity in any jurisdiction. No guarantee is made that the information in this report is accurate or complete and no warranties are made with regard to the results to be obtained from its use. In addition, Lipper will not be Lliable for any loss or damage resulting from information obtained from Refinitiv Lipper or any of its affiliates. For immediate assistance, feel free to contact Lipper Client Services toll-free at 877.955.4773 or via email at LipperUSClientServices@refinitiv.com. For more information about Lipper, please visit our website at refinitiv.com/en or lipperalphainsight.com |

Be the first to comment