Evgeny Gromov/iStock via Getty Images

Earnings of First Interstate BancSystem, Inc. (NASDAQ:FIBK) will most probably benefit from the first quarter’s acquisition of Great Western Bancorp. Further, decent organic loan growth will likely support the bottom line. Moreover, the margin will benefit from the rising rate environment and the topline’s moderate rate sensitivity. Overall, I’m expecting First Interstate BancSystem to report adjusted earnings of $2.72 per share for 2022, up 6% year-over-year. For 2023, I’m expecting earnings to grow by 52% to $4.12 per share. The year-end target price is close to the current market price. Therefore, I’m downgrading First Interstate BancSystem to a hold rating.

Following The Outsized Acquisition, Organic Growth Will Boost The Loan Portfolio

First Interstate BancSystem reported decent organic loan growth of 1.5% in the second quarter, or 5.9% annualized, following the merger of equals in the first quarter of 2022. The management is optimistic that it can achieve mid-single-digit annualized loan growth for the second half of 2022, as mentioned in the July presentation. Given that loan growth, excluding acquisitions, has remained in the mid-single-digit range in the past, the management’s target appears achievable.

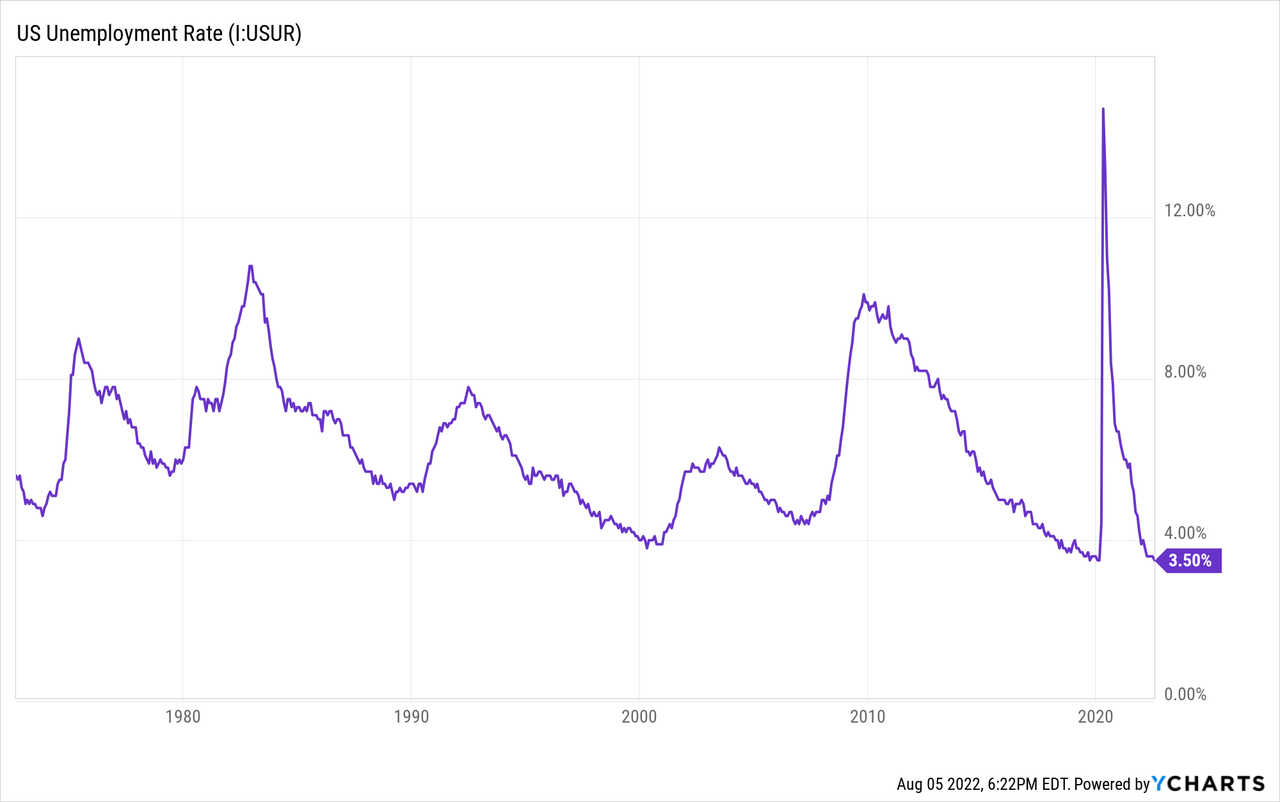

Strong job markets will also make the loan growth target easy to achieve. First Interstate operates in several states; therefore, the national average for the unemployment rate is appropriate to gauge the company’s product demand. As shown below, the unemployment rate is near record lows. This near-full employment will support loan growth.

However, the U.S. leading economic indicator maintained by the Conference Board continued its downtrend in June 2022, which is bad news for loan growth. Further, high interest rates will naturally dampen borrowers’ appetite for credit.

Considering the factors mentioned above, I’m expecting organic loan growth to return to the mid-single-digit range during the second half of 2022 and the full year of 2023. I’m expecting the loan portfolio to grow by 88% in 2022 (including 86 percentage points from the Great Western bank acquisition) and 4% in 2023.

Revising Downwards The TBVPS Estimate

The growth of other balance sheet items will most probably trail loan growth. Tangible book value per share declined by 4.3% in the second quarter mostly because the rising interest rates reduced the value of securities. Going forward, the value of securities will decline further which will pressurize the tangible book value per share. In my last report on First Interstate BancSystem which was published back in December 2021, I estimated a tangible book value per share of $25.8 per share for December 2022. I’ve now slashed it because the interest rate trend so far this year has been different from what I anticipated at the end of 2021. The tangible book value per share has already fallen from $20.83 at the end of December 2021 to $18.92 at the end of June 2022, and I’m expecting it to suffer further from the rising rate environment.

The following table shows my balance sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||

| Financial Position | ||||||||

| Net Loans | 8,431 | 8,858 | 9,663 | 9,209 | 17,283 | 17,984 | ||

| Growth of Net Loans | 11.8% | 5.1% | 9.1% | (4.7%) | 87.7% | 4.1% | ||

| Other Earning Assets | 3,255 | 3,988 | 6,150 | 8,714 | 12,072 | 12,563 | ||

| Deposits | 10,681 | 11,664 | 14,217 | 16,270 | 27,404 | 28,516 | ||

| Borrowings and Sub-Debt | 815 | 798 | 1,291 | 1,251 | 1,549 | 1,612 | ||

| Common equity | 1,694 | 2,014 | 1,960 | 1,987 | 3,186 | 3,456 | ||

| Book Value Per Share ($) | 29.1 | 31.5 | 30.8 | 32.2 | 29.2 | 31.7 | ||

| Tangible BVPS ($) | 18.7 | 21.8 | 21.0 | 21.0 | 17.9 | 20.4 | ||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

||||||||

Net Interest Income Appears Moderately Rate Sensitive

Around half of the loan portfolio will mature or re-price within a year, according to details given in the July presentation. In comparison, around 63% of the deposit book will re-price soon after every rate hike as it comprises savings and interest-bearing demand accounts. Nevertheless, the management was confident that the increase in earning asset yields will exceed any increase in the funding cost, as mentioned in the conference call.

The management’s expectation is not unreasonable because currently there is a lot of liquidity industrywide, which gives banks higher-than-usual power to price deposits. This pricing power will wane in the next two quarters as businesses will chase yields and shift their cash in the bank into treasury securities.

The management’s income simulation model predicted that net interest income could increase by 2.78% over twelve months on an immediate 100 basis points shock, assuming a static balance sheet, as mentioned in the second quarter’s 10-Q Filing.

I’m expecting the fed funds rate to increase by a further 75 basis points in the remainder of the year and then to start declining by the mid of 2023. Considering these factors, I’m expecting the net interest margin to grow by 30 basis points in the second half of 2022 and then remain mostly stable next year.

Economic Factors To Lift Provisioning For Expected Loan Losses

Allowances were 200.5% of non-performing loans at the end of June 2022, which is a comfortable position when compared with peer banks. However, historically First Interstate has kept a large cushion. In the second quarter of 2021 for instance, the allowances were 380.6% of non-performing loans. Therefore, there is reason to believe that First Interstate will want to bolster its reserves especially because of heightened interest rates and the possibility of a recession. Fortunately, a majority of the portfolio is backed by real estate; therefore, the asset quality cannot dip too low.

I’m expecting the provisioning to be a bit higher than the historical norm in the second half of 2022 and the full year of 2023. I’m expecting the net provision expense to make up 0.20% of total loans (on an annualized basis) in the last two quarters of 2022 and throughout 2023. In comparison, the net provision expense averaged 0.17% in the last five years.

Expecting Earnings To Grow By 6%

The first quarter’s acquisition, organic loan growth, and slight margin expansion will likely lift earnings this year. On the other hand, higher provision expenses will likely drag the bottom line. Overall, I’m expecting First Interstate BancSystem to report earnings of $2.72 per share for 2022 after adjusting for merger-related expenses, up 6% year-over-year. On a GAAP basis, I’m expecting FIBK to report earnings of $2.15 per share in 2022. For 2023, I’m expecting earnings to grow by 52% to $4.12 per share. The following table shows my income statement estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||

| Income Statement | ||||||||

| Net interest income | 433 | 495 | 497 | 488 | 931 | 1,061 | ||

| Provision for loan losses | 9 | 14 | 57 | (15) | 76 | 32 | ||

| Non-interest income | 139 | 143 | 157 | 151 | 202 | 207 | ||

| Non-interest expense | 356 | 389 | 388 | 406 | 757 | 660 | ||

| Net income – Common Sh. | 160 | 181 | 161 | 192 | 235 | 449 | ||

| EPS – Diluted ($) | 2.75 | 2.83 | 2.53 | 3.11 | 2.15 | 4.12 | ||

| Normalized EPS – Diluted ($) | 2.35 | 2.50 | 2.15 | 2.56 | 2.72 | 4.12 | ||

|

Source: SEC Filings, Earnings Releases, Author’s Estimates, Seeking Alpha for Historical Normalized EPS (In USD million unless otherwise specified) |

||||||||

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Downgrading To A Hold Rating

First Interstate BancSystem is offering a dividend yield of 4.0% at the current quarterly dividend rate of $0.41 per share. The earnings and dividend estimates suggest a payout ratio of 40% for 2023, which is below the last five-year average of 48%. Although there is room for a dividend hike, I haven’t incorporated an increase in the dividend level in my investment thesis to remain on the safe side.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value First Interstate. The stock has traded at an average P/TB ratio of 1.94 in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| T. Book Value per Share ($) | 18.7 | 21.8 | 21.6 | 21.0 | ||

| Average Market Price ($) | 42.3 | 40.3 | 33.8 | 43.6 | ||

| Historical P/TB | 2.26x | 1.85x | 1.57x | 2.08x | 1.94x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $17.9 gives a target price of $34.7 for the end of 2022. This price target implies a 14.5% downside from the August 5 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.84x | 1.89x | 1.94x | 1.99x | 2.04x |

| TBVPS – Dec 2022 ($) | 17.9 | 17.9 | 17.9 | 17.9 | 17.9 |

| Target Price ($) | 32.9 | 33.8 | 34.7 | 35.6 | 36.5 |

| Market Price ($) | 40.6 | 40.6 | 40.6 | 40.6 | 40.6 |

| Upside/(Downside) | (18.9%) | (16.7%) | (14.5%) | (12.3%) | (10.1%) |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 16.7x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| Normalized EPS ($) | 2.35 | 2.50 | 2.15 | 2.56 | ||

| Average Market Price ($) | 42.3 | 40.3 | 33.8 | 43.6 | ||

| Historical P/E | 18.0x | 16.1x | 15.7x | 17.0x | 16.7x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $2.72 gives a target price of $45.4 for the end of 2022. This price target implies a 12% upside from the August 5 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 14.7x | 15.7x | 16.7x | 17.7x | 18.7x |

| Normalized EPS 2022 ($) | 2.72 | 2.72 | 2.72 | 2.72 | 2.72 |

| Target Price ($) | 40.0 | 42.7 | 45.4 | 48.1 | 50.9 |

| Market Price ($) | 40.6 | 40.6 | 40.6 | 40.6 | 40.6 |

| Upside/(Downside) | (1.4%) | 5.3% | 12.0% | 18.7% | 25.4% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $40.1, which implies a 1.3% downside from the current market price. Adding the forward dividend yield gives a total expected return of 2.8%.

In my last report on First Interstate BancSystem, I projected a target price of $43.2. I’ve reduced my target price because I’ve slashed my tangible book value per share estimate for year-end 2022. Based on the updated total expected return, I’m downgrading First Interstate BancSystem to a hold rating from my previous rating of buy.

Be the first to comment