Viorika

Get to Know FinWise

FinWise (NASDAQ:FINW) share price is too cheap for a fast growing fintech firm and deserves to compete for a spot in your portfolio. FinWise is ripe for a share price upswing as it becomes more well known (11/2021 IPO) and works out of its miscategorized microcap ($117M) shell.

On the surface FinWise is categorized as a run of the mill regional bank but their run of the mill services account for less than 4% of their revenue. FinWise would be more properly categorized as a financial technology bank that provides online lending services.

FinWise has not always been more than a regional bank as the fintech transformation started in 2010 when there was a change in management. Kent Landvatter came on and shifted the firm’s strategic direction towards developing exponentially scalable lending services. It took a few years to make the adjustment but in 2014 FinWise launched their SBA 7(A) small business loan lending program, and then in 2016 they rolled out FinView Analytics and their Strategic Partners Loan program.

FinWise is Scaling

These two new lending programs have grown dramatically and now account for more than 95% of FinWise’s revenue.

Sources of non interest revenue ($20 million) in the first half of 2022 were:

-

77% Strategic Loan Programs

-

20% SBA 7(A) Lending

-

3% Residential and Commercial Real Estate Lending

-

0.4% POS lending (Growth Opportunity)

Strategic Loan Program

FinWise’s largest, youngest, and fastest growing line of business is the strategic loan program. FinWise partners with various technology firms that streamline their lending process but may not have the capability or proper licenses to originate the loans. FinWise originates the loans and then sells +99% of them back to their various partners. As FinWise does this they earn a fee and they collect data empowering their FinView analytics platform. The fee revenue from these partnerships has grown by more than 85% over the past half year over year comparison from $6.9 million to $12.8 million.

In the short term the revenue may fluctuate but with FinWise continuing to add 2-3 partners per year I expect growth to continue over the long term. FinWise currently partners with: Upstart, Edly, American First Finance, Mulligan Funding, Great American Finance, OppLoans, Lending Point, Rise, Reach Financial, and Empower.

FinWise Is Building a Moat

In their strategic programs I found Cross River Bank to be a direct competitor to FinWise as I found them originally originating 70% of Upstart’s loans while FinWise only originated 25%. I continued to track FinWise vs Cross River Bank over time and FinWise was taking market share. According to KBRA on February 24, 2022 62.7% of Upstart’s loans were originated by Cross River Bank and 18.77% by FinWise. Then checking in again on April 12, 2022 FinWise originated 40.25% of Upstarts loans and CRB was at 59.75%. FinWise started 5 years later than CRB originating loans for Upstart and FinWise is continuing to take market share. According to Upstart, the plan is for CRB and FinWise to be used each 50/50 going forward as stated in KBRA’s June 3rd report, if the loan fits within both banks origination requirements they (Upstart) will send for origination from each bank “randomly”.

The second largest line of business for FinWise is their Small Business Associations loan program where they originate, hold and sell SBA loans, of which the majority are sourced from the Business Finance Group (BFG). In order to protect this relationship and line of business FinWise purchased a 10% share of BFG and has negotiated an option to purchase them outright and a first right of refusal up until January 1st 2028.

Interest Income – Another Competitive Advantage

In the first half of 2022 FinWise generated $13 million in interest income and $9 million in non-interest income from their fees and gains on loan sales. So not only does FinWise benefit from origination fees, servicing fees, and upselling loans, they also have first pick at loans they are originating. This can be seen by FinWise originating $2.1 billion last quarter but choosing to hold less than 1% ($1.8 million) of those loans originated on their books.

How does FinWise Stack Up

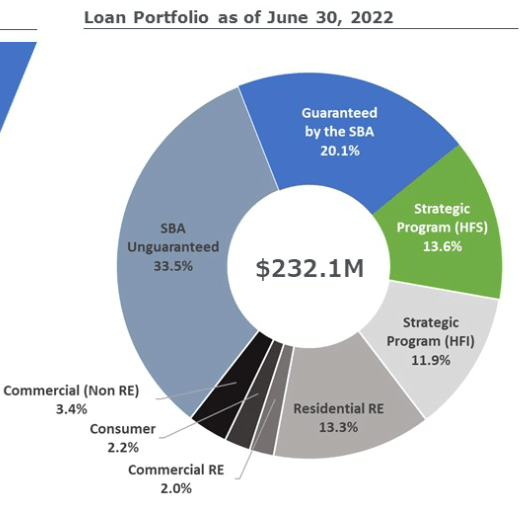

FinWise is categorized as a regional bank but 97% of their non-interest income and 80% of their loan portfolio is derived from their fintech business lines. The loan portfolio as of June 30, 2022 is below.

Finwise

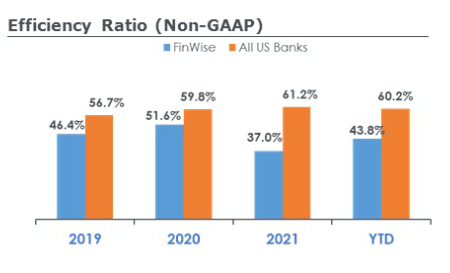

If I am correct in uncovering a potential gem then when comparing FinWise to the average bank they should stand out in a few metrics. Let’s see where they are at in efficiency and interest margin in comparison to the average US bank. I would expect FinWise’s efficiency to be excellent if the technology and software they have built is working and making FinWise a more efficient bank. FinWise’s efficiency ratio thus far in 2022 is 43.8% (efficiency ratio is defined as the total noninterest expense divided by the sum of the net interest and fee income). As Investopedia puts it “An efficiency ratio of 50% or under is considered optimal.” Thus far in 2022 FinWise is at 43.8% in comparison to the average US bank at 60.2%.

Finwise

So FinWise is considered efficient, now lets see if they are earning a premium on the loans they hold in house by cherry picking the best of the best by looking at the net interest margin. As of June 30, 2022 the average net interest margin for US banks was 2.7% and FinWise was 13.5%.

Finwise

It appears FinView, FinWise’s in-house analytics platform is working as FinWise’s net interest margin was 5x the average. (Thus far 0.3% of their loans are delinquent).

Risk

Although I am attempting to paint the picture that FinWise is a fintech firm, I don’t want to make any impression that they do not have banking default risk. Their current loan portfolio consists of $233 million of which only 33.7% is guaranteed, 20.1% by the SBA and 13.6% by their strategic partners. As the federal reserve works to bring inflation under control we may get a good stress test sooner than later on FinWise’s loan portfolio. Seeking Alpha’s editors might not like me adding this into the article but I think it’s worth mentioning the default risk is real and it is the primary reason I don’t hold more.

Management – Reduces Our Risk

Default risk is never good but it helps to know we are in this boat/rocket ship together. Insiders own 24% of the outstanding shares.

FinWise’s share structure is:

- 13,567,311 diluted shares – includes 170,558 warrants @ $6.67 and 619,516 stock options that have not yet been executed.

- No preferred shares or minority interest ownership

CEO Kent Landvatter owns 6.8% of the company. His leadership and proven track record is accompanied by Ms. Cannon, the COO who has over 20 years of banking experience, including Vice President of Operations at EnerBank where she helped build a point of sale (POS) lending program from 23 to 285 full time employees and from $10 million to $1.4 billion in total assets. POS is only 0.4% of FinWise’s current fee revenue but is another growth opportunity not included in my valuations below.

A Few More Tailwinds for FinWise Not Previously Mentioned

FinWise announced a share repurchase program to purchase up to 5% of their outstanding shares (August 2022)

FinWise’s direct competitor Cross River Bank is private and harder to understand but it is worth mentioning they recently raised $620 million, at a $3 Billion valuation.

The POS software market FinWise is entering is worth more than $9 billion and expected to grow.

The Peer to Peer Marketplace of which FinWise is serving is expected to grow at almost 15% CAGR and hit $5.1B by 2032.

The 180-day share lock-up period after the IPO ended in May and if there was any selling it could be subsiding soon.

Valuations

There are a lot of great and growing businesses that are known and priced that way, but luckily for us FinWise isn’t there yet. FinWise is almost 3x cheaper than the average community bank by means of P/E (10 P/E for iShares U.S. regional banks ETF) and FinWise is 11x cheaper than your average fintech firm with an average P/E of 40 (FINX Global X FinTech ETF).

My base stock price estimate for FinWise is $32/share of which is based on a P/E of 10 (regional bank average) and 30% year over year growth. My low price target is their cash value of $9.67 and my upper end price target is $184 of which is based on 40% year over year growth and a multiple in line with their fintech peers.

Stock Price Estimates FINW (Author)

Conclusion

In conclusion, FinWise appears to be an undervalued, unknown, growing and profitable bank/fintech firm. If FinWise’s loan portfolio stays strong through the current stress test and this story becomes better known I think FinWise’s valuation could go 10x and still be cheap in comparison to its fintech peers.

Be the first to comment