Central Bank Watch Overview:

- Rates markets are locked-in for the Federal Reserve to hike rates by 25-bps in March.

- Expectations for a 50-bps rate hike continue to push higher, having escalated meaningfully since the January Fed meeting.

- Commentary around the potential for a 50-bps rate hike as well as the start of QT has provoked significant volatility in financial markets.

Fed Grows More Hawkish

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers since the communications blackout window around the January Fed meeting ended. There has been a notable hawkish shift in tone among most policymakers, though the more dovish members continue to issue caution about too aggressive of a rate hike cycle.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

25-bps or 50-bps?

There is a discernible shift in tone among Fed policymakers since the January Fed meeting. Two notable events have transpired during this timeframe. First, the January US nonfarm payrolls report beat expectations handily, showcasing the resilience of the US labor market in the face of COVID-19 omicron variant concerns. Second, the January US inflation rate report (CPI) showed price pressures at a fresh 40-year high, leading to market chatter that the Fed is falling further and further behind the curve.

January 28 – Kashkari (Minneapolis president) suggested that rate hikes were coming soon, noting that “we haven’t raised interest rates yet but we have signaled that we’re likely to begin that process soon. That would then not tap the brakes on the economy, but it would let our foot off the accelerator just a little bit.”

January 30 – Bostic (Atlanta president) noted that high inflation could provoke the FOMC into a 50-bps rate hike.

January 31 – Daly (San Francisco president) insisted that the Fed is “not behind the curve,” and expanded on her comment by saying “when you’re trying to get an economy from extraordinary support to one that’s going to just gradually put it on to a self-sustaining path, you have to be data-dependent — as we say — but you also have to be gradual and not disruptive.”

George (Kansas City president) hinted that quantitative tightening (QT) may be preferred to more rate hikes, saying that “more aggressive action on the balance sheet could allow for a shallower path for the policy rate.”

February 1 – Harker (Philadelphia president) pushed back against the idea of a 50-bps rate hike in March, commenting “I would be supportive of a 25 basis-point increase in March. Could we do 50? Yeah. Should we? Well, I’m a little less convinced of that right now…but we’ll see how the data turn out in the next couple of weeks.”

Bullard (St. Louis president) also downplayed a 50-bps rate hike, noting that such a move doesn’t “help us — at least sitting here today, I don’t think that really helps us.”

February 2 – Daly proved non-committal to an aggressive rate hike cycle, saying “I do absolutely expect the policy rate to rise over the course of the year, but by how much and how quickly and during what meetings — those things I’m going to leave open.”

February 8 – Daly suggested that she was in favor of a 25-bps rate hike in March, saying “without a big surprise in the data, negative surprises, we would be looking to raise interest rates as early as March — that’s certainly my view — and that is going to start the process of helping get inflation in control.”

February 9 – Mester (Cleveland president) warned that this rate hike cycle would be different than prior cycles as “risks to inflation are still tilted to the upside.”

February 10 – Bullard changed his tone from the start of February, coming out in favor of a 50-bps rate hike in March while also suggesting he’d “like to see 100-bps in the bag by July 1.”

February 14 – George suggested that an immediate change in Fed policy was warranted, as “I don’t think you can look at 7.5% inflation and a tight labor market and think that zero interest rates are the right calibration. So I think where we have to be careful though is not to oversteer.”

February 15 – Kashkari warned against aggressive policy tightening, noting “if we raise rates really aggressively, we run the risk of slamming the brakes on the economy, putting the economy in recession.”

The January FOMC meeting minutes highlighted “if inflation does not move down as they expect, it would be appropriate for the Committee to remove policy accommodation at a faster pace than they currently anticipate.”

{{NEWSLETTER}

Rate Hikes are Coming, That’s Certain

Expectations for a March rate hike have crystallized. We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 2 below showcases the difference in borrowing costs – the spread – for the March 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (March 2022-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (February 2021 to February 2022) (Chart 1)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are 160.75-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly is just off of its widest spread since the Fed taper talk began in June. Prior to the expiration of the February 2022 Eurodollar contract, there were 185-bps discounted through the end of 2023; in other words, a 25-bps rate hike is fully priced in for March. Rates markets are pricing in a 100% chance of seven 25-bps rate hikes and a 40% chance of eight 25-bps rate hikes through the end of next year.

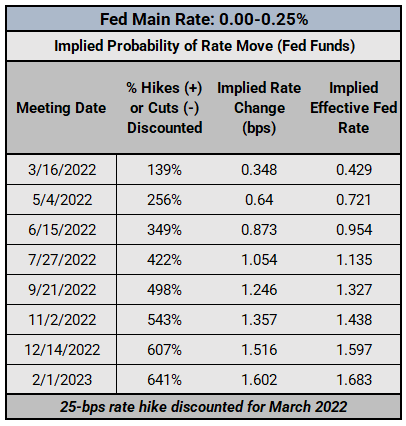

Federal Reserve Interest Rate Expectations: Fed Funds Futures (February 17, 2022) (Table 1)

Fed fund futures have continued to become more aggressive in recent weeks. Ahead of the January Fed meeting, traders see a 100% chance of a 25-bps rate hike in March, with a 5% chance of a 50-bps rate hike. Now, there is a 100% chance of a 25-bps rate hike in March, with a 39% chance of a 50-bps rate hike.

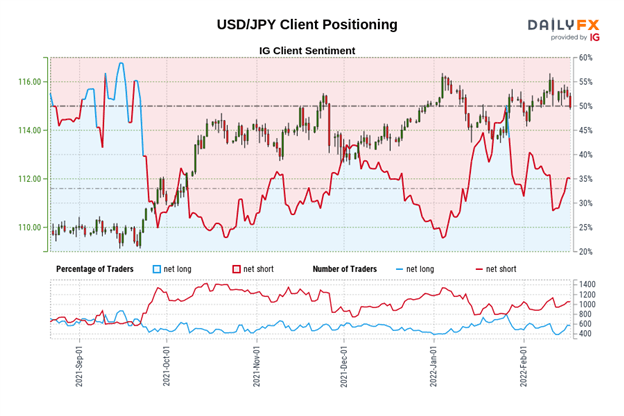

IG Client Sentiment Index: USD/JPY Rate Forecast (February 17, 2022) (Chart 2)

USD/JPY: Retail trader data shows 35.78% of traders are net-long with the ratio of traders short to long at 1.79 to 1. The number of traders net-long is 1.81% lower than yesterday and 21.57% higher from last week, while the number of traders net-short is 9.59% lower than yesterday and 14.30% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/JPY price trend may soon reverse lower despite the fact traders remain net-short.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment