Thinkhubstudio

Investment Thesis

Fastly (NYSE:FSLY) is a content delivery platform. Fastly allows its users the ability to distribute digital content. Essentially, transmitting content via digital assets, such as websites and other media to end-users.

During the pandemic, many investors and companies bought into a narrative that didn’t play out.

With Fastly’s stock down more than 85% from its all-time highs, I believe most would agree, in hindsight, demand for Fastly’s infrastructure services wasn’t quite as high as stakeholders’ expectations.

But that’s now in the rear-view mirror. What matters today is whether the analyst from Bank of America that made the call on Fastly makes sense for new investors. Those investors looking at Fastly from this price point, and looking ahead.

Personally, I struggle to buy into its prospects. At least for now.

More Muted Expectations

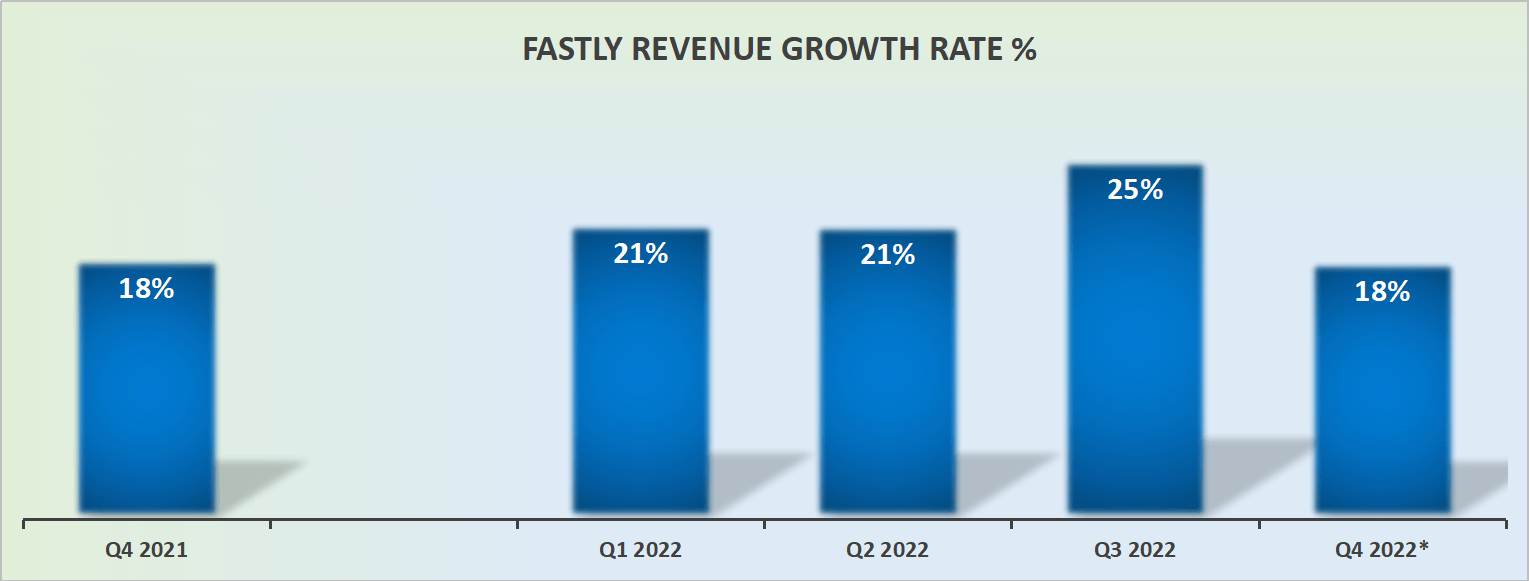

FSTLY revenue growth rates

I believe that most investors would by now come to terms with the fact that Fastly is no longer a hyper-growth company (+30% CAGR).

Indeed, most investors would probably even be inclined to acquiesce that Fastly is only ”just” a high-growth company. Typically, high-growth companies consistently report a +20% CAGR.

And while we don’t have any visibility into its full year 2023, I’m inclined to believe that Fastly’s revenue growth rates will now stabilize at around 20% CAGR.

That being said, consider how much analysts have already downwards revised their expectations for Fastly.

SA Premium

On average, analysts are expecting FSLY’s growth rates to stabilize at around 15% CAGR in the coming year, so if in fact, my own estimates of 20% CAGR turn out to be closer to reality, then analysts will be rapidly raising their financial targets, like we saw yesterday, which will further provide support for this ailing stock.

Next, we’ll discuss Fastly’s profitability profile, and how investors should think about the pluses and minuses here.

Profitability Leaves Much to be Desired, But

At the most superficial level, Fastly is an unprofitable business.

And not only unprofitable at a GAAP level, but also burning through free cash flows. And that’s not a good combination.

Indeed, compared with many of Fastly’s content delivery peers, including the formidable Cloudflare (NET), Fastly’s free cash flow line in Q3 burnt through $44 million and shows no sign of abating.

Moreover, looking back over Fastly’s cash flow line over the previous 8 quarters the business hasn’t ever turned cash flow positive.

FSLY cash flows

Note, the graphic above shows cash flows and not free cash flows, simply to accentuate the core of the problem.

However, I don’t believe this is where this story ends. I believe that investors are being too quick to disregard Fastly’s potential.

FSLY Q3 2022

Indeed, if Fastly’s able to provide tangible evidence in its Q4 results that its platform continues to resonate with a growing number of enterprise customers, given that these are the needle movers for Fastly, this could see this company’s prospects revitalized.

Hence, I believe that in the same way as during the pandemic many companies bought into the idea that they needed to reshape and adapt to allow their workforce to work seamlessly from anywhere, the same currents could unfold if more companies reposition their business for the oncoming wave of AI technology.

Perhaps the biggest blemish to this story is that FSLY holds approximately $700 million of senior convertible notes, which make up about 50% of its market cap.

Given that the business isn’t self-sufficient yet, its 2026 convertible notes could cause a problem for investors.

The Bottom Line

At its core, Fastly is a network infrastructure company. And unlike many of its peers, its share price was seen as dead and unmoving. That is until yesterday when an analyst yesterday created a spark, that revived and revitalized FSLY.

Now, the only question that remains unanswered is whether there’s more upside to this name from this valuation.

I’m not entirely convinced as of yet. But I retain some room for doubt. The next catalyst for this stock will be its Q4 2022 earnings in the coming few weeks. Whatever you decide, good luck and all the best.

Be the first to comment