Irina Kashaeva

The Dogs of the Dow strategy gained popularity in 1991 when it was published in Michael B. O’Higgins’ book, Beating the Dow. In this book is where Mr. Higgins coined the phrase “Dogs of the Dow.”

For those of you unfamiliar, the Dogs of the Dow strategy looks at the 10 highest yielding dividend stocks within the Dow Jones Industrial Average at the conclusion of the year.

At the end of 2022, here are your 10 Dogs of the Dow:

- Verizon (VZ) 6.2% dividend yield

- Walgreens (WBA) 5.2%

- Intel (INTC) 4.9%

- Dow, Inc. (DOW) 4.8%

- 3M (MMM) 4.6%

- International Business Machines (IBM) 4.5%

- Chevron (CVX) 3.2%

- Amgen (AMGN) 3.1%

- Cisco Systems (CSCO) 3.1%

- JPMorgan Chase (JPM) 2.8%

This strategy is used by not only dividend investors but value investors as well because after all as a stock price goes down a dividend yield goes up. However, just because a stock is on this list does not necessarily mean it had a bad year over the past 12 months. After all, Chevron was one of the best performing stocks in the S&P 500 last year, let alone the DJIA.

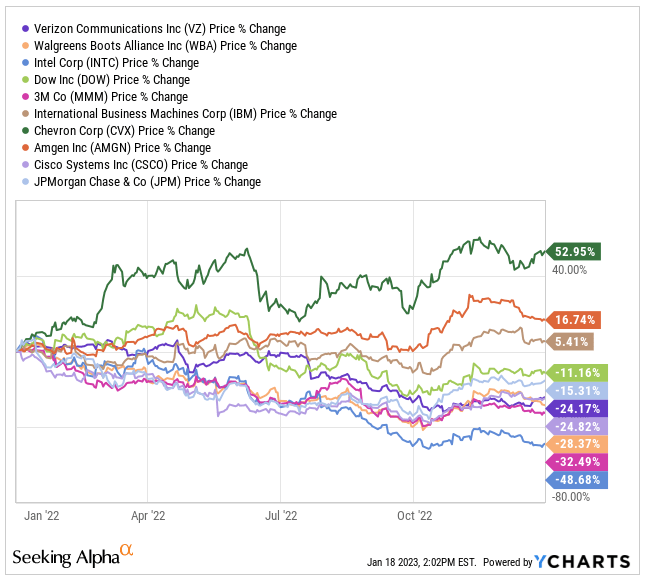

Here is a look at how all 10 of these Dogs of the Dow stocks performed in 2022:

ycharts

As you can see in the chart, Chevron shares we up over 50% in 2022, far surpassing all the others. Only 3 of these 10 stocks were positive on the year, as Amgen and IBM also joined CVX in positive territory.

Intel, 3M, and Walgreens were the three worst performing stocks on this list, as Intel was down nearly 50% on the year.

3 Dogs of the Dow For 2023

Dog of the Dow #1 – Intel Corp (INTC)

As we saw above, Intel was the worst performing stock out of all 10 Dogs of the Dow. The company has gone through a lot of changes and delays in the recent years, which has led to a loss of market share. Advanced Micro Devices (AMD) has been progressing fast in the chip space, and is right on the cusp of surpassing INTC when it comes to market cap.

INTC has a market cap of $122 billion compared to AMD having a market cap of $115 billion.

Although the company has been down, I am not counting them out. INTC has had numerous hiccups along the way, many having to do with the execution or lack thereof and delays from many of their new chips, which has allowed companies like AMD and NVDA to take advantage.

The company is led by long time Intel employee Pat Gelsinger who took over the CEO reigns in February 2021.

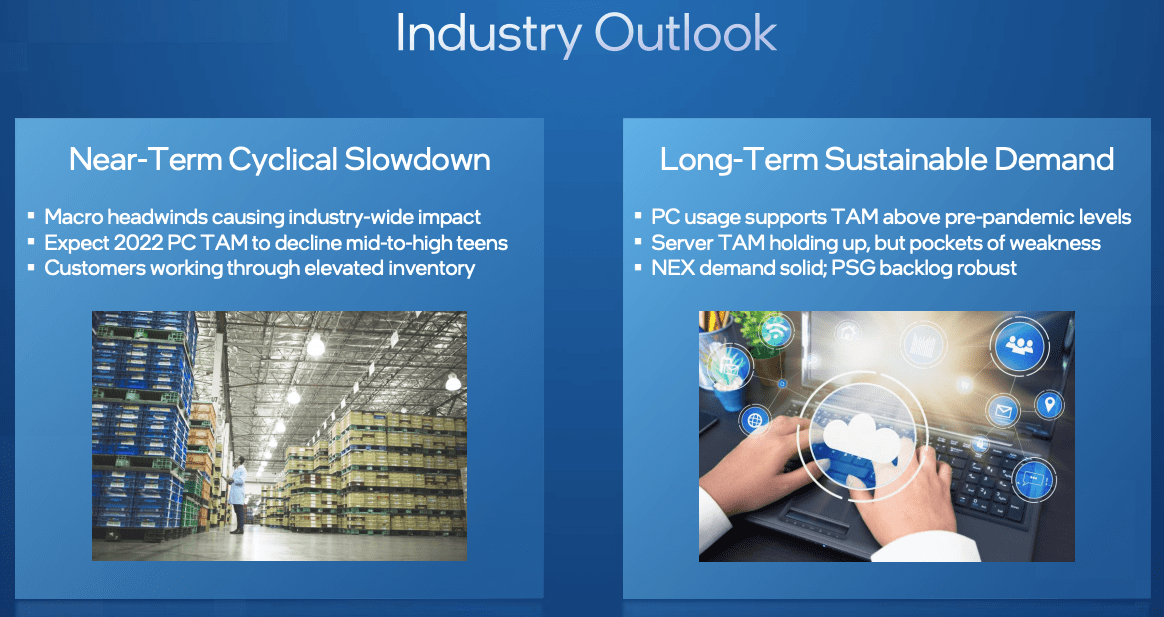

Intel leadership is confident they can turn things around from an operations standpoint, and as they do, the industry is ready. Macro headwinds such as higher interest rates and slowing economic growth, which pose near-term headwinds for the company.

The total addressable market has surpassed pre-pandemic levels as demand remains strong, which is a long-term tailwind for a company like Intel.

INTC Q3 Investor Presentation

Mr. Gelsinger has set out to “right size” the company, in which they announced layoffs at the end of 2022 and further layoffs could be coming. That will be an interesting point to follow up on when the company reports Q4 earnings next week.

Intel is still flush with cash as they have over $25 billion of cash and short-term investments on the balance sheet as of Q3, which should give dividend investors comfort at least in the near-term.

The company pays a $1.46 per share dividend, which was increased 5% in 2022, and is expected to get another hike next week when the company releases earnings. The dividend yield currently sits at 4.9%.

Dog of the Dow #2 – 3M (MMM)

3M has long been an industrial bellwether that is found in many dividend portfolios. However, like Intel, 3M had a rough year as they were the second worst performer on the list, as the stock fell over 30% on the year.

3M is known for having a diversified portfolio of products, more well-known for items like their post-it notes, masks, scotch tape, and MANY other products.

However, 2022 was less about those primary products letting them down and more about a single product letting them down. The company has found themselves wrapped up in thousands of lawsuits, over 200,000 to be more precise, in regards to earplugs that were sold by one of the company’s subsidiaries. Military personnel who are the ones suing the company, have stated that they have encountered a loss of hearing due to defective earplugs.

The subsidiary, Aearo Technologies, ended up filing for bankruptcy, but a federal judge saw this as 3M attempting to offset the liability from their books, which was denied, but 3M has since appealed that decision. In 2018, 3M paid $9.1 million to the Department of Justice to resolve any allegations, but the current lawsuits are now coming from individual military personnel.

Military Times

Exposure estimates are quite wide from $10 billion to $80 billion. If it is on the higher side, it could really pose a threat to 3M, but I believe as the process plays out through appeals, things will come out closer to the lower end, but that is just my opinion.

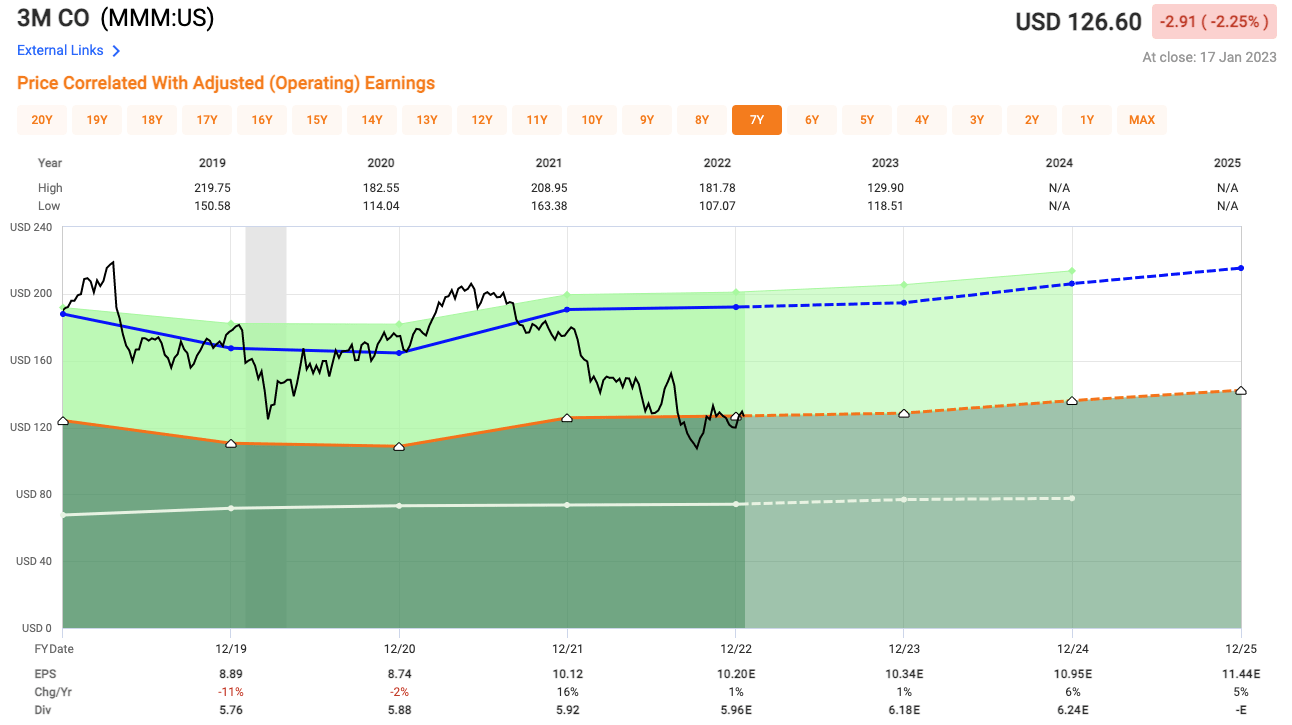

As such, there is plenty of risk when it comes to 3M, but at the same time you are getting the opportunity to add shares at a very cheap valuation when it comes to their historical average.

Shares of 3M currently trade at 12x next year’s earnings compared to a 5-year average of 18.8x. The risk is there, but the price is cheap, plus you get 4.6% dividend yield.

Fast Graphs

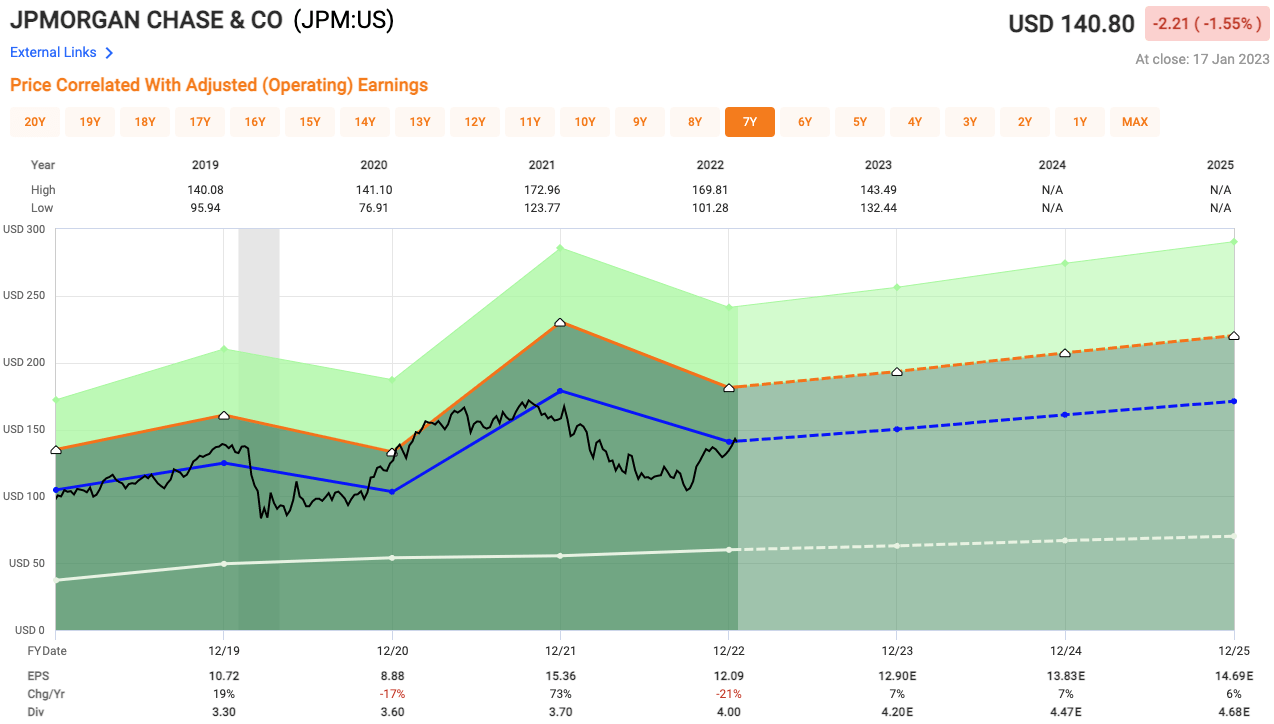

Dog of the Dow #3 – JPMorgan Chase (JPM)

JPMorgan Chase (JPM) is the third Dog of the Dow for 2023, and easily considered the safest investment between the three stocks we have looked at today.

Intel is a quality company that has had failed execution and 3M has plenty of legal issues to deal with, so both of those stocks have some risks that come along with them. JPMorgan on the other hand is led by the great Jamie Dimon.

Given the current state of the economy and the rising rate environment we are going through, banks could prove to be a great investment. As rates increase, so does Net Interest Income, or NII, which is the difference between the interest income you receive from products like loans and the interest you pay out on products like savings accounts.

Rates are expected to continue to increase in the near-term, albeit at a slower pace, but we are also expected to remain at much more elevated rates than we are accustomed to seeing the past few years, which benefits financial stocks.

The thing to watch closely with banks is the strength of the consumer. JPM reported Q4 earnings last week that beat analyst expectations, but we did see them apply more cash towards their credit loss reserve. In addition, during the earnings call, JPM alluded to a “mild recession.” If we get a mild recession, banks could be a big winner in the markets, but a moderate or big recession, would prove to be bad.

CNBC

JPMorgan had been increasing their dividend every year for nine straight years, but that ended in 2022, as we did not see any increase. The dividend yield currently sits at 2.8%.

In terms of valuation, JPM shares currently trade at 10.9x based on 2023 estimates, which is below their historical average of 11.7x.

Fast Graphs

Investor Takeaway

The Dogs of the Dow is both seen as a dividend strategy as well as a value strategy. Stocks on the list does not necessarily mean they performed poorly the year prior, but rather that they pay a high yield.

These three stocks, INTC, MMM, and JPM, all have inherent risks, some larger than others.

Intel is a company that needs to turn things around and they are investing a lot of money in an attempt to do that.

3M has been a great company for over 100 years, but they have fallen on tough times due to the military earplug issue they are facing right now, where over 200,000 military personnel have entered a case against the company for selling a defective product. Exposure amounts are all over the map, but if it comes in at the low end, these levels are going to prove to be a great buying opportunity.

JPMorgan is the largest US bank in terms of assets, and also one of the most well run banks under the leadership of Jamie Dimon. If we do get a mild recession, I believe banks like JPM will prove to be a major success.

Let me know down in the comments section below, which Dog of the Dow stock you like for 2023.

Be the first to comment