da-kuk

Fair Isaac Corporation (NYSE:FICO) is a leading financial technology company which is known for its iconic “FICO Score”. These specialist credit scores are utilized by 90% of the top U.S. lending institutes, for risk assessment needs. FICO is a high-quality, established company that has continually produced consistent financial results, since its founding in 1956. Recently, the company reported a strong fourth quarter, as it beat both its revenue and earnings growth estimates. In this post, I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model

As mentioned prior, FICO offers credit scores via its leading data analytics platform. Its technology is used by over 50 of the top 100 banks and financial services companies, including Fannie Mae and Freddie Mac. In addition, the platform is used by rating agencies such as Standard & Poor’s, as well as Fitch.

This business operates across 120 countries and serves a range of industries from insurers, to retailers, telecommunications, and automotive companies. FICO has created a unified platform that uses a modular cloud architecture, which enables its customers to configure bespoke solutions.

Its products include:

- FICO Score Models

- Debt Resolution Services

- Prescriptive Analytics

- Fraud Protection and Compliance

- and much more.

In 2021, the company sold its “Collections and Recovery” product to a joint venture in China. This enabled the company to refocus on its core B2B SaaS platform and FICO score segment. The big data industry was valued at $162.6 billion in 2021 and is forecast to grow at a rapid 11% compounded annual growth rate (CAGR), reaching $273.4 billion by 2026. FICO is poised to benefit from this growth trend.

Solid Financials

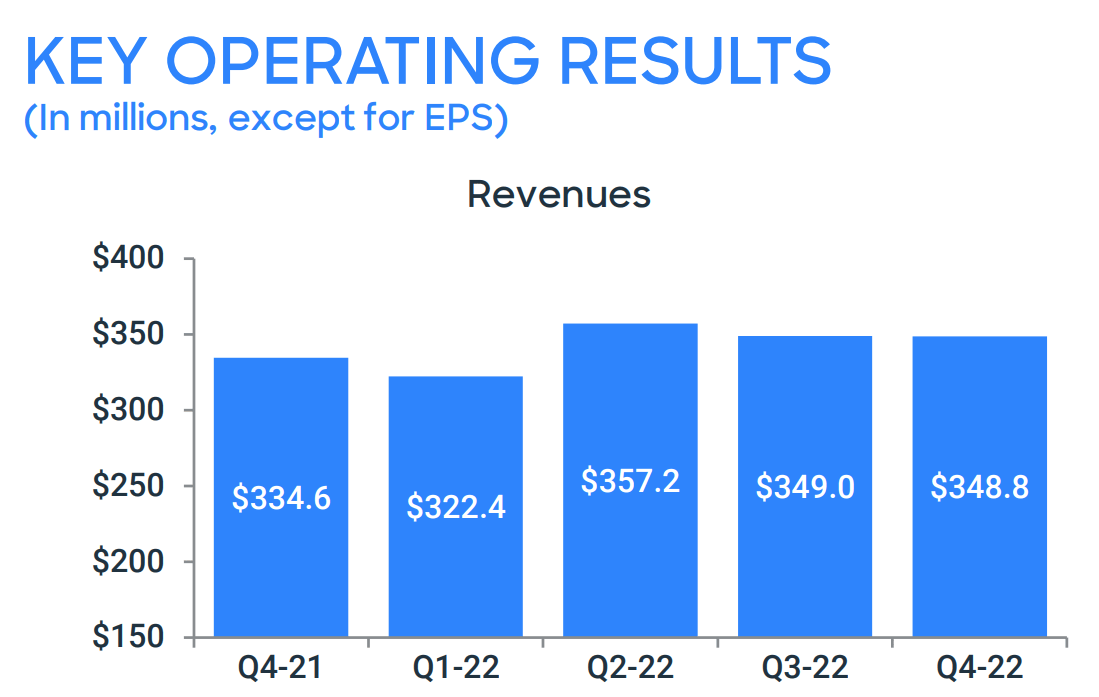

FICO reported solid financial results for what the company refers to as the “fiscal” fourth quarter of 2022, (but actually it would be Q3 of the calendar year). Revenue was $348.75 million, which beat analyst expectations by $4.85 million and increased by 4.25% year over year. This is not an amazing growth rate, but it is expected due to the company’s mature business model.

Revenue (FICO Q4 FY22 report)

Breaking revenue down by segment, FICO’s “Scores” segment increased by 3% year over year to $174 million. B2B revenue increased by 6%, which was driven by credit card and auto scores growth. This offset the continued decline in mortgage score revenues, which has been driven by the high-interest rate environment, which has impacted mortgages. Its B2C revenue declined by 3% year-over-year due to lower subscribers to the myFICO.com platform.

Taking a step back, full-year Scores revenue was $707 million, which increased by 8% year over year. Its Software segment reported stronger growth of 5% year over year to $175 million and was up a solid 9% year over year, with sale divestitures.

FICO reported positive news in the quarter as its new FICO score models (10T) were “validated” and “approved” by Fannie Mae and Freddie Mac.

The vast majority (82%) of FICO’s revenue is derived from the “Americas” which includes North America and Latin America. While the EMEA region contributed to just 11% growth, followed by 7% from the Asia Pacific. Although its revenue isn’t very diversified internationally, this is actually a positive given the macroeconomic climate. A strong dollar versus the euro has caused foreign exchange headwinds for many companies which derive a large portion of revenue from outside of the U.S.

Revenue Mix (Q4 ’22 report)

Annual recurring revenue (ARR) is arguably a better metric to analyze its SaaS platform. In this case, I was pleasantly surprised to see an ARR of $114 million, which increased by a rapid 52% year over year.

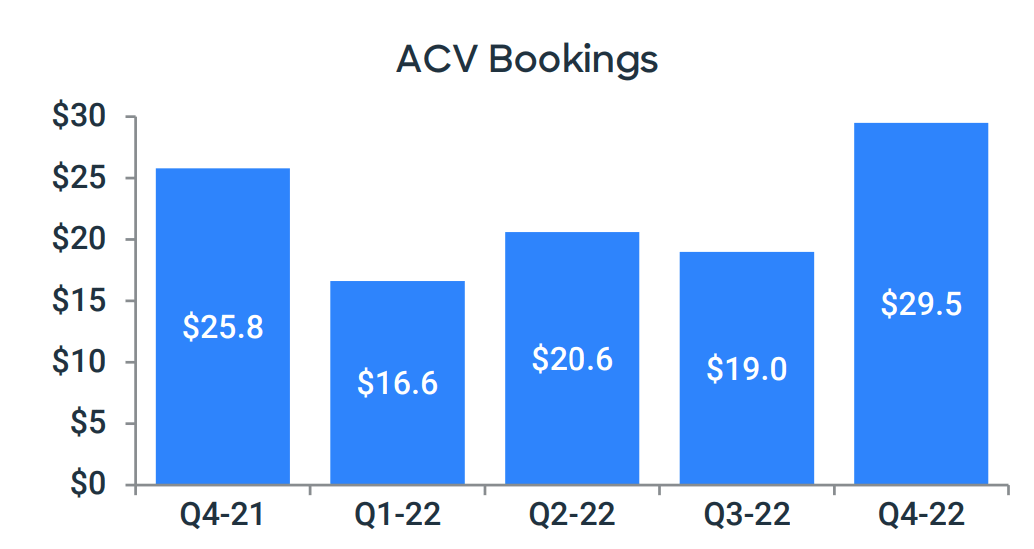

The company also reported a strong dollar-based net retention rate of 128%, which means customers are staying with the platform and spending more. Average Contract Value (ACV) bookings increased from $25.8 million in Q4 ’21 to $29.5 million in Q4 ’22, which is a positive sign.

ACV Bookings (Q4 ’22 report)

Moving onto profitability, FICO reported earnings per share (EPS) of $3.55, which beat analyst estimates by $0.22 and increased by a solid 8.94% year over year. This was driven by a $4 million reduction in expenses, from $219 million last year to $215 million this year. This was mainly caused by improved operational efficiencies and headcount reduction.

FICO has $130.2 million in cash and short-term investments on its balance sheet. The company does have a fairly high debt of $1.912 billion but just $30 million of this is current debt and thus manageable. Approximately 70% of FICO’s debt is also at a fixed rate, which is a positive sign given the rising interest rate environment.

Moving forward, for the fiscal year 2023, FICO is expecting revenue of $1.475 billion, which would represent an increase of 7% year over year. Net income is expected to be $401 million, which would mean an increase of 7.5% year over year.

Advanced Valuation

In order to value FICO, I have plugged the latest financials into my discounted cash flow model. I have forecast 7% revenue growth for next year, which is aligned with management’s forecast. However, in years 2 to 5 I have forecast a faster growth rate of 10% per year. I expect this to be driven by an improvement in the mortgage market, in those future years, as economic conditions tend to be cyclical.

FICO Stock Valuation 1 (Created by Author Ben at Motivation 2 Invest)

To increase the valuation accuracy, I have capitalized on R&D expenses, which have lifted net income. In addition, I have forecast a pretax operating margin of 43% over the next 8 years. I expect this slightly better margin to be driven by scale improvements in operating efficiency and its software platform.

FICO Stock Valuation 2 (Created by Author Ben at Motivation 2 Invest)

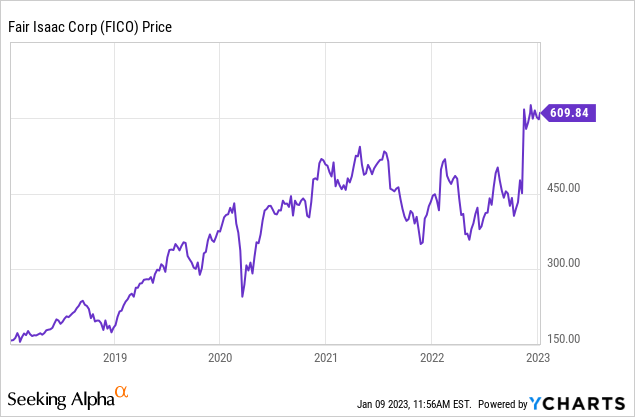

Given these factors, I get a fair value of $518 per share, the stock is trading at $608 per share at the time of writing, and thus it is ~17% overvalued.

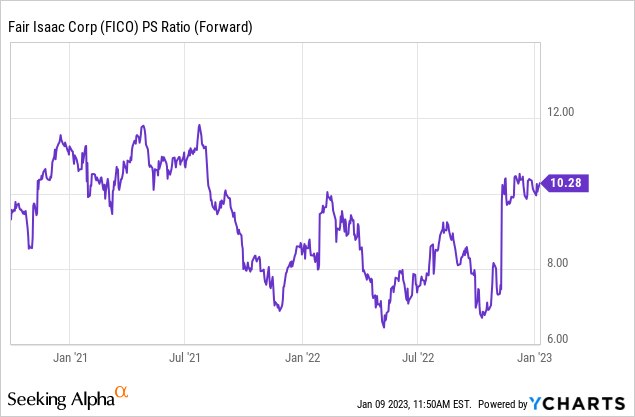

The company is trading at a price-to-earnings ratio = 42, which isn’t exactly cheap relative to the IT sector average of 22. However, it is over 10% cheaper than its 5-year average.

Risks

Recession/Mortgage Market

The high inflation environment has caused many analysts to forecast a recession, which will likely further impact the already tepid mortgage market. The Fed has continued to raise rates, which increases the cost of borrowing and the number of defaults for the everyday consumer.

Final Thoughts

FICO is a legacy fintech company with a strong brand and a series of huge, well-established customers. The business has consistently produced solid and consistent financial results, which is a strong positive. In addition, the company is poised to benefit from the growth in both the fintech and big data industries. The only issue with the stock is its valuation, which is higher than my fair value point intrinsically, and thus, I will label it as a “hold” for now.

Be the first to comment