Hammad Khan

I recently covered the iShares Latin America 40 ETF (ILF), a Latin American equity index ETF. ILF offers investors an incredibly cheap valuation, an outstanding 12.7% dividend yield, and a double-digit annual dividend growth track record. ILF is a strong, albeit risky, investment opportunity, and a buy.

The iShares MSCI Brazil Capped ETF (NYSEARCA:EWZ) is a simple Brazil equity index ETF, with broadly similar characteristics and investment thesis relative to ILF. EWZ offers investors a strong, growing 12.7% dividend yield, and an incredibly cheap valuation. EWZ is also a strong, albeit risky, investment opportunity, and a buy.

I slightly prefer EWZ over ILF, as EWZ yields more and sports a cheaper valuation. ILF is more diversified and less risky, but not significantly so, as ILF focuses on Brazilian equities, and as Latin American equities tend to be strongly positively correlated. Brazil goes down and Mexico, Argentina, Colombia, etc., will very likely go down too, so ILF’s diversification is only a tiny benefit.

EWZ – Basics

- Investment Manager: BlackRock

- Underlying Index: MSCI Brazil 25/50 Index

- Expense Ratio: 0.58%

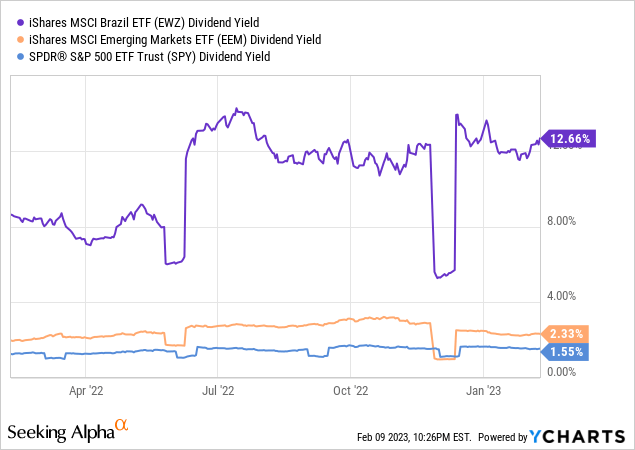

- Dividend Yield: 12.66%

EWZ – Overview

EWZ is an equity index ETF, tracking the MSCI Brazil 25/50 Index. Said index invests in the most relevant Brazilian equities, subject to a basic set of liquidity, trading, etc., inclusion criteria. It is a market-cap-weighted index, with security caps meant to ensure a modicum of diversification, as well with compliance with regulatory standards.

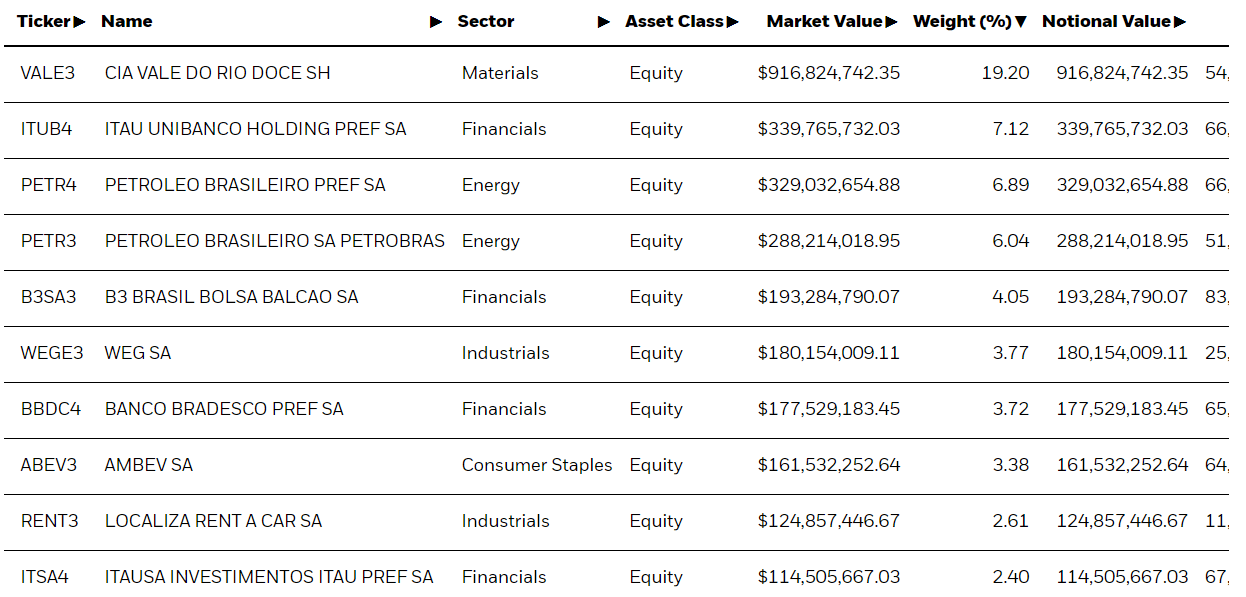

EWZ currently invests in 49 different companies, encompassing approximately 85% of the Brazilian public equities market by market cap. The fund is incredibly concentrated and top-heavy, with the fund’s top five holdings accounting for around 40% of its value. Vale (VALE), an iron ore producer and the fund’s largest investment, accounts for almost 20% by itself.

EWZ

Concentration increases risk, volatility, and means fund performance is strongly dependent on the performance of its top 2-3 holdings.

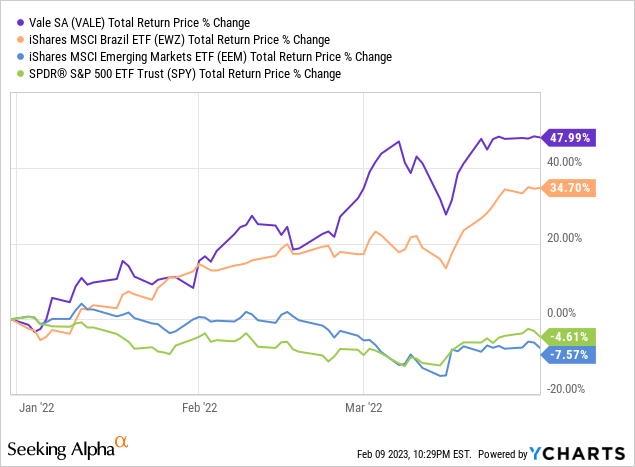

Expect significant gains and outperformance if Vale outperforms, as was the case during 1Q2022, during which iron ore prices skyrocketed.

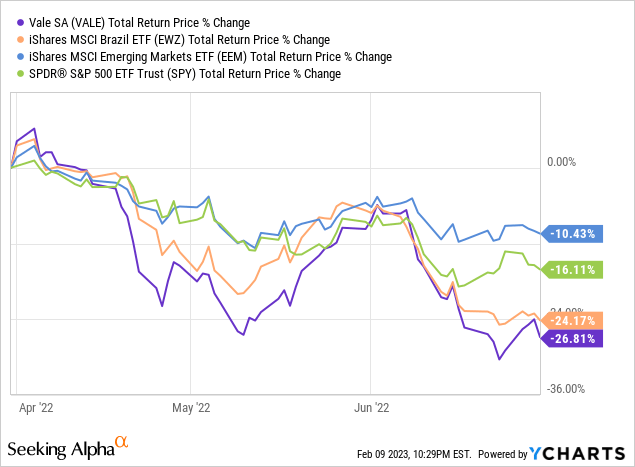

Expect significant losses and underperformance if Vale underperforms, as was the case during 2Q2022, during which the market clawed back some of Vale’s gains (which seemed excessive).

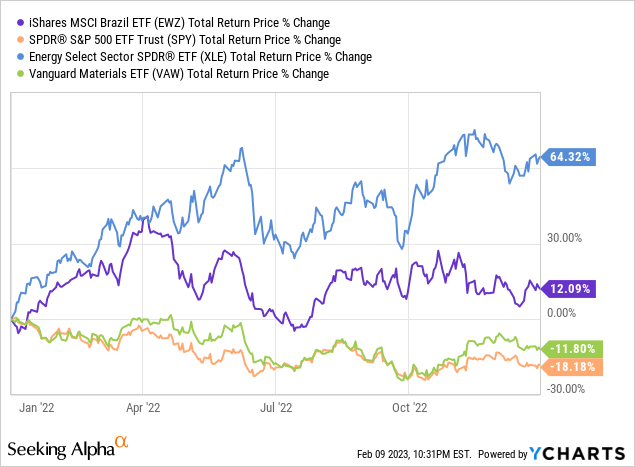

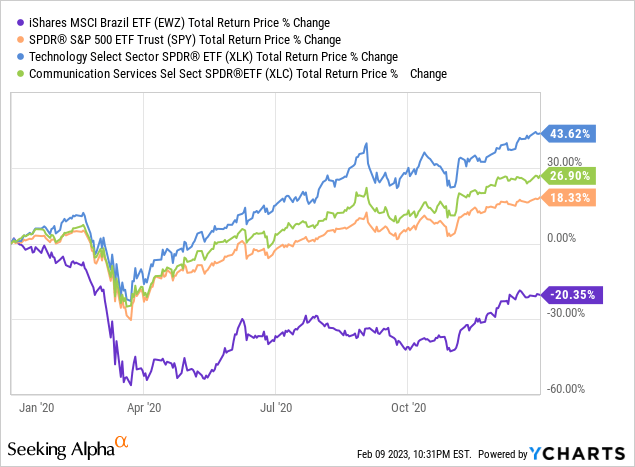

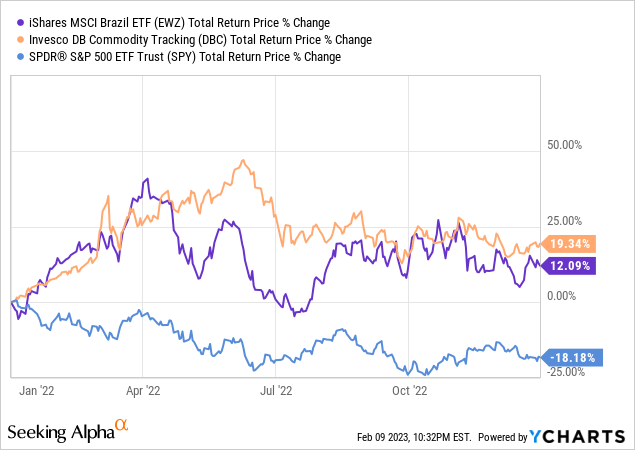

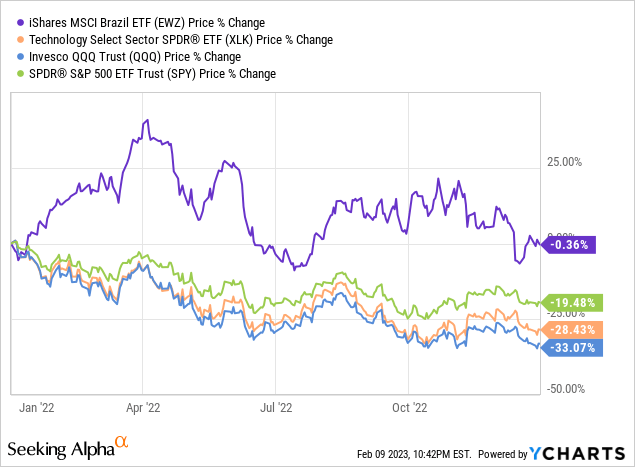

Importantly, and as can be seen above, EWZ’s performance was at least partly driven by its sizable investment in Vale: neither U.S. nor emerging market equities saw losses of the same magnitudes.

As should be clear from the above, EWZ’s concentrated portfolio increases risk, volatility, and the potential for significant losses and underperformance. These risks will not necessarily materialize moving forward, but the risks remain.

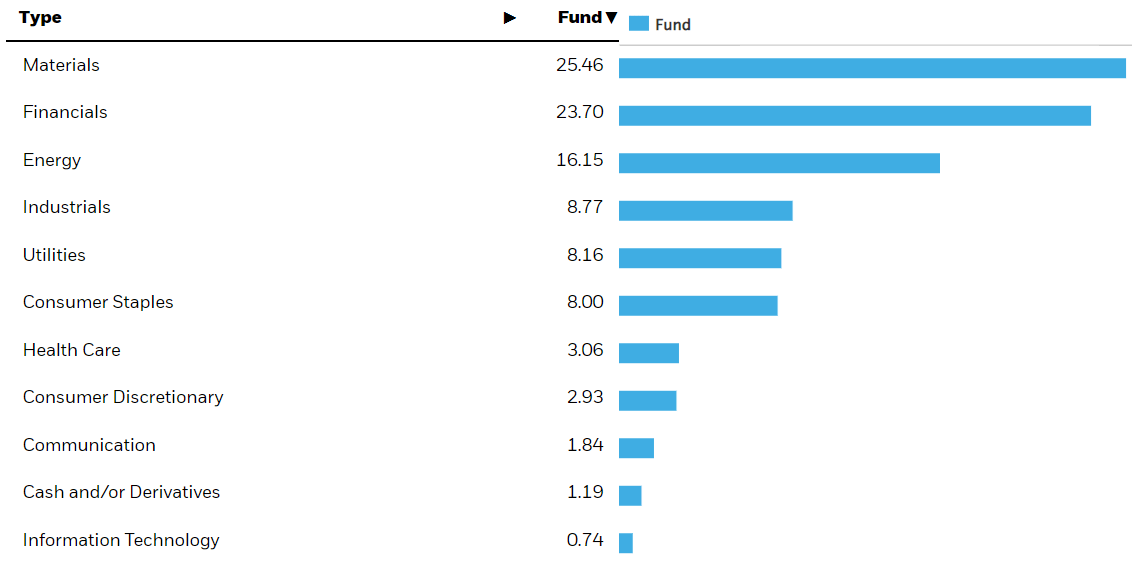

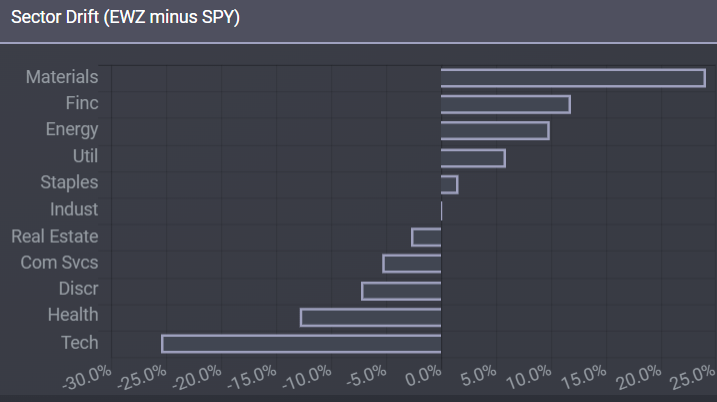

EWZ provides exposure to the most relevant industry segments, although tech and communication weights are tiny and almost inconsequential to the fund’s performance.

EWZ

EWZ’s industry weights markedly differ from those of the S&P 500, and most broader U.S./global equity indexes as well. As can be seen above, the fund is significantly overweight materials and financials, with a sizable allocation to energy. EWZ’s largest holdings are reflective of its industry weights, with sizable allocations to Vale, an iron ore producer, Petrobras (PBR), Brazil’s national oil company, and Itau (ITUB), the country’s largest bank. On the flip side, the fund is underweight tech, communications, healthcare, and consumer discretionary.

etfrc.com

Due to the above, EWZ’s relative performance is strongly dependent on the relative performance of the different equity industry segments. The fund tends to outperform when energy, materials, and other old-economy industries outperform, as was the case in 2022.

On the other hand, the fund tends to underperform when tech, communications, and other growth industries outperform, as was the case during 2020.

EWZ is overweight energy, an industry with significant commodity price exposure, and materials, with moderate exposure to the same. Brazil itself is overweight these and other similar industries, as evidenced by the country’s public equity markets, the large size of Vale, Petrobras, and other similar companies. Commodities encompass most of the country’s exports, and so are particularly important for the value of its currency, and for the value, in dollars, of local investments.

OEC

From the above, it seems incredibly clear that EWZ’s performance and returns are somewhat dependent on commodity/commodity prices. The relationship is definitely there, although somewhat obscured as other factors, including market sentiment and dividends, matter too. Still, it does seem like commodity prices influence EWZ’s share price, much more so than average.

EWZ’s significant commodity exposure increases risks, as does the fund’s concentrated portfolio, as does focusing on emerging markets. The result is an incredibly risky, volatile fund, and one which is only appropriate for the most risk-seeking, aggressive investors. In my opinion, at least.

Although EWZ is a relatively risky investment, it is also one with significant potential returns. Let’s have a look.

EWZ – Investment Thesis

EWZ’s investment thesis is remarkably simple and rests on the fund’s strong, growing 12.7% dividend yield and incredibly cheap valuation. These combine to create a fund with significant potential returns, and one which should, in my opinion, outperform moving forward. Let’s have a closer look at each of these two points.

Strong, Growing 12.7% Dividend Yield

EWZ currently sports a 12.7% dividend yield. It is an incredibly strong yield on an absolute basis, and much higher than the U.S./emerging market equity average.

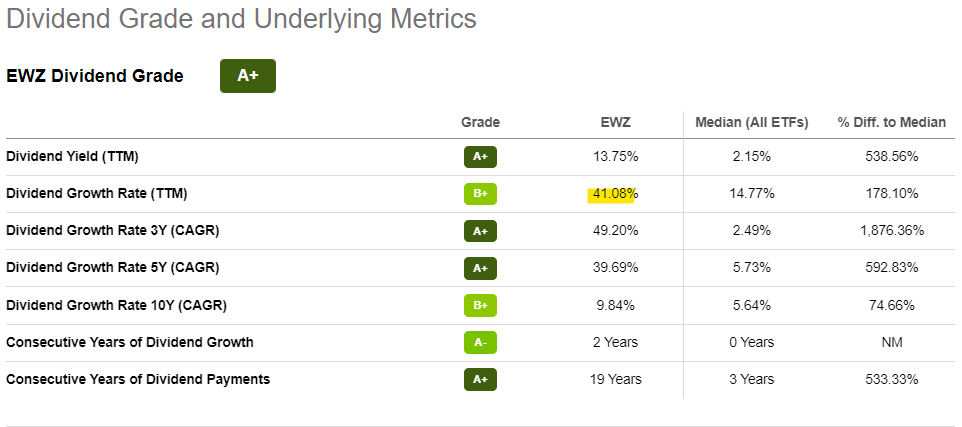

EWZ’s dividends have seen strong growth since inception too, in the high-single-digit/low-double-digit range. Growth has accelerated in the recent past, with fund dividends growing a whopping 40% YTD.

Seeking Alpha

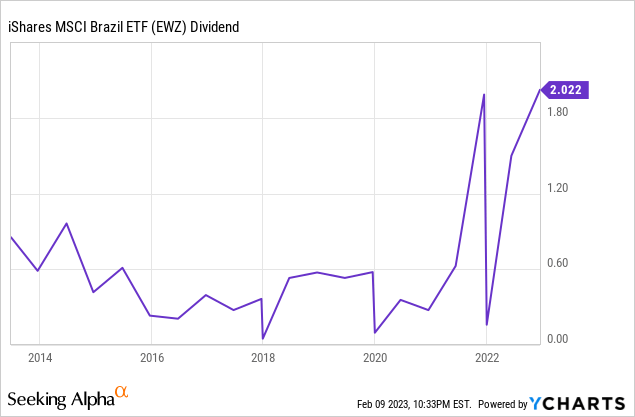

On a more negative note, EWZ’s dividends are very volatile. Looking at fund dividends for the past decade is, I think, informative in this regard.

EWZ’s dividend volatility is, in and of itself, a negative for investors, and might be a deal-breaker for some retirees and income investors. EWZ’s dividend volatility also means dividend growth metrics might not be all that informative, or indicative of future dividends. EWZ’s dividends have seen significant growth YTD, but said growth could, perhaps, have simply been due to volatility.

As a final point, EWZ’s dividends are entirely covered by underlying generation of income. As per fund management, EWZ’s underlying holdings generated 11.7% in income last November, as per its SEC yield. EWZ had an 11.7% dividend yield at the time, so dividends were fully covered by income.

EWZ

EWZ’s strong, growing 12.7% dividend yield is a significant benefit for the fund and its shareholders, and a core aspect of its investment thesis. Dividends are quite volatile, so investors should not expect steady, consistent dividend payments and growth from here on out, but dividends should be hefty regardless, and I do think long-term growth should be strong.

Cheap Valuation

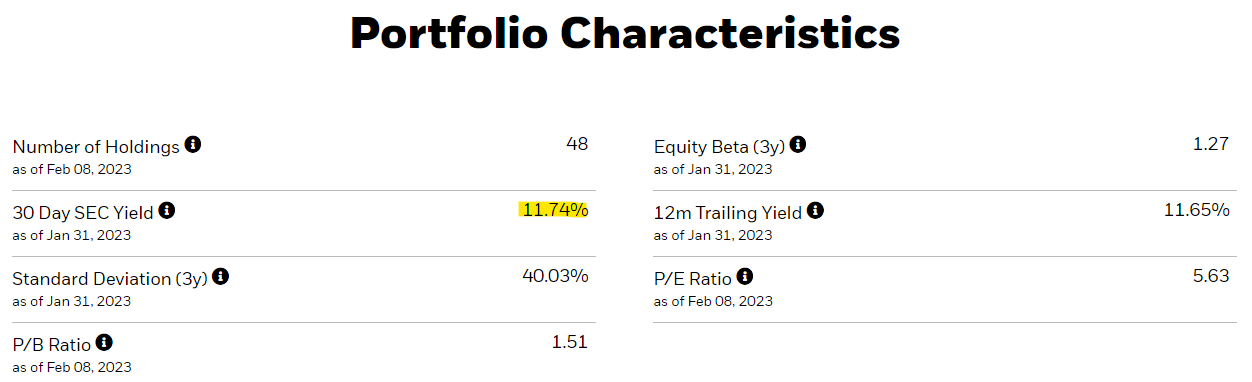

EWZ currently sports an incredibly cheap valuation, with a PE ratio of 5.6x, and a PB ratio of 1.5x. Both are incredibly low figures on an absolute basis, and lower than that of most broad-based equity indexes.

EWZ’s cheap valuation could lead to significant capital gains and market-beating returns, contingent on valuations normalizing. Valuations have started to normalize, with the most expensive/overvalued equity segments seeing significant capital losses in 2022. EWZ fared much better, being flat/very slightly down, during the year. Ideally, EWZ’s outperformance would take the form of higher capital gains/total returns, but minimizing losses is still, on net, beneficial.

EWZ’s cheap valuation could lead to significant capital gains and market-beating returns moving forward, an important benefit for the fund and its shareholders.

On a more negative note, these gains and returns are at least partly dependent on market sentiment, which is not always rational nor speedy. There is no guarantee that EWZ’s share price will increase moving forward, even assuming improved economic and industry fundamentals.

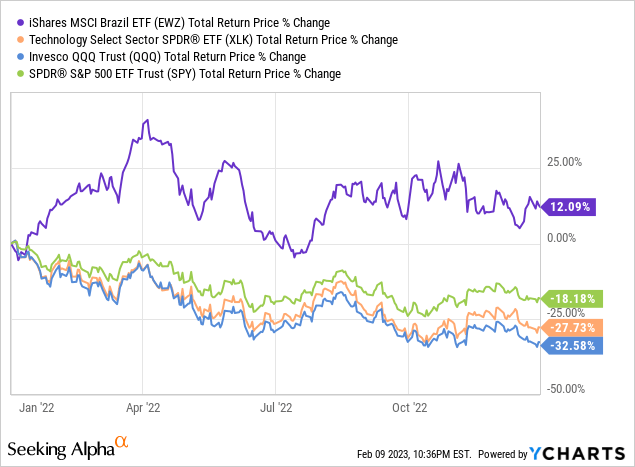

On a more positive note, dividends are not dependent on market sentiment, and EWZ does offer a strong, growing double-digit dividend yield. Said dividends help ensure a modicum of total returns even if capital gains are low or non-existent. As an example, EWZ had total returns of 12.1% in 2022, even with zero capital gains.

EWZ versus ILF

Finally, a quick comparison between EWZ and ILF.

EWZ is a Brazilian equities index ETF.

ILF is a Latin American equities index ETF.

Brazil is the largest Latin American country and economy, so ILF focuses on said country. Brazilian equities encompass almost 60% of ILF’s portfolio, with sizable allocations to Mexican equities and small allocations to equities from other countries.

ILF focuses on Brazilian equities, with investments in other similar regional countries, while EWZ exclusively invests in Brazilian equities. These are very similar strategies, and so result in very similar funds.

Both are overweight old-economy industries and commodities while being underweight tech and growth.

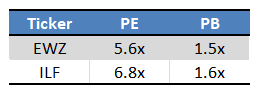

Both offer strong, growing dividend yields, with EWZ yielding 12.6% and ILF yielding 12.2%.

Both have extremely cheap valuations.

Fund Filings – Chart by Author

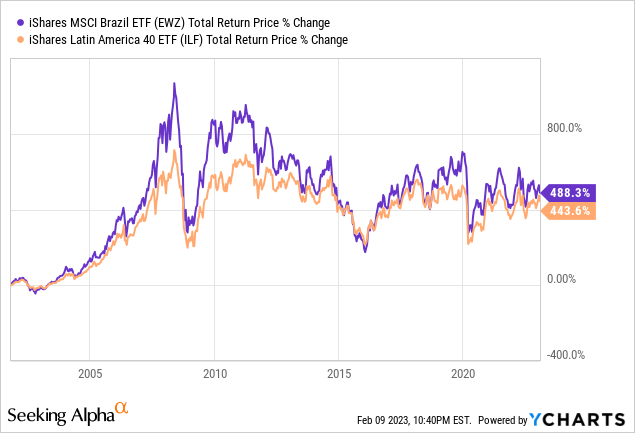

Both have extremely similar performance track records, although EWZ tends to slightly outperform.

EWZ’s fundamentals seem a bit stronger than those of ILF, across the board.

ILF is somewhat more diversified than EWZ.

In my opinion, EWZ’s stronger fundamentals outweigh ILF’s greater diversification, as Latin American equities are all strongly positively correlated, so the benefits from diversification are quite low. If Brazil is down, then Mexico will very likely be down too, so investing in both does not materially decrease risk, volatility, or potential losses for investors. Still, these are very similar funds, with very similar fundamentals and investment thesis.

Conclusion

EWZ’s strong, growing 12.7% dividend yield and incredibly cheap valuation make the fund a buy.

Be the first to comment