Delmaine Donson/E+ via Getty Images

We’re upgrading Spotify (NYSE:SPOT) to a hold after the company’s strong ending of FY2022. We previously wrote on Spotify with a sell-rating based on our expectation that the company would not be able to generate meaningful profit with the harsh macroeconomic backdrop. We’re more constructive on Spotify after the 20% Y/Y increase in monthly active users (MAU) and cost-cutting measures. Still, we believe Spotify is pressured in the near term on two fronts: figuring out how to maneuver the macroeconomic headwinds and regain pandemic growth levels. We believe Spotify’s financials will continue to be pressured in the near term due to the harsh macroeconomic environment, namely the softer ad spending and rising operating expenses. We believe Spotify’s ad-supported revenue and podcast offerings are mid-to-long-term growth drivers, but we don’t expect either to be a near-term growth driver. In the near term, we continue to believe there is more downside to be factored in before the stock provides a favorable risk-reward profile.

Still sifting through near-term headwinds

Spotify’s 4Q22 earnings report inspired confidence in the company’s FY2023, but we expect there are macroeconomic headwinds surrounding the company in the near term. While we believe Spotify will continue to show healthy added user growth, we expect the company to struggle to grow its profit margins. While the company’s 4Q22 gross margin exceeded expectations at 25.3%, Spotify’s outlook for 1Q23 is lower at 24.9%. We expect gross margins to normalize further toward 1H23.

The following graphs outline Spotify’s gross margins.

Spotify 4Q22 Shareholder Deck

We also believe it’s important to turn heads and look at Spotify’s operating expenses, which grew 44% Y/Y. We believe the company’s higher operating expenses result from the higher personnel costs and advertising expenses. As of its last quarter, Spotify’s operating expenses grew at a faster rate than the company’s total revenue. We upgraded the stock to a hold as we expect this to slowly shift to total revenue growth outweighing operating expenses, but we don’t see this switching happening in 1H23.

On the right path, but still not there

We expect Spotify is on the right path with its surprise on added users and cost-cutting measures. The company’s already joined the downsizing wave of the tech sector as it announced it’ll be cutting 6% of its employees in January. Spotify got a positive reaction from the market after the layoffs, with the stock trading higher by nearly 4% in pre-market Monday. We expect Spotify’s two growth drivers to be its ad-supported and podcast revenue. Our bearish sentiment is based on our expectations that neither will experience major tailwinds in the near term. The following outline our expectations for Spotify’s two main growth drivers:

1. Ad-supported revenues:

While Spotify’s premium revenue continues to show somewhat solid growth, with premium revenue growing 18% Y/Y, we expect the company to face resistance in growing its ad-supported revenue which grew 14% Y/Y. We believe softer pricing will pressure the company’s ad-supported revenue due to the macroeconomic headwinds. We don’t believe Spotify’s ad-supported revenue is immune to the current weaker spending environment. We expect the macroeconomic headwinds and economic slowdown have reduced growth expectations for ad spending in 2023. Interpublic Group’s (IPG) Magna forecasted ad revenue to grow 4.8% this year, down from the 6.3% growth expected for 2023 in June. We expect the slower growth in ad spending will impact Spotify’s ad revenues in 1H23.

2. Expanding as an “audio company”:

We believe Spotify is combating the macro headwinds by investing in its Podcast offerings, with podcast revenue growing in the mid-30% range Y/Y. We’re constructive on Spotify’s business maturing as more than a music streaming platform, actively making a name for itself as an audio streaming company. The podcasting market is estimated to grow at a massive CAGR of 31.2% between 2022-2030, and we believe Spotify is well-positioned to take advantage of this market in the long term. Still, we believe the podcast revenue cannot offset the macro headwinds pressuring the company’s margins in the near term.

Valuation

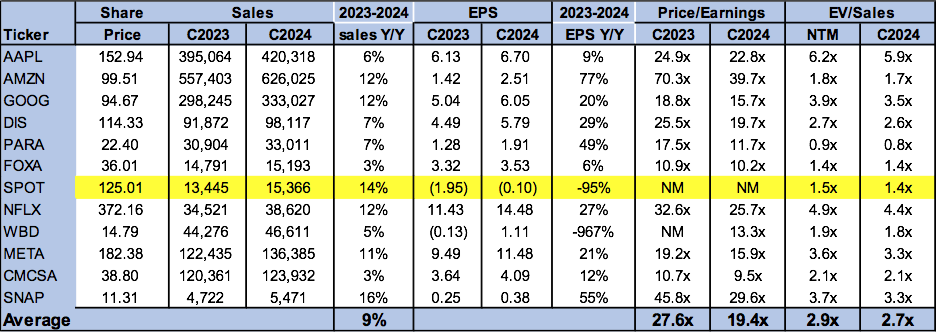

While Spotify is relatively cheap, we recommend investors against buying the stock based on weakness yet. The stock is trading at 1.4x EV/C2024 Sales versus the peer group average of 2.7x. We believe Spotify is on the right path to potentially regain pandemic growth levels but expect more downside in the near term because of the weaker spending environment.

The following table outlines Spotify’s valuation against its peer group.

TechStockPros

Word on Wall Street

Wall Street shares our bearish sentiment on Spotify. Of the 32 analysts covering the stock, 14 are buy-rated, 17 are hold-rated, and the remaining are sell-rated. The median price target for SPOT is $125, which is where the stock currently trades. The average price target is $127, meanwhile.

What to do with the stock

We’re moving Spotify from a sell to a hold. While we like the company’s added users this quarter and its cost-cutting measures, we expect Spotify is not out of the woods regarding macroeconomic headwinds triggering a weaker spending environment on consumer and advertiser fronts. We see green shoots for Spotify in the mid-to-long term, but we believe there is more downside to be factored into the stock in 1H23. Spotify stock is down nearly 29% over the past year and trading almost 30% lower than its 52-week-high of $178. We’re bullish on Spotify in the long term but don’t believe the stock provides a favorable entry point at current levels. We’re staying tuned to see Spotify’s earnings in 2H23 and expect to see the downside factored in over 1H23.

Be the first to comment