da-kuk/E+ via Getty Images

Investors are going through a rough period as inflation has soared to a 40-year high and the aggressive interest rate hikes of the Fed may cause a recession. It is thus natural that many investors consider resorting to utilities, which are resilient to recessions and can pass their increased costs to their customers. Essential Utilities (NYSE:WTRG) certainly meets these criteria. It is a high-quality Dividend Aristocrat, which has raised its dividend for 30 consecutive years and is essentially immune to recessions and inflation. Nevertheless, as the stock is almost fully valued, investors should probably wait for a correction of the stock.

Business overview

Essential Utilities is one of the largest publicly traded providers of water and natural gas in the U.S., with about 5.5 million customers across ten states. Its most important segment is its regulated water business, but it also generates a material portion of its earnings from the distribution of natural gas. Due to the seasonality of the consumption of natural gas, the company generates 65%-75% of its earnings during the first and fourth quarter.

Just like most utilities, Essential Utilities operates in an essential monopoly thanks to the regulated nature of its business and the vast amounts it has invested in infrastructure. These amounts pose essentially unsurpassable barriers to entry to potential competitors and thus offer Essential Utilities one of the widest business moats investors can hope for.

In addition, thanks to the essential nature of water and natural gas, Essential Utilities is immune to recessions. This has proved to be the case in all the recessions, including the fierce recession caused by the coronavirus crisis two years ago. While most companies were hurt by the pandemic, Essential Utilities grew its earnings per share by 7.5% in 2020 and by another 6% in 2021, to a new all-time high. The resilience of Essential Utilities to recessions is paramount, especially in the current economic environment, as the aggressive interest rate hikes of the Fed will cause the economy to decelerate and may even trigger a recession.

Moreover, Essential Utilities is expected to grow its earnings per share to a new all-time high of $1.79 this year. In the first quarter, it grew its revenue and its earnings per share by 8.5% and 6%, respectively, over the prior year’s quarter thanks to price hikes in its water segment and increased volumes in its natural gas business. Thanks to solid business momentum and the highly predictable results of this business, management reaffirmed its guidance for record earnings per share of $1.75-$1.80 this year, implying 7% growth at the mid-point.

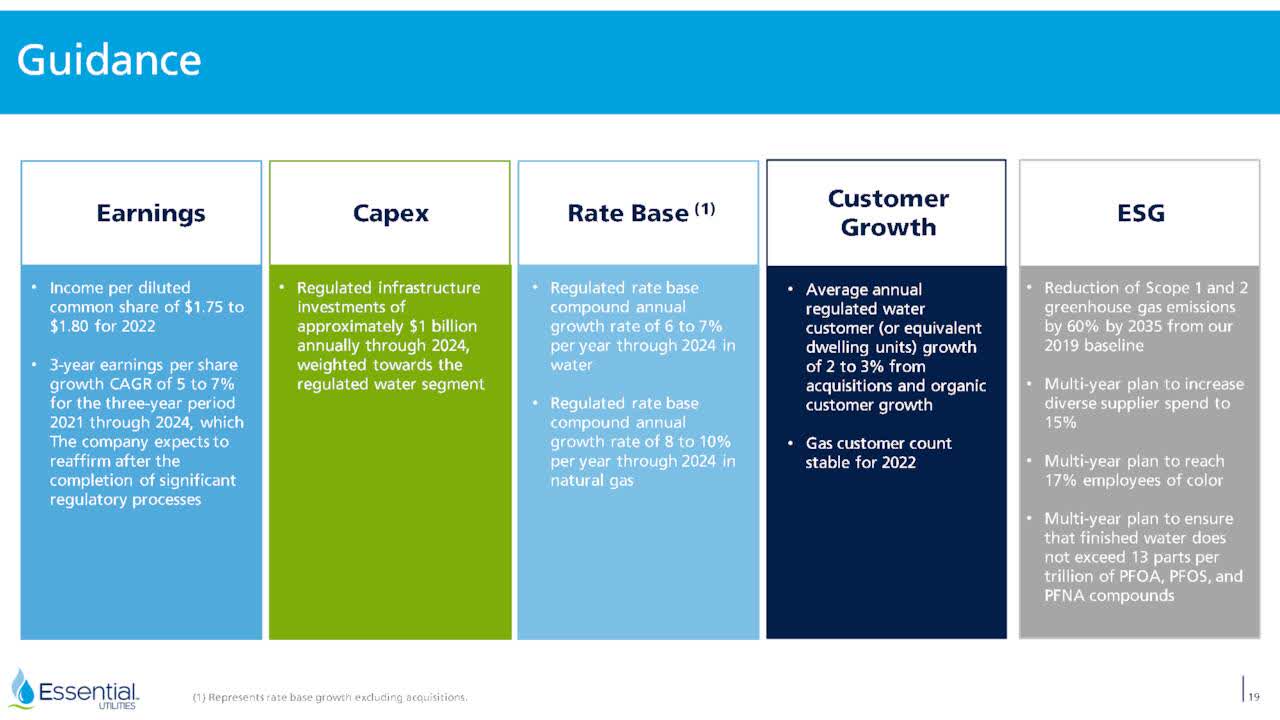

Growth prospects

Essential Utilities has one of the most consistent growth records in the investing universe. To be sure, it has grown its earnings per share in 9 of the last 10 years, at a 7.5% average annual rate. Its growth trajectory is so reliable and predictable that analysts have forecasted the earnings per share of the utility correctly (with maximum deviation of $0.01) in 12 of the last 20 quarters. In fact, analysts were almost always correct in their forecasts until Essential Utilities acquired People’s, a company that distributes natural gas, whose consumption is affected by the underlying weather conditions.

Essential Utilities has grown its earnings per share year after year thanks to the approval of rate hikes in its regulated water business and the acquisition of small water utilities, which have been assimilated in the vast network of the company. Essential Utilities has performed approximately 200 acquisitions over the last decade.

Even better, there is still ample room for future growth. The company has signed seven acquisitions, which are expected to add about 224,000 customers to its water business for a total amount of $418 million. In addition, management has identified acquisition opportunities for another 415,000 customers. Overall, Essential Utilities expects to continue growing its customer base at an average annual rate close to its historical rate of 2%-3%.

Moreover, it expects its rate base to compound at a 6%-7% average annual rate in water and at an 8%-10% average annual rate in natural gas until 2024.

Essential Utilities Growth Prospects (Investor Presentation)

As a result, the utility expects to grow its earnings per share at a 5%-7% average annual rate until at least 2024. Overall, investors should rest assured that Essential Utilities will keep growing its bottom line at an average annual rate close to its historical rate.

Dividend

Thanks to its consistent growth record, its wide business moat and its immunity to recessions, Essential Utilities has raised its dividend for 30 consecutive years. It is thus a Dividend Aristocrat.

Essential Utilities is currently offering a dividend yield of only 2.3%, but it is expected to raise its dividend in the third quarter. As management has consistently raised the dividend by 7% in each of the last five years, it is reasonable to expect the stock to offer an approximate 2.5% dividend yield from August.

Moreover, Essential Utilities has a solid payout ratio of 63% and an interest coverage ratio of 2.9. Given also its reliable growth trajectory and its resilience to downturns, Essential Utilities can easily continue raising its dividend for many more years.

Valuation

Essential Utilities is currently trading at a price-to-earnings ratio of 25.5, which is higher than the historical 10-year average of 24.5 of the stock. However, interest rates were depressed throughout most of the last decade. Therefore, given the highly inflationary environment prevailing right now, the stock is richly valued. Due to the 40-year high inflation and the resultant interest rate hikes of the Fed, the 10-year treasury yield has rallied to 3.2% this year and thus it has surpassed the 2.3% dividend yield of Essential Utilities.

Of course, the dividend of the utility is likely to rise at a mid-single-digit rate for years, but still investors are likely to be able to identify more attractive yields than the yield of Essential Utilities in an environment of rising interest rates. Therefore, investors should probably wait for a lower entry point before purchasing Essential Utilities. An attractive entry point is probably around the technical support of $40, which corresponds to a price-to-earnings ratio of 22.2 and a forward dividend yield of 2.8%-2.9%.

Final thoughts

Essential Utilities is a high-quality Dividend Aristocrat, which is expected to raise its dividend in the third quarter. It is also immune to recessions and high inflation and hence it can provide a safe haven in the challenging investing environment prevailing right now. However, the market has already appreciated the virtues of this stock and thus the latter seems almost fully valued. As a result, investors should wait for an approximate 12% correction of this slow-moving stock before purchasing it.

Be the first to comment