Marcus Lindstrom

“My own formula is very simple. It starts and ends with replacement cost because that is the ultimate game.” – Sam Zell, Equity Residential Chairman/Founder.

During the second half of 2022, investor appetite for apartment REITs has waned as interest rates have caused valuations to dip, NOI growth has slowed, and many private investors have pulled back from acquisitions.

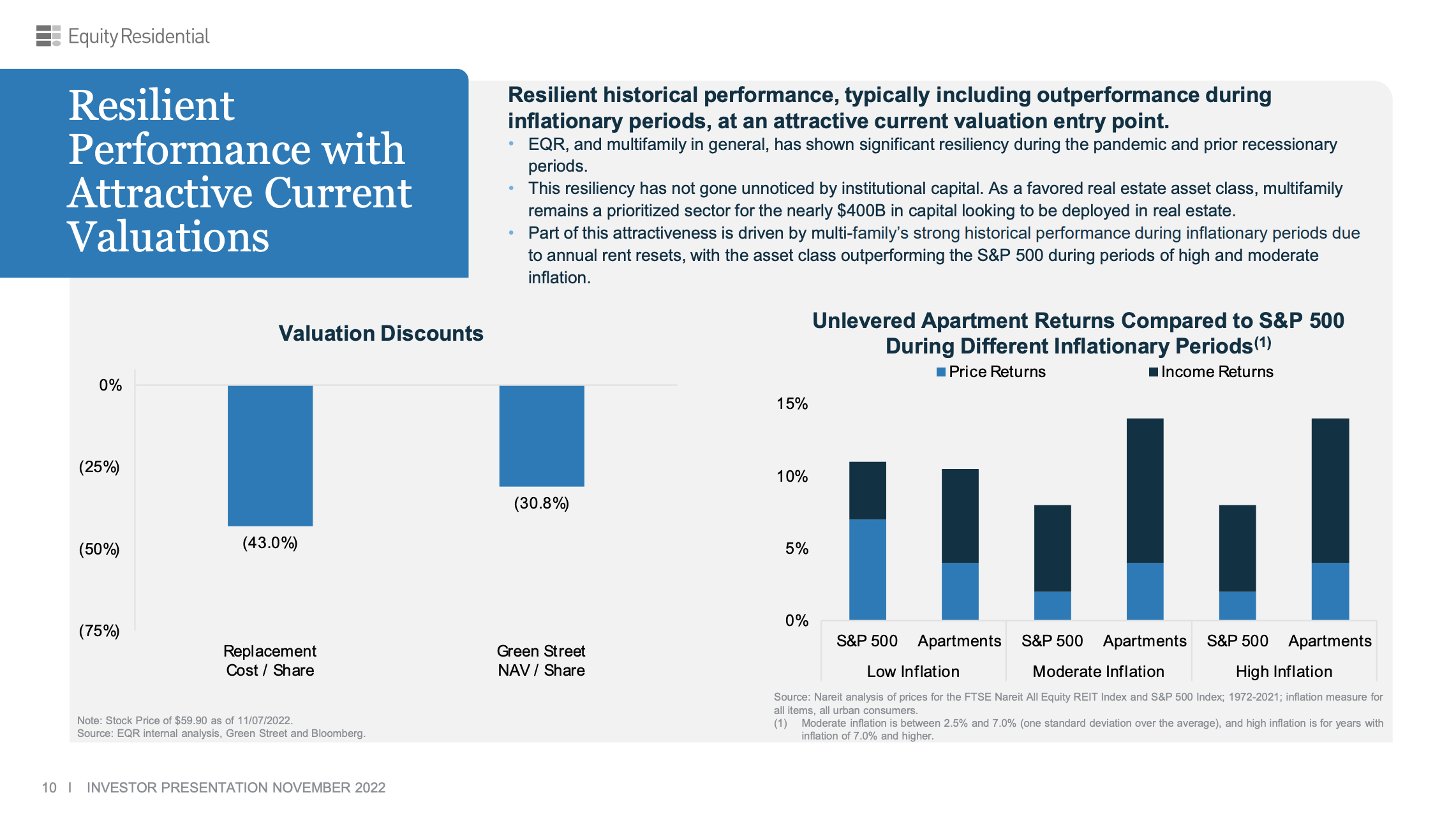

After a 35% share price decline in 2022, at $59 per share, Mr. Market is offering investors the opportunity to buy Equity Residential’s (NYSE:EQR) high quality collection of apartment assets in gateway markets for a 43% discount to replacement cost and a 31% discount to NAV (discussed below). Trading at an implied cap rate of 6% and a dividend yield of 4.2%, I see Equity Residential as an enticing investment opportunity for long-term, conservative investors.

Overview

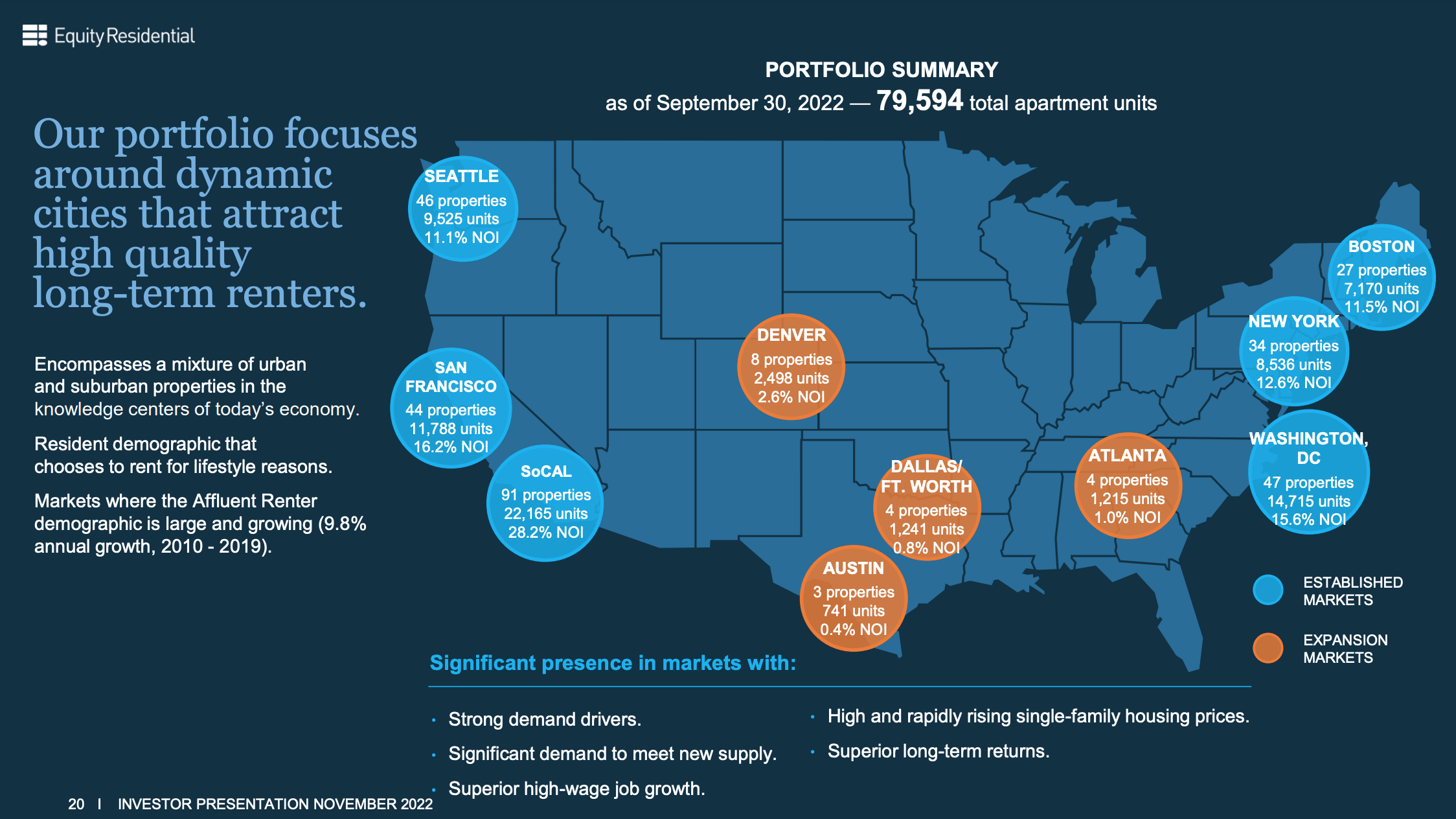

Equity Residential is one of the largest owners of gateway apartment assets in the US with nearly 80,000 apartments. While the company is primarily focused on high density coastal markets, it began to expand its geographic reach in late 2020 and has since acquired properties in sunbelt markets including Atlanta, Dallas, Denver, and Austin (as shown below these ‘new’ market represent just 5% of group NOI).

Portfolio Overview (EQR Investor Presentation)

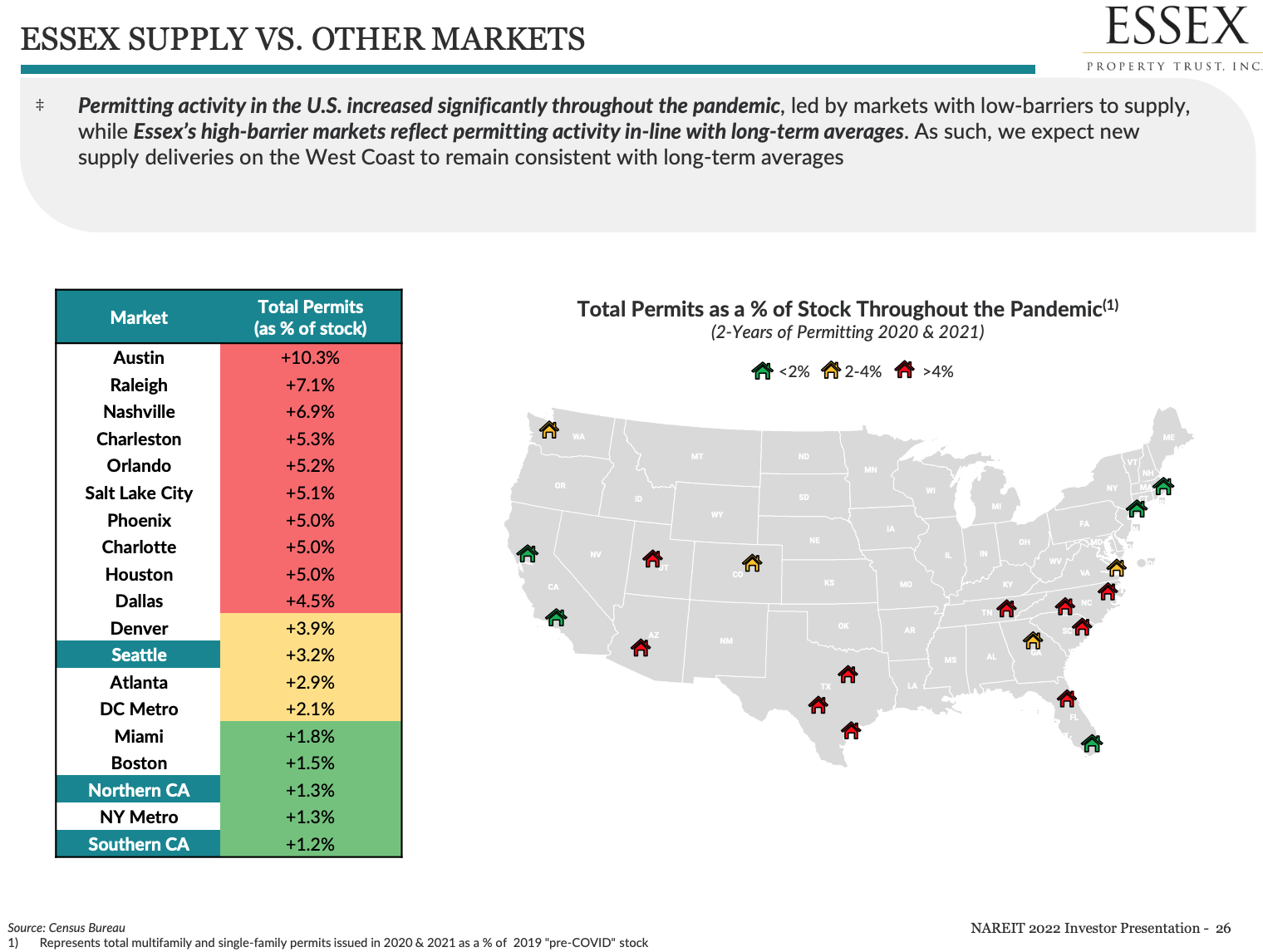

While there is an apartment building boom, as shown below, most of the expected supply increase is coming from sunbelt markets.

Supply Growth by Market (Essex Property Trust Investor Presentation)

EQR’s core coastal markets benefit from a structural lack of supply. As I discussed in my recent writeup of the Essex Property Trust (ESS), it is both difficult and costly to build new apartments in California (CA represents 42% of EQR’s NOI).

EQR also benefits from a high propensity to rent in its core markets driven by stratospheric costs of home ownership in places like California, Boston, and New York (further exacerbated by higher mortgage rates). The inability of renters to transition to home ownership creates a large captive pool of renters.

Current Results

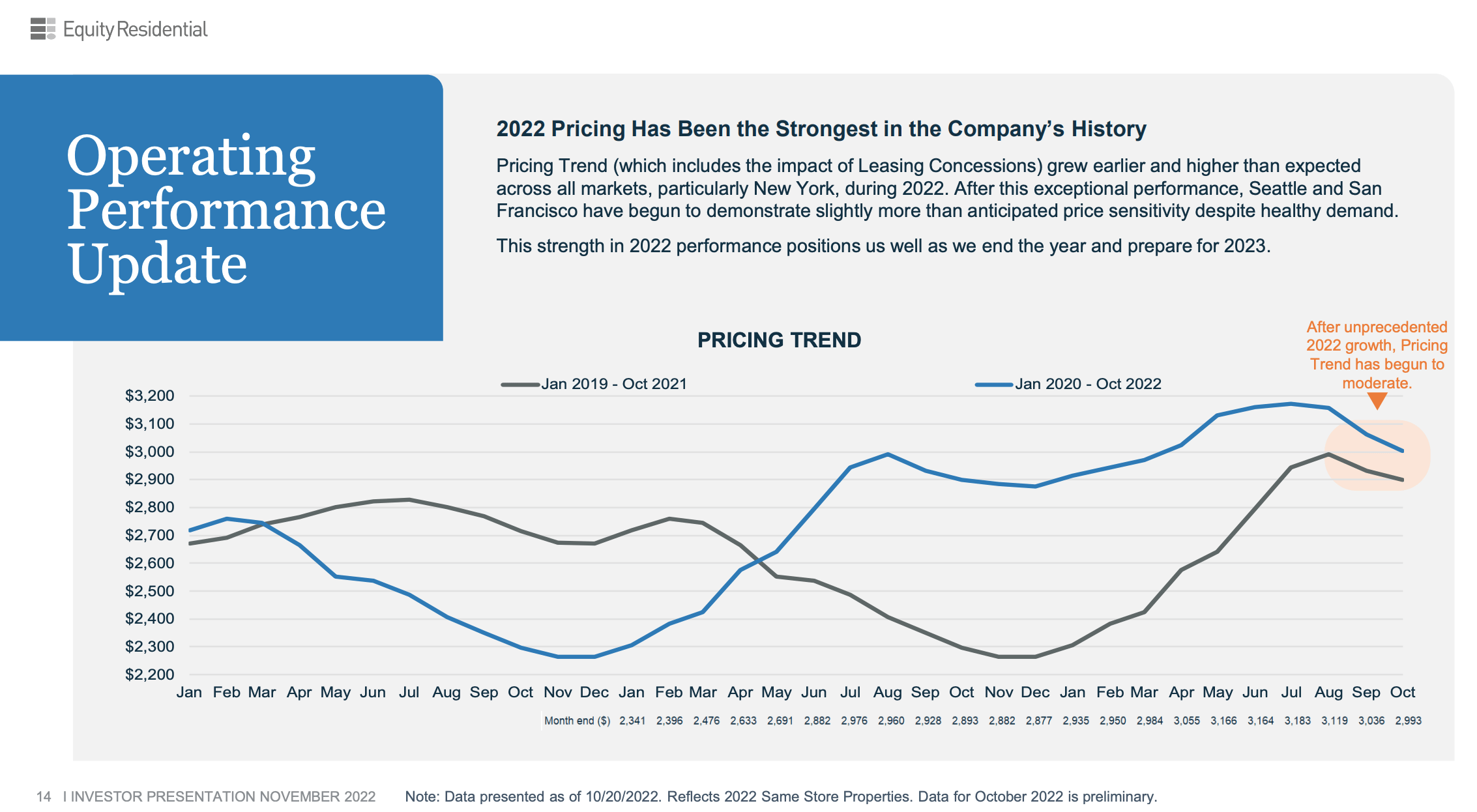

While its share price suffered, as shown below, 2022 was an exceptional year as NOI is poised to increase 14% over 2021 levels as both rents increased dramatically in EQR’s key markets.

EQR Rent Trends 2020-22 (EQR Investor Presentation)

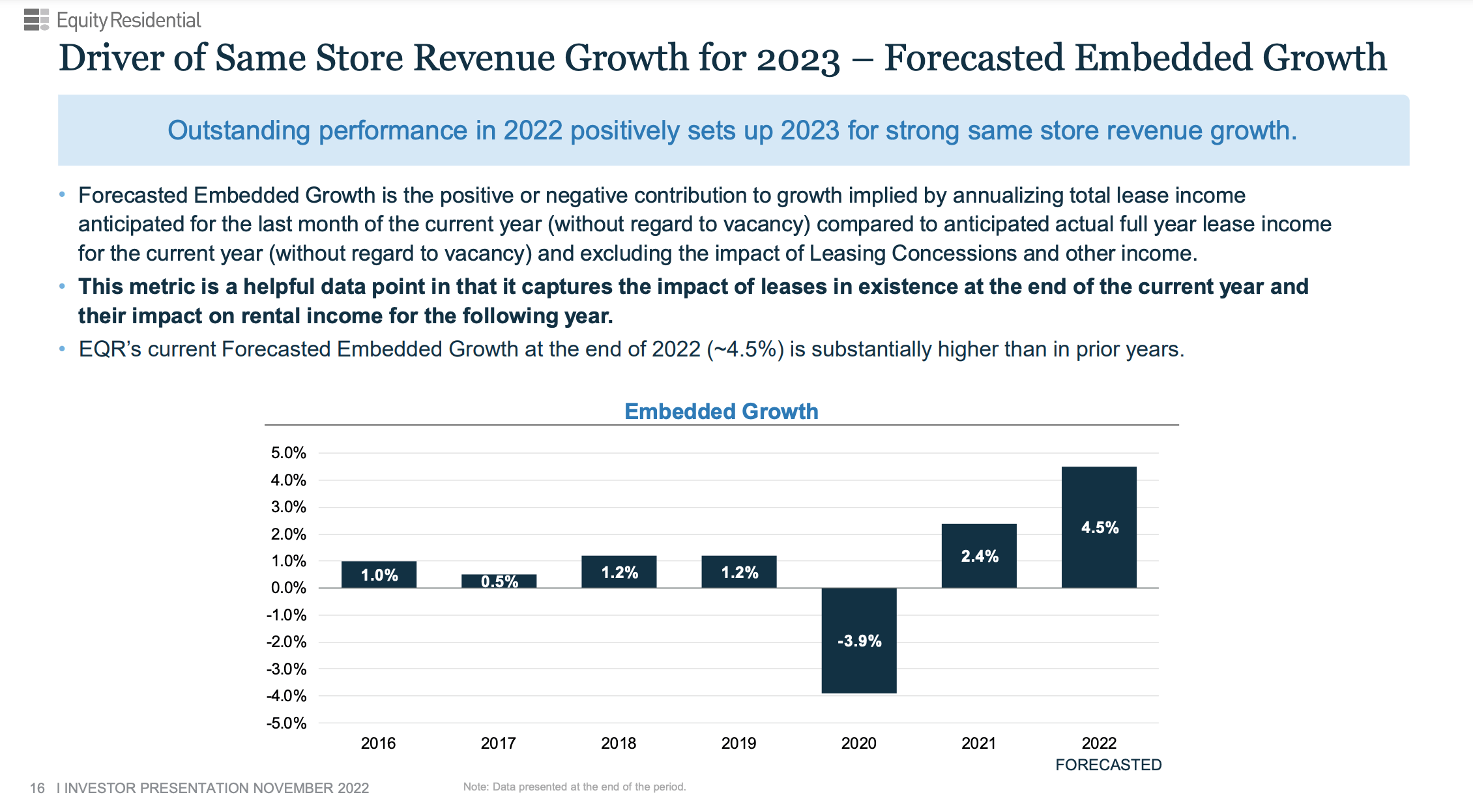

While rent growth has moderated (year over year) and seasonality has returned (rents tend to soften in 4Q as move activity is subdued), the sharp rise in rents throughout most of 2022 portend further strength in 2023. As shown below, in 2023 – EQR management sees an ‘earn in’ of 4-5% as achieved rental growth will have a full year P&L impact.

Embedded Revenue Growth (EQR November Investor Presentation)

NOI should actually increase faster than revenue given EQR’s significant exposure to California and Massachusetts – these states have limitations (2 and 2.5%, respectively) on annual property tax increases (property taxes are the largest expense component for apartments) which leads to positive operating leverage.

Valuation & Conclusion

Equity Residential Discount to Replacement Cost/NAV (Equity Residential November Investor Presentation)

As shown above, Equity Residential estimates that its shares trade at a 43% discount to replacement cost ($103/share). Replacement cost is defined as the current cost to build new buildings of equivalent characteristics and quality. It can be higher or lower than the current market value of the buildings. As we sit today, replacement cost is ~21% above estimated current market value. In the slide above, market value is estimated by commercial real estate boutique Green Street Advisors which sees EQR at a ~31% discount its $85/share NAV (which imputes a 4.5% cap rate).

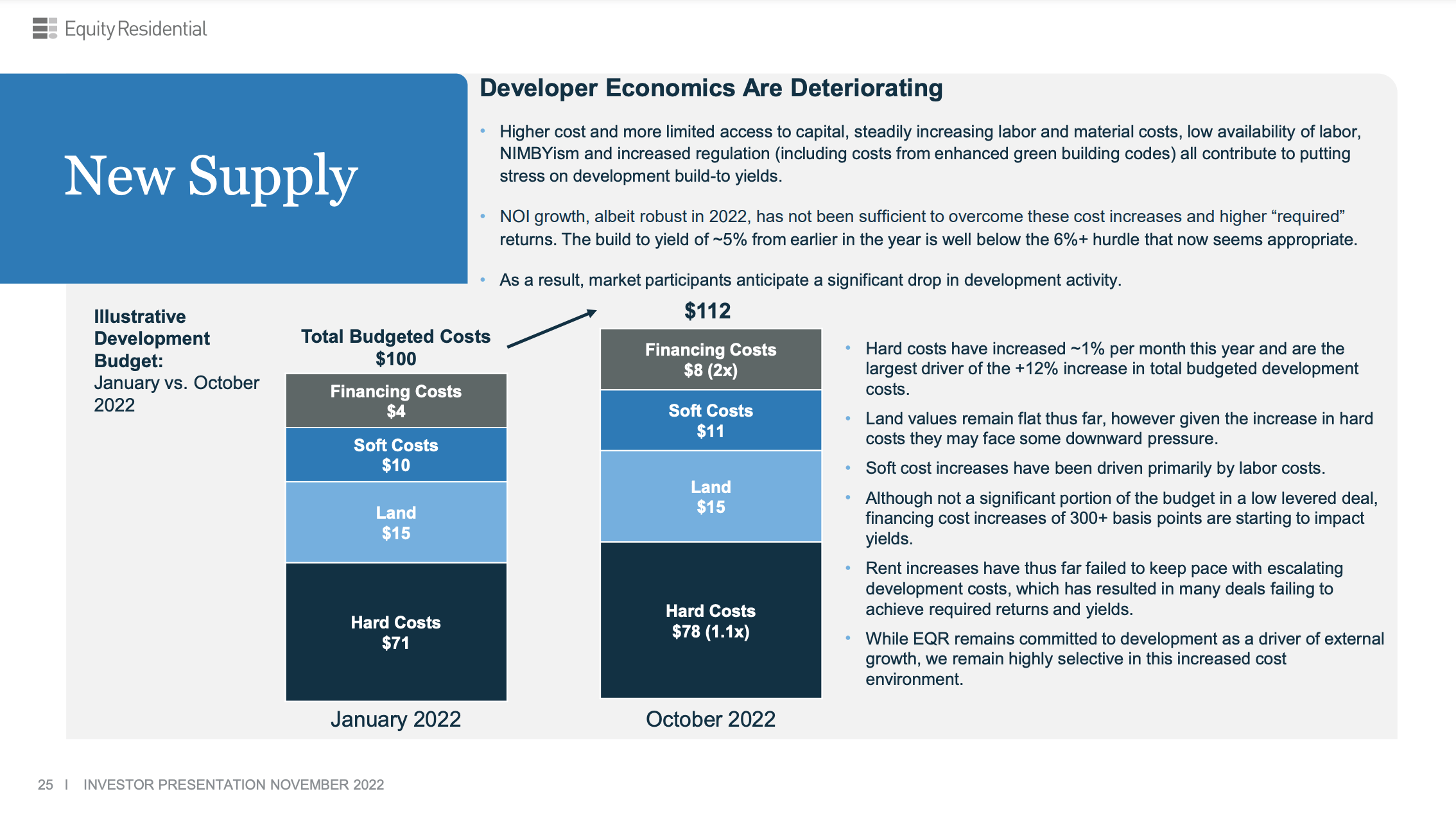

The recent divergence between market value and replacement cost is due to the decline in apartment asset values (driven by higher interest rates/more difficult financing environment) while replacement costs have risen due to escalating construction costs (driven by building cost inflation which has exceeded overall inflation) as shown below.

Increased Cost to Develop (EQR Investor Presentation )

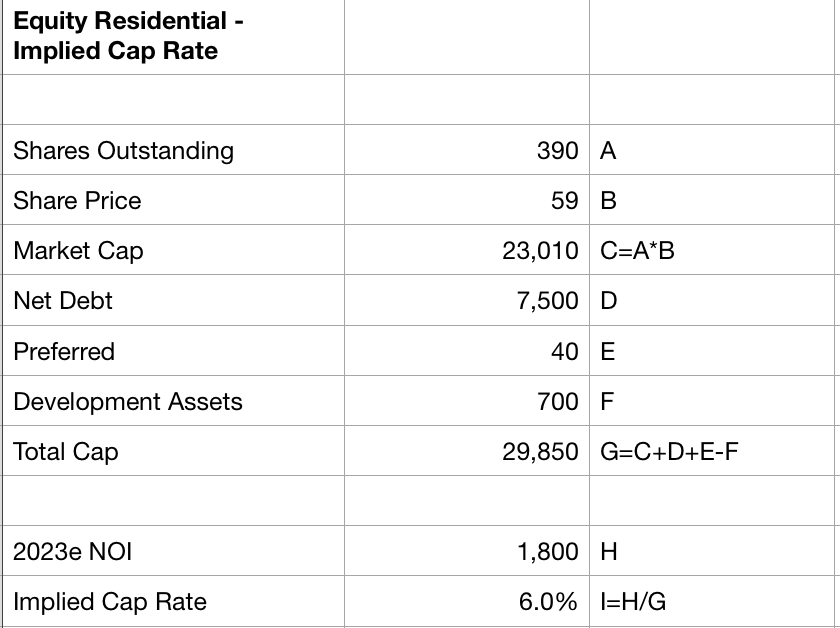

While replacement cost is always an important consideration in making the optimal decision of whether to buy existing assets or develop new apartments, in today’s environment of limited price discovery (massive slowdown in private market apartment transactions), it holds even greater importance. Cap rates (NOI yield) tend to be fluid and dependent on NOI growth expectations, interest rates, and fund flows (demand by investors for apartment assets). Conversely, construction costs, which determine replacement cost, tend to be sticky. While an economic slowdown could lead to a decline in building material (immaterial thus far) and labor costs, in the absence of an economic depression, the overall cost to develop buildings in EQR’s core coastal markets is unlikely to decline significantly. Similarly, I believe that EQR’s valuation is attractive when viewed on an implied cap rate basis. Historically EQR has traded at an implied cap rate of 3.8-6% over the past decade. At $59/share, Equity Residential trades at the low end (highest implied cap rate) of its ten year historical range.

Equity Residential Implied Cap Rate (Company Filings; Author Estimates)

Assuming EQR trades back up to NAV within the next 4-5 years (EQR traded at or above NAV in 2014-2016, 2019 and again in 2021-1Q22), after factoring in the dividend, investors can expect a 13-14% annualized return. I view this as being very attractive given the company’s high quality collection of assets in supply constrained markets and low level of financial leverage (4.5x net debt to EBITDA; 25% loan-to value).

Be the first to comment