Leestat

Introduction

The share price of Valero Energy (NYSE:VLO) saw a very strong rally in early 2022 on the back of the Russia-Ukraine war that handsomely rewarded their shareholders but as my previous article warned, their shares were looking exorbitantly expensive with potential for large losses. Whilst the share price is still around this same level right now, albeit after a bumpy ride, it seems that 2023 will be a story of Russia versus the economy as upcoming sanctions on the former effectively fight against a gloomy economic outlook.

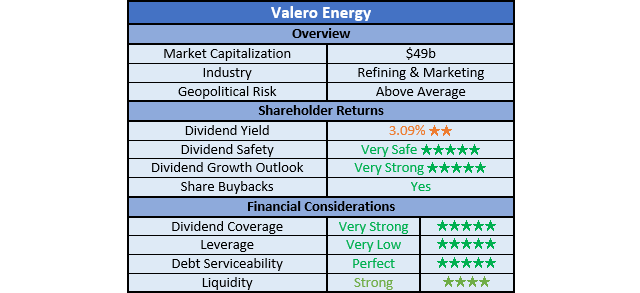

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

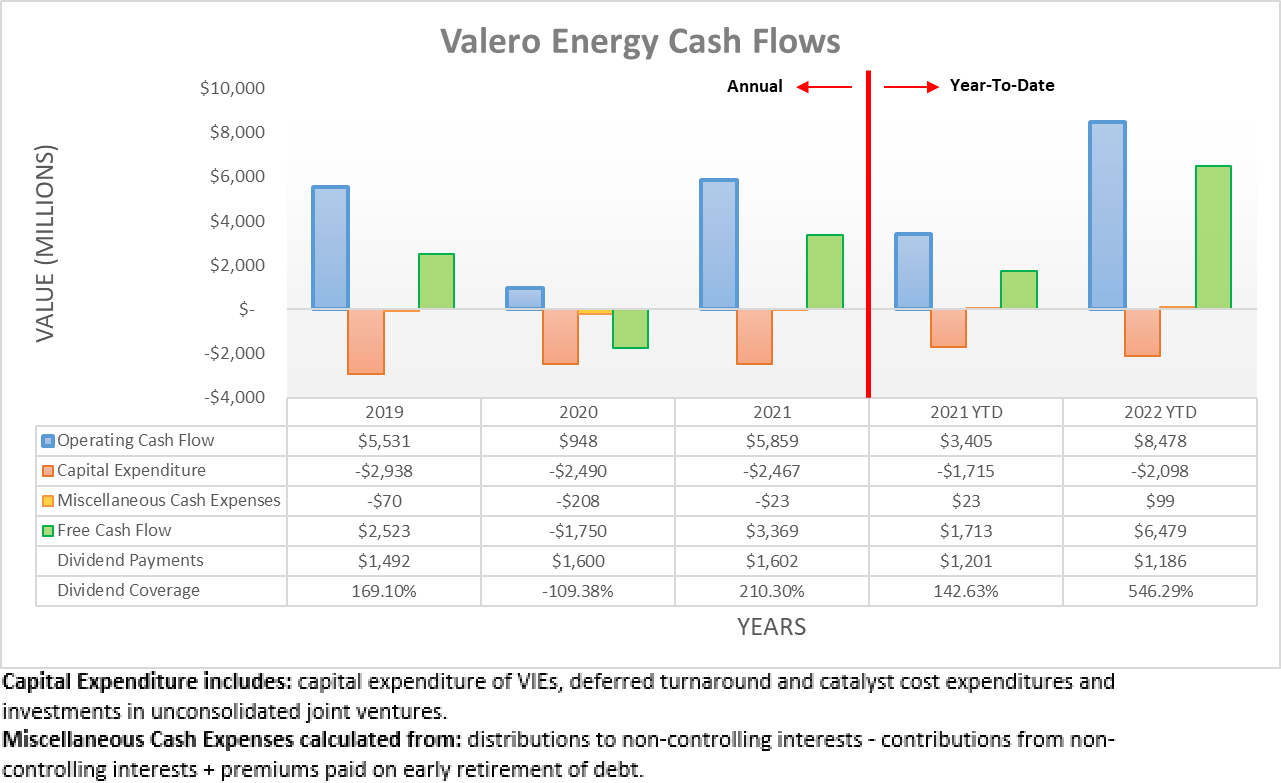

Despite their very strong start to the year, it turns out the first quarter of 2022 was barely a blip on the radar compared to what was laying ahead during the second and third quarters, as refining margins hit levels never-thought-possible on the back of the Russia-Ukraine war. As a result, their operating cash flow during the first nine months climbed to a massive $8.478b, an almost unthinkably high result merely one year ago. Since their capital expenditure remained modest, this resulted in record-setting free cash flow of $6.479b. Whilst their operating was already more than twice their previous result of $3.405b during the first nine months of 2021, they still had more fuel left in the tank, metaphorically speaking.

Author

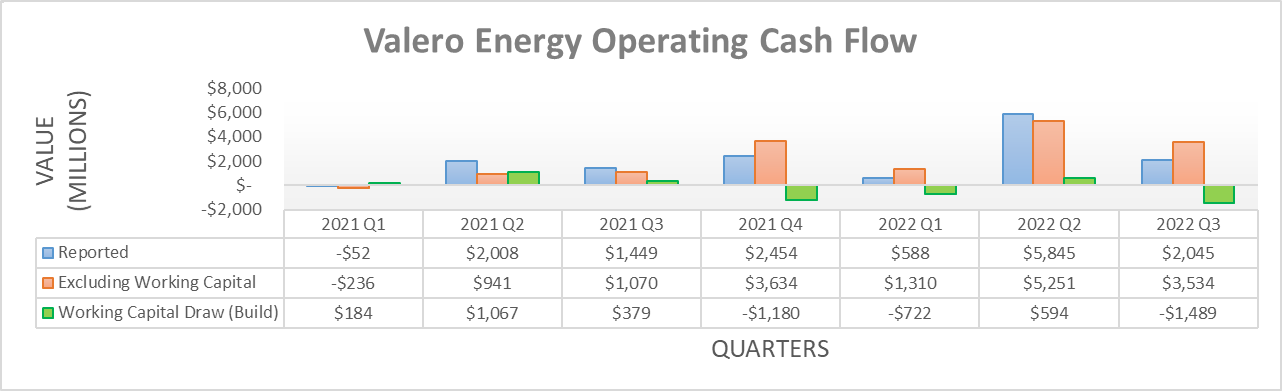

If viewing their operating cash flow on a quarterly basis alongside their working capital movements, it shows their already massive result during the first nine months of 2022 was actually weighed down to a material extent. Once aggregating these quarterly movements, it equals a net working capital build of $1.617b and thus if not for this hindrance, their underlying operating cash flow was even higher at $10.095b. Despite their cash flow performance easing during the third quarter of 2022 versus the second quarter, their underlying operating cash flow of $3.534b was still a massive result, historically speaking. As for their upcoming fourth-quarter results, they should remain strong given the concurrent supportive operating conditions, even if they happen to ease further once again.

When looking ahead into 2023, there are two competing forces fighting each other at opposite sides of the bull and bear spectrum. On the former side, it is the upcoming sanctions that are being levied by Europe against Russia that as of the 5th of February 2023 will prohibit the purchase of their refined product exports, much in the same way as their 5th of December 2022 ban on seaborne oil exports. If this proves effective, this will further pull more gasoline, diesel and so forth away from an already tight market, thereby supporting prices and thus, refining margins across the globe. As we know from 2022, geopolitical events have an extremely potent capacity to drive their financial performance.

Although on the bear side, this bullish catalyst is occurring in conjunction with a gloomy economic outlook as most of Europe and North America face prospects of a recession. Or if not, it still appears that weaker economic conditions are more likely than not as central banks fight inflation with the tightest monetary policy in over a decade. It is widely known that weaker economic conditions are directly linked to lower refined product demand and obviously, weaker margins.

Whilst these dynamics are clear in a qualitative sense, alas how they intersect in this never-before-seen situation nevertheless remains impossible to quantify with accuracy. If the early signs of the sanctions on Russian seaborne oil exports are used as a guide for what to expect for refined products exports post-February 2023, the drop off in exports should have a material benefit. Although, as the hypothetical resulting higher fuel prices would contribute to higher inflation, their ‘benefit’ would result in even tighter monetary policy than otherwise would have been the case. In turn, this could possibly offset the benefit as subsequent months pass heading into the second half of 2023. Sadly, no one can say with certainty how these competing forces will transpire but at least if nothing else, their financial position is solid and ready for either outcome.

Author

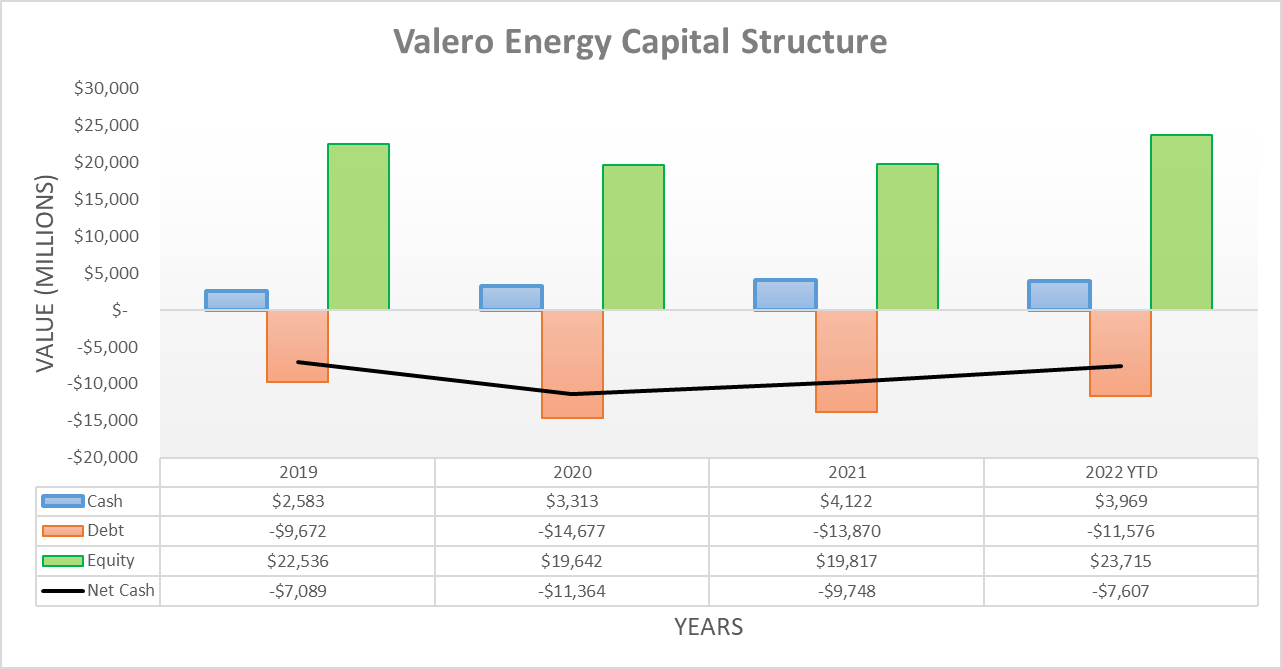

Thanks to their record-setting free cash flow during the second and third quarters of 2022, they managed to shave away almost $3b of net debt, which is a truly impressive feat, especially given their accompanying share buybacks that totalled $2.625b. As a result, this now sees their net debt landing at $7.607b versus its previous level of $10.523b following the first quarter, thanks in part to their cash balance swelling to $3.969b versus $2.638b across these same two points in time. The upcoming results for the fourth quarter of 2022 and forthcoming quarters in 2023 should see their net debt continue its downward trajectory since they wish to push their net debt-to-capitalization towards the bottom of their targeted range, as per the commentary from management included below.

“On a long-term debt to cap — net debt to cap, we have a 20% to 30% range that we target. We’re at 24.5% now at the end of the third quarter…”

“I’d like to be even lower, you’d like to be at the 20% range to give you more financial flexibility going forward.”

– Valero Energy Q3 2022 Conference Call.

Until such time as they reach this target, they will continue varying their share buybacks to return between 40% and 50% of their free cash flow to their shareholders with the remainder obviously retained for deleveraging. Once hitting their 20% net debt-to-capitalization target, there was no discussion about lifting their shareholder returns to 100% of their free cash flow. This means their net debt should still continue its downward trajectory during 2023 and possibly beyond, even if their shareholder returns are pushed relatively higher once hitting this target. Admittedly, if the world experiences a downturn that is far more severe than expected, this could potentially change but as it stands right now, they should still produce free cash flow regardless of whether sanctions on Russia prevail in this metaphorical fight.

Author

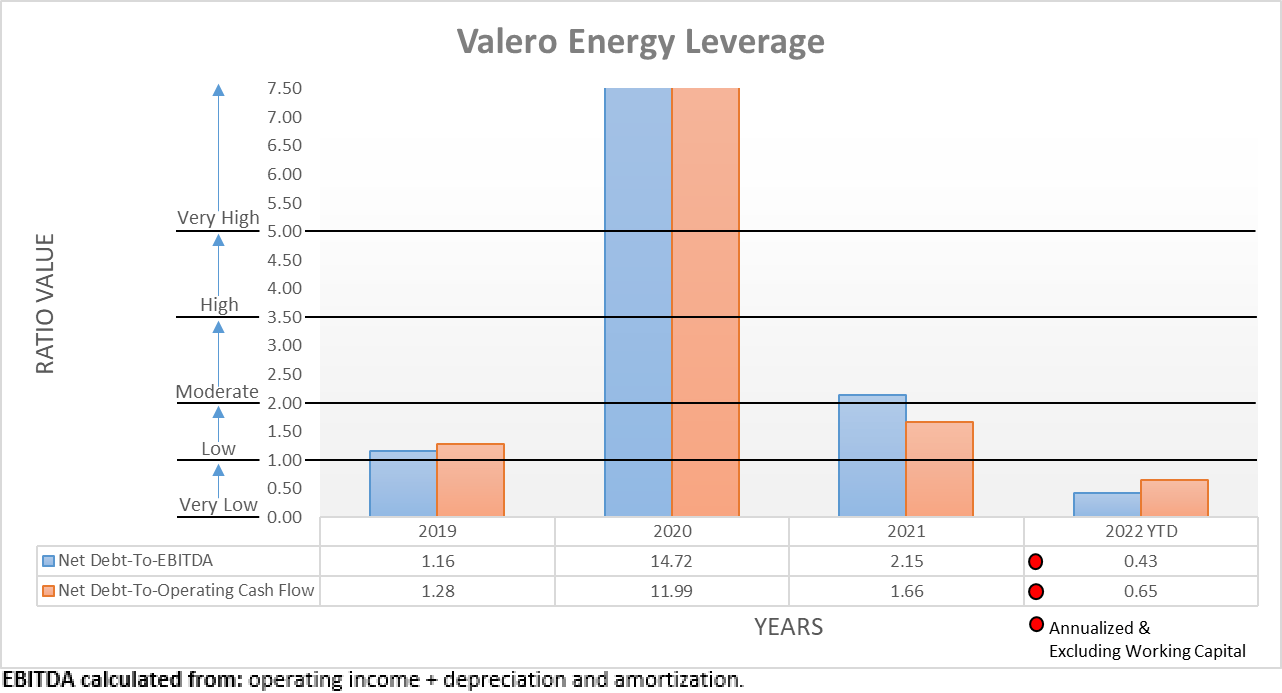

Naturally, their lower net debt and booming financial performance during the second and third quarters of 2022 translated into significantly lower leverage. Consequently, their net debt-to-EBITDA plunged to 0.43 versus their previous result of 1.32 following the first quarter, whilst their net debt-to-operating cash flow landed at 0.65 and 2.00 across these same two points in time. In both instances, their leverage is now firmly within the very low territory and going forwards, this will continue to be impacted by their volatile financial performance. Although, as their net debt continues its downward trajectory, it places downward pressure upon their leverage going forwards, relative to the prevailing operating conditions.

Author

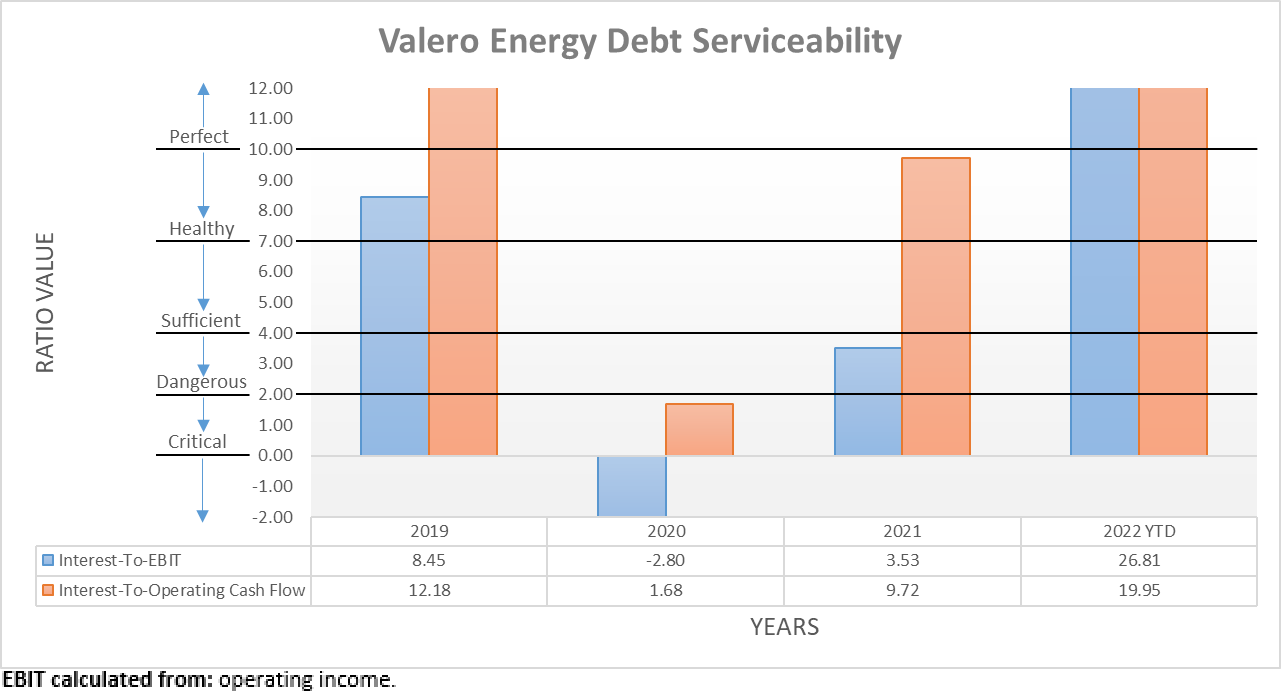

Unsurprisingly, the same driving forces influencing their leverage also played a sizeable role in their debt serviceability, which is timely given central banks have been rapidly tightening monetary policy during the second and third quarters of 2022. In fact, their interest expense during the third quarter was $138m and thus actually down around almost 10% year-on-year versus their previous expense of $152m during the third quarter of 2021, despite the higher interest rates, thanks to their lower net debt. As a result, their interest coverage is a perfect 26.81 when compared against their EBIT versus its previous result of 9.54 following the first quarter. Plus, the accompanying comparison against their operating cash flow sees a similar result of 19.95. Importantly, going forwards this should move downwards alongside their leverage, thereby further enhancing their resilience to downturns.

Author

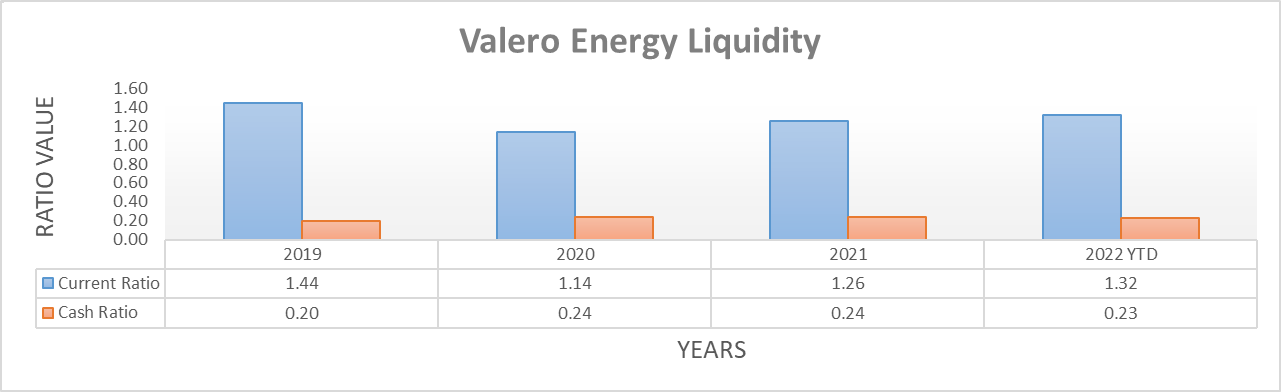

Nothing quite benefits liquidity as positively as cash generation, especially free cash flow and as we know, the second and third quarters of 2022 certainly did not disappoint on this front. Thanks to their cash balance swelling, it lifted both their current and cash ratios to 1.32 and 0.23 respectively, which are modestly above their previous results of 1.18 and 0.13 following the first quarter. Once combined with their large operational size, it alleviates any issues surrounding debt maturities or credit facility availability in the foreseeable future, regardless of where monetary policy heads.

Conclusion

Even though their share price ultimately performed better than expected back around the middle of 2022, it nevertheless was far from a stellar investment as volatility made for a bumpy ride. As we open the books for the new year ahead, their direction depends upon which of the competing forces has a greater impact, namely the upcoming sanctions on Russia or the gloomy economic outlook. This is a flip-a-coin situation in my eyes because both geopolitics and economics are notoriously difficult to predict and therefore, I am upgrading my rating from sell but at the same time, I remain cautious with their share price not far from record-setting levels and thus believe that a hold rating is now appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Valero Energy’s SEC Filings, all calculated figures were performed by the author.

Be the first to comment