naphtalina/iStock via Getty Images

We all tend to think that if your stock or fund is acquired that would be a good thing since any unlocked value would be realized.

But in the case of the Delaware Investments Dividend & Income Fund (NYSE:DDF), $8.41 current market price, that wasn’t the case and shareholders are left wondering what just happened to their fund that was trading at about par valuation one day and then a -9% discount a week later.

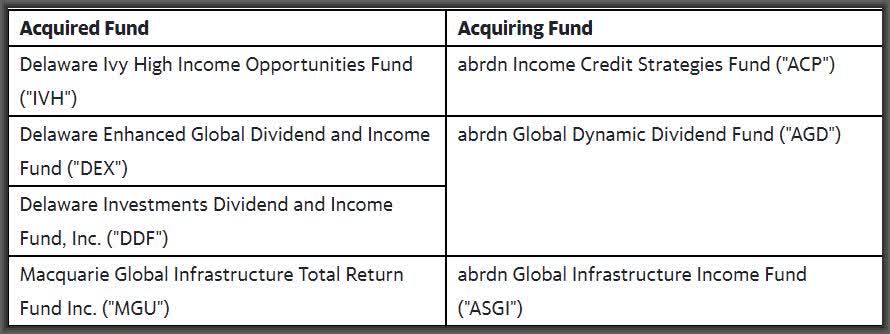

Through no fault of the fund, the Board of Directors of DDF agreed that three Delaware funds, i.e. DDF along with the Delaware Enhanced Global Dividend & Income Fund (DEX), $7.65 current market price and the Delaware Ivy High Income Opportunities Fund (IVH), $11.48 current market price, would be acquired by two Aberdeen funds, the Aberdeen Global Dynamic Dividend Fund (NYSE:AGD), $9.36 current market price, and the Aberdeen Income Credit Strategies Fund (ACP), $7.84 current market price.

Here’s a summary of the proposed mergers from the Aug. 11 press release:

Note: I’m leaving out the Macquarie Global Infrastructure Total Return fund (MGU) merger into the Aberdeen Global Infrastructure Income fund (ASGI) since they were essentially a merger of equal valuations

Aberdeen

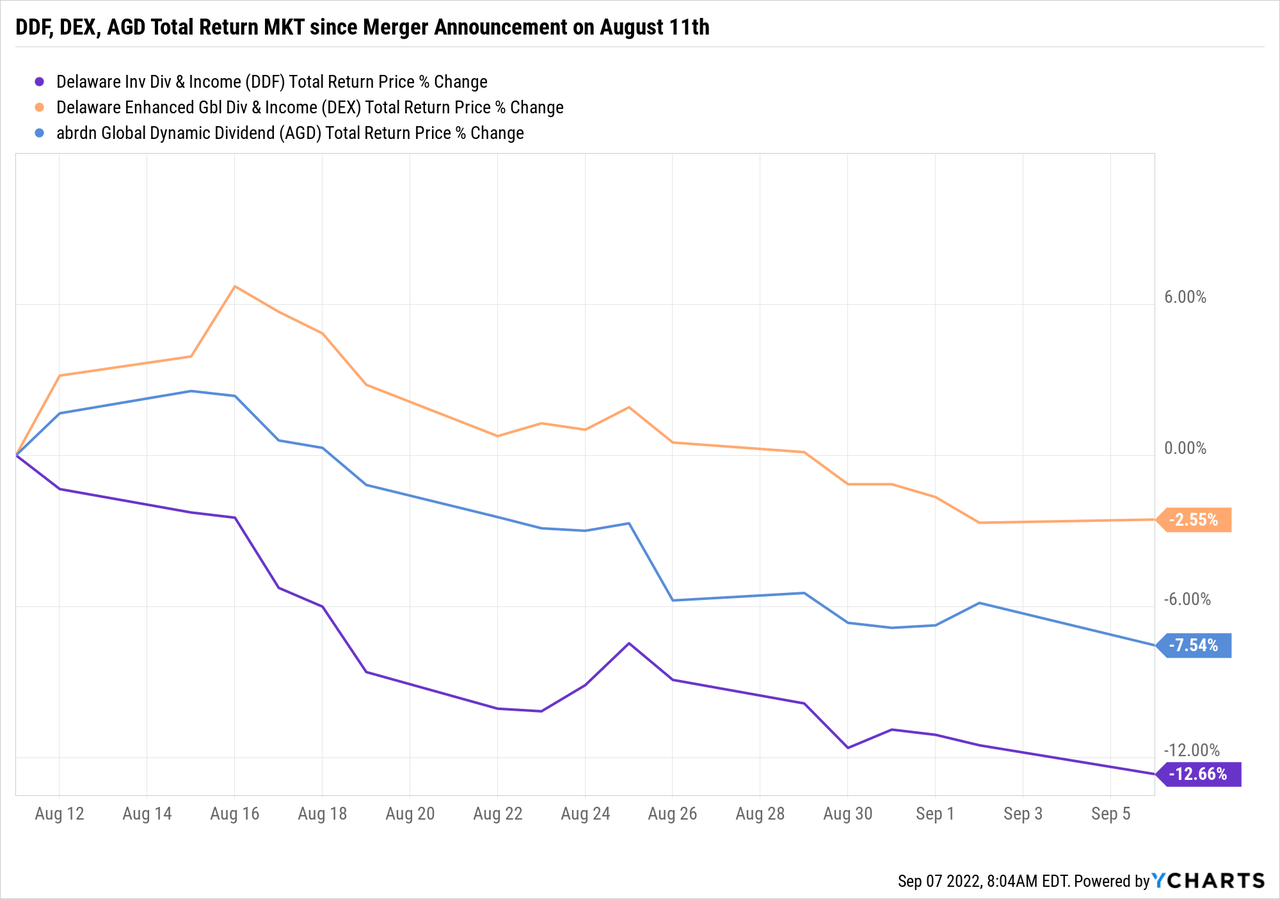

On the day of the merger announcement, DDF was trading at a slight 0.1% premium while DEX was trading at a -14.4% discount. So just what do you think was going to happen when the acquiring fund, AGD was trading at a -10.0% discount?

That’s right. Within one week, DDF had dropped to a -9% discount, while the other fund, DEX had moved up from a -14.4% discount to about a -9% discount also. Good for DEX shareholders but a disaster for DDF shareholders.

Here’s a market price graph of what has happened since the Aug. 11 merger announcement:

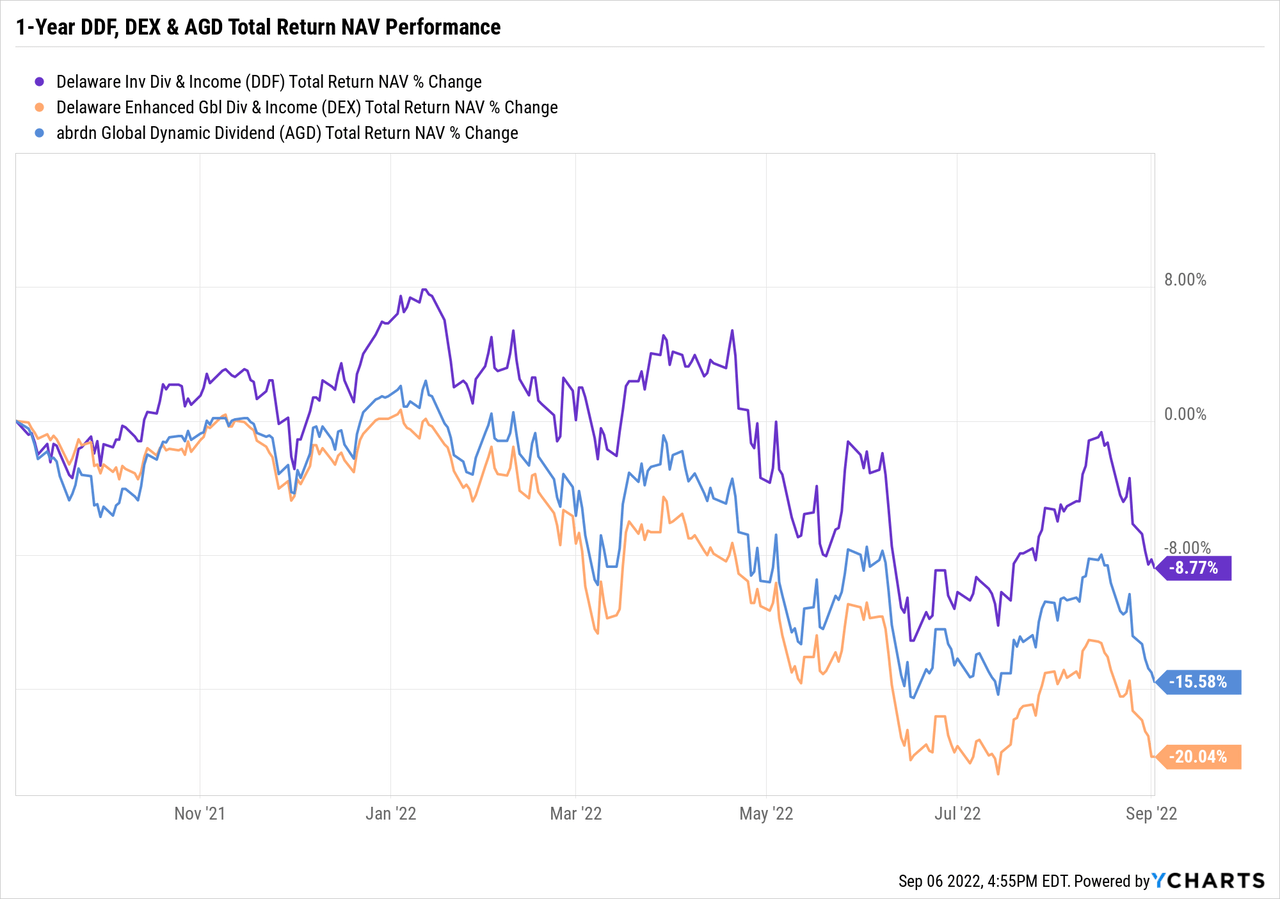

What makes this even worse is that DDF had been outperforming AGD and DEX over the past year at total return NAV. In fact, it’s not even close:

So tell me, why should DDF shareholders have to bite the bullet and suffer a roughly -10% valuation drop just to make this merger work when DDF was doing fine on its own?

Well, they don’t have to. From the Aug. 11 press release:

It is currently expected that each Reorganization will be completed in the first quarter of 2023 subject to (i) approval of the Reorganization by the respective Acquired Fund shareholders, (ii) approval by the respective Acquiring Fund shareholders of the issuance of shares of the Acquiring Funds, and (iii) the satisfaction of customary closing conditions. No Reorganization is contingent upon any other Reorganization.

Maybe in a bull market, one could accept the take-under terms even if they were a slap-in-the-face to DDF shareholders. But in a bear market in which DDF was already down -12.8% YTD (still outperforming the broader markets), this merger proposal has resulted in DDF dropping another -10% through no fault of the fund.

This is unacceptable and I, for one, will NOT be voting for this merger later this year. If the Board of Directors of DDF want to give the fund’s assets away to another fund, do it at a fair valuation for DDF shareholders. Because right now, DDF shareholders have been thrown under the bus.

Be the first to comment