winyuu

Investment Thesis

EOG Resources (NYSE:EOG) is one of the biggest oil and natural gas exploration and production companies.

The core of the bull case revolves around its +6% dividend yield. But as we go beyond its yield and think about its core business, there’s a lot to be compelled about here.

Here’s why I’m bullish on EOG.

EOG’s Exposure to Energy Markets

Slightly over half of EOG’s revenues come from crude oil and condensates. The other side of its business includes natural gas and natural gas liquids (”NGL”). While the final business unit is its Gathering, Processing, and Marketing segment.

In the graphic that follows, we see a rough approximation of how its exposure breaks down.

Author’s work, Q3

Note, the graphic above is an approximation and doesn’t include hedge losses or adjustments.

Vaguely speaking, EOG’s Gathering, Processing, and Marketing segment is responsible for the extraction, transport, and preparation of both oil and natural gas that EOG produces to be sold to the market.

So, one could argue that exposure to the oil market goes beyond 60% of its business.

Thus, as we progress with the remainder of this analysis, I highlight what I believe is holding back the bull case and how we should think about EOG’s near-term prospects.

What’s Happening Right Now?

The oil market doesn’t appear to be moving much. It dropped substantially since EOG reported its Q3 results, at which time its average WTI achieved In the quarter was $92.

Since then, we’ve seen WTI prices fall significantly. But WTI pricing appears to be hovering close to $80 WTI at the time of writing. This tells me that the potential weakness in the bull case does not stem from the WTI market, but rather from the natural gas market.

So, with that in mind, I’ll now turn our focus to discussing EOG’s near-term prospects from the natural gas and natural gas liquids market.

What we’ve seen in the last few weeks is that natural gas prices have tumbled in the US. This was predominantly due to the following four factors:

- Unseasonably warm winter in both the US and Europe, led to a drop in natural gas demand.

- Surging supply of LNG from the US to Europe and Asia, led to an oversupply of LNG. Particularly as Asia has also rerouted excess LNG to Europe.

- Ramp-up in thermal coal consumption in Europe

- Many industries, for example, fertilizer or glass-making companies cutting back production, as energy become uneconomic.

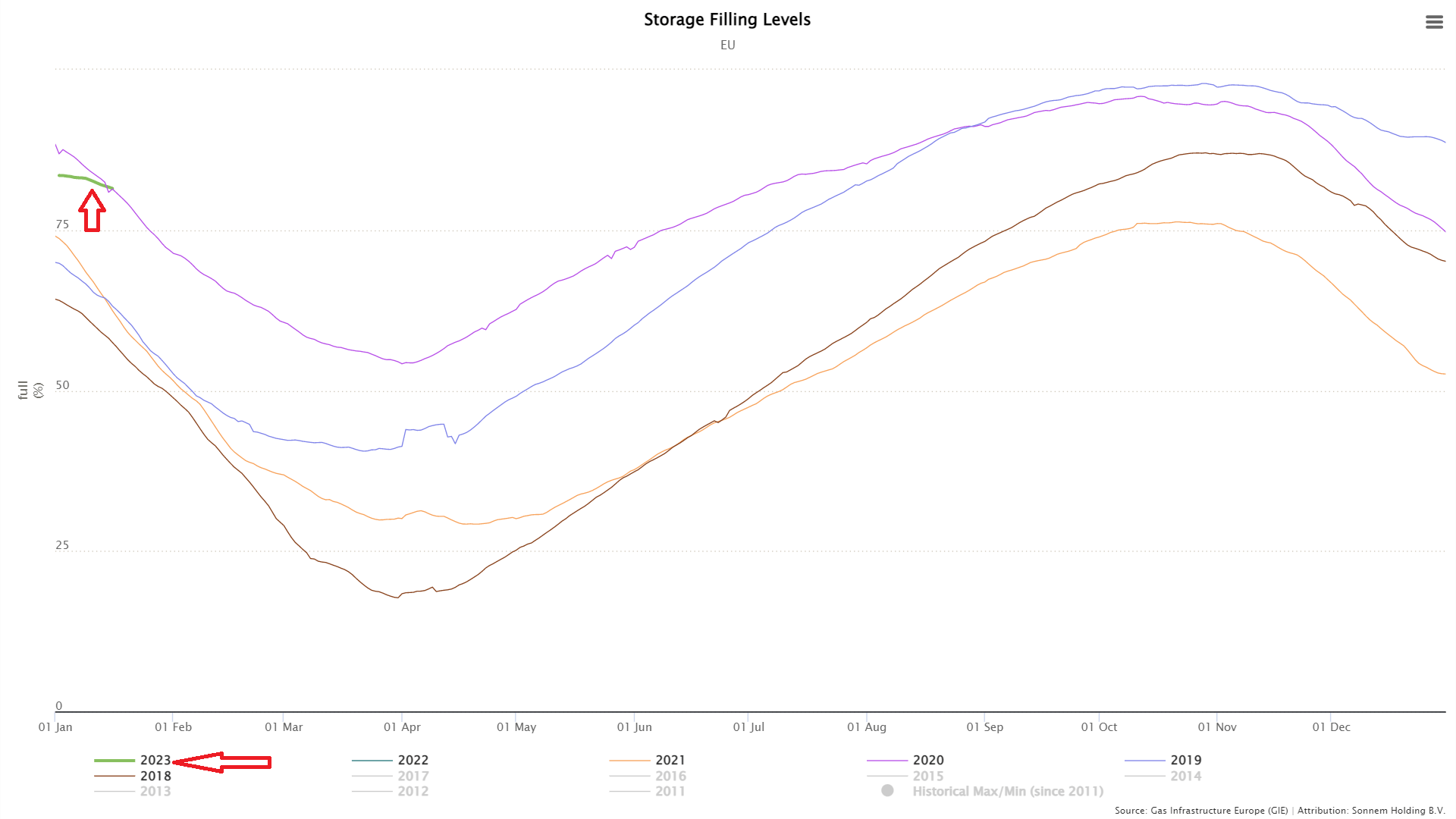

My point here is that all these considerations are temporary. Yes, Europe has more than enough natural gas right now.

GIE (Gas Infrastructure Europe)

But the issues that got us here haven’t been solved.

This is my key contention, even though winter 2023 is in the rearview mirror, I urge investors to think about winter 2024. And if that is seen to be too far away (12 months), keep in mind that natural gas is restocked in the summer months, in anticipation of the winter ahead.

Consequently, given that the market is forward-looking, there are many catalysts afoot that will sooner rather than later lead to US natural gas prices moving higher, as demand for natural gas from Europe and elsewhere steadily increase in the months ahead.

And by extension, this will lead to US natural gas prices improving.

Now that we’ve discussed the secular growth opportunity, let’s turn to discuss EOG’s dividend.

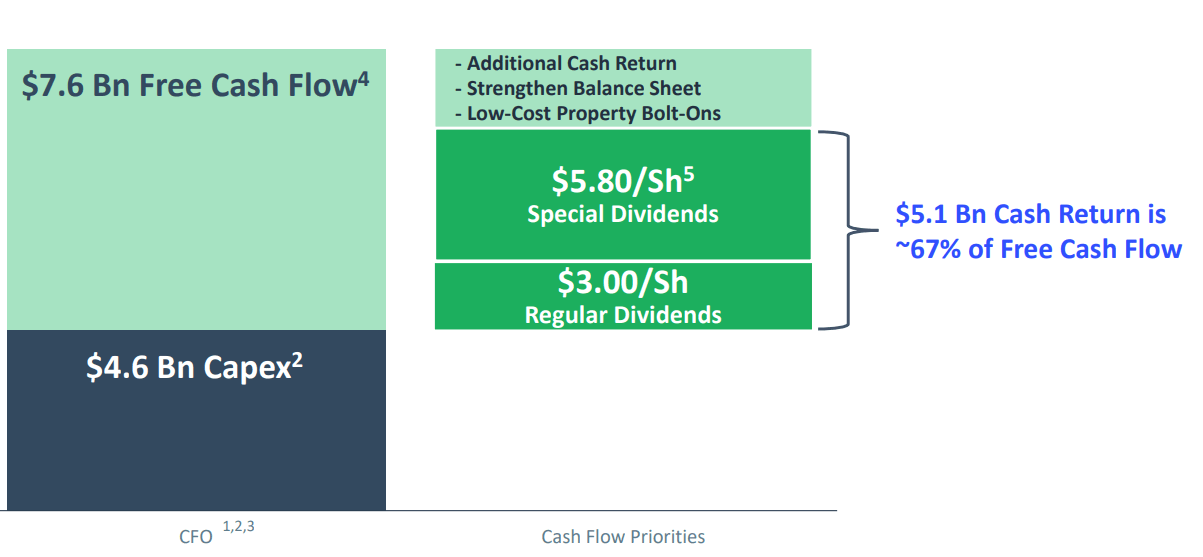

EOG’s Dividend, +6.0% Yield

EOG is committed to returning at least 60% of its free cash flow to shareholders.

EOG Q3 2022

Put simply, EOG’s base dividend annualized is now at $3.30. Hence, if we could vaguely count on at least $5 of special dividends in 2023, this would imply that its combined dividend could reach $8.30 per share, or close to 6.4%.

The Bottom Line

EOG is a dividend-paying stock that’s likely to pay out at least a 6% yield in 2023, via its base plus special dividends.

Given that EOG does not carry much debt at all, or better said, it holds a $200 million net cash position, this implies that EOG can easily continue to deploy more than 60% of its cash back to investors.

There are many different ways for investors to be rewarded here. The dividend is one. But if an investor believes in the increasing need for energy in 2023, in this case, natural gas, then investors will be well rewarded for buying this name.

Be the first to comment