CHUNYIP WONG

Looking for a piece of the energy sector high-yield pie? If you’re looking for a company with seasoned management, well-placed assets, and strong financials, consider Enterprise Products LP (NYSE:EPD), one of the largest market cap firms in the midstream industry, with a $55B market cap.

Company Profile:

In 1968, Enterprise Products formed as a wholesale marketer of natural gas liquids. Its integrated energy infrastructure network provides midstream energy services to producers and consumers of natural gas, natural gas liquids, crude oil, refined products and petrochemicals, linking producers from some of the largest North American supply basins with domestic consumers and international markets. (EPD site)

EPD’s network of assets is huge, with 50,000 miles of NGL, crude oil, natural gas, petrochemicals and refined products pipelines; 24 natural gas processing facilities; 18 fractionators; 7 splitters; 11 condensate distillation facilities; 1 PDH facility; 2 iBDH facilities; 260 MMBbls of NGL, petrochemical, refined products and crude oil and 14 Bcf of natural gas storage capacity; and 20 deepwater docks handling NGLs, petrochemicals, crude oil and refined products.

EPD’S largest segment is NGL Pipelines & Services, which generated 55% of its Q3 ’22 and Q1-3 ’22 gross operating margins; followed by Crude Oil Pipelines & Services, at ~18%; Petrochemical & Refined Product Services, at 15%; and Natural Gas Pipelines, at ~12%:

EPD site

Earnings:

Q3 2022: The Natural Gas segment had the most sequential growth in Q3 ’22, adding $49M in Gross Operating Margin, GOM. Crude oil GOM grew by $8M, whereas NGL was down by $31M, and the PetroChemicals segment was down by $68M:

EPD site

In Q3 ’22, EPD’s pipelines transported a record 11.3 million barrels/day equivalent of NGLs, crude oil, natural gas, refined products and petrochemicals. Its natural gas pipelines transported a record 17.5 trillion Btus/day.

Q3 ’22 vs. Q3 ’21 earnings were strong: Q3 ’22 Net Income rose by ~18%, while Adjusted EBITDA was up 12%; Distributable Cash Flow, DCF, rose by 34%; Adjusted Cash Flow From Operations, CFFO, grew by 13%, and diluted EPU rose by 19%:

EPD site

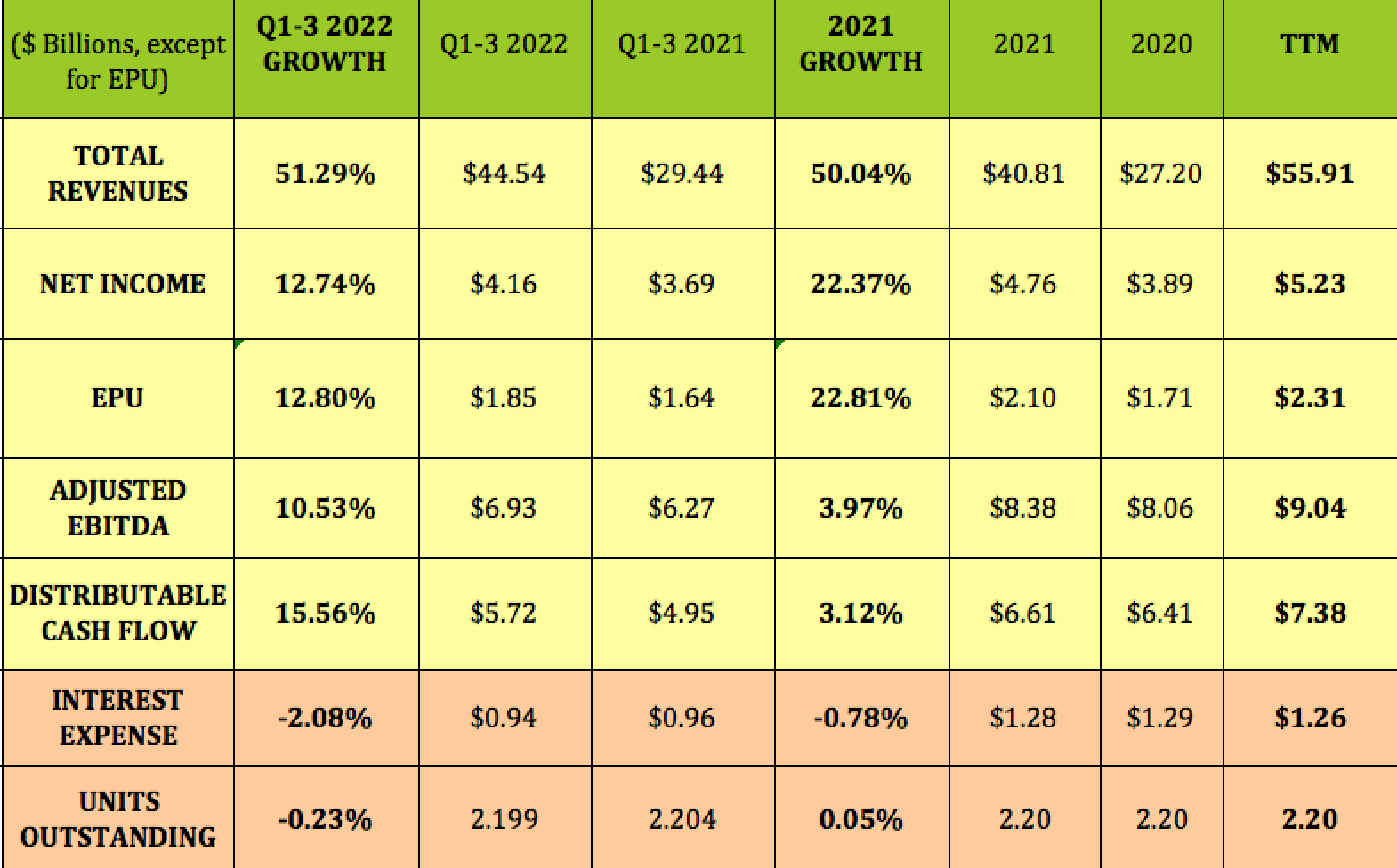

Looking back at Q1-3 ’22 earnings shows Revenues up 51%, with double-digit growth in Net Income, EBITDA, and DCF. Interest Expense also fell ~2%, not so common an event in 2022, with rates rising. As usual, management kept the unit count flat.

Hidden Dividend Stocks Plus

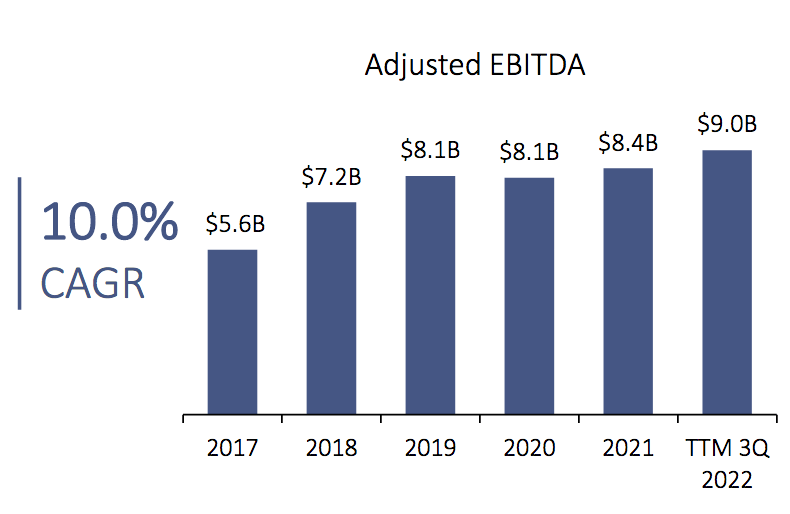

This growth is an ongoing story for EPD – it has a 10% Adjusted EBITDA growth rate since 2017:

EPD site

Growth Projects:

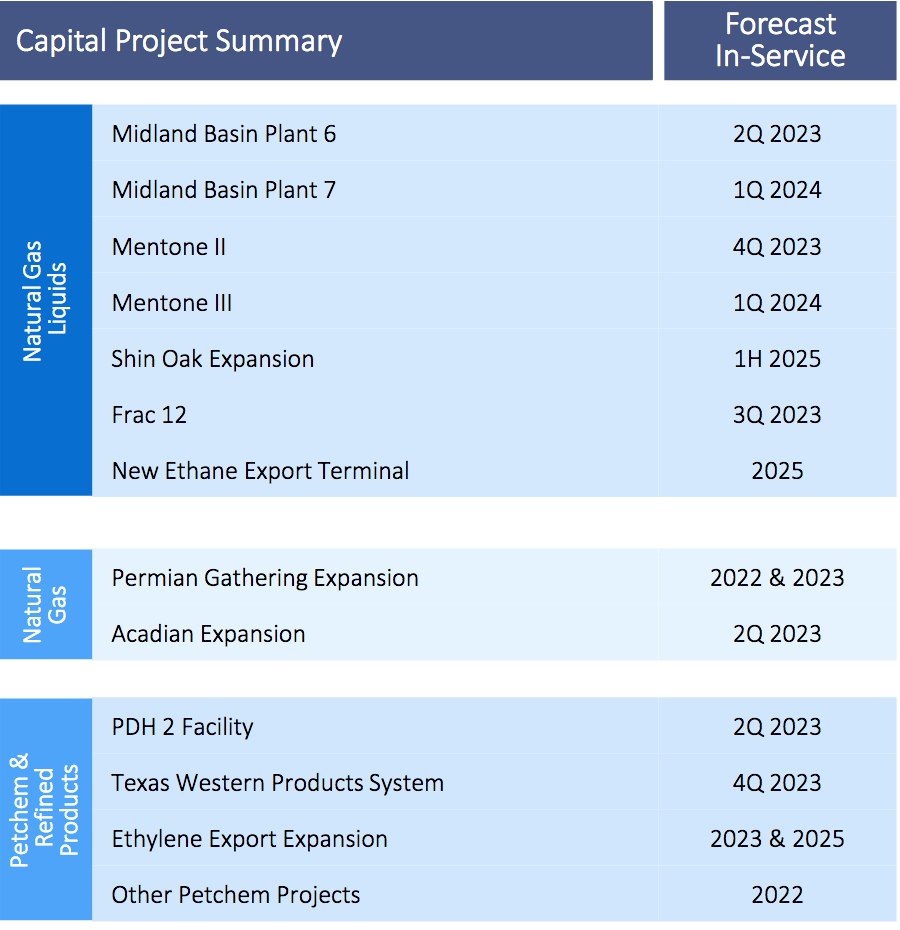

That growth has been fostered by capex projects. EPD has $5.5B forecast for projects so far in 2023-2025, with seven separate projects expected to come online in 2023, which should support further earnings and cash flow growth.

EPD site

Dividends:

Management has raised EPD’s dividends for 25 straight years, as of Q1 ’23. They raised the quarterly payout twice in 2022, and already raised the Q1 2023 distribution from $.475 to $.49. You’d think that would land them in the Dividend Aristocrats, but they’re still not part of the S&P 500, which is a prerequisite for joining the list.

At its 1/18/23 $24.14 closing price, EPD yields 7.80%. It goes ex-dividend on 1/30/23, with a 2/14/23 pay date. Its five-year dividend growth rate is 2.43%, which may not sound very high, but it’s pretty good for the Energy industry, which suffered big demand destruction during the pandemic in 2020.

EPD also has a buyback program. In Q3 2022, Enterprise repurchased ~3.9M of its common units on the open market for ~$95 million. For the nine months ended Sept. 30, 2022, the partnership repurchased ~5.3M common units for ~$130 million. Including these purchases, the partnership has utilized 31 % of its authorized $2B unit buyback program.

Hidden Dividend Stocks Plus

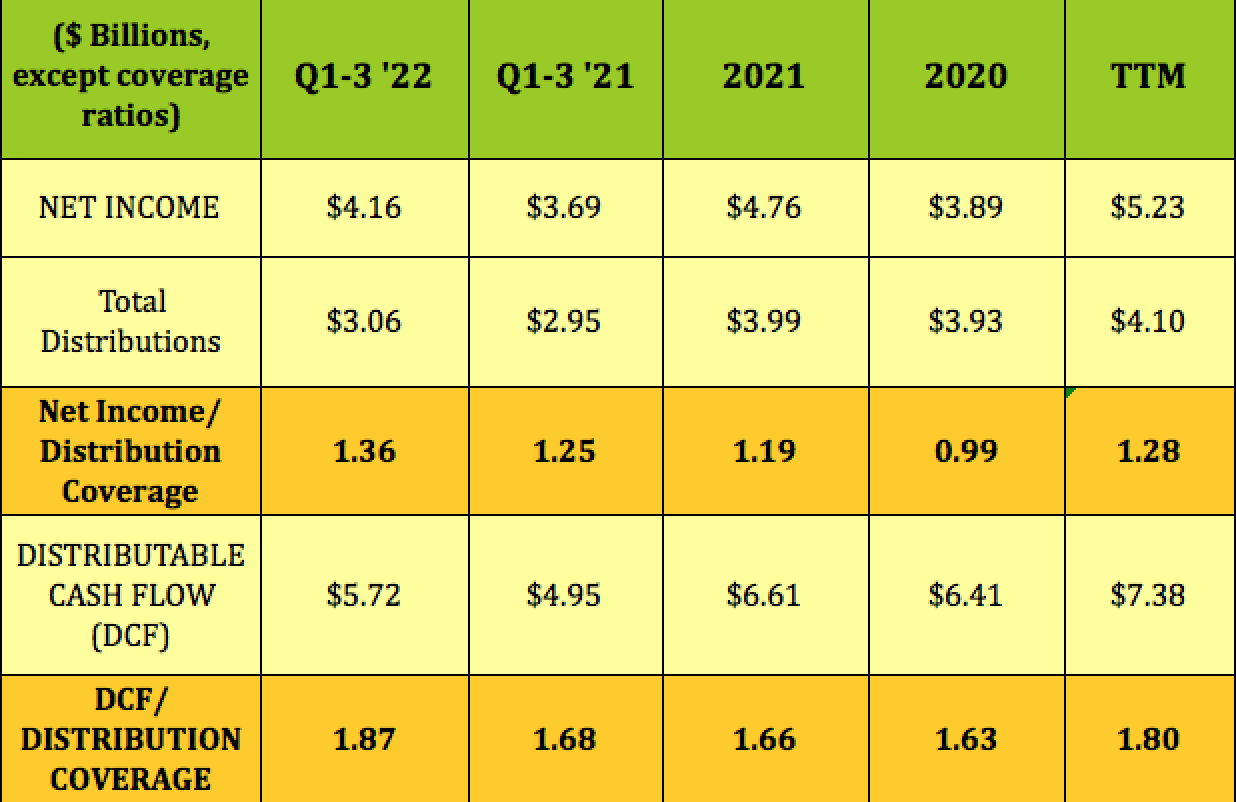

We looked at dividend coverage from two angles, and both were strong. On a Net Income basis, EPD’s dividend coverage improved to 1.36X in Q1-3 ’22, vs. an already strong 1.25X in Q1-3 ’21. The trailing Net Income coverage factor is 1.28X.

On a DCF basis, EPD’s distribution coverage rose from 1.68X in Q1-3 ’21, to 1.87X in Q1-3 ’22, with a trailing 12 month 1.8X factor.

Hidden Dividend Stocks Plus

Taxes:

EPD issues a K-1 at tax time.

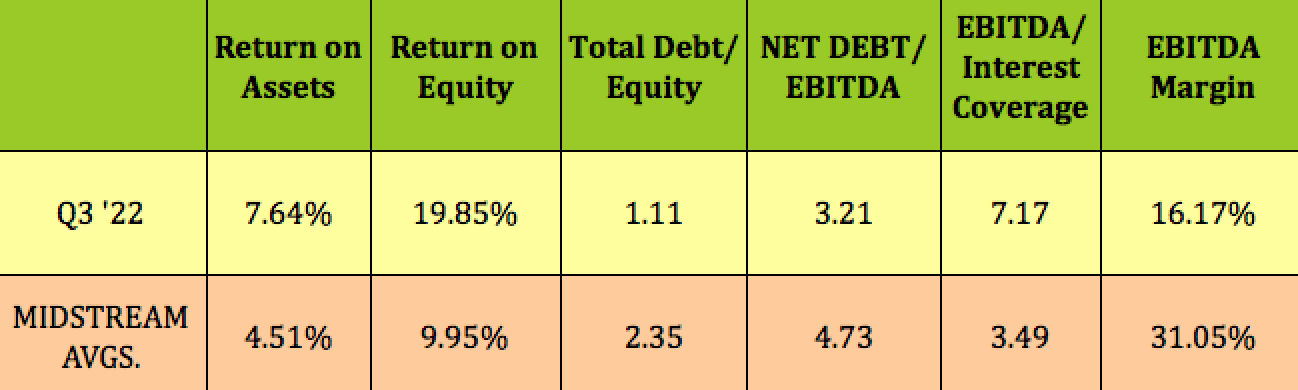

Profitability and Leverage:

EPD’s ROA and ROE remain far above midstream average, as does its EBITDA/Interest coverage. Management maintains debt leverage ratios that are much lower than midstream averages.

Hidden Dividend Stocks Plus

One of the outstanding features of EPD is that it’s able to self fund its growth projects, vs. getting buried in debt, and/or heavily diluting its unitholders, actions taken by many other energy firms over the years. After the fallout from the low energy demand cycles, other energy firms began to adopt EPD’s self-funding model.

EPD site

Debt and Liquidity:

EPD has one of the highest debt ratings in the midstream industry, at BBB+/Baa1.

Its has $1.25B in Senior Notes coming due in 2023, which is ~4.3% of its outstanding debt. In September 2022, it entered into a new $1.5B 364-Day Revolving Credit Agreement.

EPD site

As of Sept. 30, 2022, EPD had $3.3B of consolidated liquidity. This amount was comprised of $3.1B of available borrowing capacity under revolving credit facilities and $167M in unrestricted cash.

~93% of Enterprise’s debt had fixed interest rates, as of 9/30/22. Its debt portfolio had a weighted-average maturity of ~20 years, with a weighted-average interest rate of 4.4%.

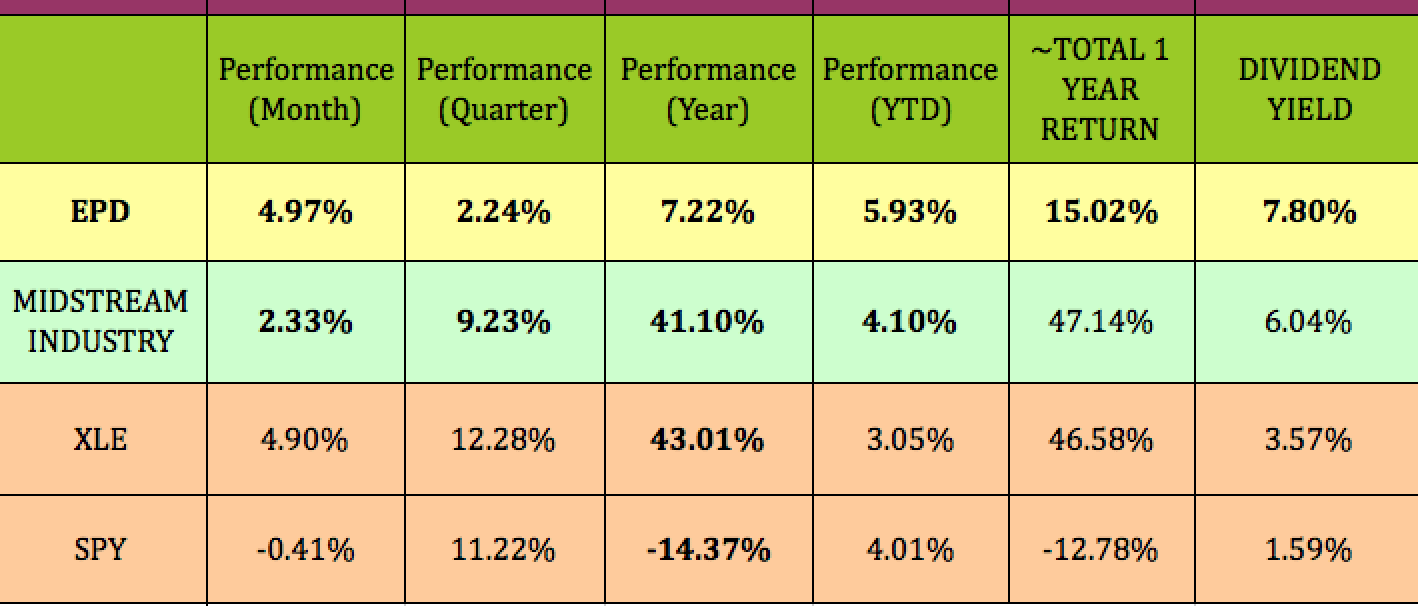

Performance:

EPD outperformed the S&P in price over the past month, and over the past year on a total return basis. However, it lagged the midstream industry and the broad energy sector over the past year.

However, EPD has outperformed the midstream industry, the broad Energy sector and the S&P 500 so far in 2023, and over the past month.

Hidden Dividend Stocks Plus

Looking back further, to 1998, shows EPD with a total return of 3230%, vs. 596% for the Energy sector, and 392% for the S&P 500:

EPD site

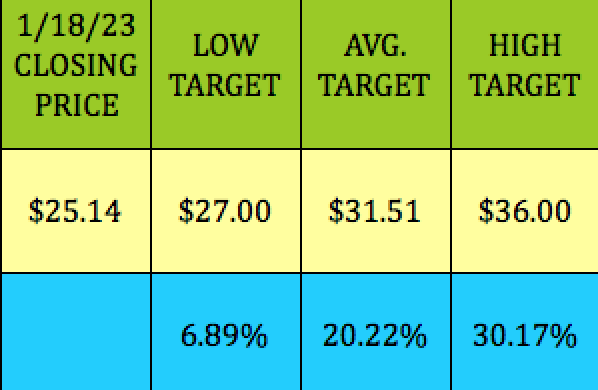

Analysts’ Upgrades and Targets:

On 1/9/23, EPD received an upgrade to outperform from Wolfe Research, with a $27.00 price target.

At its $25.14 closing price, EPD was ~7% below Wall St. analysts’ $27.00 lowest price target, and 20% below their $31.51 average price target.

Hidden Dividend Stocks Plus

Insiders Buying:

Co-CEO Teague and 2 other insiders bought units in November-December 2022 at prices ranging from $23.60 to $24.88.

EPD site

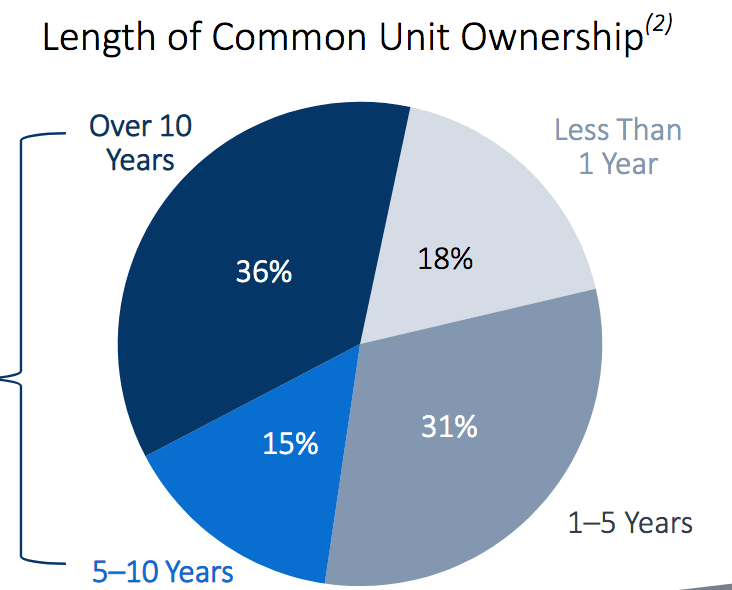

Management noted in its November presentation that EPD unitholders tend to hold these units for a long time, with 36% holding them for over 10 years, and 15% holding them for 1-5 years.

EPD site

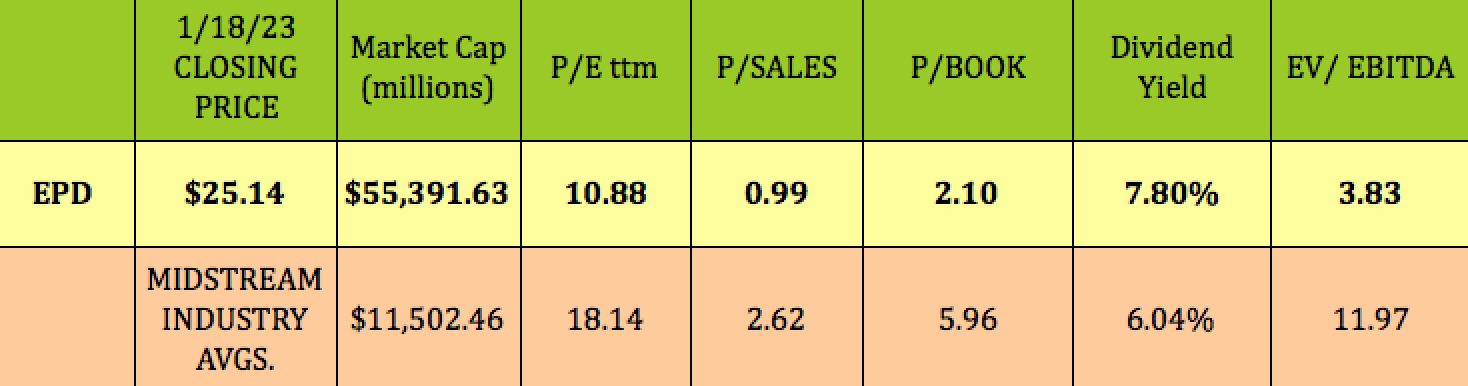

Valuations:

At its $25.14 closing price, EPD was priced at a much cheaper trailing P/E of 10.88X, vs. 18X for the midstream industry average. Its P/Book of 2.1X is only 35% that of the midstream industry’s 5.96X average, and its EV/EBITDA of 3.83X is very low also.

Hidden Dividend Stocks Plus

Parting Thoughts:

We’ve owned EPD for years, receiving those steadily rising dividends. At its current price level, EPD looks undervalued vs. midstream averages.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment