Sundry Photography

Introduction

Enphase Energy, Inc. (NASDAQ:ENPH) is an American-based solar energy company specializing in both microinverters and energy storage solutions. Enphase is the world’s leading supplier of microinverters, with the U.S. being its primary market, but Enphase has been quickly expanding its offering in Europe as well. It has been able to quickly grow its Europe business segment driven by the energy crisis on the Continent as a result of the Russia/Ukraine war. With green energy demand skyrocketing in Europe (and the world), Enphase has been one of the main beneficiaries with its microinverter product superior to competitors.

For those unfamiliar with solar microinverters, this is what I wrote in my previous coverage:

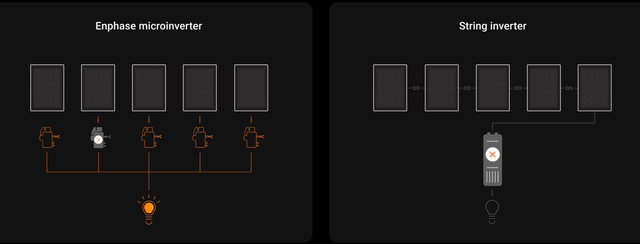

A microinverter converts the direct current power generated by a solar panel into grid-compatible alternating current for use or export. So why would consumers pay extra for a microinverter over a built-in central inverter in their solar system? Well, if a solar panel with a central inverter built in fails, solar production stops completely. With just one microinverter per solar module, solar production keeps working even if a microinverter stops working. The picture below shows this system.

Microinverter system (Enphase)

As indicated above, I have covered Enphase before and rated the company a buy as the long-term growth drivers looked incredibly strong and the firm keeps posting incredible growth rates easily outperforming analyst estimates. I concluded the following when I wrote my initial coverage of the company:

I think the dominant position of the company within the solar market, by using its microinverters to penetrate businesses and households and then cross-sell into more products like EV chargers and its IQ batteries, gives the company a very strong business position in an extremely fast-growing sector.

Yesterday, February 7, 2022, Enphase reported its Q4 2022 and managed to beat the consensus, again. Enphase managed to beat EPS by $0.25 and revenue by $21.49 million, resulting in an aftermarket jump in the share price of above 11% at some point. Now, at the time of writing this article, the stock is up 10% pre-market and looks like it is going to open above a share price of $251.

Within this article, I am going to revisit my thesis and see whether I believe the company is still a buy at current levels by going through the latest earnings release and outlook.

Quarterly Review

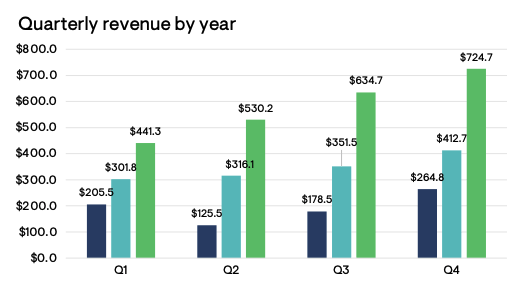

Enphase delivered another impressive quarter and, as indicated above, managed to beat the consensus once again, as it has done for 16 straight quarters now. Enphase reported revenue of $724.7 million which was again a quarterly record as the company shipped 4.9 million microinverters to customers and deployed 122 MWh of batteries. Revenue increased by a very impressive 75% compared to 80% for the previous quarter. Many Wall Street analysts cut expectations for revenue growth, as solar demand was falling quicker than previously anticipated, but Enphase seems to see absolutely no significant slowdown as of yet.

Enphase revenue (Enphase)

Approximately 55% of shipped microinverters were the new IQ8 series which also ships with higher margins compared to previously released models due to its new capabilities. As for revenue mix by regions, Enphase reported that 71% of revenue came from the U.S. with International (primarily Europe) being responsible for 29% of revenue. Growth in the U.S. was strong during the quarter with 59% growth YoY and 15% growth sequentially. Enphase did point out that storage and channel inventory was slightly elevated in the U.S., but not in any worrying way.

Europe was the primary growth driver (although U.S. growth was also great) with growth of a staggering 130% YoY and 21% sequentially. In previous earnings calls, Enphase already indicated that demand from Europe was strong enough to deliver growth rates of over 70% for many years and this quarter was absolutely no exception. Primary demand came from a selection of countries being The Netherlands, France, Germany, Belgium, Spain, Portugal, and the UK. For now, Enphase is still primarily shipping its older version microinverters in Europe but did start delivering its IQ8 series to the Netherlands and France over the latest quarter with these, together with Germany, being its primary European markets. The delivery of IQ batteries to European countries is also increasing and is expected to accelerate by the first half of 2023.

As for battery shipments, due to some software upgrades and faster installation times, Enphase saw higher sell-through during Q4 compared to Q3. With the first quarter of the year generally being a bit weaker due to seasonality, Enphase expects to ship another 100 to 120 MWh of batteries in 1Q23. Overall, Enphase expects battery shipments to increase by the second half of the year due to the adoption of NEM 3.0 in California.

Another product category for Enphase to discuss is EV (electric vehicle) chargers in which Enphase is quickly expanding its footprint as a result of multiple acquisitions in the past. This is illustrated by the following comment from management during the earnings call:

Our GreenCom Networks acquisition, which closed in the fourth quarter helps to integrate Enphase microinverters and batteries with third-party EV chargers and heat pumps, enabling homeowners to control their devices from one app, which is the Enphase App. We are integrating the GreenCom offering with the Enphase ecosystem and expect to make it available to our European installers shortly.

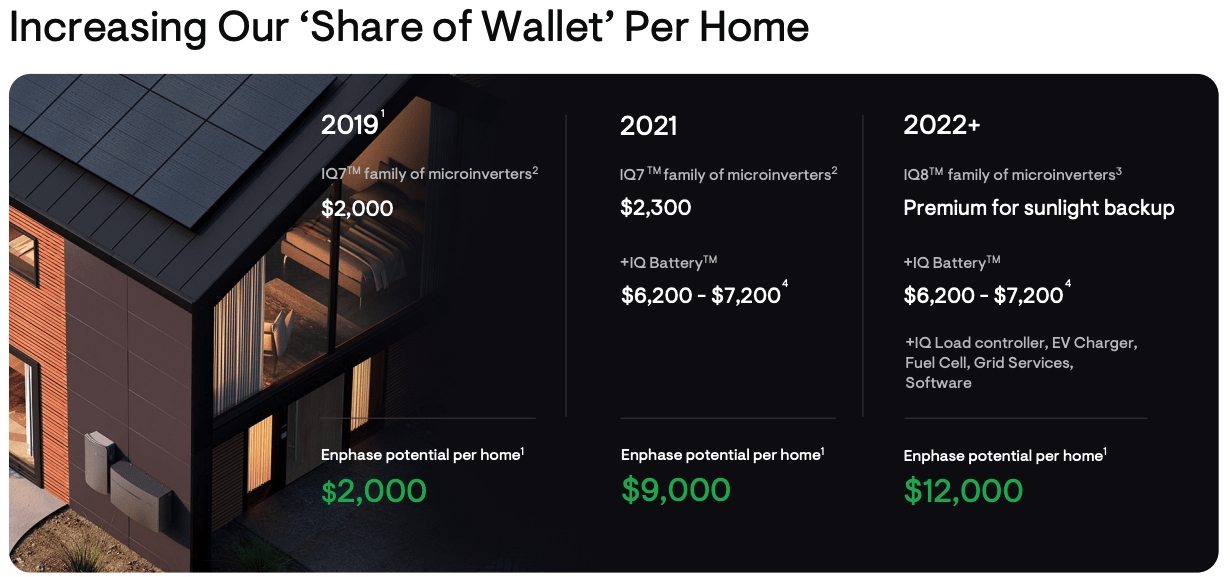

Enphase shipped 7600 EV chargers in the 4Q22 which increased almost 20% sequentially. This increase was possible due to Enphase starting production in Mexico for its Enphase-branded EV chargers which increased capacity and lowered production costs. Enphase plans on bringing significant technological advancements starting the second half of 2023 until the end of 2024 which involves new charging technologies and Enphase ecosystem functionalities. One of the largest opportunities for Enphase continues to be the opportunity of upselling existing microinverter customers. Enphase already has great consumer exposure thanks to its strong market presence in microinverters and this opens it up to the possibility of cross-selling additional products such as batteries and EV chargers.

Besides offering a significant opportunity to Enphase to increase its revenue without having to acquire new customers, it offers excellent benefits to customers. For example, it gives consumers the possibility to control and monitor all Enphase products in one single app, from energy generation to both storage and usage. New product updates will accelerate this opportunity for Enphase. This is what management concluded during the Q4 earnings call:

In summary, we are quite pleased with our performance. As a reminder, our strategy is to build best-in-class home energy systems and deliver them to homeowners through our installer and distributor partners, enabled by the installer platform. We have many new products that are coming out in 2023 that will increase our served available market and positively contribute to the top line.

Enphase home offering (Enphase)

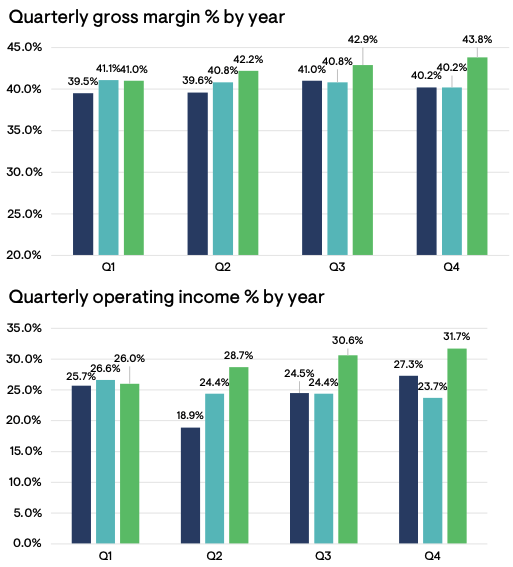

Enphase has already been profitable on both a GAAP and non-GAAP basis for many years and continues to increase its margins QoQ. This quarter was no different as gross margins came in at 43.8% compared to 40.2% for 4Q21 and 42.9% for the previous quarter. Operating expenses for Enphase grew by approximately 50% and this resulted in an operating income of $157 million or a 134% increase YoY. Net income was $212 million and increased by 106% YoY resulting in EPS of $1.51. To top off these excellent results, Enphase reported a strong free cash flow of $237.3 million, bringing the total cash position to a solid $1.61 billion, up from $1.42 billion at the end of the third quarter, solidifying the financial position.

These results are highly impressive as the company continues to fundamentally perform to perfection. As I said in my coverage of Enphase’s third-quarter results, I am still looking for a company posting these same growth rates on a constant basis, outperforming analyst estimates every single quarter, while being profitable. Do you know one?

Enphase margin development (Enphase)

Enphase continues to struggle to keep up with global demand for its products as it keeps expanding its production capacity. As of the latest quarter, Enphase has a quarterly capacity of 5 million microinverters and Enphase is far from done expanding. As of 2023, the company will start its manufacturing in Romania which should enable it to better serve demand in Europe and bring down shipment costs. Also, the company is planning to increase manufacturing in the U.S. over the next couple of years as demand remains incredibly high.

A great tailwind for these expectations in the U.S. is the IRA (inflation reduction act) as it will help Enphase to bring back manufacturing to the U.S. and increase local manufacturing. Enphase plans on starting microinverter production in the U.S. in the second half of 2023 with one new production partner and two existing ones. Together, these should boost quarterly microinverter production by 4.5 million to a total of over 10 million microinverters. To reach this target, a total of 6 new production lines will be opened in the U.S. As of the earnings call, Enphase could not give the exact tax benefits of the IRA as it awaits details on its implementation. Still, the significant increase in production capacity will function as an excellent tailwind for Enphase to satisfy global demand and massively increase its moat, presence, and financial results. With demand still very high and production capacity doubling over the next year, Enphase looks set for solid growth going forward.

Overall, Enphase delivered another stunning quarter with the company seeing absolutely no significant slowdown in the top and bottom-line growth. Even more, with significant margin growth, Enphase managed to report bottom-line growth rates of over 100% during the quarter. Management keeps focused on the long-term as it sees a long growth runway ahead and plans to benefit from increased solar demand as a secular growth driver. This is what management stated:

The basic thesis ongoing solar and storage remains intact, aided by a few factors: first, the utility rates, which are rising in many states across the U.S.; second, the 30% ITC tax credit, which has been extended for 10 years with the IRA; and third, the desire for energy independence and tackling climate change. At Enphase, we will continue to make best-in-class home energy systems with a laser focus on product innovation, quality and customer experience.

Outlook & Valuation

To come back to my own estimates, back in my third quarter update on Enphase I wrote the following:

This is a slowdown compared to last quarter’s 20%. Yet I expect Enphase to beat revenue again and I feel like $725 million is still a safe estimate. This would be closer to a 15% increase QoQ.

With Enphase reporting $724,7 billion in revenue, my estimate was pretty much spot on. Now, for 1Q23 Enphase has again guided for revenue above the consensus. Enphase expects revenue of between $700 to $740 million (vs $682.3 million consensus) which is pretty much flat at the midpoint compared to the previous quarter. As stated before, the first quarter is generally a weaker one for Enphase due to seasonality. Still, this represents over 63% revenue growth YoY based on the midpoint of guidance, and although a slowdown from the 75% from the previous quarter, this is still very impressive considering Enphase also managed to report similar growth rates last year. Enphase expects margins of between 41% to 44%.

Enphase expects growth from Europe to remain very strong as it launches new products and expands its offering to more European countries. It managed to double revenue from Europe from 2020 to 2021 and managed to more than double again from 2021 to 2022. This is an incredibly impressive feat and while I do not expect Enphase to double again this year, revenue growth is expected to remain very strong according to management. As for the U.S., Enphase expects this to be down slightly compared to 4Q22 due to both seasonality and the impact of macroeconomic circumstances. Both distributors and installer partners are a little more cautious with booking orders and are reducing their spending slightly as they watch the economic development. This is no surprise and as expected. In addition to this, management is seeing increased activations compared to December illustrating that consumer demand is still strong. As a result, management remains confident:

Although the data we have is limited, these two points make us cautiously optimistic about Q2. We have also seen some analyst reports about a possible shift from loans to PPA due to the high prevailing interest rates. We work with thousands of installers every quarter. Our installer base is very diverse, both small and large installers that offer cash, loans and PPA options to homeowners. Any shift from one type of financing to another only has a minor impact to our business, almost negligible. No matter what the conditions are, our approach at Enphase does not change.

According to Seeking Alpha, analysts currently guide for revenue of $682.33 million (54% YoY growth) and EPS of $1.13 (43% YoY growth). These estimates are simply far too low and will be revised upwards over the following weeks. For FY23, analysts currently guide for revenue of $3.13 billion or growth of just 33%. EPS is expected to be $5.34 and grow just 12%. And again, these estimates are far too low and will be revised upwards over the following weeks.

Personally, I expect Enphase to report revenue of around $741 million for the next quarter, or growth of 68% YoY. I expect demand to remain high and Europe to keep up the strong growth rates as shown over previous quarters, although slowing down ever so slightly. I expect this to couple with margins of between 43% and 44%.

For FY22 I project Enphase to bring in revenue of $3.35 and show YoY growth of 44%. I expect Enphase to grow EPS at a slightly slower pace of 32% and report EPS of $6.30. While these estimates are currently significantly above current analyst estimates, I believe these estimates will be revised upwards and with Enphase having a strong history of even outperforming revised estimates, I believe my current estimates are fair and still rather conservative. Please do note that I do not expect a severe recession for either Europe or the US. If this were the case, this could significantly impact revenue projections for the second half of the year.

As a result of these estimates and a current pre-market share price of $251, the stock is currently valued at a forward P/E of around 40. While for some this will be too expensive, for others this will be fair or even far too cheap. Considering current estimates guide for EPS growth of between 20% and 30% until 2026 (expecting analysts to revise expectations up slightly), I believe a P/E of between 40-50 is actually quite fair for Enphase. I will therefore assume a P/E of 45 which results in a price target of $284 and leaves investors with a 13% upside from current levels.

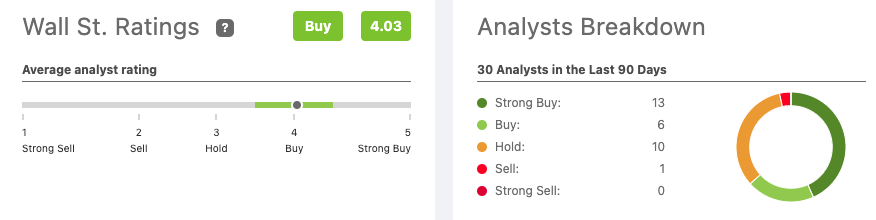

For comparison (without expected revisions) 30 Wall Street analysts currently have a target price of $293, leaving investors with approximately a 17% upside. The company receives a buy rating from analysts.

Seeking Alpha

Conclusion

Enphase Energy, Inc. delivered a stunning quarter once more and easily beat the analyst consensus and its own expectations. With growth drivers still in place and the long-term outlook still strong, there is not much reason to change my investment thesis. While the financial results could be impacted in the near term by macroeconomic headwinds and an economic slowdown, I expect Enphase to keep reporting solid growth rates (although possibly lower than current expectations) driven by government incentives, a push towards green energy, and high energy prices. The long-term growth story is strong and Enphase had plenty of growth opportunities and great management to act on them.

With the Enphase Energy’s business continuing to grow revenue at a rapid pace and the share price falling over the last 2 months, the share price has become increasingly more attractive.

I believe a P/E of 45 is fair for this high-quality business. This results in a price target of $284 and leaves Enphase Energy, Inc. investors with a 13% upside from current levels which makes me balance between a buy and a hold from a valuation standpoint. Considering I expect Enphase to see solid long-term growth, I believe the current share price offers enough downside protection. I believe Enphase Energy, Inc. is a buy at any price below $255 a share.

I, therefore, rate Enphase Energy, Inc. a buy after excellent financial results.

Be the first to comment