davidkl/E+ via Getty Images

Give water enough time and it will carve a tunnel through the thickest mountain.”― Marty Rubin

It has been more than a year and a half since our initial take on Kodiak Sciences (NASDAQ:KOD) which reached this conclusion:

I am always somewhat leery when existing shareholders are selling significant stakes. If the market sentiment on the biotech sector was better, I would be tempted to establish a small holding in Kodiak via covered call orders given the recent decline in the stock. However, with the SPDR Biotech ETF (XBI) down some 30% from its recent highs in February and some negative analyst views on Kodiak, I am passing on any investment recommendation in this name for the time being.”

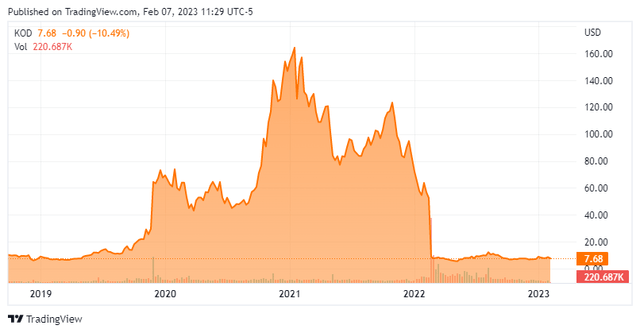

The pass on taking an investment at that time was a good one as the shares have lost roughly 90% of their value since then.

Seeking Alpha

Company Overview

Kodiak Sciences is headquartered just outside of San Francisco, CA. This clinical stage biotech concern is focused on developing therapeutics to treat retinal diseases. Currently, the stock trades just under eight bucks a share and sports an approximate market cap just north of $400 million.

October Company Presentation

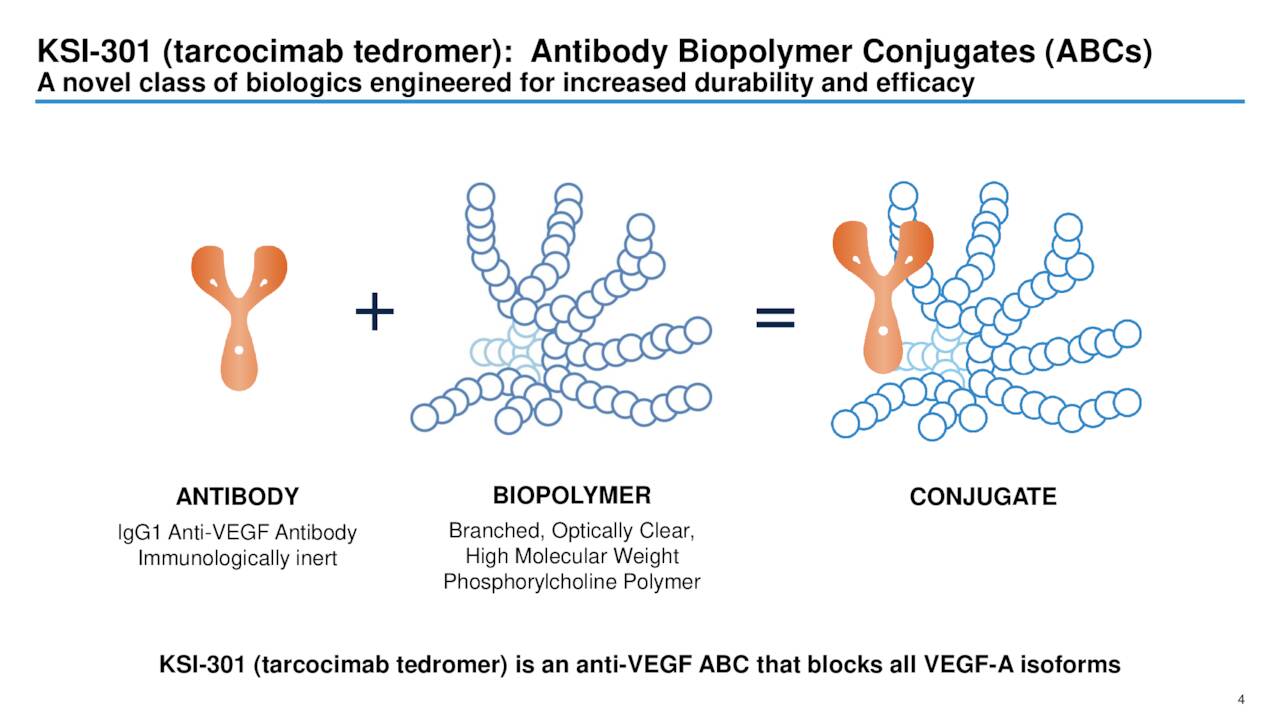

Kodiak’s lead product candidate is KSI-301 which is also known as tarcocimab tedromer. This is an anti-vascular endothelial growth factor antibody biopolymer. The company is developing this candidate to be a new first-line agent to improve outcomes for patients with retinal vascular diseases as well as to enable earlier treatment and prevention of vision loss for patients with diabetic eye disease.

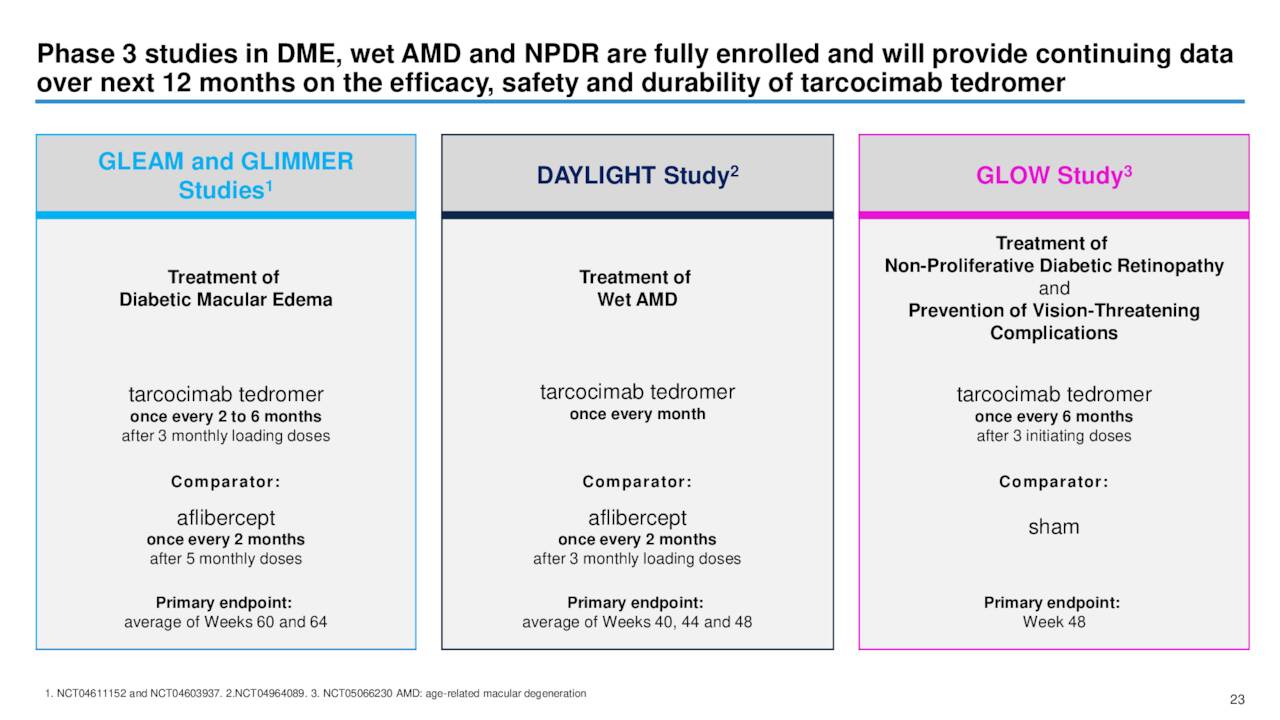

KSI-301 is currently in mid/late stage development treat wet age-related macular degeneration or AMD, as well as for the treatment of diabetic macular edema, naïve macular edema due to retinal vein occlusion, and non-proliferative diabetic retinopathy. Here is the update management provided around these trials within its third quarter earnings press release.

- GLEAM / GLIMMER: A paired Phase 3 long-interval (as infrequently as every 6 months) studies GLEAM and GLIMMER in diabetic macular edema (“DME”) are expected to report topline data in mid-2023 and if successful are designed to serve as the primary basis for a licensing application and potential regulatory approval of tarcocimab.

- DAYLIGHT: A Phase 3 short-interval study DAYLIGHT in wet AMD is expected to report topline results in mid-2023. If successful, we expect DAYLIGHT to contribute data to support approval of tarcocimab in wet AMD.

- GLOW: A Phase 3 long-interval (every 6 months) treatment and vision loss prevention study GLOW of tarcocimab versus sham in non-proliferative diabetic retinopathy without DME (“NPDR”) is expected to report topline results in the second half of 2023. If successful, we expect GLOW to contribute data to support approval of tarcocimab in NPDR with the potential to be the longest-interval intravitreal therapeutic option in this disease.

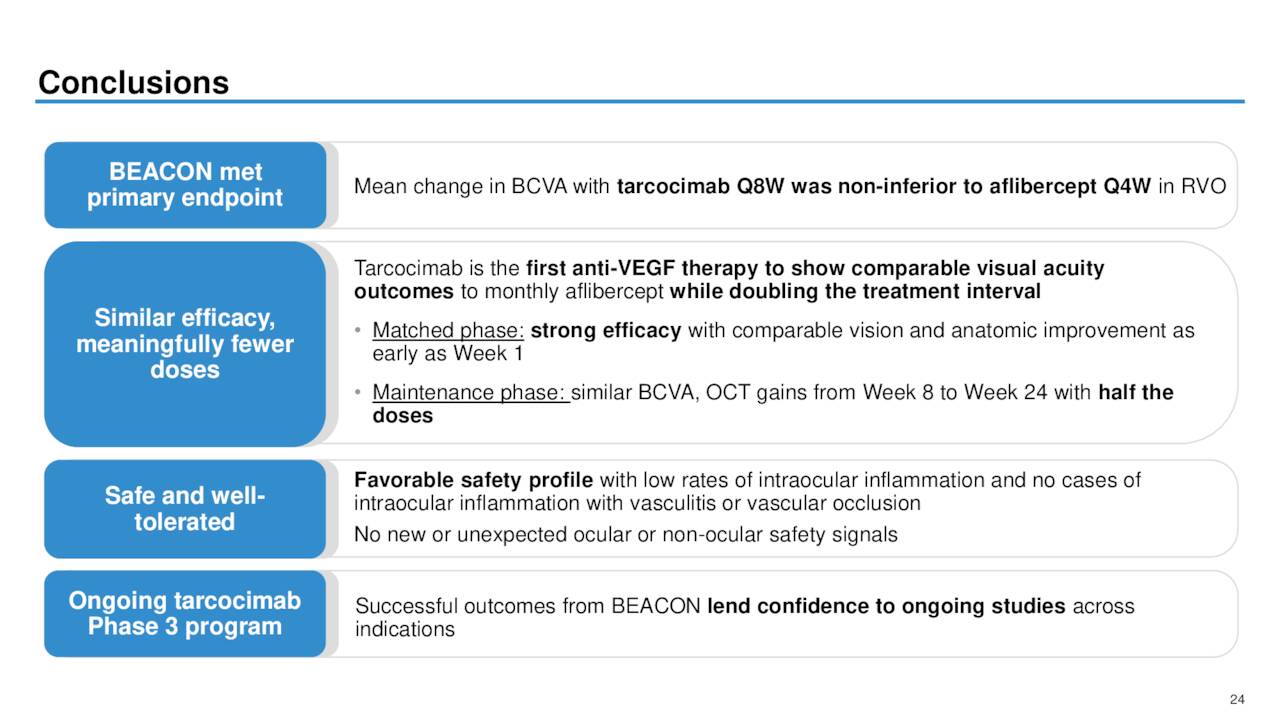

- BEACON: The primary (6 month) efficacy and safety results of our successful BEACON study of tarcocimab versus aflibercept in retinal vein occlusion were reported at the 2022 EURetina and AAO scientific congresses.

October Company Presentation

All four of these trials are scheduled to have top-line data come out in 2023.

The company has a couple of other compounds in development. One is KSI-501, which is a bispecific conjugate targeting retinal diseases with an inflammatory component. This is KSI-601, a triplet inhibitor for the treatment of dry AMD. Both are in pre-clinical development so will not be germane to this analysis.

Analyst Commentary & Balance Sheet

Since third quarter results posted on November 9th, four analyst firms including Goldman Sachs and Morgan Stanley have reissued Hold/Sell ratings on the stock. Price targets proffered ranged from $6 to $12 a share. The lone optimist on this equity at the moment seems to be Capital One Financial which initiated the shares with an Overweight rating and $24 price target right after third quarter numbers came out.

Approximately five percent of the outstanding float of the stock is currently held short. There has been no insider activity in this equity since June of last year. The company ended the third quarter with just over $535 million in cash and marketable securities on its balance sheet after posting net loss of $77 million during the quarter. Kodiak Sciences has no long-term debt.

Verdict

With a market cap currently under the net cash the company ended the third quarter indicates investors are assigning no value to KSI-301 despite top line results due out for four late stage indications this year. Analyst firms are also firmly in the bear camp around Kodiak Sciences currently.

Certainly some skepticism is warranted. Investors were shellacked late last February when KSI-301 did not meet the primary endpoint in a Phase 2b/3 trial for wet AMD. At the time, members of management stated the trial design was partly to blame for the disappointing data and that these issues had been addressed in its remaining studies.

It should be noted than in early August, the company disclosed data from its BEACON Phase 3 study that did meet the primary endpoint in patients with macular edema due to retinal vein occlusion. Four more trial readouts should come starting mid-year through year end of 2023.

October Company Presentation

Given this, I have initiated a small ‘watch item‘ position via covered call orders in Kodiak Sciences as the stock seems worthy of a small bet in anticipation that news flow around the company gets more positive in the quarters ahead.

Wealth-building is a crockpot, not a microwave.”― Dave Ramsey

Be the first to comment