Sundry Photography

Enphase Energy (NASDAQ:ENPH) has seen an impressive run in 2022, with the share price up over 42%. With plenty of tailwinds for the entire sector this has made some company’s valuations inflated, such is the case for Enphase. With a high forward p/e of 60, the current share price would present a lot of potential downside risks for an investor. Given these reasons I think the course of action would be to sell any shares in the company, and wait for a better entry point again.

Q3 Earnings Report

On October.25 2022 Enphase Energy provided investors with their Q3 earnings report. For me there were quite a few highlights showcasing the company’s ability to generate revenues and increase the bottom line despite an increasingly difficult economic environment.

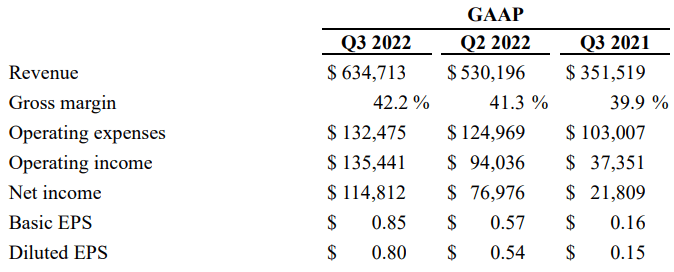

Revenue Sheet For Enphase (Enphase Q3 Earnings Report)

With revenues coming in at $634 million, an increase of just over 80% compared to last year, Enphase Energy is proving themselves to be something to count on. Like I also mentioned, the bottom line saw a big jump too. EPS was $0.80 per share this quarter, a big increase from last year’s performance of $0.15 per share.

With the ongoing energy crisis in Europe, Enphase Energy saw a large increase in their revenues from its operations here. Revenues increased by 70% compared to the second quarter of 2022, a massive increase showing the potential the company has for overseas operations.

All in all Enphase had a very successful third quarter, able to increase gross margins and also its bottom line in great fashion. It remained optimistic about its future and ability to efficiently maneuver around any obstacles.

Growth Outlook

In terms of outlook for the last quarter of 2022 Enphase Energy has provided some forecasts. Revenues are expected to be between $680 million and $720 million, something I think they will definitely be able to achieve. The company provided us with an investor presentation, where they go more in-depth in certain areas.

Looking at the market outlook for Enphase there are plenty of tailwinds. With their all-in-one product aimed at creating an ecosystem of home energy they have a large market to grow in. According to most researchers, the market for residential solar equipment hasn’t been penetrated more than around 7-9% today. Right now the TAM for residential solar adoption is $14.2 billion. But looking ahead this will increase to $44.77 billion by 2030.

With an increased demand for a green energy source, Enphase will have an easier time getting their products sold and hopefully land larger and larger projects with it too. Up until now ENPH has been able to maneuver quickly and efficiently taking more and more market share and become a reliable supplier of energy equipment.

The Market Share

Given the recent positive earnings report that Enphase Energy provided investors, it can be noted that they now hold around 22.83% of the market. This makes them one of the largest companies in the space. With competitors such as JinkoSolar (JKS) and SolarEdge (SEDG), Enphase is making a mark and establishing themselves as the solar module and storage company for customers.

Looking at the way these companies are expected to grow there is an average EPS growth of between 20 and 25% for them. That seems realistic as the entire sector is expected to grow 21-22% CAGR for the next 10 years. What puts me off Enphase right now is the rich valuation. The same goes for its competitors JinkoSolar and SolarEdge. What might be better for investors instead is to look for smaller companies offering a better entry point.

The Financial State

Knowing how a company is doing financially always comes down to understanding the balance sheet properly. In the case of Enphase Energy there are a few red flags I have found, but there are also things I find good.

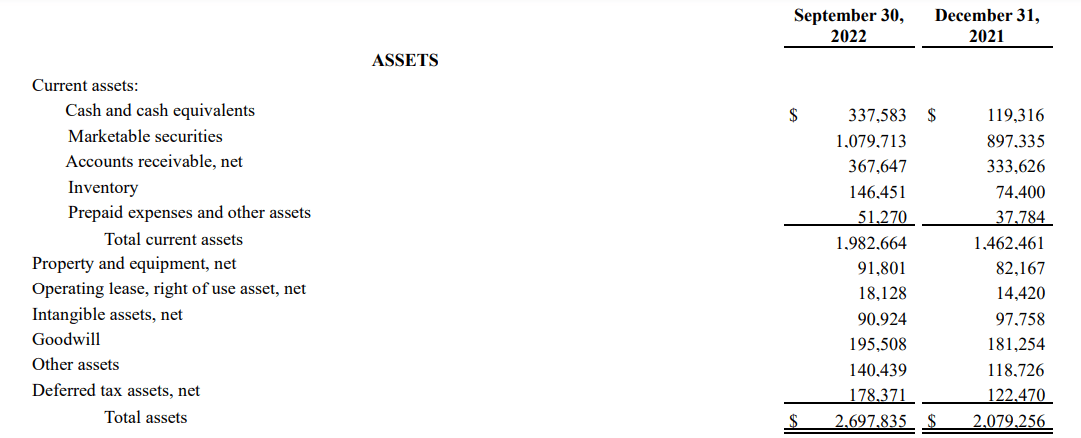

Assets Of Enphase Energy (Enphase Q3 Earnings Report)

First would be the amount of cash the company holds in comparison to the amount of debt they have. From the last earnings report, Enphase held $337 million in cash and had $1.1 billion in debt. Almost 4x more debt than cash is not a good position to be in as a company. It brings uncertainty and drastically increases the risk of share dilution in my opinion.

Enphase Liabilities (Enphase Q3 Earnings Report)

In terms of share dilution, Enphase has not relaxed on diluting their shareholders. With the outstanding shares going from 82 million to 135 million is worrying. But with cash flow topping out at $400 million in the last report, I have faith that perhaps this drastic increase in shares will slow down soon.

Enphase Outstanding Shares (Seeking Alpha)

One of the positives I found on the balance sheet would be that assets are growing faster than liabilities right now. That usually means that the company isn’t taking on too much new debt and stays reasonable. I would however watch out for the “accounts payable” section in the future, as that will give an indicator of the increase in supplies.

Valuing Enphase Energy

This is the hard part for me. The market is massive for Enphase and I might very well be wrong with my assumptions. But having some sort of grip about the realistic number a company is worth is vital in my opinion.

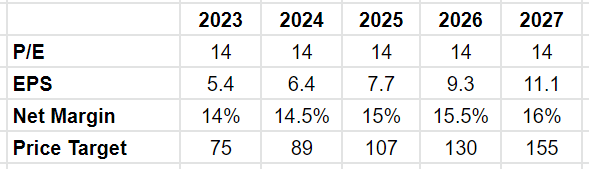

The Potential Valuation Of Enphase (Author’s Own Calculations)

The price targets I have might seem way too conservative, but I think that’s better so I can be surprised at the upside than the downside. I have put the p/e at 14 since I believe they are growing at a rapid pace and have a relatively good financial state and deserve a multiple that reflects that. The EPS I expect to grow around 20% CAGR until 2027. But after that I expect that the market will be quite saturated and it will be difficult for Enphase Energy to extract any more value from the customer base.

One thing I believe the company will be able to achieve is better and better net margins. They already have very impressive margins compared to a lot of other competitors, the hope I have is that they will maintain them at the very least.

Right now Enphase is at a much higher price than any of my future assumptions. I don’t feel comfortable buying at these levels and expect it to drop to more realistic levels eventually. The downside risk that you have buying any company at a p/e of more than 60 is immense. Because of these circumstances I wouldn’t put any money into the company right now.

Conclusion

Enphase is an incredible company growing their top and bottom line at a rapid pace, even compared to some of their competitors. With a market that has plenty of tailwinds I don’t expect ENPH to struggle getting their product sold in the future.

On the balance sheet there are some good things and some bad things. Cash flow being positive and assets growing faster than liabilities is to me are some of the positives. But with cash being almost 4x less than the debt it has me worried about potential share dilution.

At the moment Enphase Energy is trading at around $270 per share with a p/e of above 60. This is a very rich valuation and at the current rate the company is growing it doesn’t seem to me the valuation is realistic. I would have to pay a massive premium to get a part of the company right now. Because of that my downside risk is much higher than the potential reward and this forces me to stay away from investing and recommend a sell rating. If the valuations come down and reach numbers I am more comfortable with, I would have a second thought about it.

Be the first to comment