image

Engie SA (OTCPK:ENGIY) is navigating extraordinary market conditions and at the same time is producing an excellent financial performance.

If we contextualize everything to the European market we can say that the company has also contributed predominantly to the safety of the energy supply in the old continent. At the same time, the company is also going through a period of very delicate and at the same time strategically effective reorganization. The path of change is caught in the disposal of energy sources linked to coal and large investments in so-called renewable energies (net zero by 2045 is the main target).

Analyzing the trend of the EPS and the Free Cash Flow it seems that the dividend is largely financially sustainable and that the same can also be maintained in the next quarters. A very convenient share price valuation leads me to consider this an excellent long-term investment. My rate is Buy.

General Overview

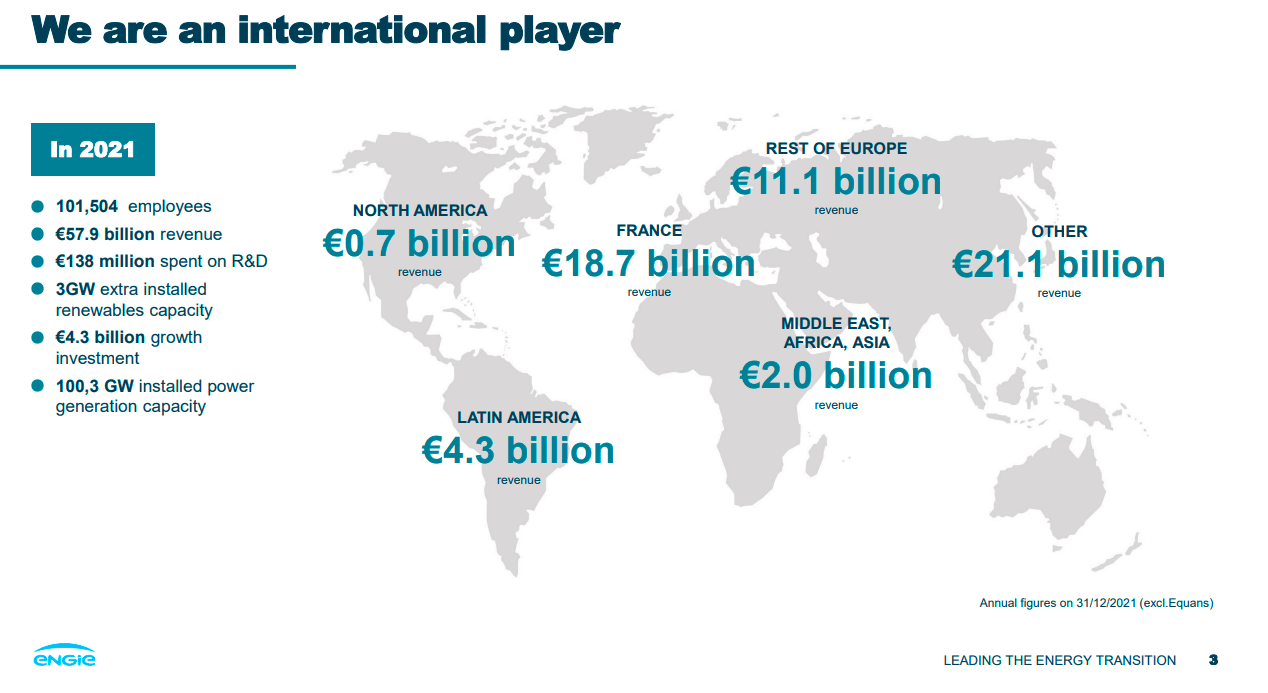

Engie SA is a French-based company providing energy and related services. The company could be defined as a global energy player based on Renewable and low-carbon energy infrastructures.

Engie is going through an important period of internal transition based on three core methods of intervention: a corporate reorganization aimed at increasing efficiency, industrial simplification of the group by redirecting operations towards emerging trends in the energy sector, and also an acceleration of investments in renewable energy and low- carbon with the target of reaching Net Zero Carbon by 2045.

In particular, the corporate reorganization is also based on 4 business segments: renewable, energy solutions, network, and thermal production. In parallel, the company is also reducing its geographical footprint intending to remain operational in 30 countries by 2030 (in 2018, there were 70 countries). These footprints are accompanied by two further concepts: digitization and data management.

By way of example and speaking of gas as one of the main energy assets worldwide, Engie is investing its energies in renewable gases such as hydrogen. The company’s hydrogen targets are ambitious and speak of a production capacity of 4GW by 2030, 435 miles of a dedicated network, and more than 100 service stations for refueling mobility.

General Shareholders Meeting 2022

Target and Highlights

General Shareholders Meeting 2022

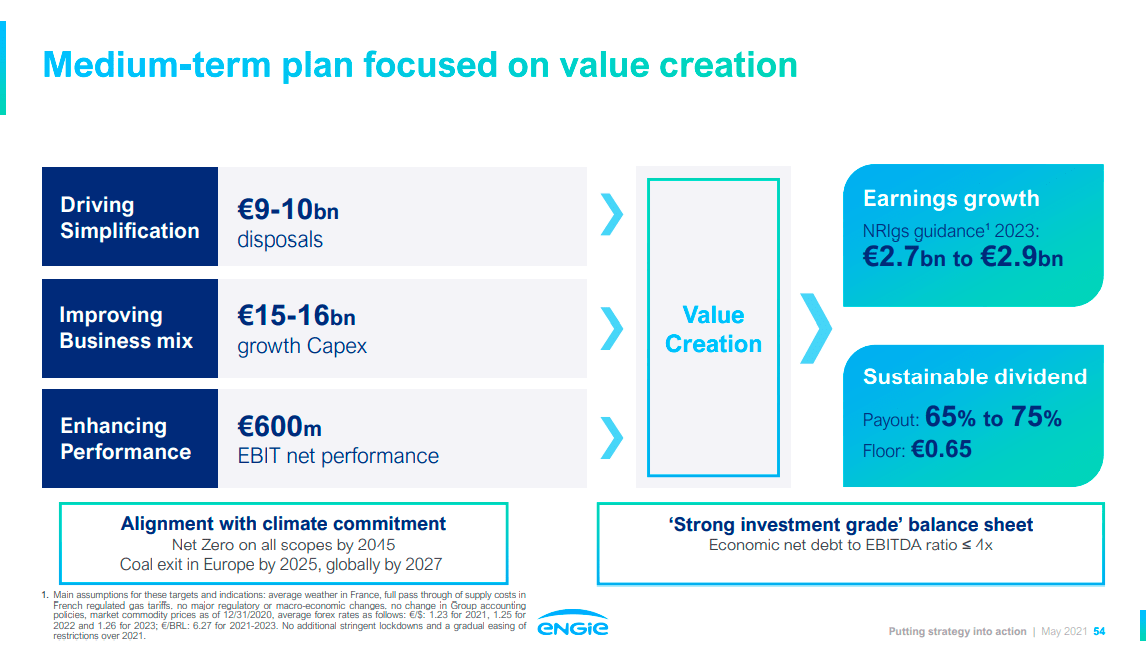

The previous chart shows the Earnings and dividend targets for 2023 and these were set in 2021. Through sales of €9-10B, significant growth in CapEx of €15-16B, and €0.6B of efficiency gains, the company aims to target €2.7-2.9B of value creation in net income capable of generating a minimum dividend of €0.65.

If this can be achieved in 2023, it is possible to hypothesize that the current dividend yield will be maintained. But to deepen the theme it is necessary to study the characteristics of today’s earnings starting from EBIT.

9M 2022 Financial information

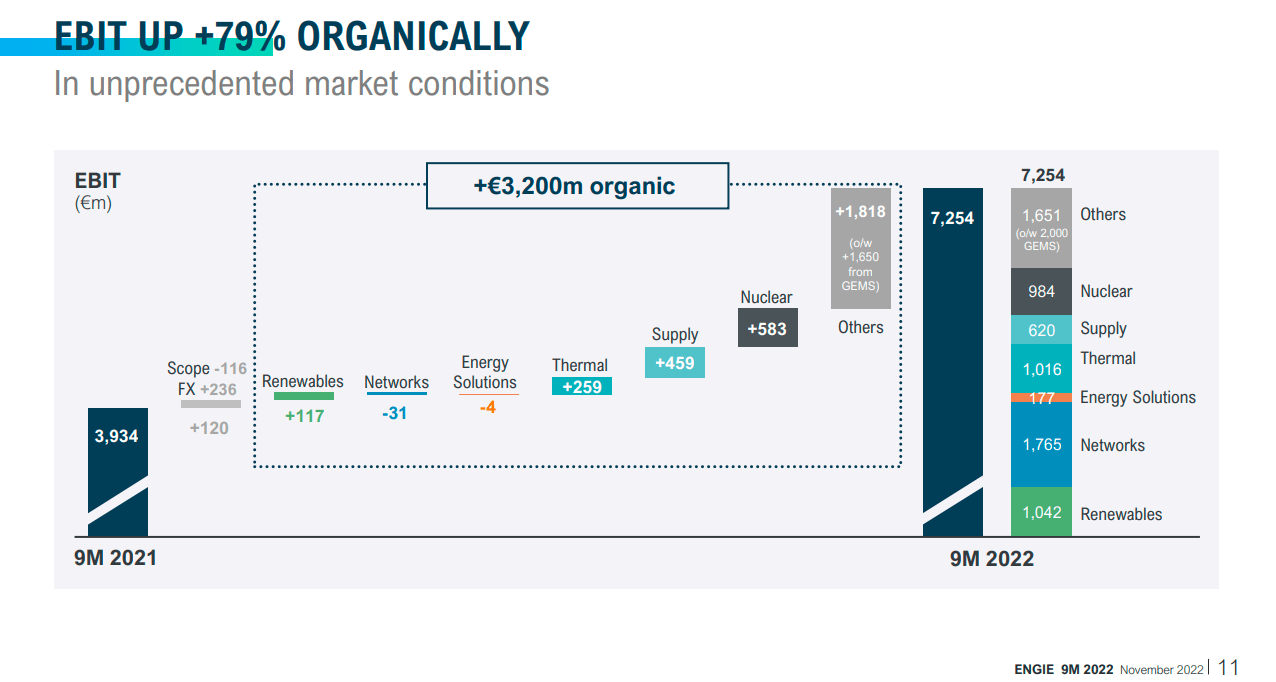

If we compare the EBIT generated in 2022 (9M) compared to the same period in 2021 we can see an impressive increase of 79%. This is mainly due to the creation of value in the GEMS (ENGIE Global Energy Management & Sales) sector (about half of the growth), in second place to nuclear power and third position to the Supply sector. The next question is whether this growth can also be sustainable in the coming quarters or years.

We have seen how the growth in EBIT was mainly generated by the GEMS sector (based on the supply of gas) and therefore let us analyze the characteristics:

9M 2022 Financial information

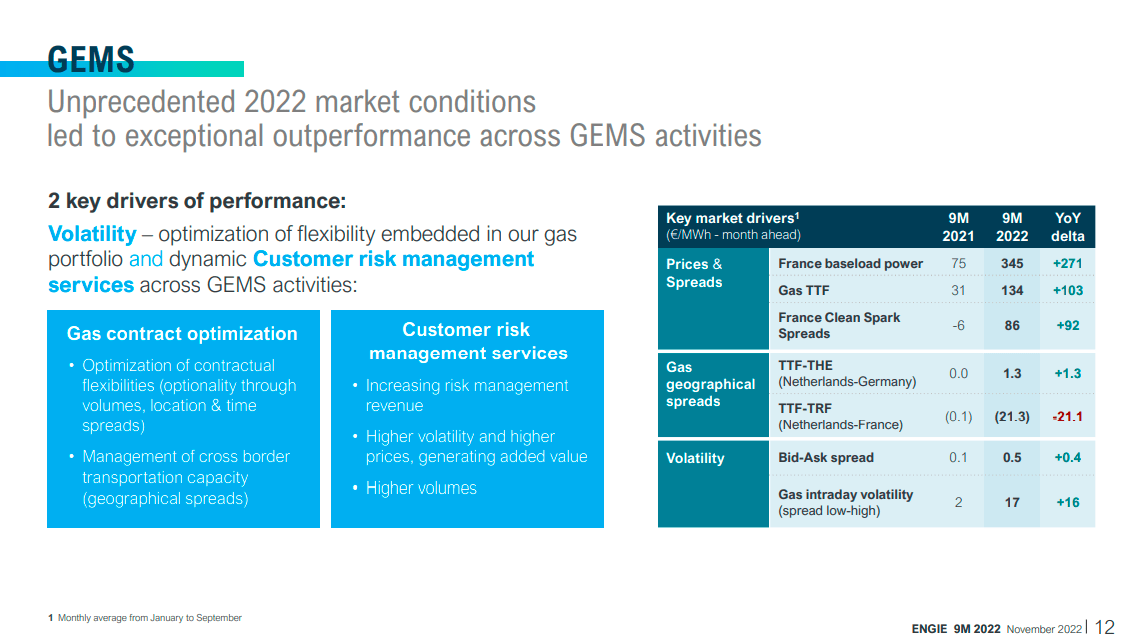

We can underline how the extraordinary market conditions had a heavy impact on performance, and in particular Prices & Spread relating to the France baseload power, which represents the predominant part of the result.

ENGIE is operating in energy markets through GEMS, and in the 2022 second half, the market has shown high volatility with peaks in the price level. This is one of the main reasons why GEMS performance has been so high. Another reason is related to risk management by customers who have asked Engie to increase volumes to hedge against risk during the winter period. This increase in volumes that Engie has been able to supply has been accompanied by an increase in prices resulting in increased profitability for the company.

The next question is: will these market conditions continue in 2023? We can borrow the answer from the management who during the last earnings call said:

So, there is a sensitivity to price, for sure, in the absolute level because part of the remuneration is based on price. But I think that the assumption that you will make about the volatility in the market and also the appetite of customers to go for more risk management are also critical. And we can be reasonably optimistic that, in the next quarters, if not in the next few years, this volatility could stay at a higher level. For sure, it is helping GEMS to boost their earnings power.

Therefore, even if it is very difficult to be able to say that the conditions of 2022 will remain intact, we can underline how the company considers the possibility of managing volatility and high prices also.

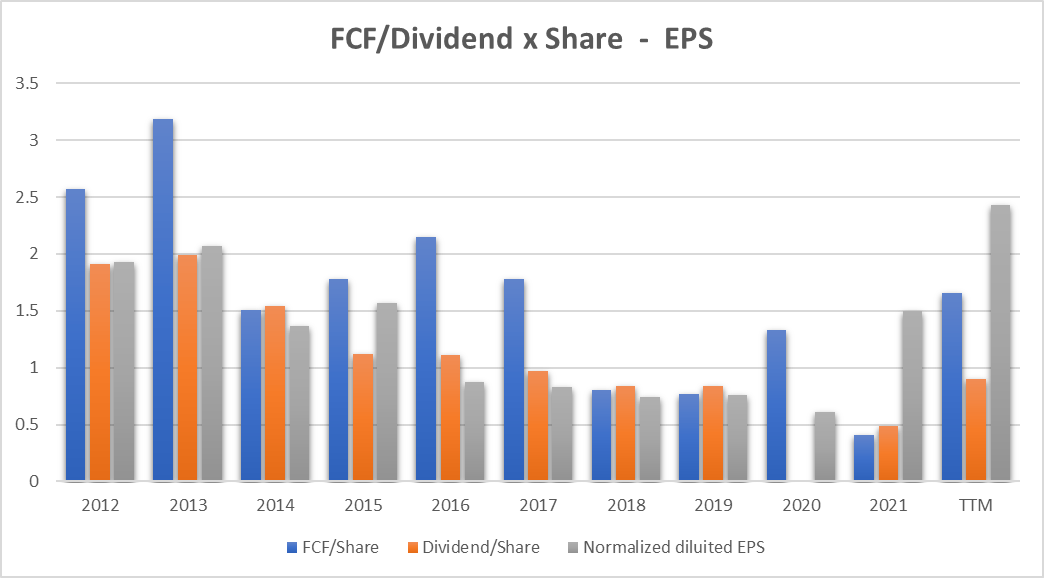

Free Cash Flow and Dividend

Seeking Alpha + Author Graphs

Looking at the graph above we can see the long-term trend of the Free Cash Flow per share (blue bars), of the EPS (grey bars), and finally of the Dividends per share (in orange). Except for the year 2020 when the company decided not to pay the dividend, we can see how this follows the EPS trend almost perfectly. Since 2021 we have been witnessing a corporate transformation and the growth trend has reversed, basically guaranteeing further growth in the dividend. We have seen in the previous paragraph how the extraordinary conditions of 2022 have allowed for an extraordinary EBIT and we have underlined how these conditions of volatility and high prices can continue also in 2023. My expectation is therefore that the dividend can remain constant or grow in the next few quarters.

Valuation

Earnings Power Value Model

Assuming that the cash profit remains constant over the long term, I use the EPV (earnings power value) method to calculate the share price

The method starts with EBIT. The second step is to add depreciation and amortization and then subtract stay-in-business CAPEX.

The result is the Cash Trading Profit

I then subtract the taxes by calculating the amount using the actual tax rate that the company pays.

The result is the After-Tax Cash Trading Profit

To calculate the total company enterprise value I divide the After-Tax Cash Profit by the interest Rate I define as fine for this kind of Company (ENGIY is a low-risk company so I decided to use 8%)

The result is the Total Company Earnings Power Value. Dividing the result by the total number of shares we find the value per single share.

The table below shows the calculation for ENGIY

|

EBIT |

11,935.00 |

|

Dep & amort |

4,625.50 |

|

CAPEX |

-8,560.00 |

|

Cash Trading Profit |

8,000.50 |

|

TAX |

29.00% |

|

TAX |

-2320.15 |

|

After TAX cash profit |

5,680.36 |

|

Interest Rate |

8% |

|

EPV |

71004.44 |

|

Share in issue |

2,551.10 |

|

EPV per share |

27.8 |

$27.8 represents the share price valuation using the EPV method. If we compare the data with the current market price ($14) we see that the current price could be seen as very cheap.

FCF/Share Model

To define a maximum buying price, I use also a formula based on FCF/Share and interest rate.

The formula is:

Maximum buying price = Cash profit per Share/interest rate – 20% (safety discount)

If TTM Cash Profit per share is $1.66

Interest Rate=inflation Rate = 7.1%

Maximum price before Safety discount = 1.66/7.1%= $23.4

The maximum price at 20% discount = $19.5

Under the FCF/Share analysis, it seems that the actual price of $14 is cheap.

Peers Comparison

To compare ENGIY with similar companies in terms of market capitalization in the Multi-Utilities industry I have defined the following peers:

- Consolidated Edison, Inc. (ED)

- Public Service Enterprise Group Incorporated (PEG)

- WEC Energy Group, Inc. (WEC)

- DTE Energy Company (DTE)

- Ameren Corporation (AEE)

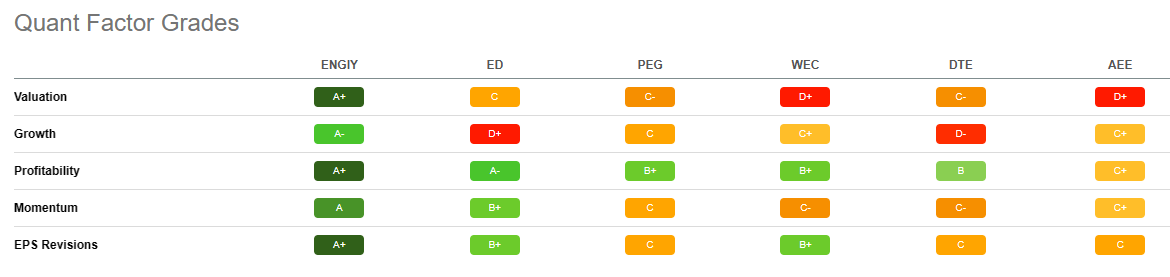

Using Seeking Alpha’s Quant Ratings we have a ‘Strong Buy’ verdict related to the ‘Hold’ or ‘Buy’ rating of the others company.

Seeking Alpha

Under the Quant Factor Grades point of view, we can see how Engie is outstanding in every area from Valuation to Profitability, and EPS Revisions. Only in Growth the grade is not outstanding but is a respectable ‘A-’. This comparison allows us to understand how at this moment Engie has all the positive ratios in his favor and that his peers are far away.

Seeking Alpha

Also related to dividend yield we can state that Engie represents the best in class with a 6.48% compared with the 3.45% of the second. Also under the 4 Year Average Yield, Engie is the best performer with a 4.38% and this could represent a long-term winning strategy.

Seeking Alpha

Geopolitical uncertainties, market volatility, and lack of clarity on the part of Governments are the major risk factors

At the moment there are two factors that most identify uncertainty in corporate accounts: nuclear provisions and taxes in Europe.

Reading the last Conference call:

ENGIE has been expecting for years the implementation of solutions for nuclear waste management by Belgian authorities and as these solutions are not yet fully available, especially with regards to low-level radioactive waste, ENGIE has been and is incurring significant extra costs for €1.3bn. We are now reviewing our legal options to claim back this amount.

We can understand how the risks associated with the governing provisions of a single European country such as Belgium can affect the cost level for a large portion of EBIT.

Under the tax laws in Europe, there are 3 issues with significant impact on Company P&L: Belgium, France, and Italy have an inframarginal rent cap that could be implemented also retroactively and this could mean a great new impact on net profit.

What could happen with government provisions regarding nuclear power and taxes is a clear example of the need to have a clear path beforehand that can give precise guidelines to allow for a correct allocation of corporate capital.

In addition to the above, the issue of global market uncertainty which generates high price volatility should also be highlighted, which must also be added to the profound issue of climate change.

Conclusion

Engie represents a global energy company with a strong balance sheet. The last year has recorded extraordinary market conditions mainly due to high market volatility and prices that have reached historic peaks. The company capitalized on the situation to the maximum, managing to generate an important margin ratio and also to sustain a high dividend yield. The Free cash flow if compared to the EPS is able, in my opinion, to maintain this dividend also in the next quarters. Ultimately, a particularly convenient share price valuation allows you to open a low-risk long position. My rating is Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment