Andres Victorero

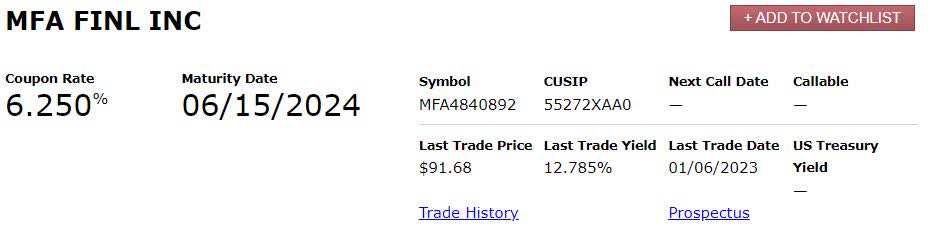

MFA Financial, Inc. (NYSE:MFA) is a real estate investment trust (“REIT”) that specializes in the investment of loans and mortgages (referred to as mREIT). Like its peers, the company has been put through the wringer in 2022, with higher interest rates and lower mortgage demand. As a result, the company’s short-term bonds, which mature next June, are trading at 91 cents on the dollar and yielding more than 12.5% to maturity. While short on duration, I believe these bonds are a good source of short-term income for investors.

FINRA

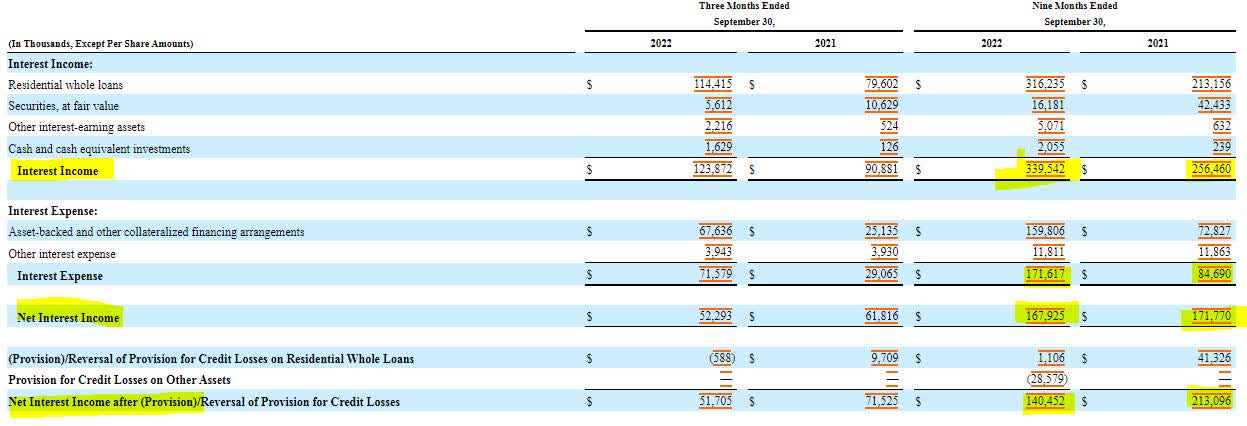

MFA’s income statement highlights its simple mode of operation. The company’s main source of revenue is interest off its investments, and its main source of expenses is the borrowing cost of its collateralized financing arrangements. In the first nine months of 2022, higher interest rates increased both revenue and expenses, but ultimately, net interest income declined by slightly more than 2%. Despite higher interest rates, the company is managing to balance its income against its borrowing cost.

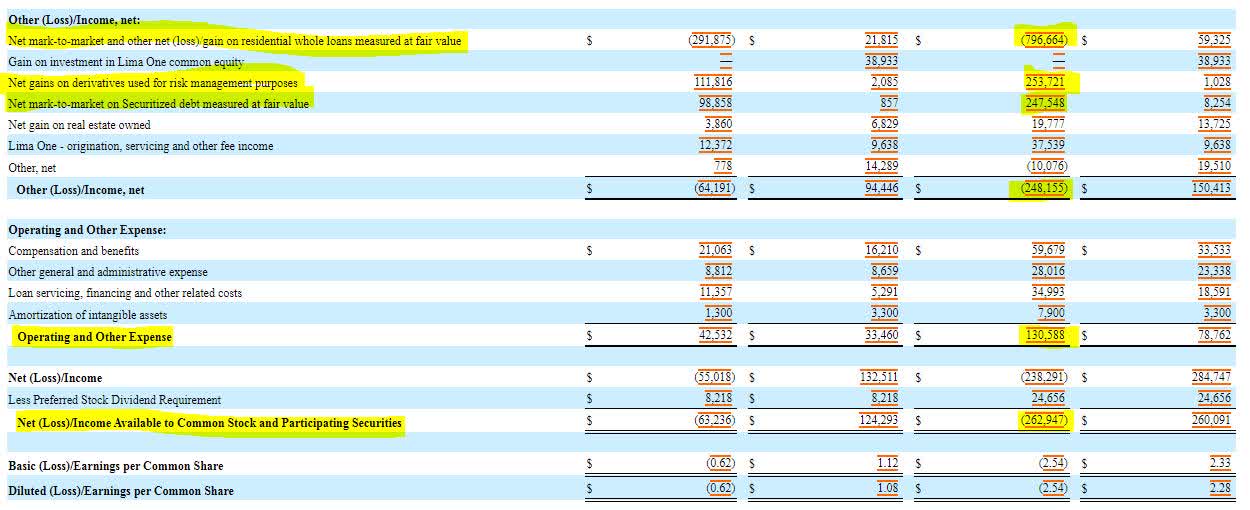

A deeper dive into the income statement shows a major loss of $800 million on mark to market adjustments. These adjustments reflect the lower value of MFA assets due to higher interest rates. It is a noncash adjustment and is offset by $253 million in gains from derivatives used to hedge against higher rates. Ultimately, the company’s higher operating expense has me hesitant to commit to a longer-term investment such as preferred or common equity, but there is nothing in the income statement to suggest immediate risk to the operation.

SEC 10-Q SEC 10-Q

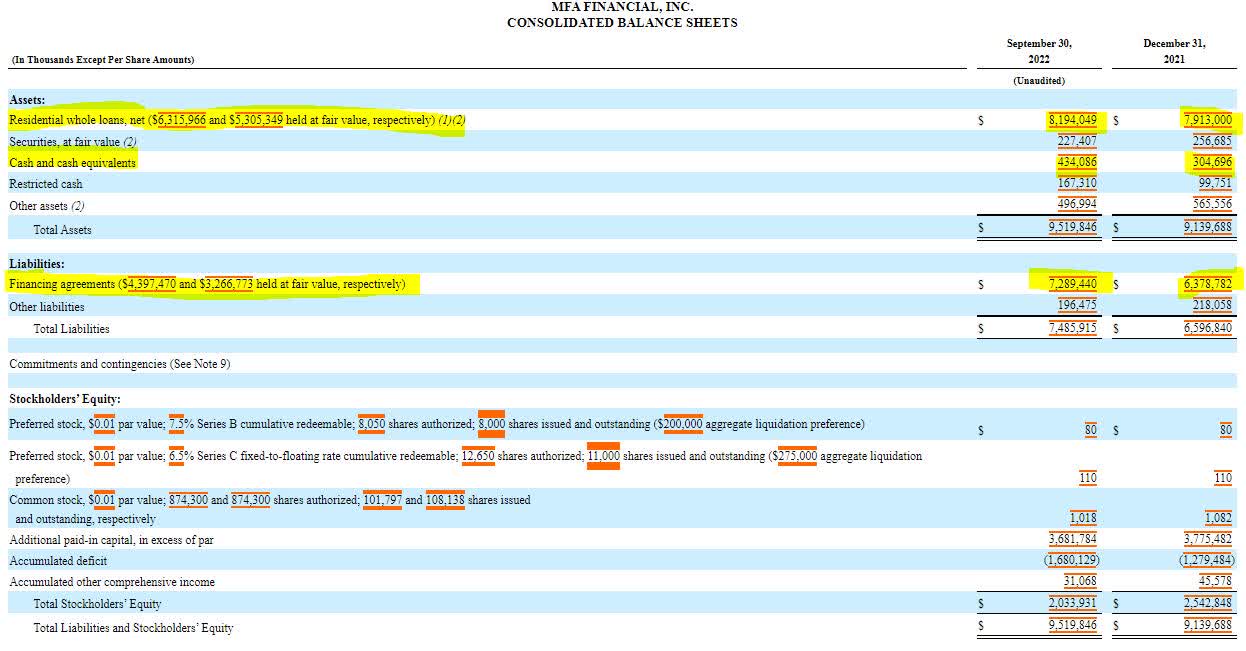

The balance sheet of MFA Financial further exemplifies the simplicity of its business. The entire balance sheet mainly consists of residential loans and cash as assets and financing agreements as liabilities. It is important to note that shareholder equity has declined specifically due to the write-down and decrease in the value of the company’s residential loans. It’s also important to note that cash on hand (both restricted and unrestricted) has increased in 2022, creating a larger buffer for the company.

SEC 10-Q

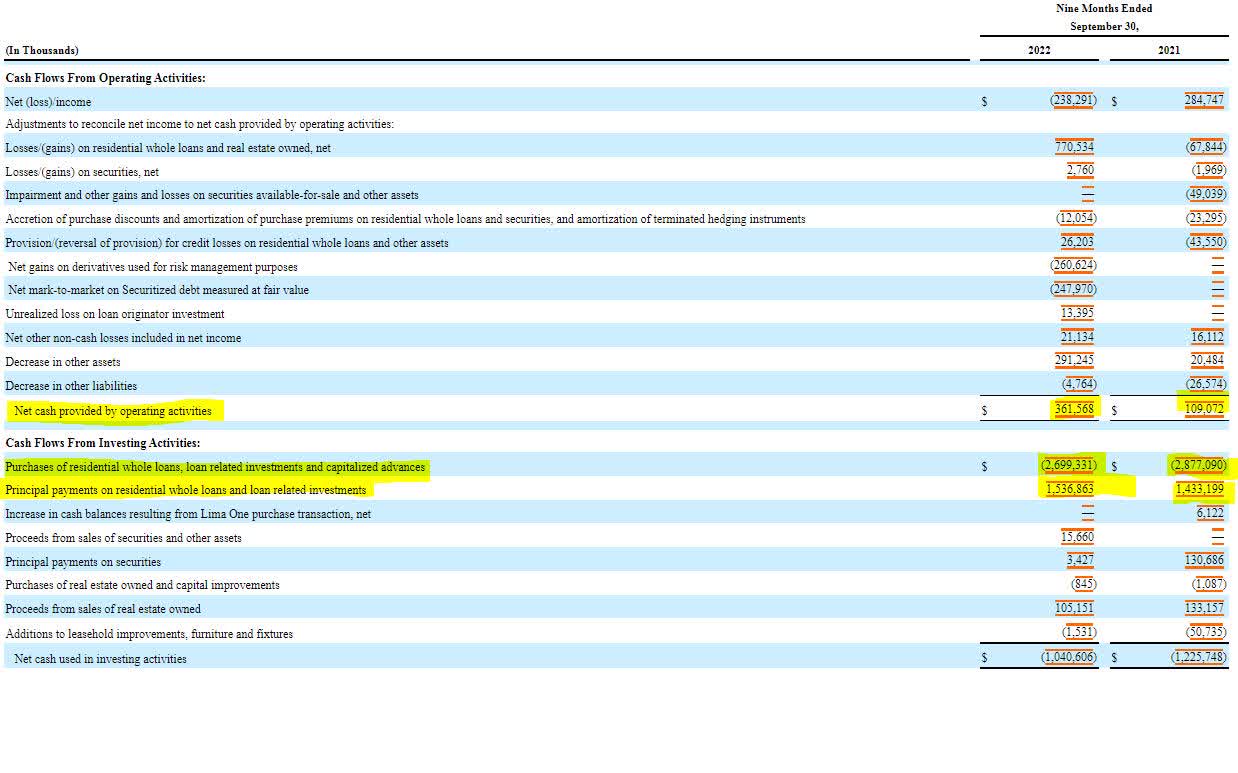

MFA’s cash flow statement paints a somewhat stronger picture than the income statement. The company has managed to more than triple its operating cash flow to $361 million compared to the same period in 2021. MFA noted in its third quarter earnings call that it had gotten more selective with its loan purchases, and this can be illustrated by looking in the investing activities where purchases of residential loans slowed by nearly $200 million from 2021.

SEC 10-Q

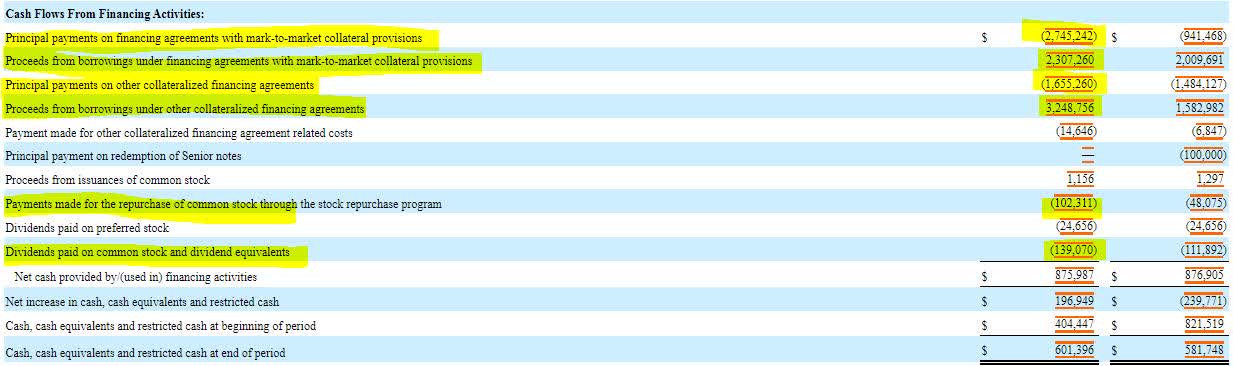

MFA has been able to cover dividends through cash flow from operations so far in 2022, but the company is walking a delicate tightrope when it comes to loan origination. MFA opted to lever itself further by borrowing nearly $1 billion to acquire loans in 2022. If these loans do not perform to management’s expectations, and MFA would need additional liquidity, the company could further reduce its dividends (already cut once in 2022) and halt its stock buy back program, freeing up at least $300 million in cash flow.

SEC 10-Q

While higher interest rates lead to higher interest expenses for MFA, the company has done a good job mitigating interest costs with its weighted average interest rate at 3.6% versus 2.4% at the end of 2021. The convertible notes represent the highest debt servicing cost. Fortunately, MFA can redeem these bonds with cash on hand if it wishes, lowering its interest expense, providing a return to fixed income investors, and avoiding a higher interest rate in refinancing.

SEC 10-Q

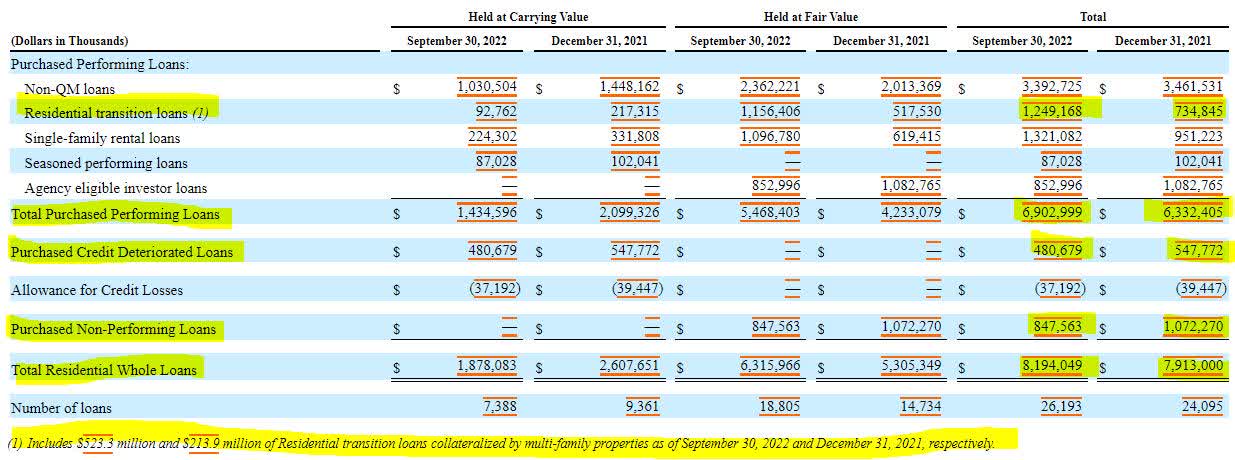

For MFA, the risk is clearly higher interest rates. Higher interest rates are a double-edged sword as they reduce the value of the company’s assets and increase their borrowing costs. The company could also face lower incomes from higher mortgage delinquencies and foreclosures. Fortunately, MFA has changed its asset composition by reducing the number of credit deteriorated and nonperforming loans while increasing the number of loans it holds on rental properties and multifamily housing.

SEC 10-Q

MFA has also provided a “shock table” to show what the company’s assets would be worth should interest rates rise or fall. According to their calculation, should interest rates rise 100 basis points, the company’s net asset decline would be $109 million, easily absorbed by a balance sheet with $2 billion in equity. Additionally, the company would experience a 1.58% increase in net interest income, which would increase cash flow and the company’s ability to reduce debt.

SEC 10-Q

As a side note, this debt issuance is convertible, but only at the option of the holder. While the prospectus notes the conversion value as $7.95 per share, it’s important to note that MFA Financial went through a 4:1 reverse split in 2022, which now values the conversion at $31.80 per share, about 2.5 times the current share price. It goes without saying that I advocate investors holding this debt to maturity and exchanging it with cash versus common shares.

CUSIP: 55272XAA0

Price: 91.68

Coupon: .25%

Yield to Maturity: 12.785%

Maturity Date: 6/15/2024

Credit Rating (Moody’s/S&P): Not Rated

Be the first to comment