Energy Transfer (NYSE:ET) and Enterprise Products Partners (NYSE:EPD) are two of the largest pipeline companies in the USA.

With operations spanning North America, ET and EPD generate huge amounts of revenue and cash flow. Although they don’t compete directly with each other, their differences in business practices and management are constant themes here on Seeking Alpha.

That article generated over 500 comments, a record for me.

In this article, I will compare the two’s potential based on their 2022 quarter 2 results and see what has changed.

1. With a combination of more than 160,000 miles of pipelines, ET and EPD pipelines span North America

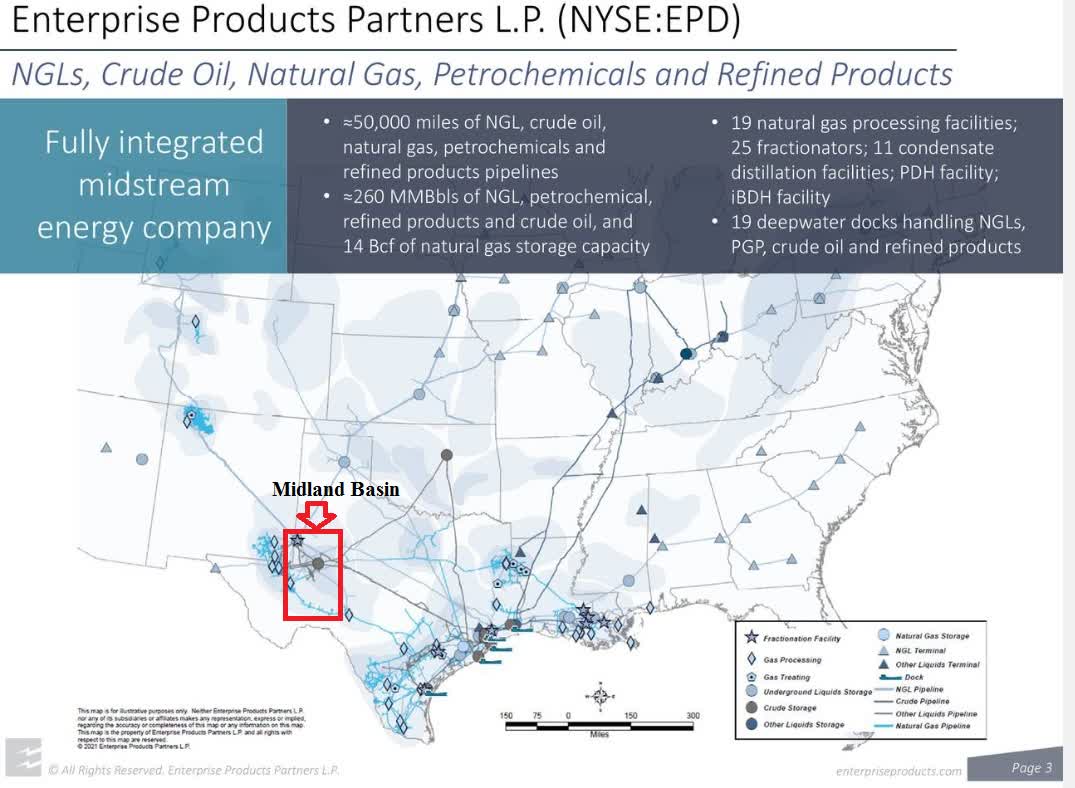

As the map below shows, ET (110,000+ miles) and EPD (50,000 miles) have an enormous pipeline footprint. Both companies have their major concentrations of production facilities in Texas and are headquartered there, ET in Dallas and EPD in Houston.

The mileage has changed somewhat due to acquisitions and dispositions by both companies since last July. ET sold its 51% interest in ET Canada for about $270 million in March. More importantly, ET acquired Enable Pipeline for stock in December 2021.

Energy Transfer

In January, EPD acquired Navitas Midstream Partners for $3.25 billion in cash. Navitas added a valuable 1,750 miles of pipelines, mainly in the Midland basin where EPD resources are limited.

EPD and author

ET has a larger footprint extending into Florida, and ET has a large terminal presence in the North East.

ET was founded in 1996 and EPD in 1998.

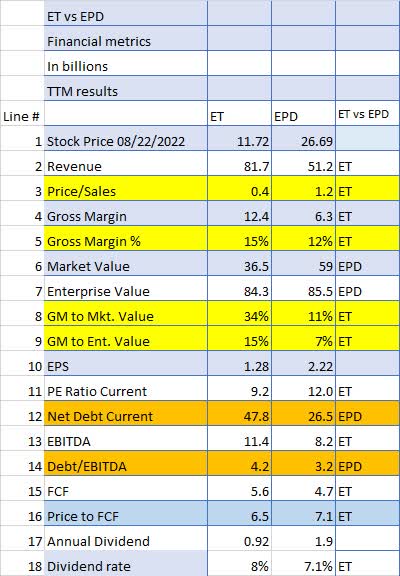

2. Financial metrics

When we look at the financial metrics comparing the two companies on a TTM (Trailing Twelve Month) basis, several metrics jump out indicating how underpriced ET is versus EPD.

Seeking Alpha and author

Looking at the yellow outlined items we can see that ET’s price-to-sales ratio (line 3) is 1/3 of EPD’s, and ET’s gross margins (Lines 5, 8, and 9) are much higher; on every metric, it is indicating that either ET is underpriced or EPD is overpriced relative to each other.

However, EPD’s more conservative approach to debt shows an advantage relative to ET’s in net debt (Line 12) and the debt to EBITDA ratio (line 14).

Looking over a longer period of 5 years, EPD’s 48% total return, which includes distributions, is much better than ET’s at 8%.

Seeking Alpha

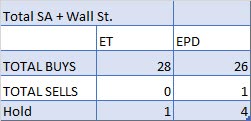

3. Analysts’ ratings show both companies are well-liked by the investment community

Both Seeking Alpha writers and Wall Street analysts love, love, love these two stocks. The total of 54 Buy recommendations and only 1 Sell, are by far the highest rating values I have seen in any of my comparison articles.

Seeking Alpha and author

Interestingly enough, quants are not nearly as excited as the analysts, with a very modest “Hold” call for both stocks.

Seeking Alpha and author

What do the quants know that the rest of us do not?

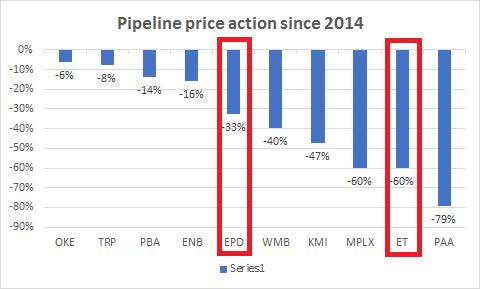

4. Historical price trends continue to be negative for both companies

If we look at the prices for midstream companies from 2014 to the present, we can see a decided downward trend.

NASDAQ and author

Note that carnage is universal, and even a conservative stalwart like EPD has seen a crushing decrease in the share price of 33%.

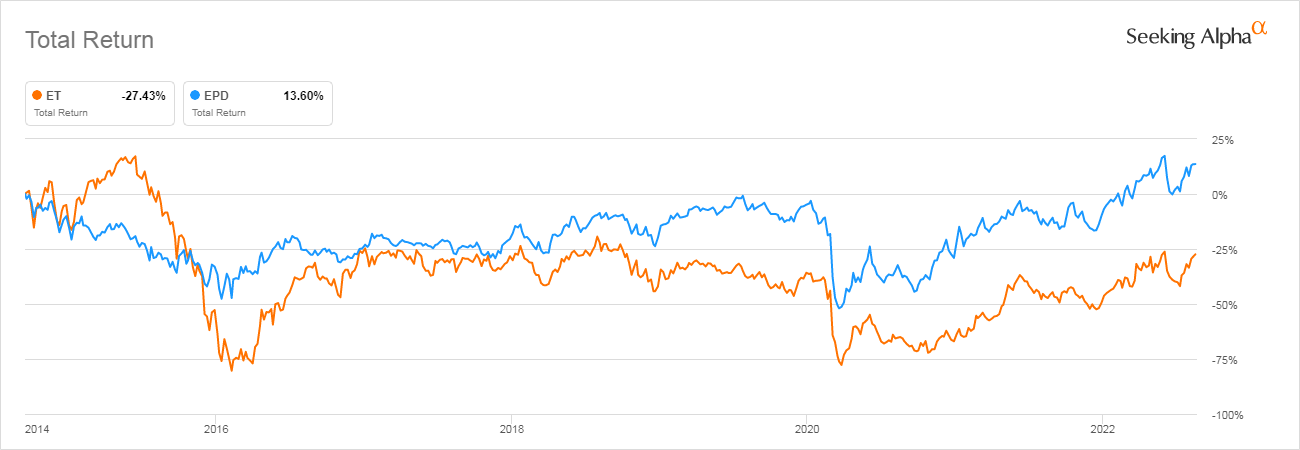

The following chart compares ET versus EPD total return since September 15, 2014. It shows that over that extended time period when both stock’s share prices dropped significantly, EPD returned a very modest profit of 13% to investors if you include the dividends. One would have to question whether less than 2% per year return was worthy of an investment in EPD 2014.

Seeking Alpha

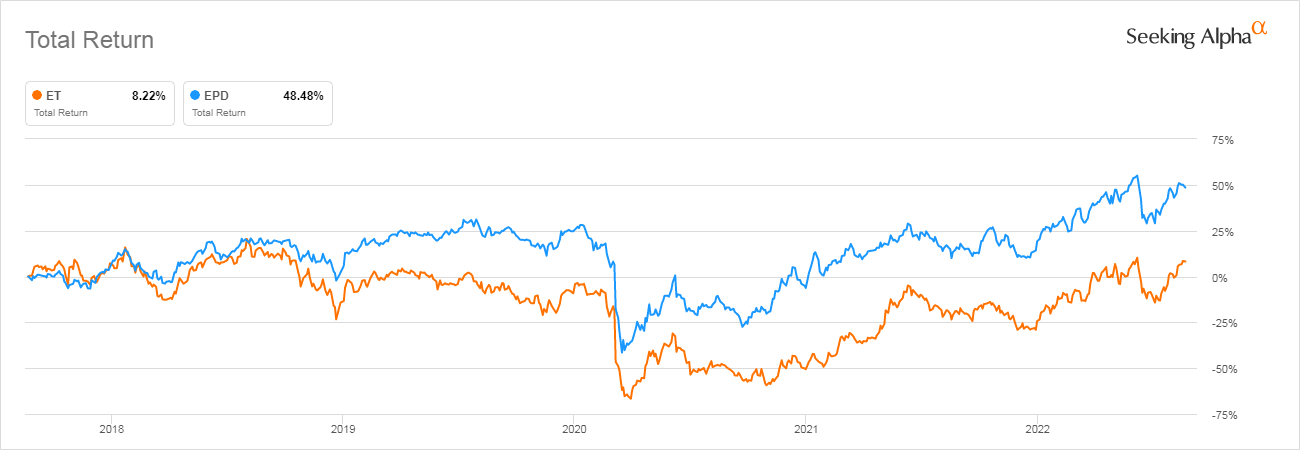

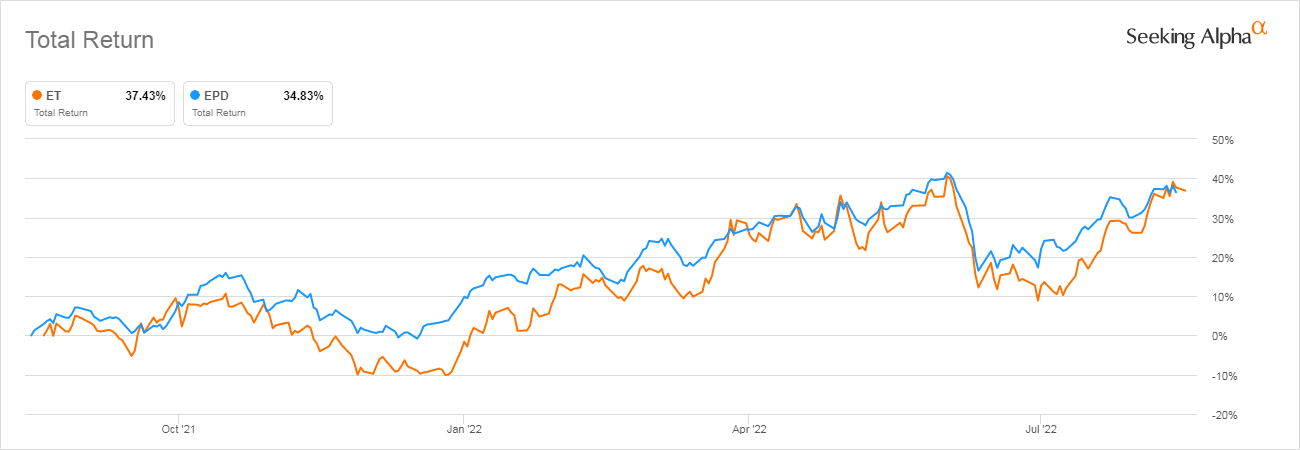

Over a much shorter period of time, one year, ET actually outperforms EPD on a total return basis perhaps signifying the beginning of a turnaround for ET.

Seeking Alpha

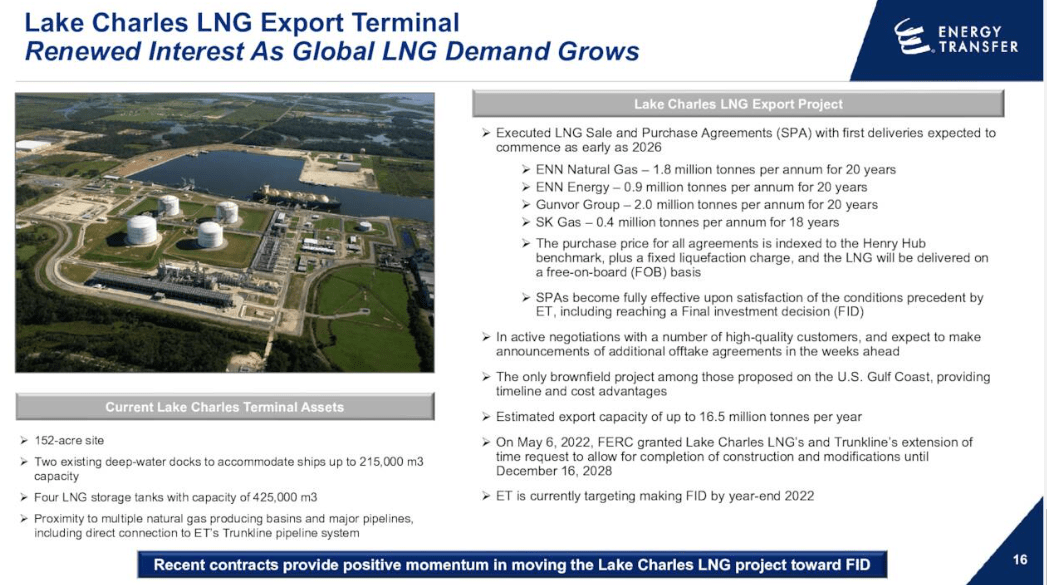

5. Is ET looking to be a quasi Cheniere?

ET’s management has spent a lot of time recently talking about establishing an LNG export terminal in Lake Charles, LA. It already has contract commitments of more than 5 million tons per year and is expecting more agreements soon.

CEO Tom Long:

Year-to-date, Lake Charles LNG has executed five LNG offtake agreements for an aggregate of 5.8 million tons per annum.

and;

We’re also in active negotiations with a number of other high-quality customers as we expect to make announcements of additional offtake agreements in the weeks ahead.

The next issue to address is FID (Final Investment Decision) hopefully by the end of the year. Financing will come from multiple resources, not just ET.

As we previously stated, we expect to finance a significant portion of the capital cost of this project by means sale of equity in the project to infrastructure funds and possibly to one or more industry participants in conjunction with LNG offtake agreements.

Energy Transfer

Having an LNG facility will not just generate revenue and cash flow from the export of LNG but will provide new markets for ET’s existing facilities.

Upon completion of the LNG project, we expect to realize significant incremental cash flows from transportation of natural gas on our trunk line pipeline system and other energy transfer pipelines upstream from Lake Charles.

Because of the ever-increasing need for LNG around the world, this effort sounds extremely promising for the years ahead. Offloading the vast majority of the investment risk to 3rd parties is exactly the right business approach.

And Lake Charles doesn’t have to be ETs last LNG facility either.

Conclusion

Pipelines are not the market’s favorite pick right now and likely won’t be in the future either. ESG and negative political headwinds will plague the market for the foreseeable future.

But that doesn’t mean that there is no potential in any MLPs. In ET’s case, the price is low enough that if it just gets back to the MLP median value on a P/E ratio and FCF (Free Cash Flow) basis, they could have a significant upside to at least $15 and maybe $20 if the LNG terminal gets built.

In the meantime, there is little doubt that ET’s management’s near-term goal is to restore the distribution to its previous $1.22 per share, which at the current price would result in an 11% dividend. Personally, I think the $1.22 dividend will be reached within the next two quarters. If it does, ET will not be priced for long at an 11% dividend payout.

On the other hand, EPD is conservatively managed, has raised its distribution for 24 straight years and just this quarter increased it again by 5.6%. But I don’t see how you get much if any capital appreciation from EPD between now and 2025 at least compared to ET.

ET is a strong buy as a turnaround candidate with an extremely high distribution yield.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment