scanrail/iStock via Getty Images

Executive Summary

Enerflex (NYSE:EFXT) acquired its biggest competitor Exterran at the end of 2022. The market is under-appreciating the synergy potential from both cost reduction and revenue perspectives. Enerflex is currently trading at 5.0x EV/EBITDA which is in line with its OFS peer group. However, looking under the hood Enerflex has the features of a midstream company and a manufacturing company, and therefore Enerflex deserves multiples in the range of 7-8x in my opinion. I believe as Enerflex reports a couple of clean numbers post-acquisition, the market will start to re-rate the stock. Even if I’m overestimating the re-rating potential, there will be a natural value shift from debt to equity as Enerflex deleverages the balance sheet with free cash flow.

Situation Overview

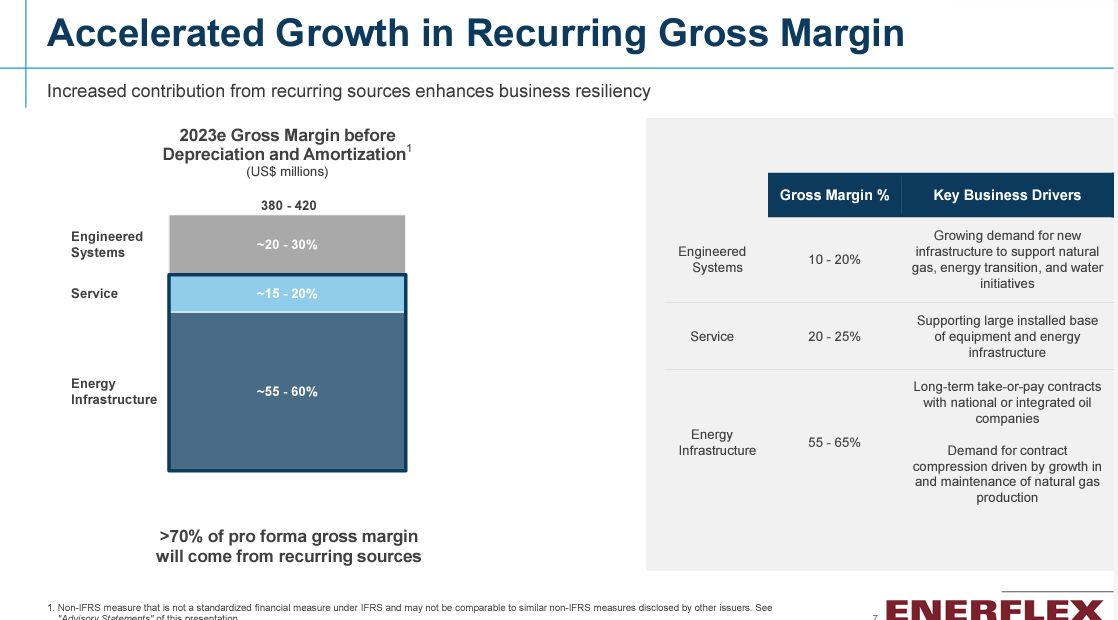

Enerflex manufactures special equipment that serves vital purposes in the natural gas compression and processing value chain. It either rents it out to collect recurring lease payments or it sells it to the customer outright. In the Energy Infrastructure segment (55-60% of pro forma gross margin), customers enter into long-term contracts with Enerflex to build, own, operate, and maintain critical infrastructure for moving natural gas and other gases. The Service segment includes installation, commissioning, O&M, and parts and supports for all products. Together, the Energy Infrastructure segment and the Service segment generate recurring revenue and account for 70-80% of the pro forma gross margin. The Engineered System segment includes the sale of modular natural gas handling equipment. This segment is tied to the demand for new infrastructure to support natural gas, energy transition, and water initiatives.

Company Presentation

While Enerflex is grouped into the OFS peers, the business model is similar to a midstream company because Enerflex’s service is critical to the movement of natural gas and customers are under multiyear take-or-pay agreements. This ensures a high level of stability for the business. In other words, Enerflex is tied to the operating expense of gas producers, not CAPEX.

Valuation

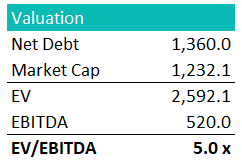

Enerflex issued shares to acquire Exterran. As of October 2022, Enerflex has 123.7 million shares outstanding. In the Q3 earnings release, Enerflex mentioned that as of November 9, 2022, Enerflex had a net debt balance of $1.36 billion. Take the mid-range of the 2023 guidance of US$400 million EBITDA (or C$520 million at 1.30 exchange rate), Enerflex is trading ~5.0x EV/EBITDA.

Author’s Estimate

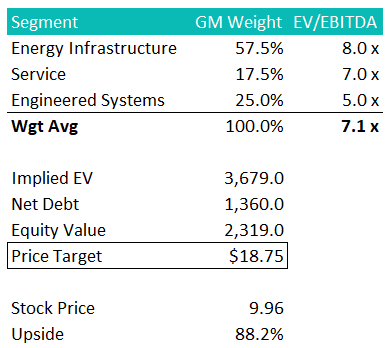

This low valuation is surprising since 60% of the business is gas compression and its direct comp USA Compression (USAC) is trading at ~10.0x EV/EBITDA. Even if we use a conservative 8.0x and treat the Engineering Systems as a generic manufacturing business (assigning a 5.0x multiple), Enerflex should still be valued at least 7.0x on a consolidated basis. The stock should be worth at least $18/share.

Author’s Estimate

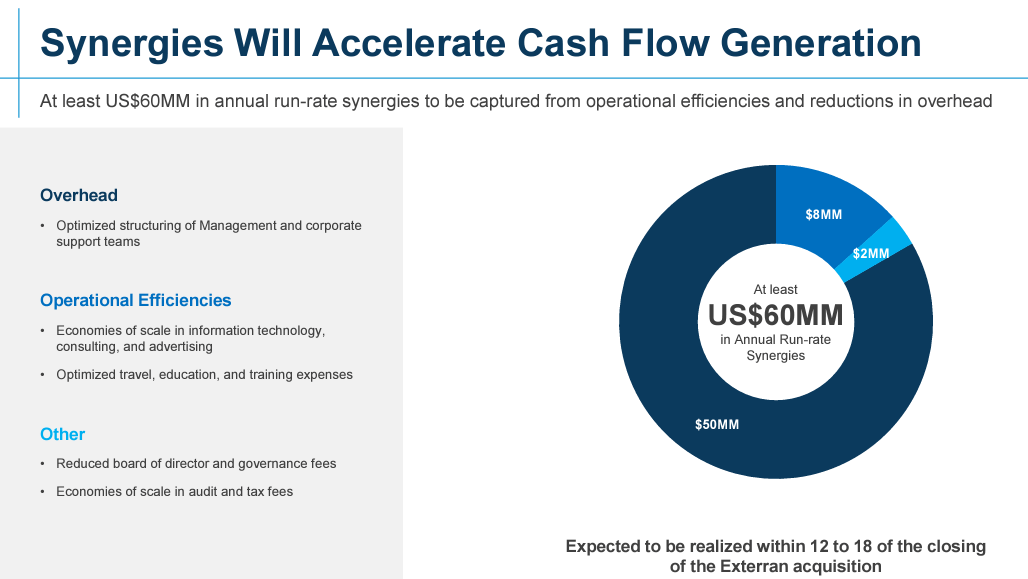

By the way, the EBITDA guidance includes US$60 million cost synergy within the next 12 to 18 months. I’m comfortable with the number since the majority of the synergy is headcount related.

Company Presentation

Macro Tailwind

Natural gas will be the bridge energy between now and the net zero world. The European demand pull is going to cause the sanctioning of more LNG projects in the near term. Inland natural gas production won’t get to the shoreline without pipelines and compressions stations. Overall the demand outlook for Enerflex’s business is pretty bright. Similarly, CO2 sequestration, transportation, and storage require pipelines to move this sin gas. So as governments around the world press on the net zero goal, Enerflex’s products and services will be even more in demand. Investors are not paying for the huge CO2 capture growth potential at 5.0x valuation.

Conclusion

The market has yet to re-rate Enerflex because the Exterran acquisition has just been completed and we haven’t seen what the combined entity can do from a financial results perspective – thus the opportunity. If you are comfortable with the guidance (which is not difficult given the recurring nature of a large part of the business, plus the headcount-related synergy), Enerflex is one of the most obvious opportunities for 2023.

Be the first to comment