miniseries/E+ via Getty Images

November may have been a relatively drama-free month-by 2022 standards-but there was quite a bit going on beneath the surface.

In addition to marking the first back-to-back up months for US stocks since August 2021, November also brought larger-than-expected downticks in key inflation barometers. The question, of course, is whether these readings were a one-off or part of a longer-term contraction investors hope will lead to the end of the Federal Reserve’s rate-tightening cycle-and an eventual return to stock-friendly rate cuts.

On the political front, Republicans managed to eke out a slim majority in the House, creating the divided government many investors prefer, since it tends to hamper the ability of one party to push through potentially inflationary spending packages or new regulations.

Finally, the US dollar weakened the most it has in a single month in nearly five years.

But as welcome as these developments may have been, investors would do well to remain realistic-and patient. Although at the end of November Fed Chairman Jerome Powell confirmed the central bank was planning to reduce the size of its upcoming rate hikes, he also stressed there was still “a long way to go.”1 (The Fed’s next policy meeting concludes on December 14-the day after the next Consumer Price Index report.)

As Morgan Stanley & Co. analysts have noted, while the current market rebound could run through the end of the year, bearish pressures with the potential to produce a new bear-market low may re-emerge after that.

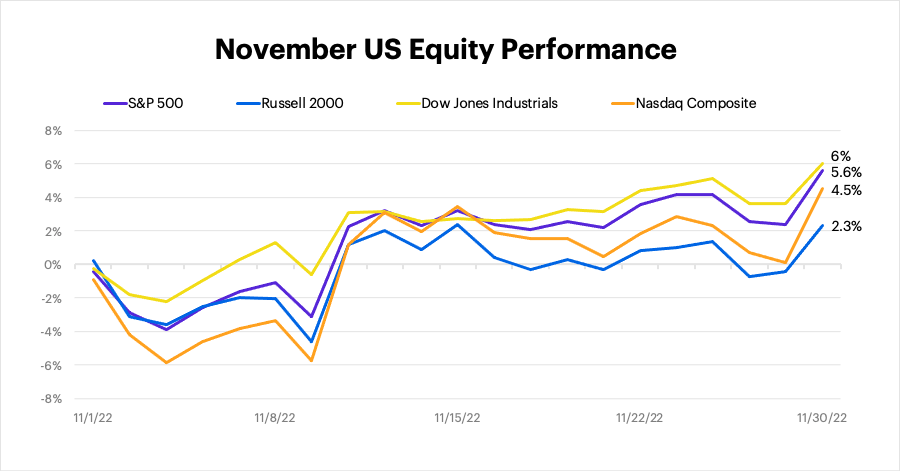

US equities

After some early weakness, US stocks padded their fall rally last month, with the market notching its two-biggest up days of the year on November 10 (after the CPI report) and November 30 (after Powell’s speech). Large caps led the way:

FactSet Research Systems

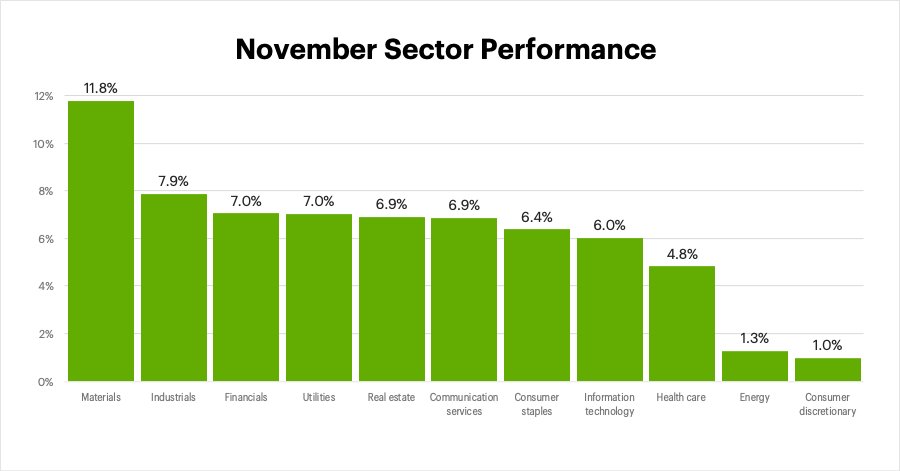

Sectors

Materials led the S&P 500 last month, while the consumer discretionary and energy sectors trailed the market:

FactSet Research Systems

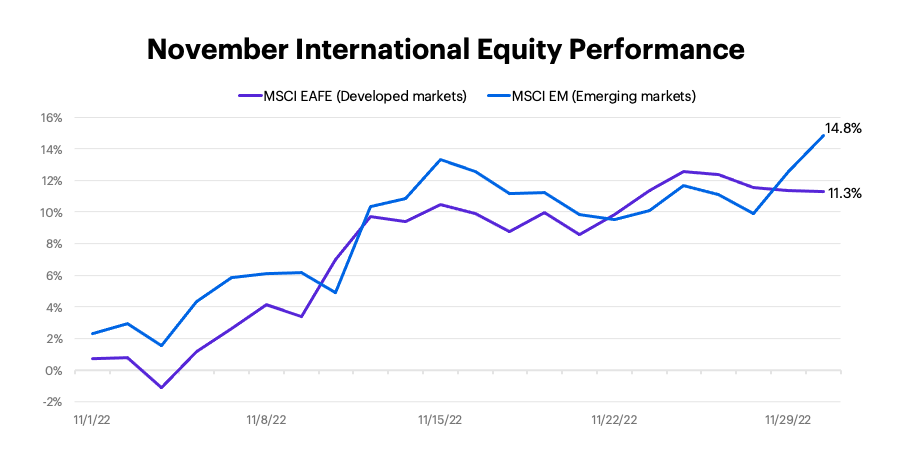

International equities

Amid a weakening US dollar, global stock benchmarks outperformed the US by a wide margin last month. Thanks to a surge at the end of the month, emerging markets led developed markets, but both returned more than twice as much as the S&P 500:

FactSet Research Systems

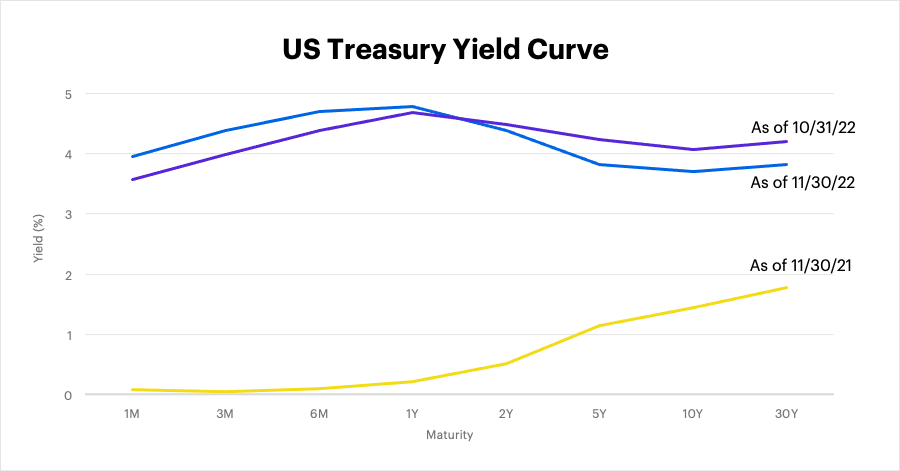

Fixed income

Shorter-term and longer-term interest rates diverged in November, with 1-month to 2-year yields increasing from October, and 5-year to 30-year yields falling. The result: an increasingly inverted yield curve (when short-term rates are above long-term rates, signaling potentially decreased confidence in the longer-term economic outlook). The benchmark 10-year T-note yield closed November down 37 basis points at 3.7%-the biggest monthly decline of the past year:

FactSet Research Systems

Looking ahead

Some thoughts heading into year-end:

- International edge? The relative strength displayed by international equity markets last month has the potential to continue, especially for emerging markets-if the dollar has, in fact, peaked. (Among other factors, a weaker dollar increases the value of assets denominated in other currencies, and it also lowers borrowing costs for emerging markets.) And despite the recent market-rattling protests over Covid-lockdown restrictions, China should eventually reopen, which could help support Asian markets.

- Focus on quality amid potential sector shifts. Even if, as Morgan Stanley & Co. analysts expect, tech and growth lead an extension of the market rebound through the end of the year,2 longer-term investors would do well to concentrate on quality stocks-companies with strong cash flows and the ability to pass on price increases-that have already shown the ability to weather market volatility.

- Fixed income still attractive. Longer-term yields may have dropped slightly last month, but fixed income, overall, is still offering a portfolio “buffer” that simply didn’t exist a year ago.

As a demanding year draws to a close, maintaining discipline, diversification, and focusing on quality remains a tested way to navigate a market that likely isn’t through challenging investors.

Be the first to comment