imaginima

Published on the Value Lab 23/8/22

Energias de Portugal (OTCPK:EDPFY) is a utility we’ve followed here for some years now. At some point it was a bargain, but now it is more reasonably priced in accordance with its assets. For the H1, we see the drought take its toll, but also great performance in solar and wind. Electricity is a valuable commodity, and highly resilient, with prices supported by definite exogenous factors that are unlikely to unwind. Networks businesses demonstrate EDP’s resilience. Overall, there is a lot to like with this stock, but we don’t feel it is compelling with such a broad utility space, and other stocks on better offer.

H1 Results

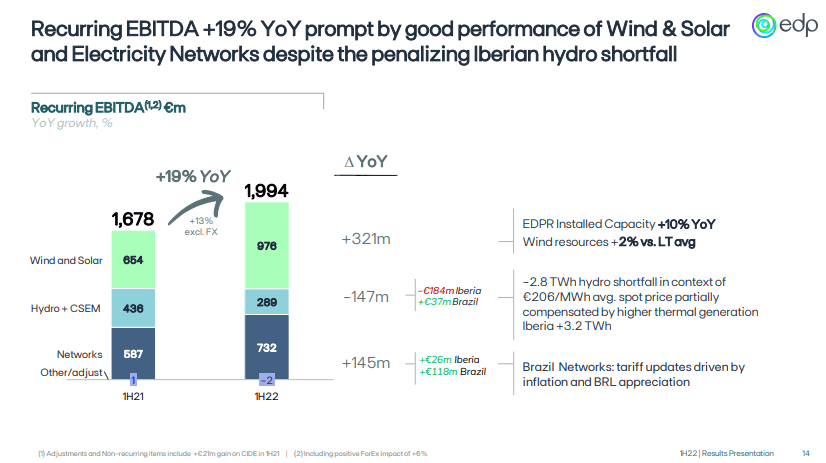

Let’s have a quick look at the H1 results. Overall EBITDA performance was really good, and the real let-down was hydro.

Comprehensive Performance (H1 2022 Pres)

Solar and wind assets performed extraordinarily well driving most of the EBITDA growth. Capacity grew thanks to CAPEX focused on those assets, and so did prices of electricity. Even unit productivity grew. It improved by every metric.

In networks the tariff reviews have resulted in substantial increases in network EBITDA, all from Brazil, where EDP operates through its majority owned EDP Brasil subsidiary that also trades in Brazilian exchanges. In general networks businesses are attractive, because in most geographies, certainly in all of EDP’s geographies, the remuneration is decided by government in a review period every 4 years, and the remuneration is usually connected to interest rates. In Brazil, as a relatively emerging economy, rates have always been rather high, but inflation and rate actions have just made it better. Moreover, the depreciation of the Real has meant that a specific additional measure had to be taken to compensate EDP. Finally, the growth in RAB in the meantime going up 50%, means a larger base to apply the new regulatory WACC on. All of this has resulted in quite the jump in regulated utility income.

Final Remarks

The droughts in Europe have been a major headline. No more watering gardens, and watch out for fires. These have affected hydrology conditions very negatively. Hydro assets were relatively unproductive this H1, and reservoirs fell very substantially by 66%. Hydro will perform badly as long as there are droughts. For investors very concerned about global warming, they should assess hydrology exposures because many environmental commentators believe these droughts will become more frequent. We refrain from judging on that.

The EDP yield is 3.6%, which is good, and it is well covered by cash flows. However, the PE of EDP is now up in the 24x range, and some of the income growth has come from assets not fully owned by EDP, namely EDP Brasil. Moreover, there are other utilities out there that are even more blue chip and similarly invested in the renewable transition, also with networks businesses. We’d look at Enel (OTCPK:ENLAY) in that regard, which trades at almost half the valuation. Overall, EDP demonstrates its quality, and we were glad to have been invested at lower levels. But there are better bargains in the utility space that we’d prefer.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment