mtcurado

Investment Thesis

Eagle Bancorp (NASDAQ:EGBN) is a small-cap regional bank that has suffered a significant setback in share prices as a result of the regional banking crisis earlier this year.

The bank has faced a declining NIM and profitability as a result of the sudden increase in interest rates which, when combined with the banking crisis witnessed in the U.S. in March 2023, has sent shares over 33% lower YoY.

However, I believe that Eagle Bancorp remains a well-managed, run and capitalized regional bank. Their core business of taking in deposits and originating loans remains profitable despite the difficult macroeconomic environment while the bank’s balance sheet is solid.

Given the potential for a 35% undervaluation in shares relative to book value and my belief that the core business model at Eagle Bancorp remains sound, I rate the bank a Strong Buy and have initiated a position worth 8% of my total portfolio value in the bank.

Company Background

Eagle Bancorp Investor Relations

Eagle Bancorp is a full-service community bank that provides banking products and services primarily in Northern Virginia, Suburban Maryland and Washington D.C. The main financial services provided by Eagle Bancorp include real estate, commercial and consumer lending along with traditional deposit and repurchase agreement products.

The bank also deals with small business loans along with the origination, securitization and sale of multifamily Federal Housing Administration (FHA) loans.

Despite being a relatively small regional bank, Eagle Bancorp offers customers various digital capabilities such as remote deposit services, mobile banking services along with access to 13 traditional banking offices.

Interestingly, Eagle Bancorp has ceased origination of first lien residential mortgages for secondary ale as of June 30, 2023.

Since its formation, Eagle Bancorp has been a largely successful, profitable and well-run regional bank that has steadily grown overall deposits, loans and their net interest margins (NIM) while continuing to accurately meet the demands of consumers.

Current CEO Susan Riel has had to face a challenging year when it comes to macroeconomic shocks with multiple surprise demand and supply side factors being compounded by contractionary monetary policy.

Despite the regional banking crisis earlier in April 2023, Riel has continued to pursue what I believe are sound banking practices to ensure Eagle Bancorp remains a profitable and healthy bank for years to come.

Economic Moat – In Depth Analysis

Eagle Bancorp has essentially no economic moat due to their small scale, geographic footprint and ultimately undifferentiated services doing little to tangibly build moatiness for their business operations on a national scale.

However, I do believe that on a regional scale, Eagle Bancorp has managed to build a loyal consumer base thanks to their above average customer service and the overall attractiveness of their service offerings.

Regional banking as a business revolves almost entirely around the very core principles that define the operations of a bank as an entity. In order for banks to generate profits, they must endeavor to attract consumer deposits at a relatively low interest cost while simultaneously providing loans at higher interest rates in order to create a healthy NIM.

While many international banking entities such as Citigroup (C), Bank of America (BAC), and JPMorgan Chase (JPM) have further expanded their business from these basic banking principles to also include corporate banking services, wealth management and special situations services, most regional banks purely focus on the aforementioned basic banking business.

Eagle Bancorp is no exception to this rule with the bank’s business model firmly centered around acquiring deposits at low interest expenses while providing loans at relatively higher interest rates. This is supported by the bank’s non-interest income being very small in comparison to their interest income.

Considering how simple Eagle Bancorp’s fundamental business model is, the real differentiator between regional banks from a customer’s perspective arises from the quality of service and the quality of products that they are provided with.

Most regional banks (including Eagle Bancorp) aim to provide a higher quality of service to their clientele compared to that offered by larger banking institutions with an emphasis on familiarity and friendliness often underpinning their customer service ethos.

The bank also has an extensive range of banking services on offer that provide consumers with competitive financial products.

Services such as high-yield time deposit accounts, savings accounts and everyday loans for automobiles, houses and small businesses makes Eagle Bancorp a surprisingly effective choice for consumers looking to benefit from a holistic set of banking services.

Interestingly, I do believe that Eagle Bancorp appears to have some form of cost effectiveness advantage compared to many other regional banks. The ability for Eagle Bancorp to consistently outearn its competitors both with regards to NIM, efficiency ratio, revenue/employee and ROE suggests that the banks has a very lean operational structure that enables the bank to generate excess returns on both their assets and equity.

While I do believe this cost effectiveness to be a key factor behind my investment thesis into the bank (which I will discuss more in the following Financial Situation section), I cannot confidently assign any real moatiness to Eagle Bancorp from this competitive prowess.

Ultimately, while the bank is very cost effective, it is not necessarily unique in this regard as a handful of other regional banks have also managed to generate similar ROA, ROE and efficiency ratios as Eagle Bancorp.

Overall, while I do not see Eagle Bancorp as enjoying a tangible economic moat due to consumers ultimately facing little switching costs, I still believe that the firm’s fundamental business case is sound. Their focus on providing a high quality of customer service and products to their commercial customers has enabled the bank to consistently grow their total deposits and loans over the last 10 years.

When combined with a clear desire for cost-control in the name of maximizing efficiency, Eagle Bancorp begins to emerge as a relatively attractive regional bank in my opinion.

Financial Situation – In Depth Analysis

Eagle Bancorp has historically been a very profitable bank with strong returns, a high NIM and consistently large net margins characterizing their fiscal past.

Over the last 5Y (spanning from FY22-FY18), the bank has managed to generate averages ROA and ROE of 1.47% and 12.14% respectively. These averages remain essentially unchanged even when considering the past 10Y starting with FY22 which illustrates just how well Eagle Bancorp has managed their business fundamentals over the past decade.

The bank has operated with efficiency ratios ranging between 45-52% over the past ten years which has ultimately enabled Eagle Bancorp to generate 5Y average net margins of 41.11%. Regardless of business, industry or sector, such high net margins are truly phenomenal to see and illustrates just how good of an enterprise Eagle Bancorp has been.

While the banking crisis kickstarted by the bankruptcy of SVB earlier in 2023 triggered a mass selloff in regional bank shares, this event had essentially no real impact on the profitability of Eagle Bancorp.

However, the persistently dovish policy pursued by the Fed has resulted in a difficult macroeconomic environment that has placed strain on the NIM and overall profitability of most banks; Eagle Bancorp included.

The incredibly rapid increase in interest rates combined with a natural cooling in growth from the post-pandemic boom has created a difficult macroeconomic environment seemingly being characterized by stagflation.

For banks, this creates a unique challenge in and of itself whereby a degradation in NIM occurs as a result of the interest cost having to be expensed in order to attract deposits outpaces both the rate of loan origination at new higher rates and the interest income being earned from existing loans.

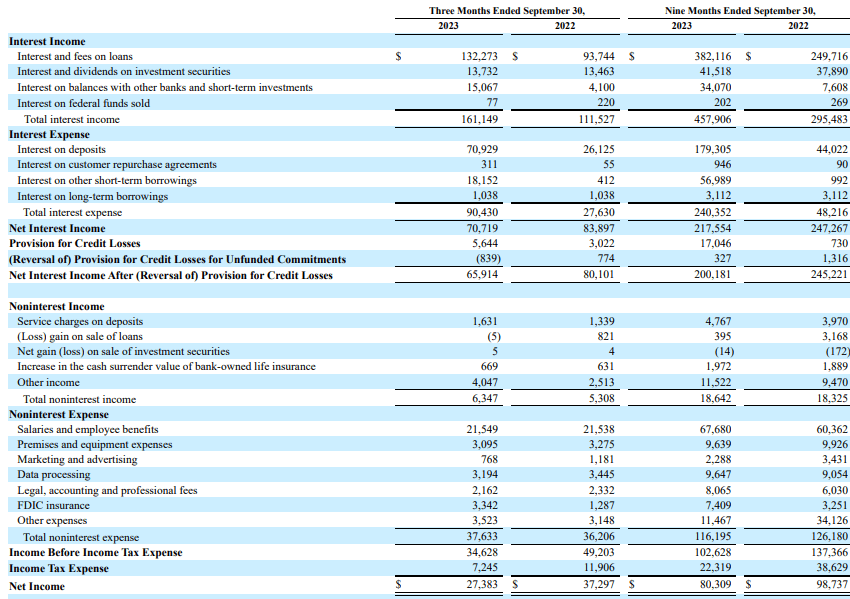

By analyzing Eagle Bancorp’s FY23 Q3 report, it is clear that this exact situation has occurred as evidenced by their income statement.

EGBN Fy23 Q3 10-Q

Eagle Bancorp’s interest income has grown rapidly since 2022 due to the higher interest rates set by the Fed with the bank generating just over $132M in Q3 FY23. This represents an increase of 40% YoY.

Unfortunately, the bank has also seen their net interest expense grow by over 233% YoY to over $90.4M in Q3 FY23. This has left the bank with a significantly slimmer net interest margin of just 2.43% compared to 3.02% in Q3 FY22.

While this significant increase in the cost of deposits for Eagle Bancorp is regrettable to see, it must be noted that many regional banks have seen their NIM decrease to around 1% from similar previous levels of around 3-4%.

This illustrates that Eagle Bancorp has managed to delicately balance the need to offer customers higher interest rate accounts and products with the bank’s own agenda of maintaining a healthy NIM. The fact that overall deposits have increased further supports this hypothesis as it suggests their deposit products are still attractive to consumers.

Net income for Q3 FY23 was down to $27.4M from just over $27.2M the previous year. While this decrease is regrettable to see, the bank’s net margin remains at 37% with a ROA and ROE of 1.12% and 10.06% respectively. These metrics are good regardless of previous results further suggesting that the bank remains well managed despite the tricky macro environment.

Eagle bank did generate around $6M in non-interest income in Q3 compared to $5.3M the previous year with non-interest expenses remaining essentially flatline YoY.

Eagle Bank also significantly increased their provisions for credit losses from just $3M in Q3 FY22 to over $5.6M in FY23. This further increases the flexibility the bank may operate with should a highly recessionary or contractionary economic environment emerge which ultimately further protects its customers deposits and the bank as a business from bankruptcy or illiquidity.

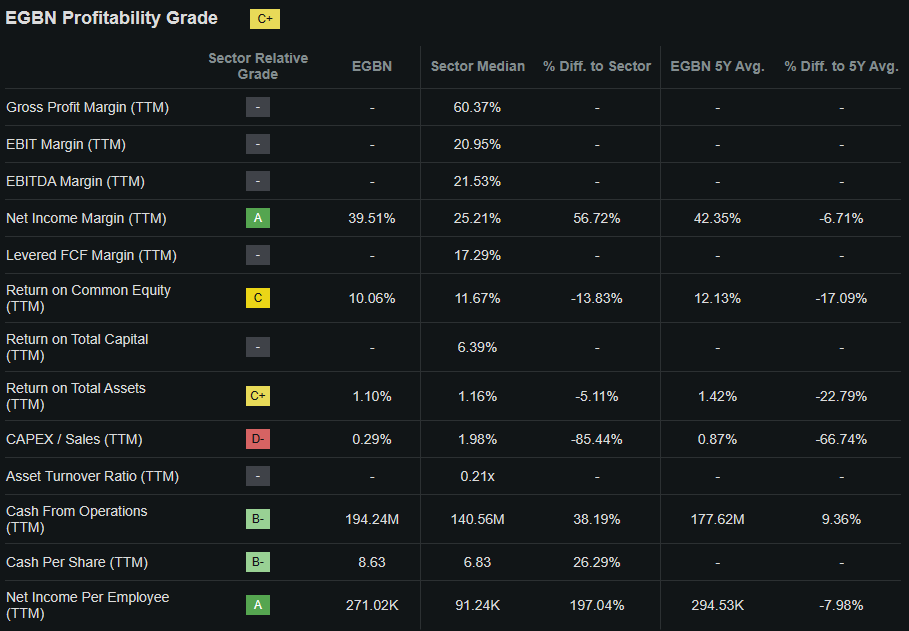

Seeking Alpha | EGBN | Profitability

Seeking Alpha’s quant assigns Eagle Bancorp with a “C+” profitability rating which I believe to be a mostly accurate representation of the profitability situation currently present at the bank. While NIM has certainly decreased, Eagle Bancorp’s management appears to have excellently managed a difficult macro environment with total deposits and loans still growing despite the increase in interest expenses.

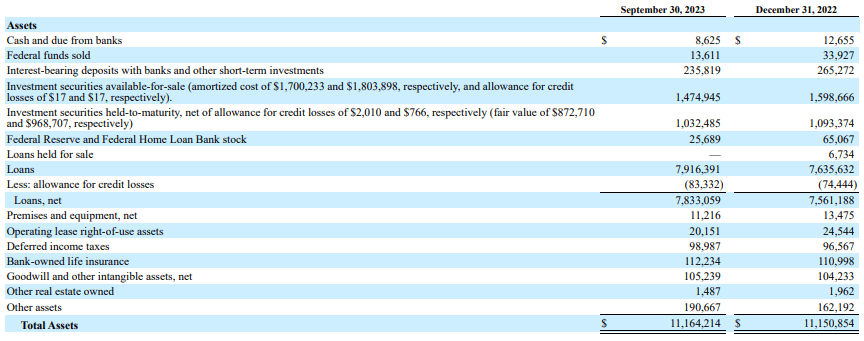

Careful analysis of Eagle Bancorp’s balance sheet is absolutely paramount to understanding what possible investment opportunity may lie in the bank’s shares.

For regional banks in particular (given their primary source of revenues is from primary banking activities) the balance sheet is where the underlying stability, future profitability and overall attractiveness of the bank can be deduced.

EGBN Fy23 Q3 10-Q

I believe that fundamentally Eagle Bancorp has a very high standard of capital allocation with their assets and liabilities appearing to be expertly managed despite the tricky stagflationary macroeconomic environment.

The bank has seen their cash levels decrease quite significantly from $12.7M in Q3 FY22 to just $8.7M in the latest quarter. This 31% decrease can largely be attributed to the higher interest rate environment placing some additional pressure on the banks liquidity and the requirement for increased cash flows particularly towards employee wages and operational expenses.

The bank’s available-for-sale (AFS) investment securities decreased slightly YoY from $1.6B to $1.48B. These are at a fair value of course and therefore represent a discounted value relative to their amortized cost.

Eagle Bancorp has chosen to report their investment securities held-to-maturity (HTM) both at their amortized cost and (thankfully) at the fair value. Given the increasingly inflationary interest rate environment, many of the government bonds purchased by banks at lower interest rates have resulted in paper losses forming in their HTM securities assets which most banks continue to report at their amortized cost rather than their fair value.

I believe this practice is misleading as it inflates many banks assets while helping to coverup any poor managerial decisions made in years prior. Eagle Bancorp’s HTM securities when reported at their fair value have decreased to $872M compared to $988M in Q3 FY22.

The FY23 Q3 figure is also around $150M less than the amortized cost of these securities which illustrates that Eagle Bancorp has suffered $150M in paper losses on their balance sheet.

This relatively low proportional decrease in HTM securities illustrates that Eagle Bancorp’s management has invested in a good selection and mix of securities which allow the firm to be incredibly resilient even amidst a high interest rate environment.

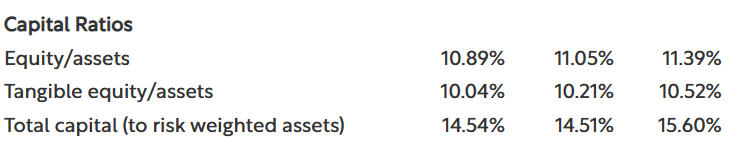

EGBN Q3 FY23 Press Release

The bank’s total assets (adjusted for fair value accounting of their HTM and AFS securities) of $11.16B while total liabilities only amount to $9.95B. Eagle Bancorp also has excellent capitalization levels with equity/assets being 10.89%, tangible equity/assets being 10.04% and total capital (to risk weighted assets) of 14.54%.

The bank has a Tier 1 capital (to average assets) ratio of 10.96% while the bank’s CET 1 (to risk weighted assets) ratio is a very healthy 13.68%.

Eagle Bancorp also operates with an efficiency ratio of 48.8% which is superb while the bank’s loan to deposit ratio is currently 93% as of Q3 FY23. While I would ideally like to see this ratio be closer to around 85%, I believe that given the difficult macro environment, the ability for Eagle Bancorp to maintain a ratio of below 1.0 (less than 100%) illustrates once again the ability held by management to balance profitability with stability.

Seeking Alpha | EGBN | Dividend

Eagle Bancorp pays investors a healthy dividend with an impressive current FWD yield of 5.97%. The firm’s excellent 3-year dividend growth streak is impressive given the macro conditions and suggests that Eagle Bancorp is keen to reward shareholders of their shares with an additional portion of profits.

The bank’s FWD annual payout is expected to be $1.80 with a payout ratio of 47.43%. Eagle Bancorp goes ex-dividend on the 01/10/2024 with the next payout date being 01/31/2024.

At its core, Eagle Bancorp appears to be a very well-run regional bank. Their ability to balance profitability with customer demands and bank stability is excellent to see. I believe that while the bank has been unable to replicate the results generated in years prior, their core profitability remains unharmed.

A more forgiving and growth inducing macroeconomic environment should help the bank to return to higher NIM margins as will time. Quite simply, the more loans Eagle Bancorp will be able to originate during this higher interest rate period, the greater their profitability should be ceteris paribus.

Smart asset allocation and fair value reporting of HTM securities inspires confidence in my mind that the management team at Eagle Bancorp are dedicated to transparency and ethical business practices. The bank has laid out their performance for everyone to see which unfortunately appears to be unique in the current banking industry rather than the norm.

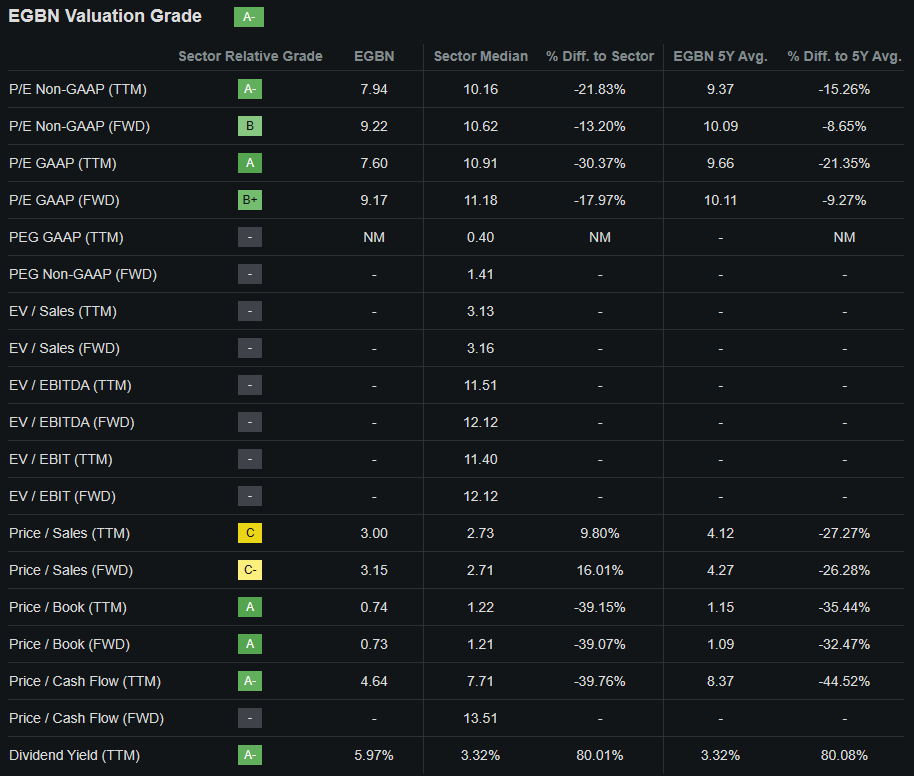

Valuation

Seeking Alpha | EGBN | Valuation

Seeking Alpha’s Quant assigns Eagle Bancorp with an “A-” Valuation grade. I believe this is still a slightly pessimistic representation of the value present within the bank’s stock and perfectly illustrates how even very accurate quant ratings can sometimes poorly represent the real value present in a company’s shares.

The firm currently trades at a P/E GAAP FWD ratio of 9.17x. This represents a significant 10% decrease in the firm’s P/E ratio compared to their running 5Y average.

Eagle Bancorp P/CF TTM of just 4.64x is quite low and once again a whopping 45% lower than their 5Y running average. Their FWD Price/Book of just 0.73x is impressive in my opinion especially when considering the firm’s EV/Sales FWD of just 3.15x.

Considering these basic valuation metrics alone I believe Eagle Bancorp should already start to appear significantly undervalued given the stock’s historic averages.

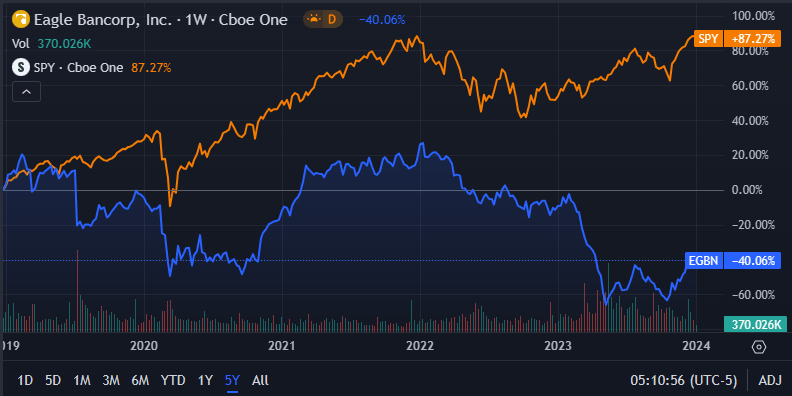

Seeking Alpha | EGBN | Advanced Chart

From an absolute perspective, Eagle Bancorp shares are trading at a significant discount relative to previous valuations with current share prices of around $29.85 representing a five-year low for the stock.

However, when compared to the 87% growth seen in the S&P 500 tracking SPY index over the past five years, Eagle Bancorp has been soundly outperformed by the U.S. market index as a whole by over 120%.

When mixed in with the turmoil witnessed within the U.S. banking industry earlier in 2023, it is understandable that many investors have decided to bet against the bank.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison allow for a basic understanding of the value present in Eagle Bancorp shares to be obtained, a quantitative approach to valuing the stock is essential.

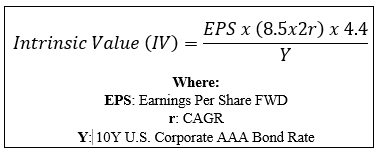

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using Eagle Bancorp’s current share price of $29.85, an estimated 2024 EPS of $2.68, a realistic “r” value of 0.06 (6%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 5.28x, I derive a base-case IV of $41.30. This still represents a significant 35% undervaluation in shares.

When using a more pessimistic CAGR value for r of 0.04 (4%) to reflect a scenario where a globally spanning recession causes Eagle Bancorp’s deposit inflows to drop along with some decrease in noninterest related incomes, shares are still valued at around $36.90 representing a 19% undervaluation in shares.

Eagle Bancorp is also trading far below their tangible book value per share which Seeking Alpha estimates to be $40.64.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that Eagle Bancorp is soundly trading in what can only be considered to be deep value territory.

In the short term (3-12 months), I find it difficult to say exactly what may happen to valuations. The general uncertainty regarding the future direction of both the U.S. and global markets as a whole means predicting the direction for most stocks from a qualitative side is very difficult.

Nevertheless, even despite the recent rally in share prices since early December, Eagle Bancorp is trading at a very cheap valuation relative to the book value and intrinsic value present in shares.

While short-term valuations can be incredibly volatile for small-cap stocks, it is difficult to see how much longer shares can remain this cheap.

In the long-term (2-10 years), I see Eagle Bancorp regaining significant profitability through a better loan origination mix and through decreasing interest rates due on consumer accounts.

I believe that as long as Eagle Bancorp remains conservative when it comes to balance sheet planning and operational efficiency targets, the bank could return to their pre-covid streak of great results and increasing consumer deposits.

Risks

Eagle Bancorp faces some tangible risks with the primary threat arising from a recessionary economic environment trigger significant deposit outflows and lower loan origination levels.

Quite simply, the biggest threat to any single bank is a sudden or prolonged stream of outflows resulting in dropping profitability and liquidity. Eagle Bancorp is quite a small regional bank which ultimately means that their consumer base is relatively more concentrated than that of larger international rivals.

A recessionary period in the United States would almost certainly result in ordinary consumers facing additional pressures on their pocket books thus limiting the ability to save and deposit money in banks. This would result in Eagle Bancorp seeing a drop in total deposits as well as in the value of any deposits present at the bank.

Fundamentally, this would result in a significant drop in profitability for the bank while simultaneously eroding the liquidity present on their balance sheet.

A sudden shock to the economy (as seen with the fall of SVB earlier in 2023) could result in a run on the bank. This would be quite catastrophic although I do not believe Eagle Bancorp would become illiquid thanks to their well-managed AFS and HTM securities portfolios.

Recessions also tend to increase the amount of non-performing loans and assets present at banks due to consumers being unable to meet payment deadlines. This could further decrease the profitability of their loan portfolio.

While these threats are real, I do not believe Eagle Bancorp faces any irreparable damage from such an event. Their well-managed balance sheet in particular should help protect the bank against even a hard-landing recessionary outcome in my opinion.

Conclusion

Eagle Bancorp appears to be a very well managed regional bank. Given their high capitalization rates, great efficiency ratio and solid NIM, I believe that the management team at Eagle Bancorp has not forgotten the basic banking fundamentals that ultimately dictate the profitability and stability of any bank, large or small.

The massive discount currently present in shares both relative to the bank’s intrinsic value and even compared to the book value per share further increases the attractiveness of this regional bank in my mind as current valuations appear to offer a massive 35% margin of safety for deep-value oriented investors.

Therefore, I confidently assign a Strong Buy rating for Eagle Bancorp and have initiated a position in the bank worth 8% of my total portfolio value.

Quite simply, I really like this regional bank. The management team exhibits integrity and ability which is evidence by above average returns and profitability from Eagle Bancorp.

While the banking crisis earlier in 2023 resulted in most regional bank stocks being dumped by investors, I believe this reaction was unfounded at least in the case of Eagle Bancorp.

Be the first to comment