YinYang/iStock via Getty Images

This article series aims at evaluating ETFs (exchange-traded funds) regarding the relative past performance of their strategies and metrics of their current portfolios. Reviews with updated data are posted when necessary.

LVHI strategy

Franklin International Low Volatility High Dividend Index ETF (BATS:LVHI) has been tracking the QS International Low Volatility High Dividend Hedged Index since 07/27/2016. It has a portfolio of 118 stocks, plus cash and positions in various currencies, a 30-day SEC yield of 5.73%, and a total expense ratio of 0.40%. Distributions are paid quarterly.

As described by Franklin Templeton, eligible stocks must pay dividends and be:

- in the MSCI World ex-US IMI Local Index,

- listed in one of 18 developed countries,

- profitable over the last 4 fiscal quarters.

A “stable yield” score is calculated by adjusting the yield of stocks with price volatility, earnings volatility, local interest rates and withholding taxes on dividends. Weights are calculated to maximize the aggregate stable yield score. Limits are set for constituents (2.5%), sectors (25% in general, 15% for REITs), countries (15%) and regions (50%). The underlying index is reconstituted annually and rebalanced quarterly.

The fund seeks to mitigate risks of currency fluctuations for dollar-based shareholders using currency contracts. Hedging positions are usually reset on a monthly basis. The fund is long in USD and short in local currencies of the companies in the portfolio. The idea is that if holdings from Switzerland (or any other country) gain +10% in CHF (or other local currency), the fund gains +10% in USD on this portion of the portfolio. If the U.S. dollar become stronger, the hedge provides excess return. However, currency risk has two sides: if the dollar falls, the hedge is a drag.

If you have a doubt about the strength of the dollar, or if you seek diversification with plain exposure to foreign economies, then you’d better choose a non-hedged fund.

There are also company-specific risks related to currencies, not covered by the fund’s currency hedge. A stronger dollar may be a competitive advantage for a non-USD based company because their products and services become cheaper in USD, but it is a drawback when providers or creditors must be paid in USD.

LVHI portfolio

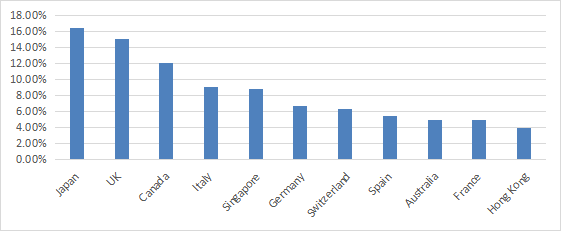

The fund invests mostly in large cap companies (about 82% of asset value). The heaviest countries in the portfolio are Japan (16.4%), the U.K. (15.1%) and Canada (12.1%). Other countries are below 10%. Hong Kong weighs 4%, so direct exposure to geopolitical and regulatory risks related to China is low. The next chart lists the top 11 countries, representing 94% of asset value.

LVHI Country allocation, % of asset value (chart: author; data: Franklin Templeton.)

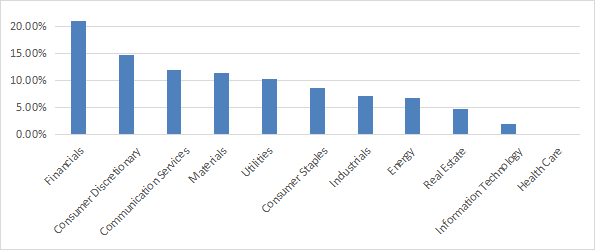

The two heaviest sectors are financials (21% of asset value) and consumer discretionary (14.8%). Communication services, materials and utilities are between 10% and 12%. Other sectors are below 9%. The fund almost ignores technology (1.9%) and healthcare (0.2%).

LVHI Sector breakdown (chart: author; data: Franklin Templeton.)

The next table lists the top 10 holdings, representing 31.7% of assets. Each of them weighs between 3% and 3.5%, so the fund is well-diversified and risks related to individual companies are moderate.

|

Name |

Weight (%) |

ISIN |

Currency |

Local Ticker |

|

STELLANTIS NV |

3.47 |

NL00150001Q9 |

EUR |

STLAM |

|

BHP GROUP LTD |

3.3 |

AU000000BHP4 |

AUD |

BHP |

|

RIO TINTO PLC |

3.2 |

GB0007188757 |

GBP |

RIO |

|

SOFTBANK CORP |

3.19 |

JP3732000009 |

JPY |

9434 |

|

IBERDROLA SA |

3.17 |

ES0144580Y14 |

EUR |

IBE |

|

PEMBINA PIPELINE CORP |

3.11 |

CA7063271034 |

CAD |

PPL |

|

HOLCIM LTD |

3.09 |

CH0012214059 |

CHF |

HOLN |

|

ZURICH INSURANCE GROUP AG |

3.06 |

CH0011075394 |

CHF |

ZURN |

|

MERCEDES-BENZ GROUP AG |

3.05 |

DE0007100000 |

EUR |

MBG |

|

NATIONAL GRID PLC |

3.03 |

GB00BDR05C01 |

GBP |

NG/ |

Competitors

The next table compares characteristics of LVHI and three hedged international ETFs:

- Deutsche X-trackers MSCI EAFE Hedged Equity ETF (DBEF), reviewed here

- WisdomTree International Hedged Quality Dividend Growth Fund (IHDG)

- iShares Currency Hedged MSCI EAFE ETF (HEFA).

|

LVHI |

DBEF |

IHDG |

HEFA |

|

|

Inception |

7/27/2016 |

6/9/2011 |

5/7/2014 |

1/31/2014 |

|

Expense Ratio |

0.40% |

0.36% |

0.58% |

0.35% |

|

AUM |

$656.46M |

$4.65B |

$2.00B |

$3.81B |

|

Avg Daily Volume |

$4.54M |

$22.16M |

$9.57M |

$18.29M |

|

4 Year Avg Yield |

5.75% |

5.99% |

4.94% |

8.43% |

|

Dividend Frequency |

Quarterly |

Semiannual |

Quarterly |

Semiannual |

|

5 Yr Div. Growth(annualized) |

10.81% |

12.92% |

63.52% |

1.76% |

LVHI is the smallest fund of this group in assets under management and has the lowest liquidity in dollar volume. Yields and dividend growth metrics of all currency-hedged funds must be taken with a grain of salt. Indeed, distributions may include gains from the currency positions depending on management decisions.

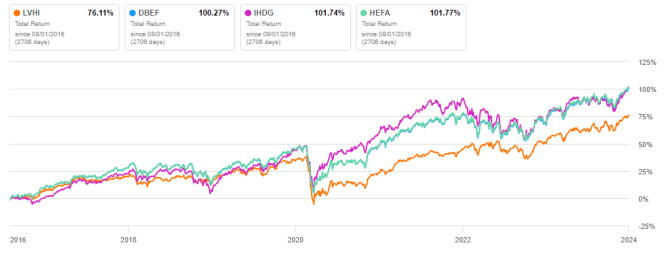

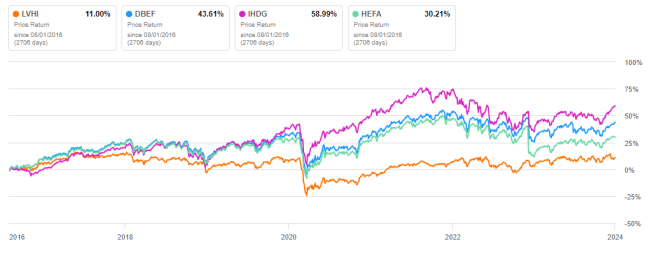

As reported on the next chart, LVHI has underperformed its competitors by a significant margin since its inception.

LVHI vs competitors, total return since 8/1/2016 (Seeking Alpha)

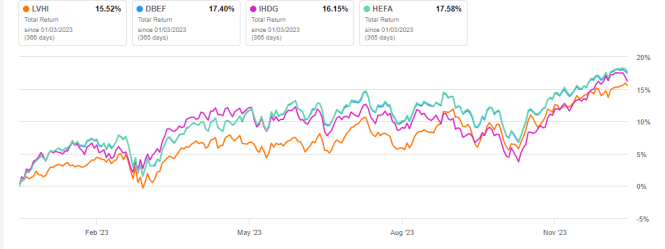

DBEF and HEFA share the same underlying index, which explains why their paths are almost identical. LVHI has also lagged them in the last 12 months:

LVHI vs competitors, 12-month total return (Seeking Alpha)

Since inception, the share price has gone sideways with ups and down, gaining only 11%. The cumulative inflation has been about 27% in the same time (based on CPI), resulting in a significant loss in inflation-adjusted value for shareholders.

LVHI vs competitors, price return since 8/1/2016 (without dividend) (Seeking Alpha)

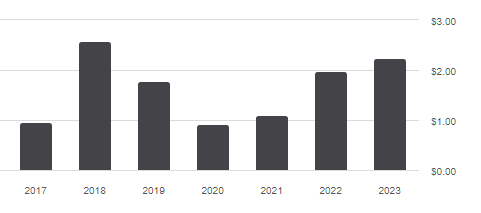

Distributions are impacted by currency rates, and also by gains and losses on currency contracts. It makes them quite variable and unpredictable, which income-oriented investors usually don’t like.

LVHI Distribution history (Seeking Alpha)

Takeaway

Franklin International Low Volatility High Dividend Index ETF is a currency-hedged dividend ETF holding 118 stocks from developed countries, excluding the U.S. The currency hedge is supposed to offset the currency risk for USD-based investors. It aims at projecting the performance measured in local currencies into a performance in dollar. Equity funds with a currency hedge always involve two bullish bets, in a stock strategy and in the USD.

LVHI is well-diversified across countries, sectors and holdings. Nevertheless, the Franklin International Low Volatility High Dividend Index ETF has significantly underperformed other currency-hedged ETFs since inception, and annualized distributions show large variations due to currency rates, which is not very attractive for income-oriented investors.

Be the first to comment