Andriy Onufriyenko/Moment via Getty Images

Investment thesis

I recommend investing in Dynatrace (NYSE:DT). I believe DT is benefiting from the structural change in how businesses operate due to the evolution of technology and digital solutions. It has a product that, I think, addresses this change and also the underlying challenges businesses face during adoption. That aside, the business seems to be executing well on profitability, which I think is a key catalyst to see valuation re-rating back to historical levels.

Business overview

Dynatrace Inc is an IT operations software company that offers software intelligence through application performance monitoring [APM], infrastructure monitoring, logging and AI ops.

As the world becomes more digitalized, software adoption becomes a norm

Companies’ ability to provide a unique experience for their customers relies heavily on the quality of the software they develop. Similarly, software is becoming more and more integrated into the fabric of the business to control mission-critical operations.

The transition from expensive, labor-intensive, and rigid technology infrastructure to more agile, modern cloud-based systems is essential for a successful digital transformation. However, it is extremely difficult to keep track of everything in a large multi-cloud setting. For instance, with conventional tools, IT staff must physically pre-configure separate agents for each part of the application. Given the dynamic and sheer complexity of multi-cloud applications, a multi-agent approach is not feasible due to its high installation and maintenance costs, as well as its inefficiency in the face of frequent changes and updates. In addition, the information these tools provide is limited to specific layers of the technology stack, which is a major drawback of the conventional monitoring methods. Thus, IT teams must physically incorporate and correspond data from different systems, using their own assumptions, in order to determine the root cause of technical problems. Because of the complexity of modern, multi-cloud applications, this procedure is time-consuming, error-prone, and frustrating.

When taken together, I believe these explanations help explain why digital transformations are so sluggish.

Furthermore, businesses are looking for ways to set themselves apart through the quality of their customers’ experiences. A key differentiator is the emphasis placed on digital mediums as the primary means of engagement between businesses and their clientele, business associates, and staff. I believe that the success of businesses’ adoption of digital solutions (e.g., webpage design) is directly related to the quality of their users’ experiences. The business as a whole, not just the IT department, benefits when applications run smoothly and users have positive experiences. In my opinion, the demand for instrumentation that aids businesses in providing high-quality, user-focused outcomes will remain buoyed by the necessity of offering a superior user experience to interact and retain customers.

DT solution is easy to deploy which enables viral adoption

DT is a monitoring platform that is specifically designed to handle cloud and on-premises workloads. It’s designed to work with the most widely used cloud services and has its own artificial intelligence engine to sift through the mountains of data produced by enterprise-level websites. DT’s streamlined deployment and focus on providing an all-encompassing platform mean that customers can quickly adopt the solution and begin leveraging it across a wider range of software applications and environments, or by simply adding new products. DT’s success in this market can be attributed in large part to the company’s ability to provide customers with a solution that is both easy to implement and provide insights from real-time, comprehensive monitoring that improve productivity and decision-making. Organizations can benefit from the platform to better understand and address performance issues. Furthermore, the platform can be tailored to the unique requirements of each business, making it flexible enough to accommodate a wide range of operational settings and procedures.

The data that DT has released backs up my conclusion. During this past few years, DT’s LTM net expansion rate for customers has been over 120%. This is strong evidence that DT’s solution is being used and appreciated by customers, and that they are adopting more solutions overall.

Marketing strategy

DT’s primary sales target is large companies with annual revenues over $750 million. With a proof of concept as the main selling point, the company takes a top-down approach, beginning with the CIO. In addition, DT employs a strategy whereby it begins with a modest rollout and then scales up as usage and customer satisfaction increase, as shown by the company’s rising ARR per customer and exceptionally high retention rate.

In addition to using a sales team, DT has also been successful in the global marketplace by establishing and maintaining strategic partnerships. Perhaps most importantly, the DT platform’s sales reach is expanded thanks to the partner network, which opens the door to additional sales, subscription renewals, upsells, and cross-sells. Cloud service providers, resellers, and system integrators are just a few examples of the types of partners that businesses can work with.

Competition

DT’s main competitor is Cisco AppDynamics, which DT recognizes as the market leader in monitoring solutions and against which DT typically triumphs. My findings suggest that customers choose DT over AppDynamics because DT’s functionality is more robust in the cloud, and it can support any modern, hybrid environment. Even though AppDynamics offers a universal agent, it is typically seen as merely an additional layer of agents on top of the various agents that users must manually deploy to hosts and set up. Furthermore, DT’s victory can be attributed to the fact that it can be implanted quicker, has lower overhead costs, and has AI at the core of its platform.

AppDynamics aside, even though their target markets are different, DT and New Relic (NEWR) occasionally compete against one another. DT caters to enterprises with annual revenues of over $750 million, while NEWR, a cloud-native monitoring solution, has found success in the SMB market and is now expanding into the enterprise sector. However, my belief is that these two companies primary markets are still very different, as such the competition factor from NEWR is not a huge threat so far. To compare, NEWR has disclosed an ARR of over $59.7k per customer, while DT reported an ARR of $267k per customer in 2Q23. Also, for customers who need visibility into their on-premises data centers and hybrid-hosted workloads, the limitations of these NEWR (targeted at SMEs) will become apparent in more complex environments.

Management raised margin guidance

With healthy pipeline generation and win rates continuing through the first half of the year, ARR growth remained at over 30% in 2Q23 earnings. Due to the worsening macro environment caused by the European slowdown, FX headwinds, and extended sales cycles, management has reduced FY23 adjusted ARR growth guidance to 24% from 27% to 28%. Nevertheless, despite a slowdown in top-line growth, EBIT margin guidance was increased by 175 bps to be close to FY22 levels, suggesting a tight budget and operating leverage. DT has a strong margin profile in terms of profitability and free cash flow, and I think this, combined with the company’s recurring revenue model, makes it an excellent defensive software provider. As such, I believe the stock is in good shape to weather the storm because of the de-risked FY23 guidance and reset in expectations surrounding their growth algorithm.

Valuation

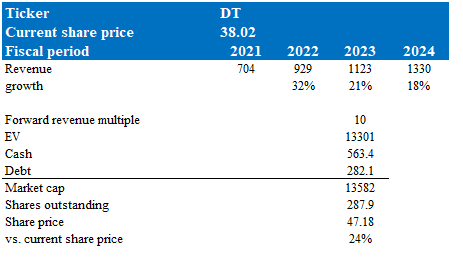

My model suggests DT is worth $47.18, if it trades at 10x forward revenue multiple in FY23.

Model walkthrough:

- Revenue to follow management full year guidance in FY23. Afterwards, I expect revenue to continue growing at a similar pace but slightly lower due to a weaker macro environment and FX impact.

- My variant view is that DT valuation is likely to improve from here as DT continues to improve its margin profile (as guided). Given that investors are now expecting software companies to turn profitable and generate FCF, I think this could be a catalyst for valuation re-rating.

Own calculations

Risk

Biggest risk is competitive dynamics

I do not think there are any constants in the software industry. This is also true in the current DT business environment. Even though DT is closing deals and outcompeting established rivals (AppDynamics), its continued dominance in the market cannot be assumed. In my opinion, there is a significant threat to DT performance forecasts and share price if Dynatrace is unable to maintain its current rate of new customer additions and product innovation.

Conclusion

I think DT is reaping the rewards of the fundamental shift in business operations brought about by the development of technology and digital solutions. It offers a solution that helps businesses deal with the transition and the problems they encounter in the process of adopting the new system. In addition, the company appears to be on track to hit its margin guidance, which is, in my opinion, a necessary condition for a re-rating of the stock price to its prior levels.

Be the first to comment