claudio.arnese/iStock Unreleased via Getty Images

Yesterday, Autogrill (OTCPK:ATGSF; OTCPK:ATGSY) reported its 8-month numbers, confirming the 2022 positive trajectory trend. Given the recent green light from the Dufry (OTCPK:DUFRY) General Meeting that we recently commented on, the merger combination (still subject to Antitrust authority & regulators’ go-ahead) between the two companies is expected to closed in Q2 2023, so it is key to overview Autogrill’s performance quarter-on-quarter and assess the main financial implication.

Autogrill results

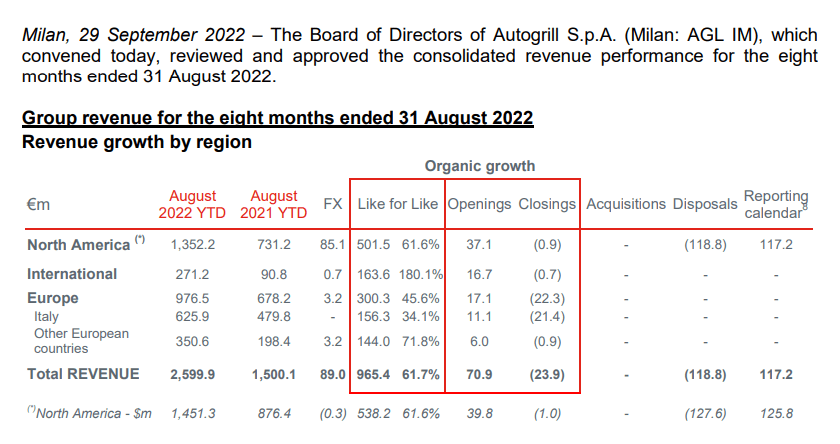

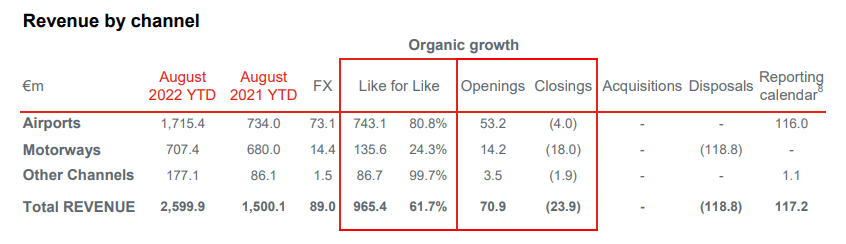

Numbers in hand, during the first eight months, the Italian giant achieved €2.6 billion in revenues (Fig. 1), up 63.6% at constant exchange rates compared to the same period last year, and beyond Wall Street consensus estimates that were forecasted on average €2.5 billion. Looking at the details, top-line sales were supported by the travel catering accounts thanks to international air travel recovery and domestic resilience of US airports and European highways (Fig. 2). To sum up and cross-check the financials versus the pre-COVID-19 results, Autogrill’s turnover represents approximately 87% of 2019 figures.

Autogrill revenue for the eight months ended 31 August 2022

Source: Autogrill Results (Fig 1)

Autogrill revenue by channel

Source: Autogrill Results (Fig 2)

Going down to the P&L analysis, operating profit was equal to €112 million, while a year ago it was still negative at 28 million. As stated in the just-released note, the clear improvement was due to 1) the company’s operating leverage, 2) price management actions and 3) better product mix optimization. This is pretty in line with Dufry’s initiation of coverage in which we explained how they achieved structural cost savings. The pandemic outbreak was a shock for the whole sector, but we are confident that operating leverage and better margins still need to be priced in by the market. This is also true for FCF generation which reached €232 million, of which €128 million were generated in the months of July and August alone.

In light of the solid financial results and considering the business seasonality, Autogrill Group confirmed the 2022 outlook on expected top-line sales, equal to approximately €3.8 billion, slightly below consensus expectation set at €3.9 billion, and on FCF expected to be around €200 million, maintaining its 2024 guidance unchanged.

Conclusion

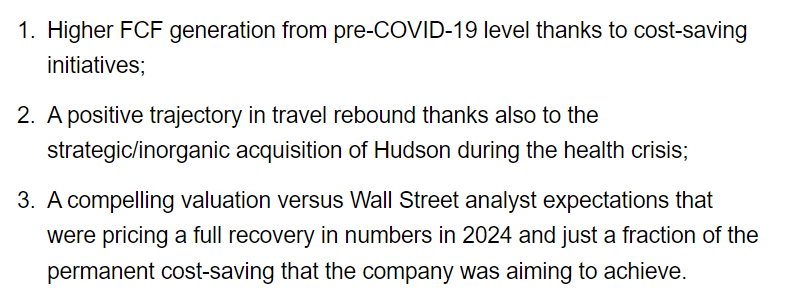

Mare Evidence Lab’s buy case recap was based on the following:

Dufry Is Still Trading At A Depressed Valuation

Source: Mare Evidence Lab’s previous publication

A few weeks ago, Dufry released its 2027 plan, yesterday Autogrill also confirmed its 2024 target. Despite the positive results, the company is still trading at a depressed valuation so we do not add anything more. The buy rating is confirmed. Another interesting company that we advise you to check is Expedia – Q2 2019 Vs. Q2 2022 – Something Doesn’t Add Up.

Be the first to comment