Anna Moneymaker/Getty Images News

By Robert Eisenbeis, Ph.D.

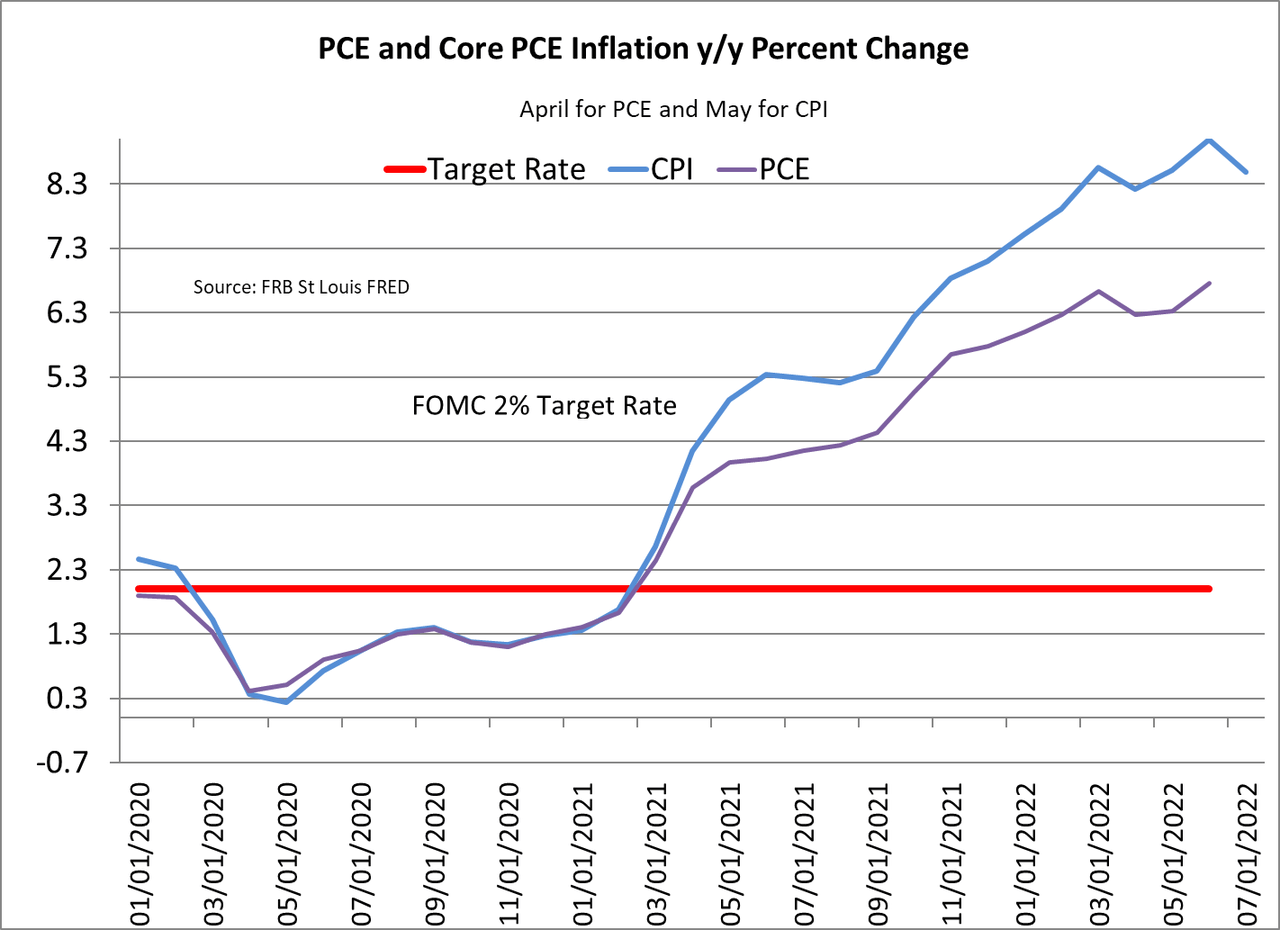

The rally in financial markets the past few weeks was rooted in the widely publicized beliefs that inflation had peaked and that the Fed would, in response, start cutting rates next year as inflation declined. That belief was probably as misguided as the Fed’s belief that the acceleration of inflation in mid-2021 was only “transitory.” As the chart below shows, the FOMC’s preferred PCE inflation index was up to 6.8% y/y in June from 6.3% y/y in May. At the same time, the CPI showed a slight dip in July to 8.5% from 9.0% in June. Given the lag in the PCE, part of the belief that the PCE will show a dip when it becomes available for July and will continue to decline in August is due in part because gasoline costs have declined significantly for the past seven or eight weeks. Gas prices are now well below $4 per gallon in many parts of the country.

But markets reversed course last Wednesday when the FOMC minutes were released and were further jolted by the support that FOMC voting member James Bullard, President of the Federal Reserve Bank of St. Louis, voiced for another large rate increase at the Committee’s next meeting.

The FOMC minutes contained several important pieces of information that provided clues as to what the appropriate stance for policy is in the Committee’s view. First, the staff forecast for GDP growth was reduced to below what was seen as “potential” for the second half of the year, and the unemployment rate was also projected to increase. PCE inflation was projected to be 4.8% for the year, which implies a significant slowdown in inflation during the second half of 2022. If the CPI for July is any indication, however, that forecast for PCE is likely to be overly optimistic.

Second, in contrast, the views of participants were not quite as optimistic on the inflation front. Indeed, the minutes indicate that participants agreed that there was little evidence that inflation pressures were subsiding and, because of the lags between policy tightening and its impact on inflation, the pressure on prices would remain “uncomfortably high for some time” and might even increase in the short run as a result of recent increases in residential property rents.

Third, the Committee noted the importance of inflation expectations in its policy framework and observed that they remain well anchored. They saw policy firming as critical to ensuring that expectations do not become unanchored. Furthermore, the Committee foresaw further increases in the policy rate in order to achieve its inflation objective. At the same time, the Committee abandoned its forward guidance on policy and will focus instead on incoming data and “implications of incoming information for the economic outlook and risks to that outlook.” The message seems to be clear that further policy tightening is on the horizon and is appropriate from a risk management perspective.

On Thursday, a day after the FOMC meeting, the market’s view of the likely path of policy took a further hit from President Bullard. Not only was he not convinced that inflation had peaked, but he pointed to the fact that he saw the policy rate range by year-end at 3.75%-4% and noted that other participants had the policy rate at over 4% in 2023. That is certainly not consistent with the view that the FOMC is likely to take its foot off the tightening cycle for a while. Bullard said that, at this point, he would favor another 75-basis point hike in the policy rate range. He also expressed the view that under his policy rate scenario, it would take about 18 months to get inflation down to the policy target.

The combination of the minutes and Bullard’s statement of his views on the appropriate path for policy caused market participants to abruptly recalibrate their optimism and resulted in two down market days to close out the week and continued into this week. The lesson here is that it is risky to try to second-guess or fight the Fed.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment