Pgiam/iStock via Getty Images

Almost two years ago, I recommended avoiding Ecolab (NYSE:ECL) due to its rich valuation back then. I specifically mentioned that the stock would probably incur a harsh landing if the 10-year Treasury yield kept rising. This is exactly what has happened to the stock. Since my article, the stock has plunged 33% due to the impact of excessive inflation on the profit margin of the company and on the valuation of the stock. However, thanks to the aggressive policy of the Fed, inflation is likely to subside in the upcoming years and thus the stock of Ecolab will probably retrieve most of its losses. Therefore, the investors who can maintain a long-term perspective are likely to be highly rewarded by Ecolab, though they should be aware that it may take years for the stock to retrieve its losses.

Business overview

Ecolab is the global leader in water, hygiene, and energy technologies and services. The company operates in three major divisions: Global Industrial, Global Institutional, and Global Energy. The former offers water treatment and process applications to companies in the food & beverage, manufacturing and chemical industries while the Global Institutional division offers solutions and services to restaurants, hotels, hospitals and retailers. The Global Energy division offers solutions to customers in the oil industry.

Thanks to its continuous expansion and the essential nature of its technologies and services, Ecolab has proved resilient to recessions. In the Great Recession, while most companies saw their earnings collapse, Ecolab kept growing its earnings per share as if there was no crisis. The company grew its earnings per share by 20% between 2007 and 2009.

Unfortunately, Ecolab is currently facing a much fiercer downturn right now due to the surge of inflation to a nearly 40-year high. The surge of inflation has greatly increased the costs of the products of the company and thus its profit margin has come under great pressure.

The impact of inflation was evident in the results of Ecolab in the third quarter. The company grew its organic sales 13% over the prior year’s quarter, primarily thanks to the implementation of material price hikes. However, its earnings per share decreased 6% due to excessive cost inflation. In other words, the strong price hikes implemented by Ecolab proved insufficient to offset high cost inflation. Even worse, management hinted that it will probably take longer than previously anticipated to recover from the highly inflationary environment prevailing right now. Due to the disappointing earnings report and conference call, the stock slumped 9% after the earnings release.

Despite the adverse current business landscape, Ecolab is likely to recover in the upcoming years. Central banks are raising interest rates aggressively in order to restore inflation to its normal range. Their efforts have already begun to bear fruit, as inflation has moderated off its peak last summer. Given the determination of central banks, one can reasonably expect inflation to continue to subside in the upcoming quarters. In such a case, Ecolab is likely to greatly benefit from lower costs and thus return to its long-term growth trajectory.

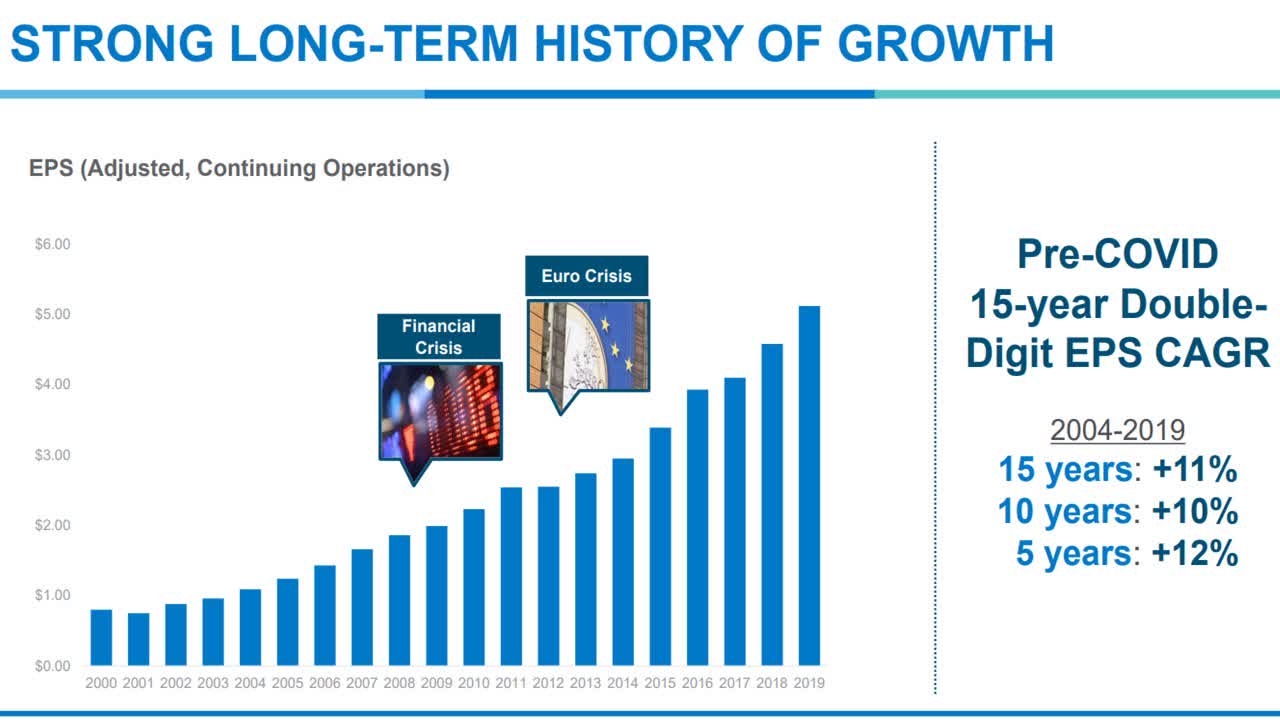

Ecolab has exhibited an impressive performance record, with admirable consistency for decades. The company grew its earnings per share every single year between 2004 and 2009, at an 11% average annual rate.

Ecolab Growth (Investor Presentation)

A consistent growth record is one of the most important features investors should look for. The exceptional growth record of Ecolab is a testament to the strength of its business model and its exemplary execution.

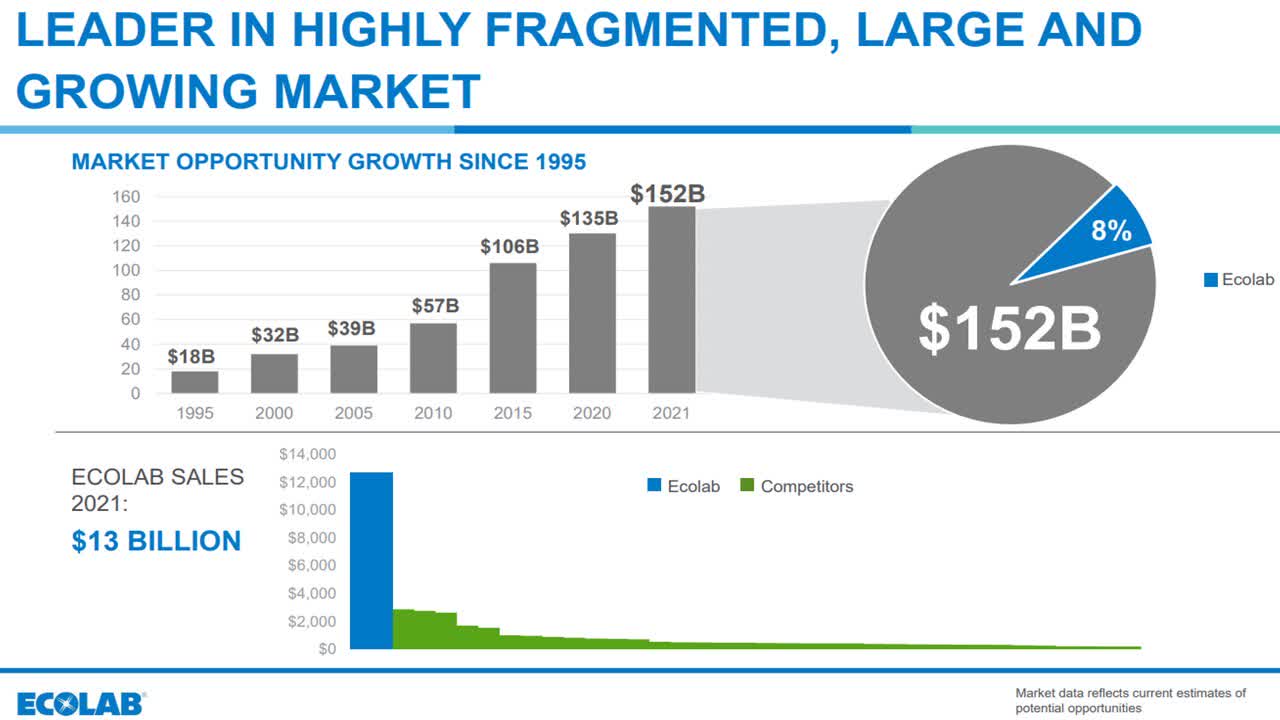

Even better, Ecolab has ample room for future growth. It is a global leader in its business but it has a market share of only 8% in a total addressable market of $152 billion.

Ecolab’s Growing Addressable Market (Investor Presentation)

Thanks to the high fragmentation of its market, Ecolab can continue growing its sales and its earnings significantly by gaining market share from smaller, less efficient companies. Ecolab has also grown by acquiring smaller competitors and incorporating their products in its immense global network.

It is also important to note that the total addressable market of Ecolab has been growing relentlessly. To provide a perspective, as shown in the above chart, the total market has grown 43% since 2015. A fast-growing total addressable market and an expansion of market share are likely to help Ecolab return to its high-growth trajectory sooner or later.

Moreover, Ecolab is currently doing its best to mitigate the effect of high cost inflation. To this end, it has accelerated its price hikes to 12% and is making great efforts on enhancing efficiencies and reducing operating costs. Thanks to its efforts and the strength of its business model, Ecolab expects to soon return to its long-term growth trajectory. Management has provided guidance for 6%-8% annual growth of sales and 15% annual growth of earnings per share in the long run.

Analysts seem to agree on the promising growth prospects of Ecolab. They expect the company to grow its earnings per share at a double-digit annual rate over the next five years, from $4.46 in 2022 to $9.39 in 2026 and $10.51 in 2027. Given the reliable growth trajectory of Ecolab and its exemplary management, analysts are likely to prove correct in their growth expectations.

Valuation – expected return

Thanks to its exceptional growth record, Ecolab has almost always traded with a remarkably premium valuation. To be sure, the stock has traded at an average price-to-earnings ratio of 30.8 over the last decade.

Based on its expected earnings per share of $4.46 for 2022, Ecolab is currently trading at a price-to-earnings ratio of 33.4. It thus seems fully valued on the surface. However, it is important to realize that the company is expected by analysts to recover strongly in the upcoming years. If it meets the aforementioned estimates of analysts, it will earn $9.39 per share in 2026.

In order to be on the safe side, it is prudent to assume a price-to-earnings ratio of about 25 in that year. Such an earnings multiple will be much lower than the 10-year average of 30.8 of the stock but it is prudent to have a significant margin of safety. If Ecolab meets the analysts’ estimates and trades at a price-to-earnings ratio of 25 by 2026, it will trade at $235 in that year. This means that the stock has 58% upside potential over the next four years. Even if Ecolab achieves these earnings one year later than currently expected, it will still offer excessive annual returns to its shareholders.

Risk

The primary risk for Ecolab is the adverse scenario of persistently high inflation for years. In such a case, the company will continue to be hurt by high cost inflation and thus its recovery will take much longer than expected to materialize. However, due to the impact of inflation on the purchasing power of households, the Fed has prioritized restoring inflation close to 2%. Thanks to its aggressive interest rate hikes, the central bank is likely to achieve its goal in 2023 or 2024.

Final thoughts

Ecolab is an exceptional company, with an impressive performance record. The stock has always traded with an excessive premium and thus it has been especially hard for investors to identify an attractive entry point. The current downturn offers a unique opportunity to buy this stock at a reasonable price. Those who purchase the stock with a long-term horizon are likely to be highly rewarded.

Be the first to comment