JamesBrey

Financial independence is often defined as generating enough passive income to be able to cover all of your living expenses (with ideally a bit extra on top to account for contingencies and potential future reductions in your passive income stream). As a result, you no longer have to work in order to support your lifestyle and can instead enjoy the independence to do whatever you want with your life.

While dividend growth investing is a popular path to get there, the downside of it is that stocks that grow their dividends by meaningful amounts year after year often offer low starting yields. This means that – unless you are already a multi-millionaire or have a massive income – it will take quite a bit of time to amass a big enough passive income stream to become financially independent.

As a result, many dividend investors pursuing the path to financial independence are enticed by the allure of high yielding stocks as they see their potential as short cuts to turbocharge their path to financial independence.

This chart that was recently published by my friend and colleague Austin Rogers illustrates this point clearly:

| Starting Dividend Yield | Dividend Growth Rate | 10-Year YoC |

| 3% | 9% | 7.1% |

| 3.25% | 8% | 7.0% |

| 3.5% | 7.25% | 7.0% |

| 3.75% | 6.5% | 7.0% |

| 4% | 5.75% | 7.0% |

| 4.5% | 4.5% | 7.0% |

| 5% | 3.5% | 7.1% |

| 5.5% | 2.5% | 7.0% |

| 6% | 1.5% | 7.0% |

For example, if you buy a high quality Dividend King like Procter & Gamble (PG) that offers a forward dividend yield of 2.5% and is growing it at ~9% CAGR, it will take ten years for the yield on cost to equal the ~5.9% dividend yield that is currently being offered by ultra-slow growth AT&T (T). And of course, if you reinvest the surplus dividends that T generates relative to PG, this math becomes even more daunting and the timeline gets pushed out significantly for PG’s yield on cost to match T’s true yield on cost. This makes the math behind the dividend growth strategy not look quite as appealing as it may have at first glance.

While high yield investing certainly has its perks for turbocharging the pursuit of an early retirement, or at the very least financial independence, it is not a risk-free approach either. In fact, high yield also often equates to high risk, though not always. Many times when a stock offers a sky-high yield it means either that its growth prospects are very weak (such as in the case of T), its dividend is about to be cut, and/or its underlying business model’s ongoing viability and/or financial sovereignty is in danger. An example of a stock that recently went from offering a double-digit dividend yield that was supposedly fully covered by free cash flow to completely eliminating its dividend is Lumen Technologies (LUMN). The company was trying to pivot to topline growth, but its investments were failing to deliver the desired results and its existing businesses were suffering from consistently eroding results. Meanwhile, its debt was junk-rated and its balance sheet was overleveraged, so management decided to eliminate the dividend in order to double down on growth investments and try to save the company.

In this article, we look at two other high yields that may not survive 2022, while also providing two that we think investors can rely on even through a likely recession this year.

Risky Dividend #1: Algonquin Power & Utilities (AQN)

Regulated utility and renewable power generator AQN has been one of our biggest losers at High Yield Investor as it suffered a massive decline in its share price in the closing months of 2022 in the wake of very disappointing Q3 results and forward guidance. Furthermore, management signaled that it would be revisiting its ambitious capital allocation plan and announce its new targets at its upcoming Investor Update Call on January 12th at 8 am Eastern Time. This uncertainty – including valid concerns about the viability of the current dividend level moving forward – combined with the poor results and guidance, causing the stock price to drop like a rock.

We think there is a 50% chance that management announces a dividend cut sometime this year and quite possibly at this Investor Day. As a result, we are downgrading our Dividend Safety rating from B- to C+. The reasons for this slightly downgraded outlook for the dividend are:

1. The Federal Reserve reiterated its hawkish intent for interest rates for the short-term and recent jobs data indicates that there is not yet sufficient reason for them to change course on raising interest rates. While we think this may change by mid-year and that the Fed could very well be cutting interest rates already by the end of this year or in early 2024 at the latest, this hawkish short-term outlook could force AQN’s hand towards erring on the side of conservatism and cutting the dividend to shore up its investment grade credit rating. This is especially true since the company does have meaningful floating debt exposure, so higher interest rates for longer will sap the company’s cash flow and limit its ability to pay its dividend, meet its funding needs, and deleverage its balance sheet simultaneously.

2. We also think a dividend cut could transpire here in Q1 already because of the FERC’s recent decision to disapprove AQN’s planned acquisition of Kentucky Power. This means that at a minimum, AQN will not be acquiring Kentucky Power when it originally thought it would (in Q1 2023), and therefore its previous estimated growth timeline is going to have to be revised downward. At a minimum, this development hurts the long-term growth outlook for AQN, though it does potentially reduce stress on the balance sheet in the near-term since AQN will not have to fork over as much cash to acquire Kentucky Power in the near future, assume its sizable floating rate debt burden, and then also fund the proposed capital budget for the growth plan pertaining to that business (estimated to be ~$4 billion over the span of four years).

However, the bigger issue here is whether or not this deal will close at all. If AQN winds up closing this deal later this year sometime, we think AQN will almost certainly cut its dividend because it will need to keep its liquidity up to fund the acquisition later on this year (i.e., an elevated share count and floating rate debt level) and also may suffer from lower growth from the deal than initially anticipated (as well as delayed accretion from the deal since it will be closing at a later date than originally anticipated). It also means that their leverage ratio will be even more elevated in 2023 than originally anticipated, putting even greater pressure on the business to cut its dividend (likely between 25% and 50% in our view) in order to save its investment grade credit rating.

For more in-depth valuation and preview analysis on the upcoming Investor Day, click here.

Risky Dividend #2: Medical Properties Trust (MPW)

MPW is a REIT that owns for-profit hospitals. Like AQN, it offers a high yield and boasts an attractive track record of growing its dividend per share while generating alpha for shareholders. However, over the past year its share price has gotten pummeled over growing concerns about the financial viability of some of its largest tenants, including Steward.

There have been some pretty viscous short attacks against this stock this year as well, emphasizing a wide range of issues with the company, including management wasting money on corporate jets as well as MPW lending money to Steward in order to help them pay rent. The fear is that eventually it will become obvious to everyone that the emperor has no clothes and that Steward will have to file for bankruptcy and its leases with MPW will either be terminated altogether or at the very least renegotiated in a manner that may force MPW to slash its dividend payout.

While there are also reasons to not believe the shorts, including:

- MPW just raised its dividend last year; if it was really in trouble, management probably would not have raised it like they did

- MPW’s hospitals are mission critical and generally very profitable at the asset level, so even if Steward and/or other tenants go into default, it has a good chance of getting new tenants fairly quickly on attractive terms for MPW

- Management has an impressive track record of managing distressed tenant situations well

It is also a very speculative high yield investment because Steward has not provided in-depth financial disclosure to the public. As a result, it is impossible for us to know whether or not MPW’s dividend is ultimately sustainable or not. Investors who buy MPW right now could be in for massive profits, but they also could be buying a highly risky yield trap.

Safe Dividend #1: Energy Transfer (ET)

ET boasts arguably the best distribution coverage ratio for any common equity with a double-digit projected forward yield. Based on its current distribution growth trajectory and management’s stated capital allocation priorities, we believe it is quite likely that ET will pay out a $1.22 distribution per unit this year, bringing the forward yield to ~10%. Based on consensus analyst estimates for 2023 distributable cash flow per unit, this payout will be covered 2.2x.

When combined with continued significant deleveraging of its investment grade rated balance sheet and relatively stable cash flowing energy midstream business model throughout business cycles and macroeconomic conditions, ET looks like a very attractive distribution that investors can sleep well at night knowing that it will continue to pour in for them through thick and thin.

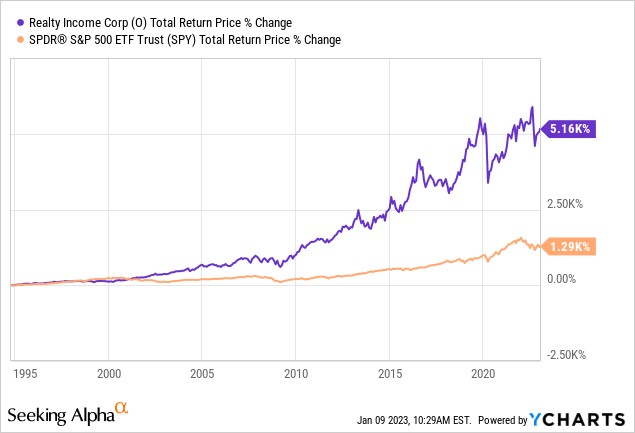

Safe Dividend #2: Realty Income (O)

O is a true sleep well at night stock given that it pays out monthly dividends and is backed by an A- credit rating, excellent management, a broadly diversified low-risk triple net lease business model that includes a large number of investment grade tenants.

Moreover, its payout ratio is quite reasonable and the company’s history of growing its FFO per share in 25 of its past 26 years and growing its dividend for 26 straight years (making it a Dividend Aristocrat) make it a dividend growth stock that you can count on. However, instead of offering a measly 2-3% like many Dividend Aristocrats and Dividend Kings today, O offers investors a juicy 4.8% dividend yield that can help people focusing on retirement income cheat a bit on the 4% Rule.

Its long-term track record of crushing the broader market’s performance also indicates the superiority of management and the business model:

Investor Takeaway

High yield investing is a powerful method for accelerating your progress towards financial independence. However, it can also be a treacherous road if you invest carelessly and do not carefully examine each investment prior to pouring your hard-earned capital into it. Despite spending tens of thousands of hours and dollars at High Yield Investor on this pursuit, we still make our share of mistakes, including buying half of our current AQN position prior to its recent stock price crash, leaving us with a weighted average share price of ~$10.

That said, we have overall won a lot more than we have lost, enabling us to beat the S&P 500 (SPY) and high yield space (DIV) significantly since the inception of our portfolio over two years ago.

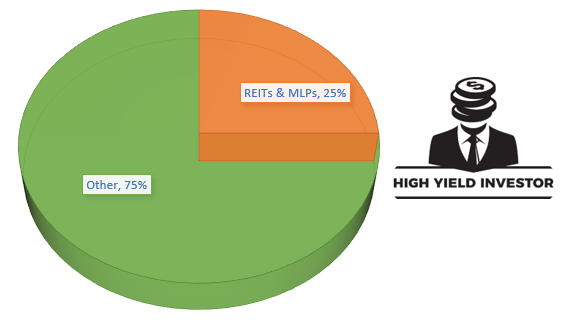

Moving forward, we think that investment grade REITs (VNQ) (especially triple net lease REITs) and investment grade midstream businesses (AMLP) are some of the best places to invest right now because they offer:

- high, sustainable yields that you sleep well at night holding

- defensive business models

- strong balance sheets

- attractive valuations

- protections from e-commerce and energy transition disruption

As a result, ET is one of our largest positions at High Yield Investor and we hold several similar positions to ET and O, bringing our overall allocation to REITs and MLPs to roughly one-quarter of our portfolio:

HYI Portfolio

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment