MJ_Prototype

Investment Thesis

Digital Turbine (NASDAQ:APPS) reports fiscal Q3 2023 results that left much to be desired. Indeed, this is a forgiving way to describe these results.

It turns out that I made a horrible call to be bullish on this company’s prospects. I honestly believed that sentiment was negative enough that I could make a contrarian call on APPS. However, this was a wrong assessment. Painfully wrong.

While it cuts me up to admit I made a mistake with this previous investment analysis, I will not compound my mistake by failing to read the writing on the wall now.

Please note, before we go further, Digital Turbine is reporting fiscal Q3 2023 results (not calendar results).

End of the Road?

Digital Turbine was a high-flying company at one point. This saw it gain a considerable following amongst investors. However, after its massive acquisition binge of 2021, the comparables have come back to harm the company.

Right now, as we eye up 2023, it’s not just the comparables that are a headwind to the company. But also, the macro environment could not be more restrictive.

The time when customers were happily willing to pay for Digital Turbine’s customer acquisition platform has now rapidly rescinded.

So, left for shareholders? Is this now the end of the road?

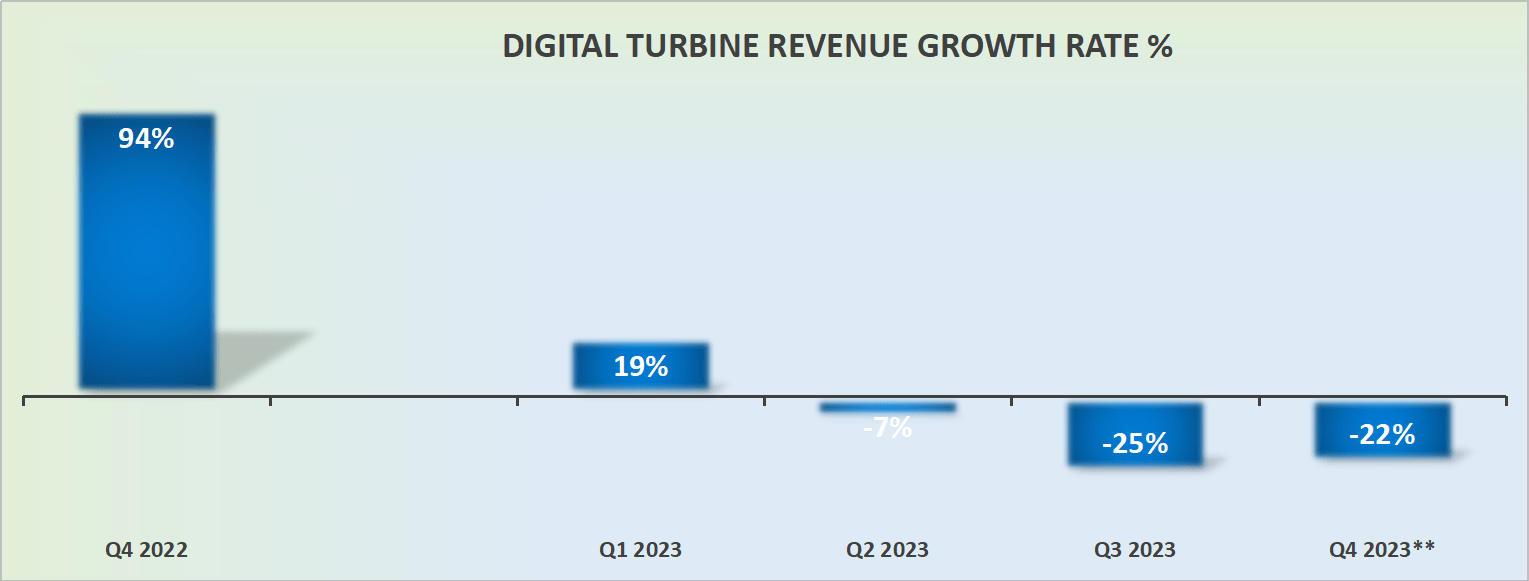

Revenue Growth Rates Turn Considerably Negative

APPS revenue growth rates

Digital Turbine’s fiscal Q4 2023 guidance points to negative 22% y/y growth rates. In other words, Digital Turbine’s revenue guidance for fiscal Q4 2023 points to approximately $144 million, which compares with analysts’ expectations of $174 million.

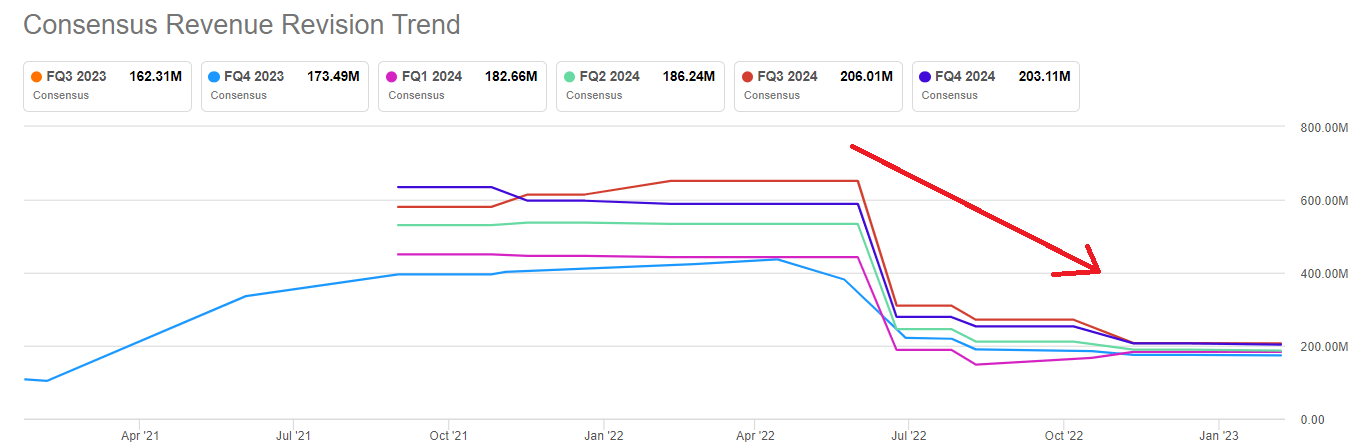

Put another way, although analysts’ expectations had been moving steadily lower over the preceding months, it turns out that expectations were still too high.

SA premium

Naturally, this forces the unpleasant question. What sort of growth rates can investors expect from Digital Turbine?

Personally, I find it difficult to expect anything above 3% CAGR in the near term. However, keep in mind that this is substantially lower than what analysts believe is possible. More specifically, analysts expected Digital Turbine’s CAGR rates to reach 10% in the coming year, fiscal 2024.

That being said, given how badly analysts estimated Digital Turbine’s fiscal Q4 2023 guidance, I believe that in the coming hours and days, we’ll all be reading plenty of analysts’ downgrades.

So, What Happened?

This is what Digital Turbine’s CEO Bill Stone stated on the call:

Our outlook for the long term remains unchanged, but I know many investors are short-term focused, but we’re confident in our future and confident in the investments we’re making to drive long-term value for Digital Turbine

Essentially, according to Stone, the problems with Digital Turbine are temporary.

Nonetheless, this doesn’t detract from the fact that what was once viewed as Digital Turbine’s crown jewel, its SingleTap product, now does not appear to be gaining as much traction. Partially due to some competitors seeking out some market share from this opportunity. But also due to the overall software environment.

Stone went on to say on the call:

What we’re seeing right now on pricing on the ad tech side is that’s the major driver more so than volumes. Volumes were relatively flat from quarter-over-quarter.

So the pricing I referenced in my remarks, 10% to 20% is across the board regardless of ad type or pretty much regardless of geography, whether that’s banners, interstitials, videos or what have you.

So, it’s primarily a pricing story on the demand side

Basically, this is the takeaway, for now, Digital Turbine is completely susceptible to weakness in the advertising sector. The customers that are advertising in this environment would much rather deploy their spending towards bigger platforms with ”more certain” ROI metrics, rather than towards smaller players, such as Digital Turbine.

APPS Stock Valuation — Cheap Can Always Get Cheaper

Digital Turbine guides for fiscal 2023 to see approximately $170 million of EBITDA. Given that for the trailing 9 months of fiscal 2023, Digital Turbine already reported approximately $137 million of EBITDA, this means that fiscal Q4 2023 will see less than $40 million of EBITDA.

Put another way, Digital Turbine’s bottom-line profitability for the quarter ahead will be down close to 30% y/y compared with the $50 million reported in the prior year’s quarter.

Accordingly, for investors, it’s difficult to pay a premium for a company that is as cyclical as Digital Turbine.

So, even if the stock appears cheaply priced at roughly 10x EBITDA, it’s only cheap if one can make a high-conviction argument that Digital Turbine’s EBITDA prospects can sustainably grow over the next several years. And at the moment, Digital Turbine’s profitability profile appears to be moving in the opposite direction.

The Bottom Line

I very much want to cheer for the underdog. But I’ve come to realize that the ”whispers” were right. 2023 is a stock pickers market.

Just because the tide lifted all boats in 2020, the same cannot be said right now.

The market is incredibly discerning and only willing to back the adtech companies that are well-positioned to thrive in this environment. And the market will rapidly and ruthlessly discard second-tier adtech companies. Whatever you decide, good luck and all the best.

Be the first to comment