TERADAT SANTIVIVUT

Article Thesis

Devon Energy (NYSE:DVN) will report its next quarterly earnings results on Monday, February 13. We will take a look at what investors can expect in terms of profits, cash flows, and revenue, and we’ll delve into the outlook for Devon Energy going forward.

Upcoming Earnings: Will Devon Energy Beat Estimates Again?

When a company announces its quarterly results, there are several important factors investors should consider. These can be grouped in the following areas:

– How did the company perform in absolute terms? I.e. how was its revenue, cash flow, shareholder payouts, etc.

– How did the company perform relative to estimates? If a company saw its profit grow, but less than expected, the market reaction can easily be negative. Likewise, if profits decline, but not as much as feared, the market reaction can be positive.

– What does management’s guidance look like? Is management’s commentary about the near-term and/or longer-term outlook positive?

In Devon Energy’s case, it is pretty likely that the company will perform well when it comes to the first of these areas. In absolute numbers, results should be strong: Oil prices were considerably higher in Q4 of 2022 versus the fourth quarter of the previous year, thus the macro environment was beneficial for Devon Energy. When it comes to earnings per share growth, an improvement versus the previous year’s quarter is even more likely, as the company will benefit from two growth drivers — it has reduced its debt position, which translates into lower interest expenses, and it has bought back some shares, which increases each remaining share’s portion of the overall net profit.

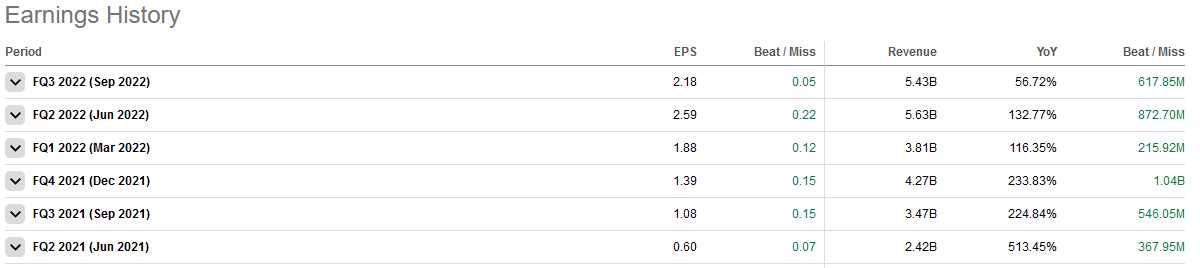

When it comes to the performance versus what analysts are predicting, the outlook still is positive, I believe — mainly due to the fact that Wall Street has a history of underestimating Devon Energy:

Seeking Alpha

For the last six quarters, Devon Energy has beaten estimates on both lines — which is a very strong track record. When one looks at all companies on the market, earnings beats are somewhat more likely than earnings misses, but a perfect 12 out of 12 is pretty rare. In other words, it is pretty rare for Wall Street to underestimate a company so consistently. The average earnings per share beat that Devon Energy has delivered over the last six quarters was $0.13, or around 7%. Revenue beats have been pretty strong as well, north of 10%, on average. I thus believe that there is a good chance that Wall Street analysts have done what they have a history of doing — underestimating Devon Energy. An earnings and revenue beat thus seems more likely than a miss, although there is no guarantee, of course.

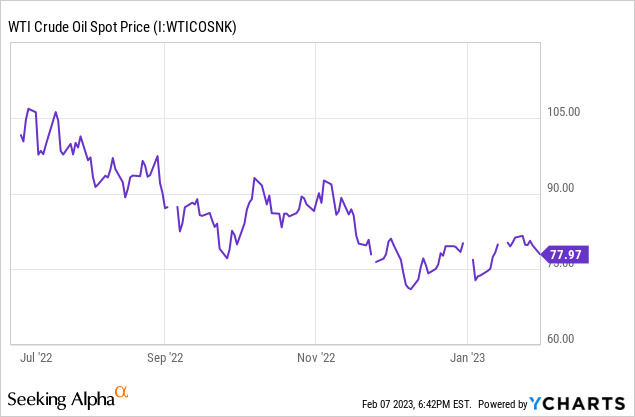

Looking at estimates for the quarter, analysts are predicting earnings per share of $1.76 on the back of a $4.35 top line result. That represents a decline versus Q3, which is not surprising, as oil prices declined from Q3 to Q4, looking at the average for each quarter:

We see that WTI traded between $80 and $105 in Q3, whereas the trading range for Q4 was $75 to $95 or so. On average, price realizations thus most likely were lower during the fourth quarter. Due to hedging, timing, etc. it is not possible to forecast what the impact looked like exactly, but a 15% decline or so seems very much possible. On the other hand, analysts are forecasting a revenue decline of 20%, which could be a little aggressive — which would fit with analysts’ history of being too bearish when it comes to estimating Devon Energy’s sales and profits.

When it comes to free cash flows, which are important for investors as they decide about a company’s potential when it comes to dividends, buybacks, and debt reduction, investors should expect a decline versus the previous quarter. That will stem from two factors. First, lower earnings result in lower cash flows, all else equal. With Q4 likely being less profitable versus Q3, a cash flow from operations decline would thus not be surprising. On top of that, Devon Energy has guided for higher capital expenditures during the fourth quarter. Since capital expenditures are subtracted from operating cash flows in order to get to free cash flows, higher capital expenditures result in lower free cash flows, all else equal.

With capital expenditures rising to almost $900 million for Q4, per management’s guidance, up by close to $300 million quarter to quarter, while operating cash flows could decline by $200 million or so, I believe that $1 billion could be a realistic free cash flow estimate for the fourth quarter, down from $1.5 billion in Q3. Note that working capital movements could substantially influence that number to the upside and downside, however. While a $1 billion free cash flow result, versus $1.5 billion during the previous quarter, would represent a significant decline, it would be far from a disaster — since Devon Energy is valued at $39 billion today, a $1 billion free cash flow per quarter level would still make for a free cash flow yield of slightly above 10%. This is, I believe, pretty attractive.

Devon Energy has a history of offering sizeable dividend payments, at least in the recent past. The dividend for the last two quarters was $1.55 per share and $1.35 per share, or $2.90 in total ($5.80 per year if the dividend would be kept at the average level over those two quarters). Dividends for the fourth quarter will most likely be lower, however, due to the expected earnings and cash flow decline. But even if Devon Energy were to cut its dividend by 26%, which would bring the payout down to $1.00, the forward dividend yield would be quite sizeable, at 6.5%. It’s also possible that Devon Energy will opt for a smaller dividend reduction. If the payout is reduced to $1.15 per share, which would make for a $0.20 reduction, comparable to what Devon did between Q2 and Q3, the implied dividend yield would be 7.4%, which would still represent a pretty sizeable dividend yield. Relative to estimated earnings per share of $1.76, a $1.15 dividend wouldn’t be unreasonably high — after all, Devon Energy has a pretty clean balance sheet already (with a net debt to EBITDA ratio of around 0.5), thus a dividend payout ratio in the 60s seems sustainable.

What Can Investors Expect In The Longer Run?

Oil prices have recently come under pressure due to recession worries, but they are still at a very solid level where many oil companies, including Devon Energy, are highly profitable. And oil prices might start to climb again, due to several potential catalysts. China’s economic reopening should drive global oil demand upwards, while sanctions on Russia’s oil industry could result in output declines, as the country does not receive technology, parts, etc. from the West that could be needed to keep assets running smoothly. Supply from the US SPR has ended as well, and if the SPR is to be filled up again, that would result in additional demand. There are thus reasons to believe that oil prices could be higher half a year, a year, or a couple of years from now, relative to today — although a deeper-than-expected recession could lead to lower oil prices as well. Overall, I’m moderately bullish on oil prices, and DVN is one of the companies that would benefit. With a clean balance sheet investors can expect that shareholder returns will remain at an attractive level, mainly via dividends.

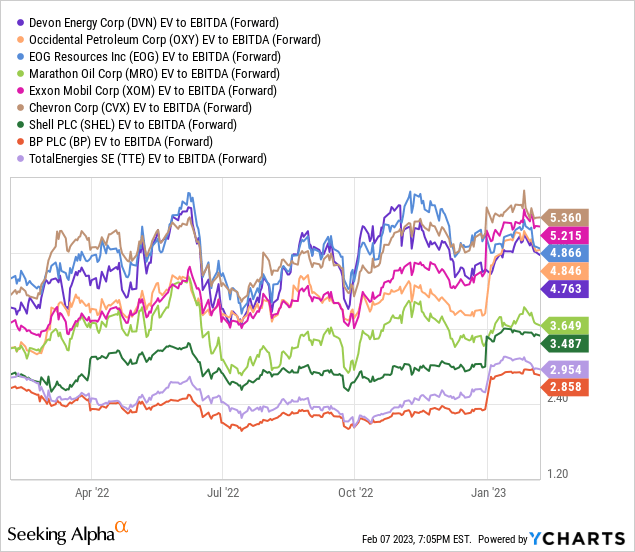

On the other hand, it is important to note that Devon Energy isn’t the cheapest energy company to choose from:

Devon Energy’s valuation is comparable to that of EOG (EOG) and Occidental Petroleum (OXY), but meaningfully higher than that of Marathon Oil (MRO). When we also include the more diversified supermajors, we see that Exxon Mobil (XOM) and Chevron (CVX) are more expensive, while the European supermajors TotalEnergies (TTE), BP (BP), and Shell (SHEL) are considerably cheaper than the rest.

When oil prices rise, all of these companies will benefit. But if prices remain stable, there’s no good reason for Devon to outperform the rest significantly, thus I’m not particularly bullish on Devon Energy. For income investors that like the company’s dividend-focused shareholder return policy, Devon Energy has merit, though.

Takeaway

Devon Energy’s Q4 likely was weaker than its Q3, as lower oil prices and higher capital expenditures will likely have pressured free cash flows. That being said, the free cash flow run rate should still be very solid. A double beat versus estimates wouldn’t be a surprise, as Wall Street has a pretty clear reason of underestimating the company. Overall, Devon looks like a solid, but not especially strong pick in the current environment, which is why I am Neutral on the stock right here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment