Scott Olson/Getty Images News

Following a nice rally off its October lows, Best Buy (NYSE:BBY) is a stock to avoid. The electronics retailer rallied after reporting better-than-expected Q3 results in November; however, its numbers and guidance still weren’t anything to get excited about and could be difficult to hit when it reports earnings next month. Meanwhile, the promotional environment remains difficult, and the company faces difficulties growing its top line.

Company Profile

BBY is an electronics retailer that operates both in the U.S. and Canada. At the end of its fiscal year Q3, it had 979 domestic stores and 160 Canadian locations. The vast majority of its stores are leased. The company plans to close between 20-30 stores annually through fiscal 2025.

Computers and smartphone make up about 44% of its domestic sales, while consumer electronics makes up around 30%. Appliances account for about another 15%.

The company also runs the bestbuy.com website and other related websites. Online sales represent about 30-40% of its total domestic sales.

BBY also has a membership program called Best Buy Totaltech that costs $199.99 a year. The service provides free 24/7/365 tech support, 24 months product protection, and free 2-day shipping, among other perks.

Q3 Earnings

For Q3, BBY saw revenue decline -10.9% to $10.6 billion. Domestic revenue dropped -10.8% to $9.8 billion on a -10.5% decline in same-store sales. Domestic online revenue fell -11.6%.

International sales plunged -14.9% to $787 million, with comparable-store sales down -9.3%. Currency negative impacted sales by -480bps.

Adjusted EPS came in at $1.38, a -33.7% decline.

Inventory was down -14.7%, as the company stockpiled inventory earlier last year due to supply constraints. $600 million in inventory receipts, or about 8% of its inventory, this year shifted into November versus October last year.

Looking to Q4, the company expects SSS to be down -10%.

On the earnings call, CEO Corie Barry said “The promotional environment continues to be considerably more intense than last year. Like Q2, the level of promotionality in Q3 was similar to pre-pandemic levels and in some areas was even more promotional as the industry works through excess inventory in the channel as well as response to softer customer demand.”

CFO Matthew Bilunas added: “The holiday, we do expect to look a little different than last year. So probably more around the sales events, so less early shopping as we saw last year, but a more early shopping than we saw in fiscal ’20. So from what we can see as we exited Q3 with October sales down around 15%. We’re seeing November’s sales start around that same amount. So we’re at this point in line with our expectations. Holiday is obviously quite different than it has been over the prior quarters. So I think we’re appropriately planned for where we see the consumer in front of us.”

Downside Risks

One of the biggest risks BBY faces is a consumer slowdown or potential recession. As the Fed continues to raise interest rates, inflation remains elevated, and tech companies lay off workers, spending on consumer electronics, especially for things like TVs and computers, is particularly vulnerable.

The company had already begun seeing weak same-store sales in 2022, and early indications are that the year did not end strongly. In fact November comparable-store sales were trailing its Q4 guidance, meaning that the company needed a strong December and January just to meet its all-important holiday quarter forecast. This weakness also began before any real economic weakness had hit the U.S. and before the swath of tech layoffs we’ve seen.

BBY execs also noted an elevated promotional environment, which can hurt both sales and margins. And while inventory is down year over year, fewer stores, a $600 million inventory time adjustment, and double-digit same-store sales declines, doesn’t mean that inventory levels are as good as it appears on the surface.

Looking further out, continued deterioration of brick-and-mortar shopping, especially for electronics, is another risk. It’s very easy for consumers to buy smartphones and computers directly from company websites, like Apple (AAPL) or Samsung, as well as through online behemoth Amazon (AMZN). After an initial post-lockdown surge, brick-and-mortar sales at BBY and other retailers have waned. This remains a secular headwind.

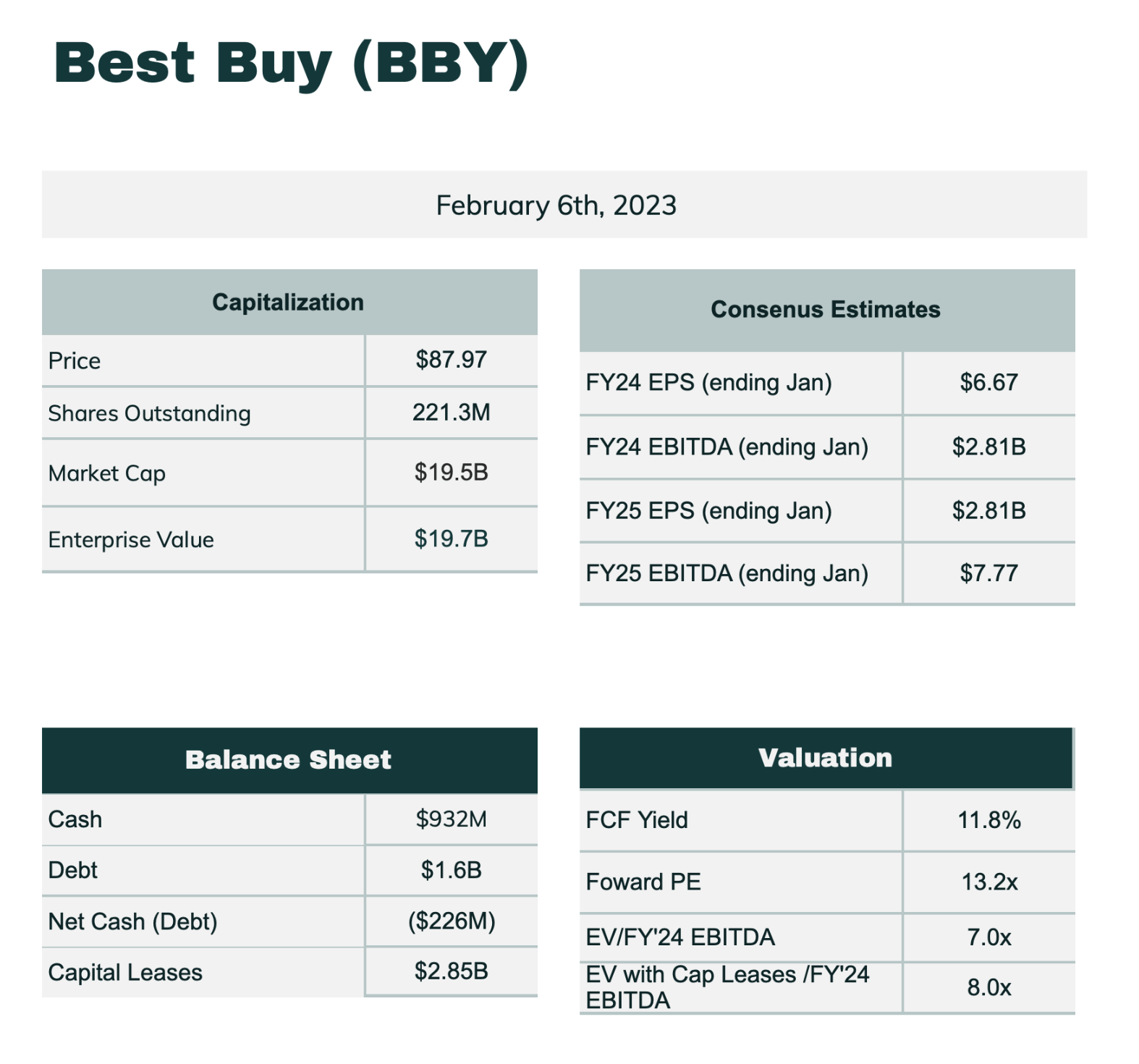

Valuation

Company Filings and FinBox

BBY currently trades around 7x the FY 2024 (ending January) consensus EBITDA of $2.81 billion and 6.5x the FY25 consensus of $3.02 billion. Including capital leases (which I would recommend when valuing retailers), the EV/EBITDA multiple would be about 8x the FY24 consensus.

It trades at a forward PE of 13.2x the FY24 consensus of $6.67.

The company generates around $2.3 billion in FCF, good for a 12.1% FCF yield. It pays out an 88 cents dividend, good for a 4% yield.

Conclusion

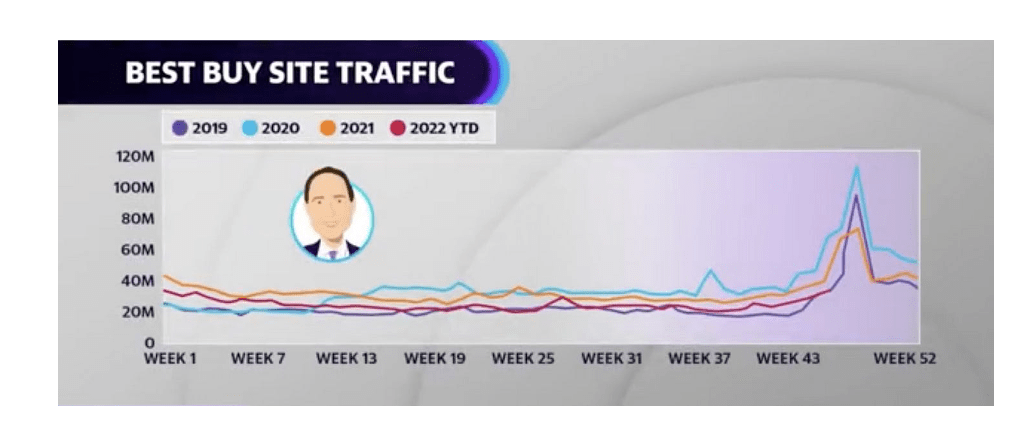

While BBY is forecasting a -10% drop in SSS in Q4, the company noted that its November SSS were tracking around -15% lower, thus indicating it expects a nice improvement in December (and possibly some in January). That could be a big ask, and Evercore was out saying in November that the retailer’s online traffic saw no big acceleration during Black Friday.

Evercore and Brian Sozzi at Yahoo Finance

Throw in a very promotional environment, which hurts gross margins, and at the very least a cautious consumer and things are looking tough for BBY when it reports its results next month.

Trading at around 8x 2023 EBITDA estimates (including capital leases in the Enterprise Value) and 13x EPS, the stock isn’t particularly cheap for a company with zero to declining revenue growth. Meanwhile, next year’s and further out estimates look like they could prove to be too optimistic as well.

It seems like the stock could drop back into the low $60s with a poor earnings report. While investor like BBY’s dividend yield, the stock faces too many headwinds both in the near term and long term. However, the dividend is safe in my view and has room to grow.

Be the first to comment