Note: this article thesis first appeared in the Daily Drilling Report, June 18th. It’s been updated with the recent new of the Validus Energy takeout.

Introduction

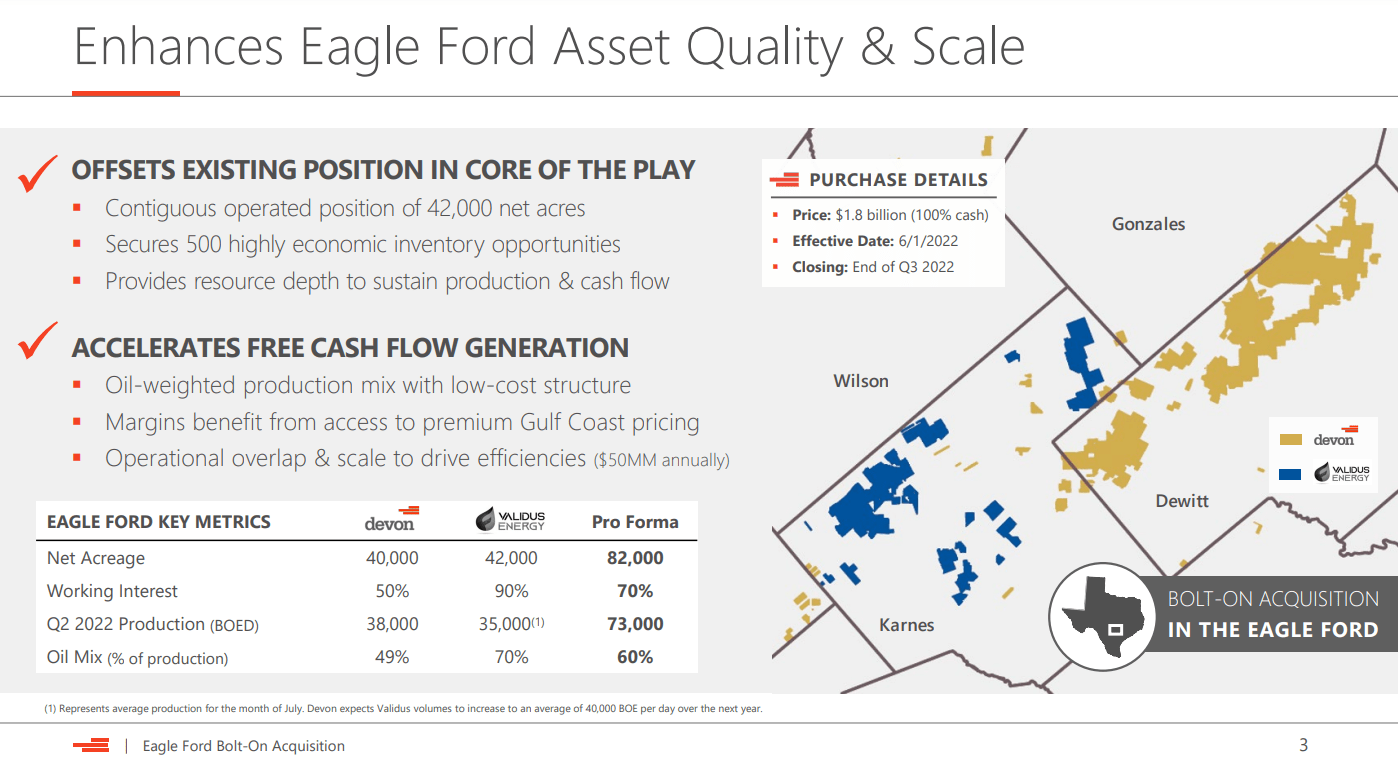

Devon Energy Corporation (NYSE:DVN) has been on a cash flow-fueled acquisition binge the last several years. It began with WPX Energy, and continuing to this week with the $1.8 bn takeout out of privately held Validus Energy. We’ll fold that discussion into the overall thesis for this article a little later.

To me, that last acquisition is revelatory. Devon is looking to beef up its acreage through low cash flow multiple deals, and right now Marathon Oil (MRO) at its current depressed price is in a sweet spot in that regard. This week it was the Eagle Ford, with the Validus deal. Where might they look next?

In this article, we are going to do a little “spitballin’,” a term I use when I am going to probe an undeveloped thesis. I think that Marathon Oil should be bought by Devon Energy. There are a lot of synergies that would come along for DVN by folding MRO into its operations. MRO’s Eagle Ford position is particularly compelling in this light, and in the context of the recent Validus deal.

If you look at areas where they both operate, there is a lot of intersectionality, a word I don’t believe I’ve ever used in an article. We will flesh out the overall thesis first, and then take a look at what MRO would contribute to DVN, thereby making them stronger.

The general idea

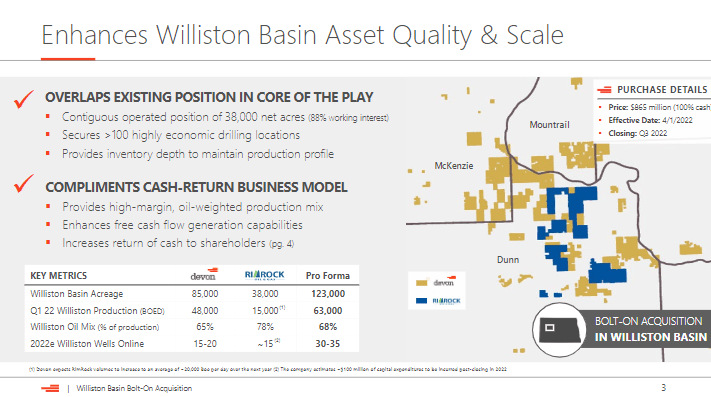

One the recurring themes that we seen behind shale M&A activity in the last couple of years is scale. As the process of extracting oil from the tightly bound pores of shale strata has matured, the advantage of drilling longer laterals has become a dominant factor. For that to happen, you need big chunks of blocky acreage that enable drilling 3-4 miles horizontally following a trend. That was the rationale behind DVN’s acquisitions of WPX, and most recently RimRock in the Williston basin. Rick Muncrief, CEO of DVN disclosed the rationale for the RimRock deal in the linked article:

RimRock’s directly adjacent acreage offers strong operational synergies, adds to our high-quality inventory in the core of the play and positions us to further increase the return of cash to shareholders.

Then there is the notion of declining acreage quality, another thesis I’ve had for Permian production eventually beginning to fall, in spite of increased drilling. At the right price, acreage additions through merger are about the only way to get more Tier I prime acreage.

Those two points- scale and Tier I acreage – fit pretty well into the thesis I’ve described above as to why DVN might be interested in MRO. As noted previously, the Validus deal is suggestive of their current interests. Now, let’s move on to the specific areas where DVN might have some interest in MRO’s assets.

The Delaware sub-basin

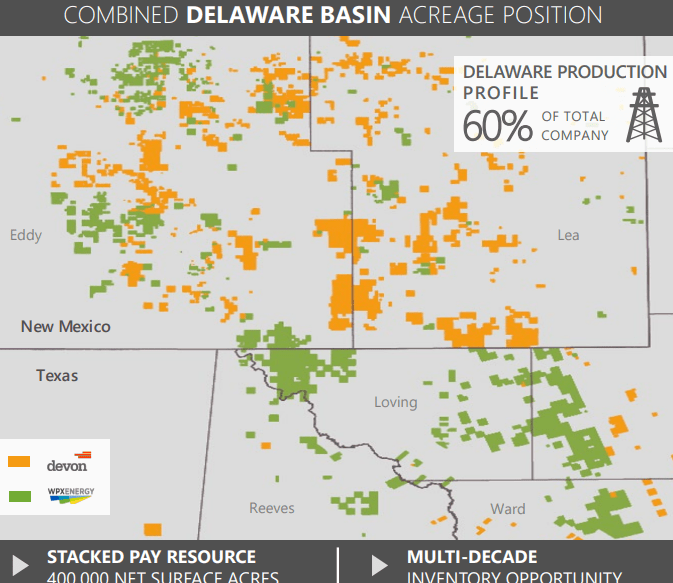

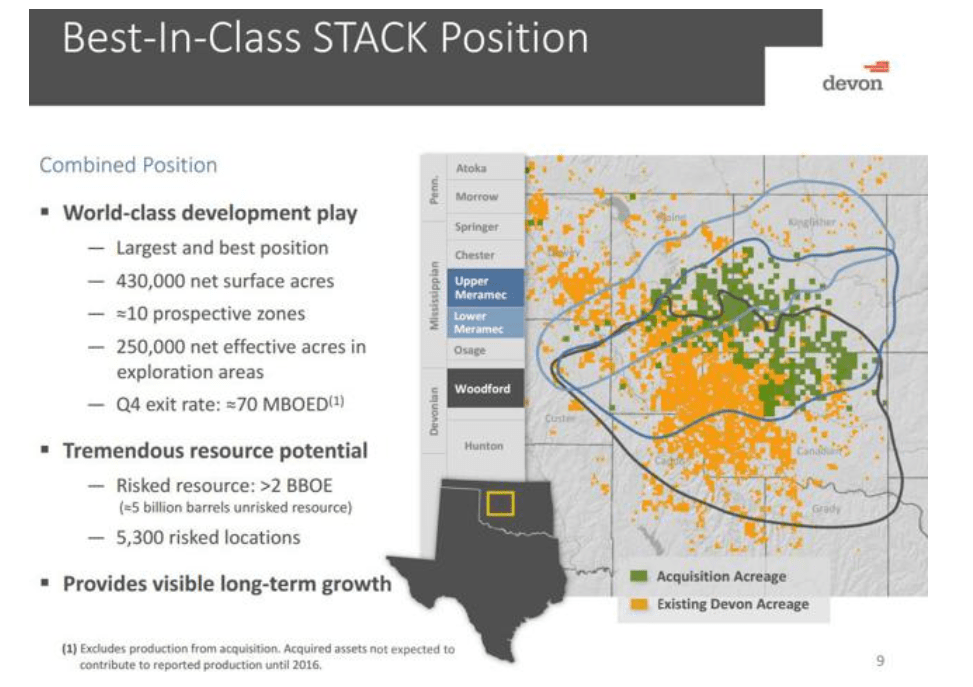

The Delaware basin is certainly the engine for DVN, as they’ve noted in past earnings calls. It’s also where the bulk of their capex budget is going this year. It’s not hard to see the rationale for the WPX merger when you look at the outtake from investor packet below.

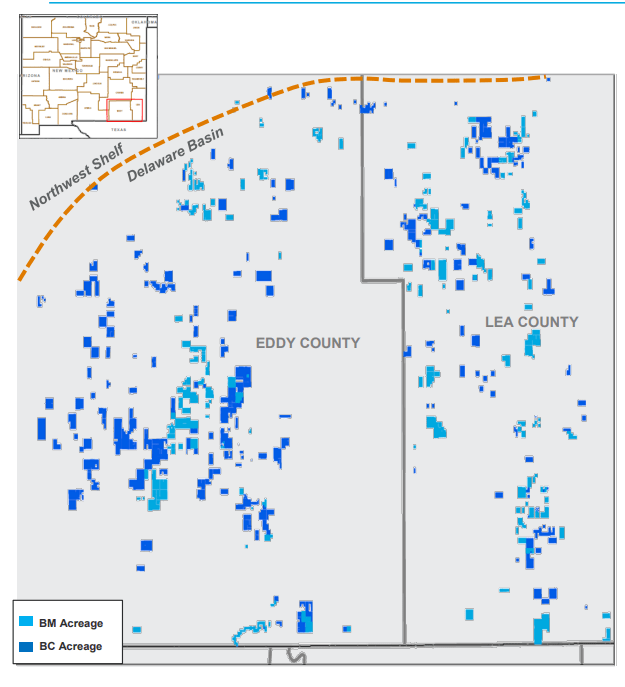

Now look at the acreage MRO picked up in 2017 with its $1.1 bn purchase of Black Mountain, and BC Operating. It fits nicely in the framework of DVN’s Lea and Eddy county, NM acreage. It’s also in the area of the Delaware where DVN is pouring on capital. If I was Rick Muncrief, I would be looking hard at MRO’s Delaware footprint.

In 2015 Devon spent about ~$2 bn to acquire the STACK assets of Felix Energy. It was a bold move at the time, 2015 was not a great year. For example, it was the year Schlumberger, (SLB) told me they had one, highly paid expat Tech Service manager too many, and paid me off. I made this “lemon” into lemonade and started the consulting and writing businesses that continue to this day.

Back to Devon. You can see from the graphic below from their deal presentation that Felix acreage was pure “bolt-on,” extending their footprint northward into the sweet spot of the STACK.

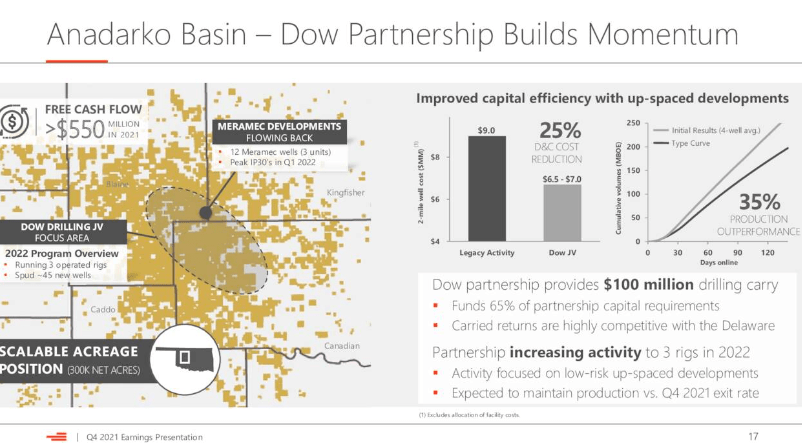

In the intervening time, the company has been fine tuning its approach to the STACK, and bringing in a working interest partner-Dow chemical which has fronted a $100 mm in development capital. They’ve streamlined operations, eliminating 25% of the capital cost of drilling, and plan keeping 3 rigs busy through 2022.

With the focus and success that DVN has had in this play, it’s easy to see how they might rub their hands together at the thought of filling in the gaps still further with the MRO acreage.

This play has probably the least amount of intersectionality of all the plays discussed so far. Devon’s very blocky acreage in northern Dewitt county. Validus’ is over in the northern edge of Karnes County in the absolute sweet spot of the play. As the slide below shows, while 500 new, and very blocky and connected, Tier I drilling locations come with the Validus deal, the acreage can’t really be considered a true ‘Bolt-on’ to DVN’s leasehold over in Dewitt country. Hmm, what would MRO’s Eagle Ford acreage look like in this context?

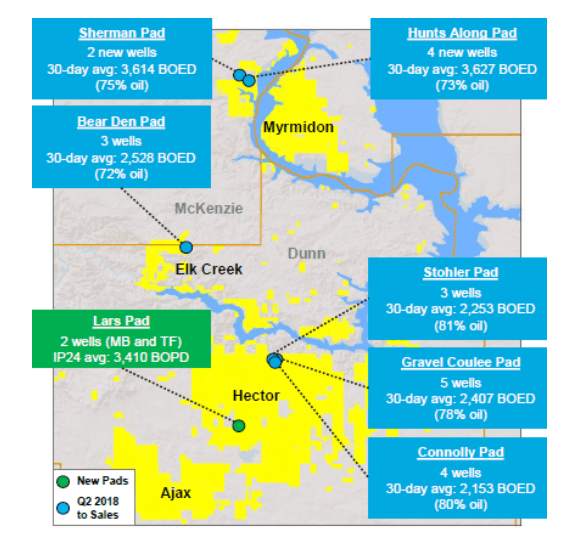

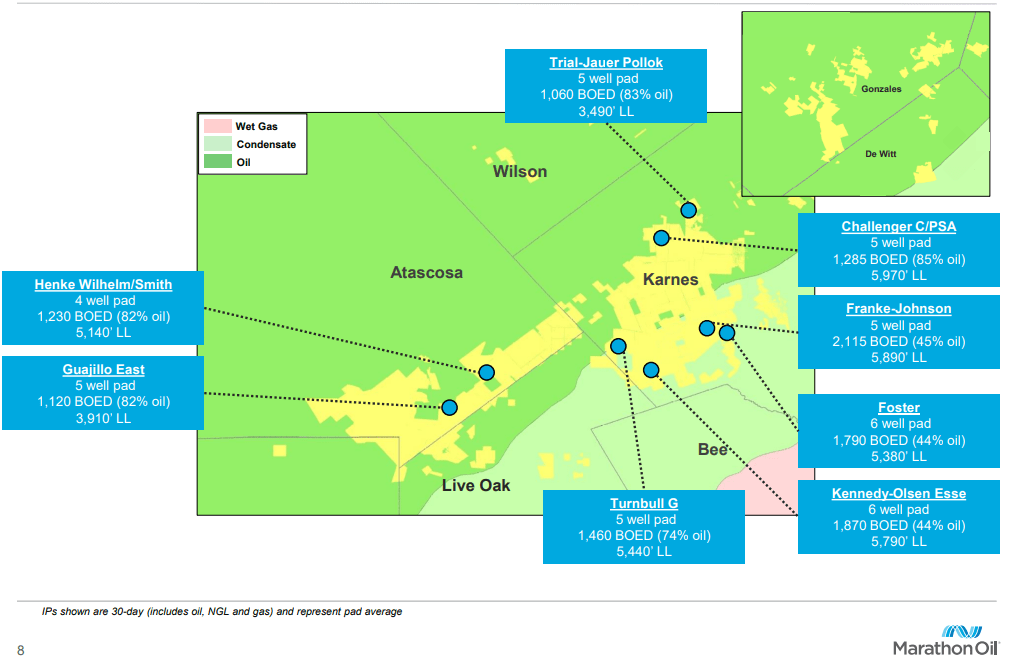

Pretty darn good actually. MRO’s leasehold, by comparison, is in the southern portion of the Eagle Ford play, in Karnes and Atascosa counties with limited and widely dispersed blocks in Dewitt and Gonzales counties. Here’s the thing, though, the critical portion of MRO’s Karnes County acreage fits like a puzzle piece into Devon’s new Eagle Ford geometry.

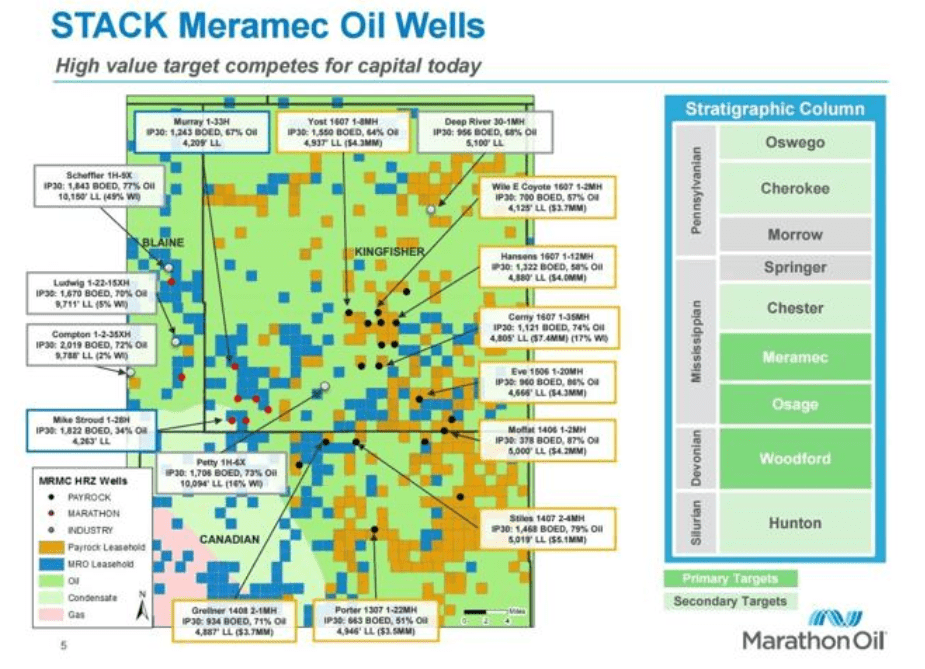

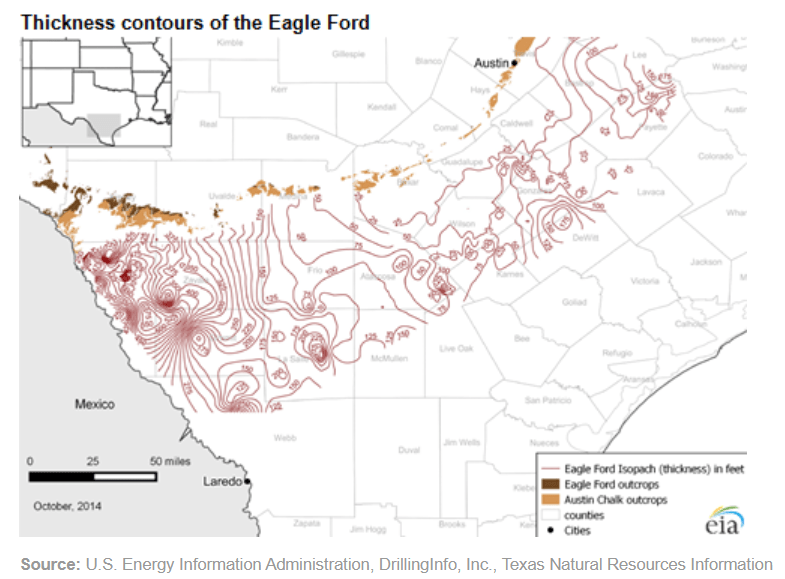

A look at the Energy Information Administration (“EIA”) thickness map of the Eagle Ford suggests that this acreage could be quite productive. The EIA map below shows that the play consists of thin, fairly lensy benches that surround a small section of thicker sand. This is repeated up and down the play. Location, location, location! You’re either in the good stuff, or you’re not.

I have no idea if Devon is looking to make another major M&A deal, and make no mistake, Marathon would be a big bite. Nor do I have the foggiest notion if MRO is shopping for a deal. But Acquisition Fever in the air these days, and it’s not just DVN. Just in May, Centennial Resouce Development, (CDEV), landed privately held driller Colgate Energy for their Delaware basin acreage.

Sometimes the best way to divine people’s intent is to carefully examine what they tell us. First, on the Delaware basin which DVN has told us time and again is their, “Franchise Player.”

Clay Gaspar, COO DVN comments on the quality of their Delaware acreage in relation to other investment opportunities:

I don’t see wholesale changes moving away from the Delaware. We have incredible depth of inventory there, and that’s always shakes out at the high end. We stress test the portfolio in a number of different ways. We move gas relative to oil and what happens is you may reallocate inside the Delaware, but it continues to drive most of that investment of ballpark 70% to the Delaware Basin. Remember, we have some deeper gas – gassier options inside the Delaware that we barely have scratched the surface on. So it’s – there’s a lot of significant upside around the portfolio, but I don’t see a wholesale change from us being a predominantly Delaware Basin focused organization.

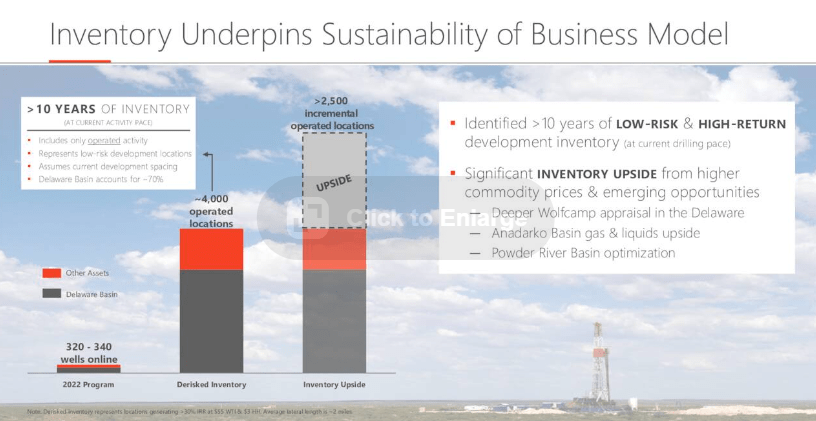

Doug Leggate, BOA analyst, asks about Delaware basin inventory durability:

On Slide 20, you show us 2,500 – sorry, 4,000 locations in the current inventory and up to another 2,500. So my question is presumably that includes the gas sensitivity, and I guess the question I’m really trying to get to is that’s about a 15-year inventory, your current pace including the 2,500. How does Devon avoid being a third smaller five years from now on this inventory deck?

If you recall that slide is all based on a 33, excuse me, a $3 (GAS) and $55 (WTI) world. And so certainly as that commodity price runs up the whole quantification of those opportunities come up as well. (The implication being that in the current price environment this inventory could be expanded.) We’ll certainly look to augment. Now, remember, we’re still looking at other deeper horizons as an example in the Wolfcamp in the Permian that adds to that inventory, We’ve done a great, some great things in the past with bolt-on acquisitions, (Referring to WPX here.) right in the heart of what we’re doing. Our land team continues to do a great job of trades that bolsters these numbers as well. And then of course, the kind of little E exploration kind of under positions that we already own also adds to these positions

Rick Muncrief in response to a question about valuation on the stock and possible M&A thinking:

We just think we’re fundamentally undervalued. And so once again that makes potential acquisitions more challenging because it fundamentally just has to be very accretive to us and we have to feel that it makes sense. And so nothing’s really changed from what you’ve seen over last several years, really.

Your takeaway

So we have a bit of mixed messaging here from management. The overall tone-which could be by design, oilies are generally pretty fair poker players, is the company is well satisfied with it’s position in the Delaware basin. As noted by Gaspar the 6,500 de-risked drilling sites could be expanded by just raising the oil and gas prices used in the calculation. This would likely involve deeper horizons, B,C,D, in the Wolfcamp and Bone Spring. This would suggest little interest in going after a mid-sized player like Marathon.

On the other hand, Leggate’s question is revelatory in regard to what’s in the analyst’s minds, which means it’s on management’s minds as well, inventory and Top Tier Drilling locations. You have to think that Muncrief is keenly aware of how well MRO acreage would fit into their current acreage position.

There is also the larger question, could DVN- 2.5X the size of MRO, go after them? Certainly not with cash or debt. Those days are gone. Muncrief does have a track record of doing stocks swaps as was done with WPX. If a deal was announced Tuesday at a 20% premium to MRO’s Friday closing price, plus the ~$4.0 bn in debt MRO is carrying it would be for about $28-9 per share, which at DVN’s closing price would be roughly a 2 for 1. It’s been done before.

In regard to MRO’s thinking about being acquired. Nothing came up in their call on the M&A subject, so I won’t speculate. MRO management has to be aware of what a tempting target they are with ~350K BOEPD production, and $4.5 bn free cash flow generation. A 23% cash flow yield will draw hungry eyes. Perhaps a merger with DVN would be a chance to control their fate with like-minded people.

We will wrap up this bit of whimsy to submit for your inspection. To my way of thinking, the table is set for someone. I expect there are a number of big game hunters doing the same legwork I have done here. It might not be DVN, after all they’ve busy recently as we’ve discussed.

Still if MRO were put in play, could DVN just sit on the side lines? So far Rick Muncrief has shown a lot of discipline, but as we have discussed, Tier I drilling don’t grow on trees. Could he pull a “Vicky Hollub” and run to the Oracle? Probably not, although in spite of the train wreck, Occidental Petroleum, (OXY) and Anadarko appeared to be, three years hence Miss Vicki is looking pretty smart.

These days it’s the “firstest, with the mostest,” and I don’t see MRO lasting very long in this environment.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment