Editor’s note: Seeking Alpha is proud to welcome Ronald Ferrie as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Variability can both be a blessing and a curse. chaofann

Investment Thesis

Sky high yields can be attractive during times of high energy prices. This however, can lead to undo risk to capital losses if entry points are not made selectively. I will make a case for entry in Devon Energy (NYSE:DVN) stock at values less than $60/share based on historical energy prices to maximize yield and minimize capital risk. I believe that over reaction to market headlines will provide a solid opportunity post earnings on February 14th.

The Company

Devon Energy Corporation is an independent oil and natural gas producer. The company operates in basins located in Texas, New Mexico, Oklahoma, Wyoming, and North Dakota.

Variable Dividend

For those of you new to Devon Energy, the company’s operating objective is to produce high levels of free cash flow, and in turn, generate a fixed plus variable rate dividend to shareholders.

During the course of 2022, shareholders have seen payout changes ranging from +27% to – 13%. To those who do not frequently follow the company or are unfamiliar with a variable dividend policy, this could be alarming and has the potential to affect the share price of the company’s stock.

To that end, following the most recent dividend reduction (-13% following Q3), the market initiated a sell off even though this should have been expected due to lowering energy prices and a variable dividend policy.

Devon Energy’s current dividend policy is defined in the company’s earning slides:

Dividend Policy (Devon Energy Q3 2022 Earnings Slide 8)

In this article, I will outline a few easy metrics to help investors more accurately predict future returns based off the price of the preceding quarter’s WTI average price and capitalize on over reactions of the market. This model does have some inaccuracies/assumptions but can be used to eliminate the guess work in predicting future returns and minimize future risk.

The Tool

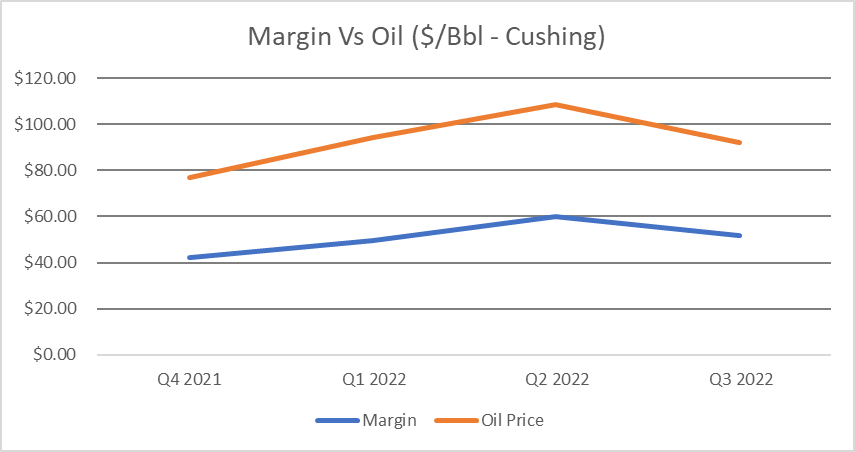

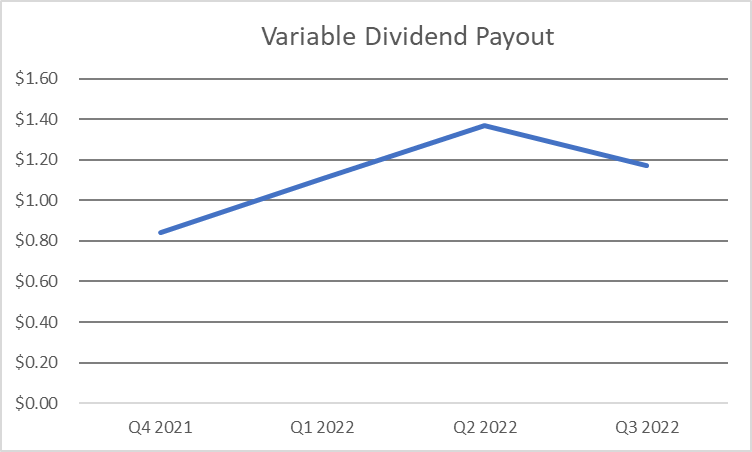

Using the company’s supplemental tables found on the Investor Page, a correlation to the price per barrel of oil and the variable dividend payout can be determined. The figures below are a visual representation of the profitability and payout over the last four quarters.

Image created by author by data from Devon Energy Q3 supplemental data tables Image created by author with data from Devon Energy’s dividend history page

You can see the similarities between the two graphs. It’s simple, that’s the best part. A little math can help us see where we are going and what we should expect.

As a shareholder, I want to know how much cash to expect from my investment. With Devon, there are two important factors:

1. Profitability is based on commodity prices (Oil, NGLs, Natural Gas).

2. The payout is for profits the company made 3-6 months prior to the payout date. Thus, there is always a time lag of one quarter. Q1 pays out at the end of Q2, Q2 pays out at the end of Q3 and so on. This gives us time to be patient and capitalize when the market is not valuing Devon Energy correctly (both to sell and to buy).

Since commodities are a highly tracked item, the average oil price is easily obtained with a quick google search using EIA data.

To determine how much a shareholder gets paid for every barrel of oil sold, I divide the total dividend by the price of the barrel of oil for the quarter. This creates what I call, the ‘Shareholder Efficiency’. This is the fraction of profits the shareholder will receive for every barrel of oil equivalents sold.

In the table below you can see the average for the last 5 quarters is approximately 1.35%, or a shareholder receives 1.35% of the price of every barrel of oil equivalents sold.

You will also note that this metric is improving as the company raises its fixed dividend, pays down debt, buys back shares, and controls capital expenses.

| Q3 2021 | Q4 2021 | Q1 2022 | Q2 2022 | Q3 2022 | |

| Total Dividend | $0.84 | $1.00 | $1.27 | $1.55 | $1.35 |

| Variable | $0.73 | $0.84 | $1.11 | $1.37 | $1.17 |

| Fixed | $0.11 | $0.16 | $0.16 | $0.18 | $0.18 |

| Field Margin | $37.17 | $42.37 | $49.45 | $60.12 | $51.90 |

| Oil Price | $70.64 | $76.91 | $94.45 | $108.70 | $91.87 |

| Shareholder Eff. | 1.19% | 1.30% | 1.34% | 1.43% | 1.47% |

Using EIA data, Q4 2022 average oil price was $82.79. Using the average ‘Shareholder Efficiency’, this would correlate to a total dividend payout of $1.12/share. This does not account for the previously announced 2% production hit and should be adjusted for accordingly.

Predicting Returns/ROI

Is this tool perfect?

No, as the company’s debt profile changes and operational decisions to add or subtract rig counts fluctuates, or weather impacts take their effect, the accuracy of the above predictions will fluctuate.

But it does give some indicators of what to expect in the upcoming earnings announcement on February 14th, 2023. Some margin has been built in using 1.35% versus the 1.47% from Q3 of 2022. I have currently calculated at 7.4% return for the upcoming payout.

I personally use this to add/subtract from my position when there is a disconnect between share price and the expected future payouts. When yields approach 8%, the payout is with worth the volatility in share price and potential risks.

The market rewards the prepared. With some forethought and a little math, we can anticipate (with some accuracy), market disappointments or market euphoria.

Baking in a Little Extra

What is not accounted for so far is the effect of buybacks and the recent acquisitions of Validus Energy and Rimrock Oil and Gas.

These acquisitions pose to increase production by roughly 10% as well as providing additional inventory and efficiencies for the future. Previous quarters did not have this benefit to add to free cash flow or the dividend payout. This should add between $0.10 and $0.12 to the dividend in the upcoming quarter.

Devon Energy has approximately $700 million left in its buyback program to help provide a price floor for its shares thanks to opportunistic purchase that has been discussed over the last several quarterly conference calls. Additionally, everyone’s ‘piece of the pie’ gets a little bit bigger thanks to buybacks and should also raise the dividends per share.

The Other Side of the Coin

Devon has committed to returning 50% of the excess free cash flow to its shareholders. So what’s happening to the other 50%? Some of Devon’s competitors are returning levels as high at 75% to its shareholders. Is Devon hoarding its cash?

YES! Well, sort of.

The Validus Energy and Rimrock acquisitions came at a total bill of about $2.6 Billion. This purchase is being used to fund growth, efficiencies, and inventory to keep the oil pumping (and cash). The remainder of the excess free cash flow goes to help fund deals like these.

Other competitors are funding acquisitions through a mix of cash and stock deals, thus diluting shareholder equity.

I am of the opinion that the current frame work strikes a nice balance between cash for me now, and allowing management to make strategic decisions with the excess cash for the future. I would prefer this vice diluting my equity in the company by issuing more shares to fund growth.

The use of excess funds for strategic acquisitions is the other side of the shareholder returns coin that makes Devon Energy a company that you hold in spite of all the volatility in the energy markets.

Summary

This article provides the framework for estimating future dividend payouts for an oil producer with a variable dividend policy based on the preceding quarter’s average oil price. Alterations may need to be made for operational changes and external impacts such as acquisitions, buybacks and weather.

At the current share price of $60.75, and a potential annualized payout of $4.48/share, this investment would yield 7.4% on an annual basis, which is solid. But we can do better.

I believe that post earning/dividend announcements for Q4, the market will react negatively to a subsequent 17% reduction in dividend payments($1.12 vs $1.35). This will provide an attractive entry point. I recommend purchasing at levels below $57/share (7.85% yield). This is about a 6% discount from today’s price of $60.75.

In addition, 50% of excess free cash flow is being used to grow the company’s cash generation as well as creating inventory for the future. This will help to drive the share price up over the long term.

Patience and preparation will create larger profits when investing with Devon Energy. Since the ex-dividend date is usually 4 to 6 weeks post earnings, we can pounce on a good opportunity when it comes our way. I expect this to come following Q4 results being released on February 14th 2023.

I hope investors find this useful to help protect their capital investment as well as boosting yields/future cash payouts.

Be the first to comment