David McNew

Investment Thesis

- Delta Air Lines (NYSE:NYSE:DAL) has competitive advantages, which help the company to build an economic moat over its competitors.

- The company’s global airlines network and high necessary capital expenditures lead to the fact that it is difficult for new competitors to enter the airline industry.

- Delta Air Lines’ EBIT Margin of 5.82% is higher than the one of United Airlines (UAL) (EBIT Margin of 2.01%) and Southwest Airlines (LUV) (0.03%), underlying the company’s relatively strong competitive position.

- At the current stock price, my DCF Model indicates an Internal Rate of Return of 10%; however, I continue to see a large amount of risk attached to a Delta Air Lines investment. This leads me to the conclusion that the reward you can achieve from investing in the company is not worth the risk.

- If you do decide to invest in the airline industry, I would recommend that you only invest a maximum of 3% of your overall investment portfolio.

Delta Air Lines’ Stock Performance

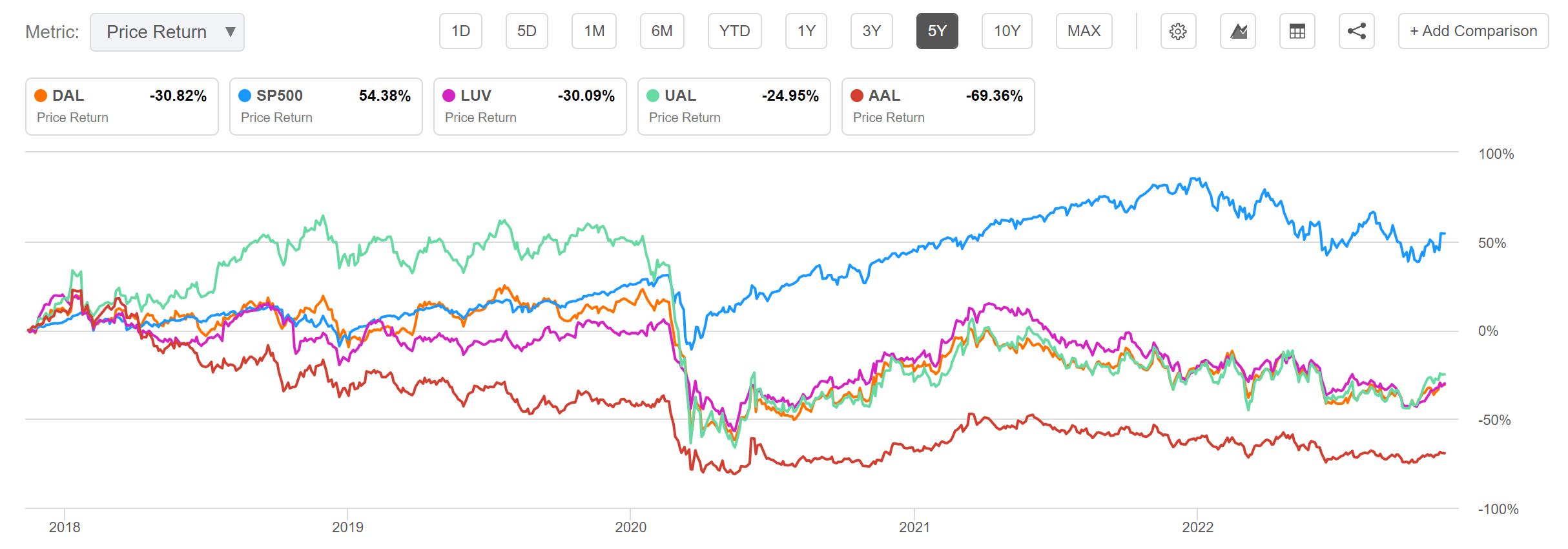

The S&P 500 has shown a performance of 54.38% in the past 5 years as shown in the graphic below. The performance of Delta Air Lines (-30.82%) as well as the performance of other companies from the same industry such as Southwest Airlines (-30.09%), United Airlines (-24.95%) and American Airlines (NASDAQ:AAL) (-69.36%) are significantly inferior when compared to the performance of the S&P 500.

Even if no direct conclusions for the future can be drawn from the past, history has shown that an investment in the S&P 500 (which is associated with less risk due to the broad diversification) has generated a significantly better return than any investments in these airline companies.

This strengthens my investment thesis that the reward is not worth the risk when deciding to invest in Delta Air Lines or the airline industry in general.

Source: Seeking Alpha

Delta Air Lines’ 3Q22 Financial Results

Delta Air Lines delivered strong 3Q22 results: the company presented an operating revenue of $12.8B, implying an increase of 3% when compared to the same quarter of 2019. At the same time, the airline company revealed an operating income of $1.5B, implying an operating margin of 11.6%.

Ed Bastian, Delta’s chief executive officer, commented on these results with the following words:

“With strong demand and a return to best-in-class operational performance, we are ahead of our plan for the year on profitability and expect to be free cash flow positive. We’re working towards full network restoration by summer of 2023, which supports a meaningful step up in profitability and cash flow next year on our path to earn over $7 of EPS and $4 billion of free cash flow in 2024.”

The Competitive Advantages and Growth Drivers of Delta Air Lines

In my previous analysis on Delta Air Lines back in August, I showed that the company disposes of strong competitive advantages. Due to this, I will only briefly discuss its competitive advantages in this analysis. Among others, I mentioned the company’s global network as a competitive advantage:

“The company’s global network contributes to a strong competitive advantage. Delta Air Lines serves over 130 countries and territories as well as over 800 destinations around the world. At the end of 2021, Delta Air Lines offered more than 4,000 daily departures to its customers. Furthermore, the company’s global network is supported by a fleet of about 1,200 aircraft that vary in size and capabilities. This gives the company flexibility to adjust aircraft to its existing network.”

In addition to the above, I mentioned in the same analysis that these competitive advantages help the company to build an economic moat over its competitors:

“The global network of Delta Air Lines and other existing airline companies in combination with high necessary capital expenditures (such as for aircraft leases and leases of airport property and other facilities) contribute to the fact that it’s extremely difficult for new competitors to enter the industry.”

From my perspective, these competitive advantages contribute to the fact that new competitors are unable to enter the market, but I don’t identify strong growth drivers for Delta Air Lines’ business, which contributes to my sell rating for the company.

The Valuation of Delta Air Lines

Discounted Cash Flow [DCF]-Model

I have used the DCF Model to determine the intrinsic value of Delta Air Lines. The method calculates a fair value of $34.61 for the company. Its current stock price of $35.00 gives Delta Air Lines a downside of 1.1%.

My calculations are based on these assumptions as presented below (in $ millions except per share items):

|

Delta Air Lines |

|

|

Company Ticker |

DAL |

|

Tax Rate |

30.0% |

|

Discount Rate [WACC] |

10.5% |

|

Perpetual Growth Rate |

2% |

|

EV/EBITDA Multiple |

9.9x |

|

Current Price/Share |

$35.00 |

|

Shares Outstanding |

638,2 |

|

Debt |

$31,936 |

|

Cash |

$7,023 |

|

Capex |

$5,384 |

Source: The Author

Based on the above, I have calculated the following results for Delta Air Lines:

Market Value vs. Intrinsic Value

|

Delta Air Lines |

|

|

Market Value |

$35.00 |

|

Downside |

1.1% |

|

Intrinsic Value |

$34.61 |

Source: The Author

Internal Rate of Return for Delta Air Lines

Below you can find the Internal Rate of Return as according to my DCF Model. I assumed different purchase prices for the Delta Air Lines stock.

At Delta Air Lines’ current stock price of $35.00, my DCF Model indicates an Internal Rate of Return of approximately 10% for the company. (In bold you can see the Internal Rate of Return for Delta Air Lines’ current stock price of $35.00.)

|

Purchase Price of the Delta Air Lines Stock |

Internal Rate of Return as according to my DCF Model |

|

$22.50 |

15% |

|

$25.00 |

14% |

|

$27.50 |

13% |

|

$30.00 |

12% |

|

$32.50 |

11% |

|

$35.00 |

10% |

|

$37.50 |

9% |

|

$40.00 |

9% |

|

$42.50 |

8% |

|

$45.00 |

7% |

|

$47.50 |

6% |

Source: The Author

Please note that the Internal Rates of Return above are a result of the calculations of my DCF Model and changing its assumptions could result in different outcomes.

The fact that my DCF Model indicates an expected compound annual rate of return of 10% for Delta Air Lines, strengthens my belief that the reward is currently not worth the risk when considering an investment in the company. For this reward, I see too many risk factors attached. Therefore, I reiterate my sell rating in regards to the Delta Air Lines stock. In the Risk section of this analysis, I will describe these risk factors in more detail.

Delta Air Lines’ Fundamentals in comparison to its competitors such as Southwest Airlines, United Airlines and American Airlines

At this moment in time, Delta Air Lines has a similar market capitalization to Southwest Airlines: while Delta Air Lines’ market capitalization is $22.20B, Southwest Airlines’ is $22.41B. However, Delta Air Lines’ market capitalization is significantly higher than United Airlines’ ($14.39B) and American Airlines’ (9.54B).

Delta Air Lines’ current EBIT Margin of 5.82% is higher than both United Airlines’ (2.01%) and American Airlines’ (0.03%), but lower than Southwest Airlines’ (7.16%). The generally low EBIT Margins of these companies from the airline industry provides proof that an investment in this sector comes with high risk factors. Declining revenues can result in losses, which in turn can increase the probability of bankruptcy.

When it comes to growth, we can see that Delta Air Lines is slightly ahead of its competitors: while Delta Air Lines has shown a Revenue Growth of 2.92% over the last five years [CAGR], Southwest Airlines’ is 1.60%, United Airlines’ 1.74% and American Airlines’ 1.58%.

In terms of Valuation, Delta Air Lines is slightly more attractive than most of its competitors: while Delta Air Lines has a P/E Non-GAAP [FWD] Ratio of 12.13, Southwest Airlines’ is 16.75 and United Airlines’ is 20.68. At the same time, Delta Air Lines’ P/E Non-GAAP [FWD] Ratio is 29.39% lower than the sector median, which is 17.18.

When it comes to risk, it can be highlighted further that Delta Air Lines has a high Total Debt to Equity Ratio of 695.77%, which is a strong indicator that the risk of investing in the company is very high. This once again reinforces my belief that the reward is not worth the risk when considering an investment in Delta Air Lines. The company’s Debt to Equity Ratio is significantly higher than that of Southwest Airlines (92.57%), but lower than United Airlines’ (783.50%).

|

Delta Air Lines |

Southwest Airlines |

United Airlines |

American Airlines |

||

|

General Information |

Ticker |

DAL |

LUV |

UAL |

AAL |

|

Sector |

Industrials |

Industrials |

Industrials |

Industrials |

|

|

Industry |

Airlines |

Airlines |

Airlines |

Airlines |

|

|

Market Cap |

22.20B |

22.41B |

14.39B |

9.54B |

|

|

Profitability |

EBIT Margin |

5.82% |

7.16% |

2.01% |

0.03% |

|

ROE |

2.25% |

7.81% |

-14.56% |

NM |

|

|

Valuation |

P/E Non-GAAP [FWD] |

12.13 |

16.75 |

20.68 |

– |

|

Growth |

Revenue Growth 3 Year [CAGR] |

0.22% |

0.43% |

-1.67% |

-0.13% |

|

Revenue Growth 5 Year [CAGR] |

2.92% |

1.60% |

1.74% |

1.58% |

|

|

EBIT Growth 3 Year [CAGR] |

-24.52% |

-19.37% |

-43.23% |

-84.55% |

|

|

Income Statement |

Revenue |

46.62B |

22.69B |

40.75B |

45.21B |

|

EBITDA |

4.47B |

2.72B |

3.09B |

2.40B |

|

|

Balance Sheet |

Total Debt to Equity Ratio |

695.77% |

92.57% |

783.50% |

NM |

Source: Seeking Alpha

The High-Quality Company [HQC] Scorecard

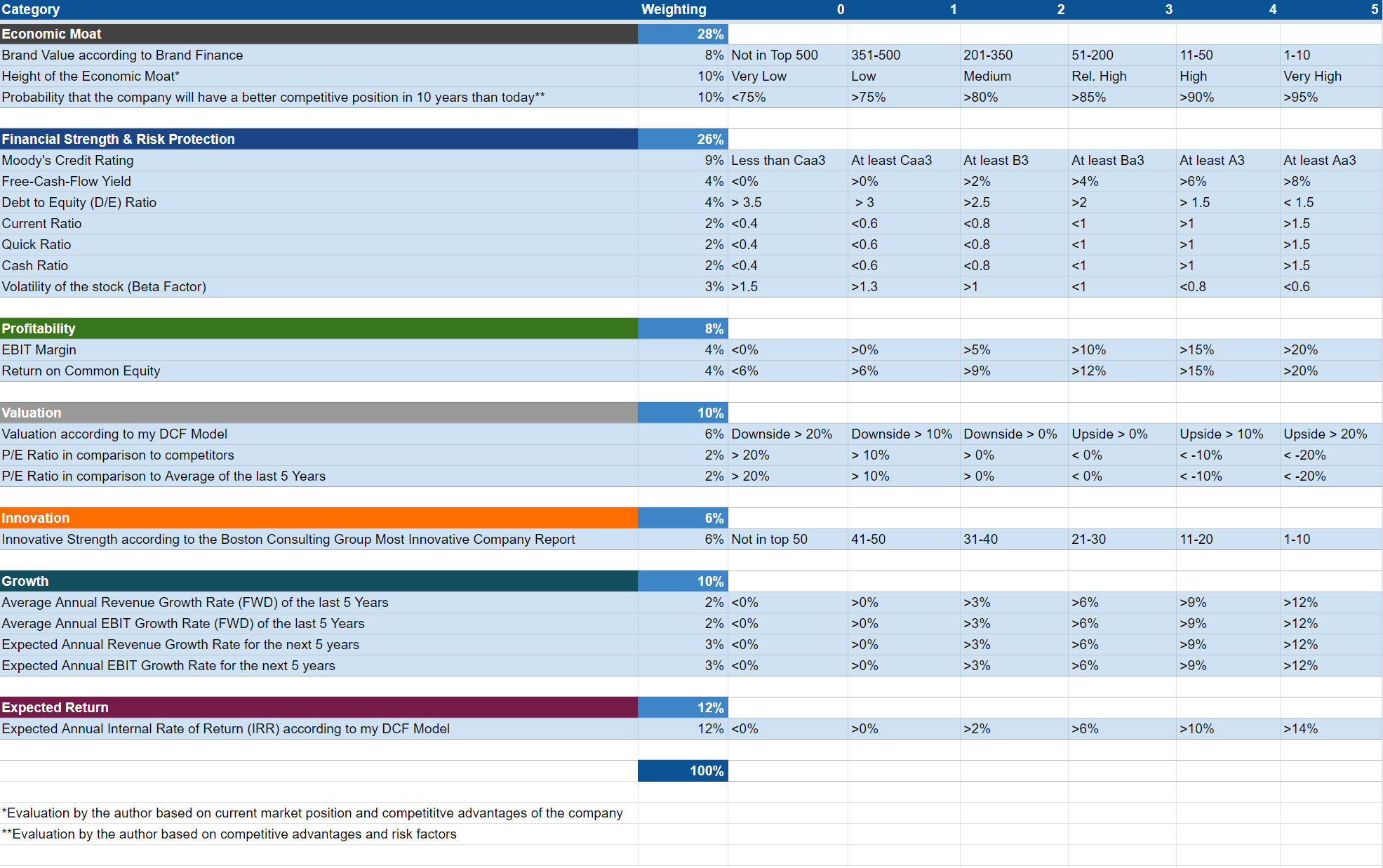

“The HQC Scorecard aims to help investors identify companies which are attractive long-term investments in terms of risk and reward.” Here, you can find a detailed description of how the Scorecard works.

Overview of the Items on the HQC Scorecard

“In the graphic below, you can find the individual items and weighting for each category of the HQC Scorecard. A score between 0 and 5 is given (with 0 being the lowest rating and 5 the highest) for each item on the Scorecard. Furthermore, you can see the conditions that must be met for each point of every rated item.”

Source: The Author

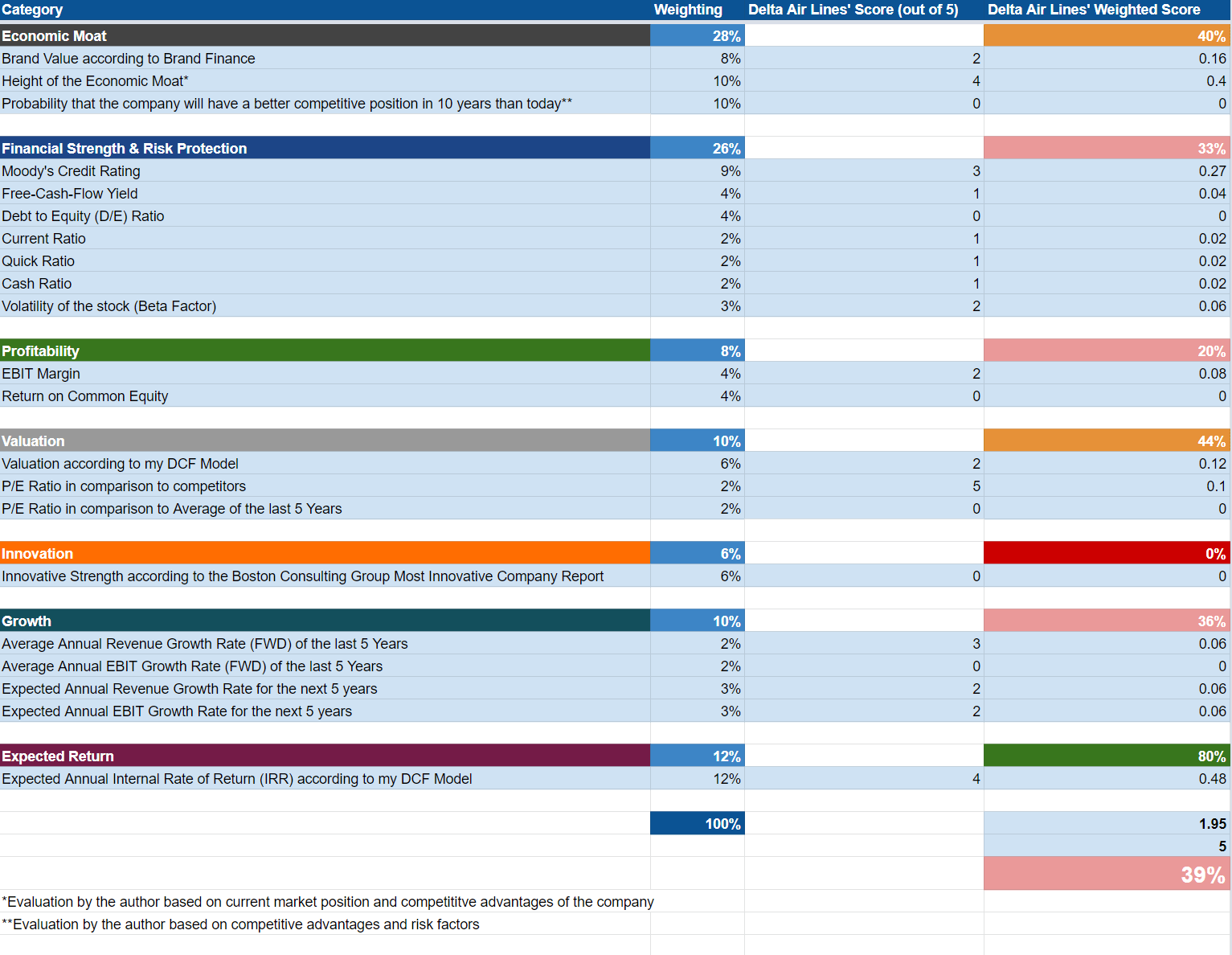

Delta Air Lines According to the HQC Scorecard

Source: The Author

According to the HQC Scorecard, Delta Air Lines is rated as unattractive in terms of risk and reward, achieving an overall score of 39 out of 100 points.

Delta Air Lines is rated as moderately attractive in the categories of Valuation (44/100) and Economic Moat (40/100). For Growth (36/100), Financial Strength (33/100) and Profitability (20/100), the company is rated as unattractive. Only in the category of Expected Return, is the company rated as very attractive (80/100).

Delta Air Lines’ unattractive overall rating (39/100), validates my opinion to rate the company as a sell at this moment in time.

Risk Factors

From my point of view, there are plenty of risk factors investors should take into consideration when thinking about investing in Delta Air Lines:

In my previous analysis on Delta Air Lines, I discussed that the financial results of companies from the airline industry vary widely depending on the price of aircraft fuel:

“Increases in the cost of crude oil could have an adverse effect on the company’s operating results. Over time, fuel prices have been highly volatile. Proof of this is the fact that from 2019 to 2021 the company’s average annual fuel price per gallon varied from $1.64 to $2.02. Year to year variations ranged from a decrease of 19% to an increase of 23%, as according to the company.”

Furthermore, I mentioned in my previous analysis that Delta Air Lines might see a situation in which it can not meet its obligations:

“Additionally, Delta Air Lines has a significant amount of existing fixed obligations (which includes, among others, aircraft lease and debt financings, leases of airport property and other facilities). A disruption to its business operations (which could be, for example, caused by another pandemic) might see a situation in which the company isn’t able to meet its obligations.”

I also explained that consumer behavior has changed as a result of the pandemic and that I do not expect it to return to the previous level:

“It can be assumed that the number of flights will not return to pre-pandemic levels in the future due to companies having recognized the advantages of virtual meetings and are therefore more likely to save on travel expenses. As according to Reuters, Amazon (NASDAQ:AMZN) alone saved $1 billion in travel costs during the pandemic.”

In addition to the risk mentioned above, Delta Air Lines’ high Total Debt to Equity Ratio of 695.77% and its relatively low EBIT Margin of 5.82% demonstrate the high risk that is attached to an investment in the company. This relatively high number of risk factors increases my confidence in the theory that Delta Air Lines should be rated as a sell.

The Bottom Line

At this moment in time, I consider that the reward is not worth the risk when considering to invest in Delta Air Lines. In the Risk section of this analysis, I mentioned a large amount of factors that you need to take into account before investing in the company. At the current stock price of $35, my DCF model demonstrates an expected compound annual rate of return of 10% for Delta Air Lines. From my point of view, this reward is not worth the aforementioned risks; underlying my sell rating for the company.

In general, I don’t see the airline industry as being very attractive from an investors perspective. This is especially due to the high-risk factors for airline companies in general; however, if you decide to invest in Delta Air Lines or in another company from the industry, I would suggest that you limit your investment to a maximum of 3% of your total investment portfolio.

Be the first to comment