kschulze/iStock via Getty Images

Homebuilding is a boring, cyclical industry, right? Wrong! The industry is trading at incredibly low PE ratios. DHI currently has a PE ratio near 6 and a forward PE of 9, in a market where the average PE for the S&P 500 is 22. Now, that’s exciting! When these types of imbalances occur, we know that there is something interesting behind the numbers, so let’s dive in.

D.R. Horton (NYSE:DHI) is the largest homebuilder in America, with 2022 revenue near $33.5 billion, netting $5.8 billion (~23% net margins). Now we see our first discrepancy. For a cyclical, highly competitive, commodity-like industry, 23% net margins are incredible. Heck, the 10-year industry average is 7%. But as the low P/E ratio suggests, the market is skeptical of these margins. And for a good reason, as there are some major headwinds upcoming for homebuilders.

The headwinds that I perceive for the industry include high inflation, high home prices, and a possible recession. The long-term outlook is significantly better, as there is a housing shortage in the US. This is a long-term tailwind that will benefit the industry as a whole. DHI is well-positioned to take advantage of this tailwind as they are the largest homebuilder in the country.

Background/Current Outlook

Industry Short-Term Outlook (Headwinds)

It may not come as a surprise to the experienced investor that a cyclical industry may not fare well in the next couple of years, as the threat of a recession is looming over the US economy. But that is the current reality of the homebuilding industry.

High inflation has caused the FED to increase interest rates to over 4%. The average 30-year fixed mortgage rate has increased to over 6%, which is nearly double the rate of one year ago.

Home prices are also at record highs and have increased rapidly over the past 2 years.

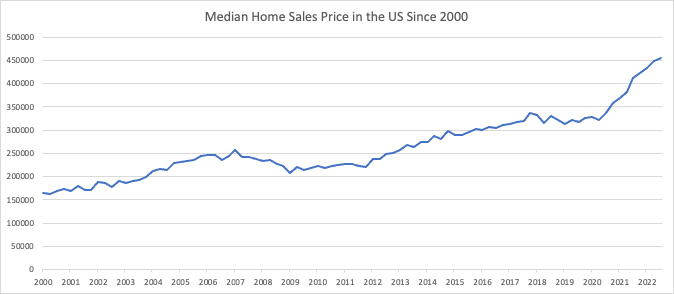

Author Created from FRED Data

As shown by the graphic above, the median sales price has increased sharply (~38%) since 2020.

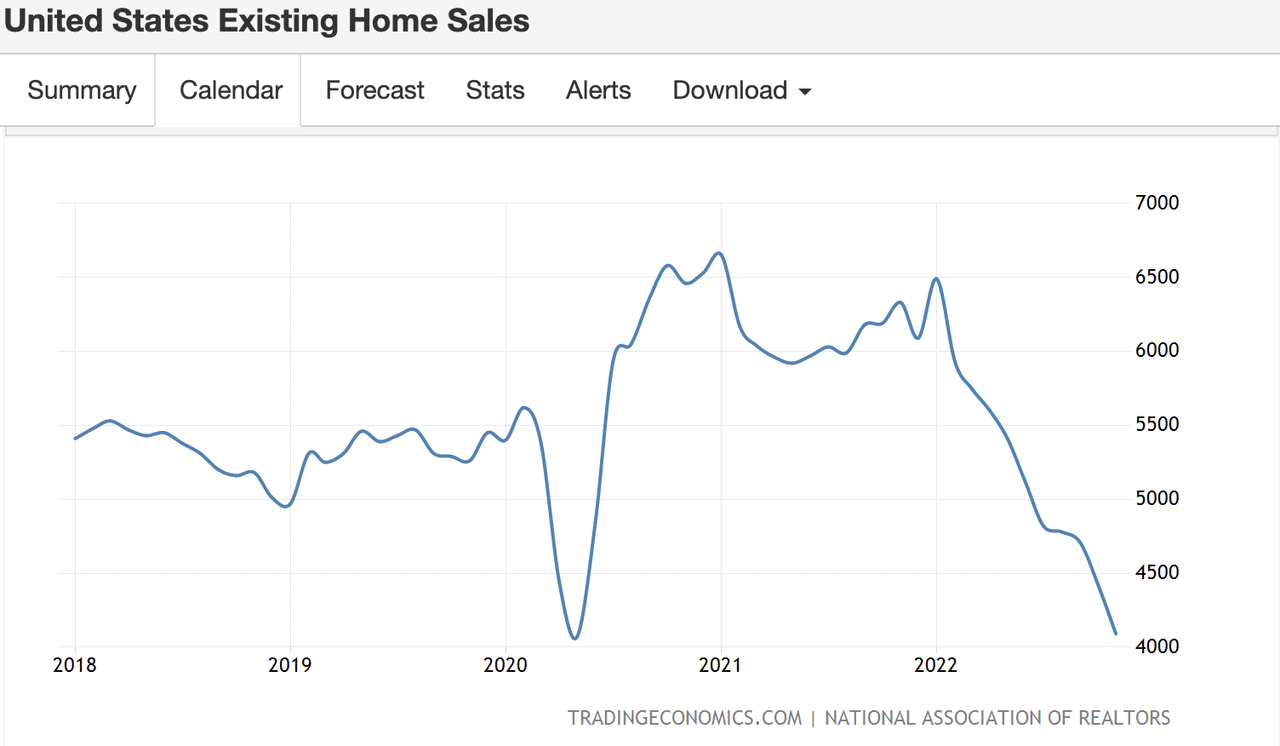

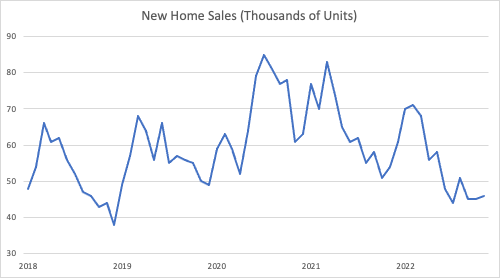

These factors have weakened housing demand, as both existing home sales and new homes sold are near 2020 peak-pandemic lows.

Tradingeconomics.com Census.gov

The final macro outlook is the threat of a recession. According to a Bloomberg article, a study was conducted in which 38 economists put a 70% chance of a recession in 2023. The widely tracked yield curve has also become completely inverted, and an inversion has preceded the last 8 recessions.

These indicators suggest that a recession this year is likely, which will cause the homebuilding industry to suffer in the near term.

Industry Long Term Outlook (Tailwinds)

Although the short term is negative for homebuilders, the long term is positive due to one main tailwind; a housing shortage in the US. Freddie Mac’s research indicates that the US has a housing supply deficit of 3.8 million homes. The shortage has been growing, as they calculate the shortage to be 2.5 million homes in 2018 (52% in 4 years). This is another factor in housing prices booming over the last 2 years. Not only were the macro factors promoting home sales and increasing demand during the pandemic (low interest rates and COVID stimulus checks), but the supply is lower than necessary, pushing up prices.

Freddie Mac also noted that millennials are now the largest segment of the US population and are at the peak age for first time home buying, which should hold housing demand high for the longer term.

These factors should be a positive tailwind for the homebuilding industry in the longer term.

DHI Background

D.R. Horton has been the top homebuilder in the US in terms of units for many years and has been the largest by top-line revenue for the last couple of years. The company is well positioned to take advantage of the long-term tailwinds in the industry as they dominate the Top 50 cities in the US, builds average homes, and benefits from economies of scale.

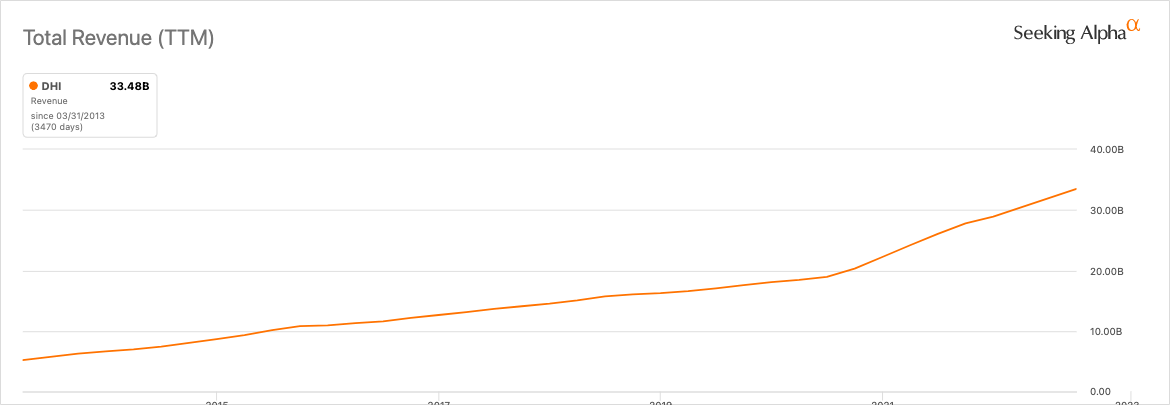

Seeking Alpha

As shown in the graph above, D.R. Horton has created tremendous growth since the end of the Great Recession. The company has done this by scooping up the market share given up by companies that went bankrupt after the Great Recession, and by strategically focusing its efforts on expanding in the Top 50 cities in the US.

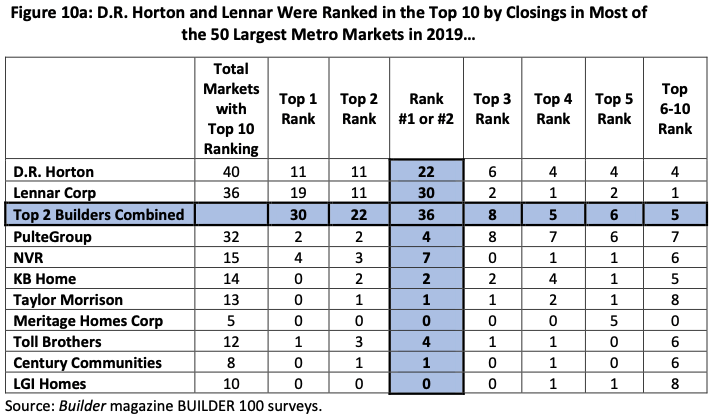

The graphic below shows how dominant DHI has been in these cities, as in 2019, the company was in the top 10 in 40 of the 50 largest markets. And they were #1 or #2 in 22 of 50.

Joint Center for Housing Studies of Harvard

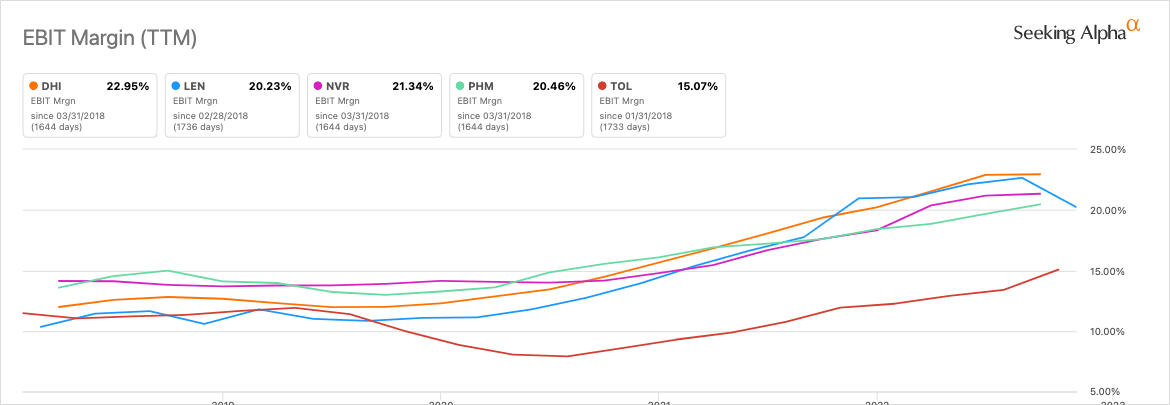

DHI sells average-sized homes, and many of them, as the company is the #1 seller of homes by total units in the US. Due to the large volume and their company’s size, they have been able to leverage economies of scale which has given them slightly higher margins than the industry average.

Seeking Alpha

DHI Outlook

The current outlook for DHI is similar to the industry as a whole. As a company in an industry that is very competitive and decentralized, there are not many competitive advantages that can be gained or leveraged.

One positive about the company is its very solid balance sheet, with nearly $2.5 billion in cash and a debt-to-equity ratio of 0.3. The company also is BBB rated, further indicating its financial strength (Although a BBB rating is not normally shown as an incredible strength, this is one of the highest ratings in the industry).

Top of the Cycle

DHI is currently trading with a P/E ratio of just over 6 which makes it appear to be a value stock. But as the company is in a cyclical business, the stock is closer to a value trap than a value stock.

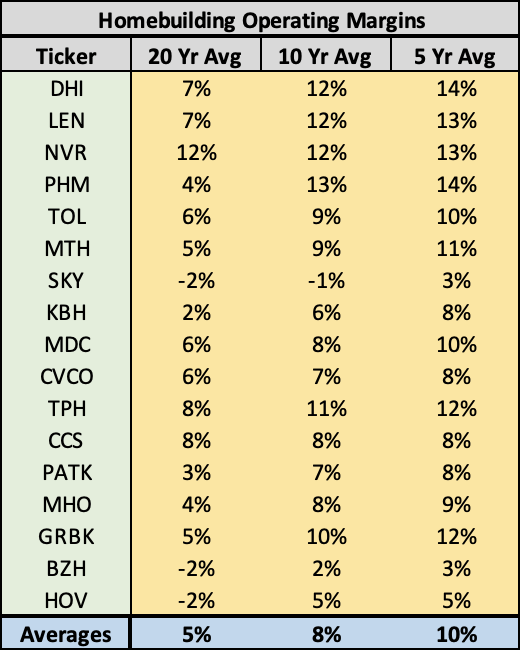

As written in the beginning of this article, all indicators suggest that the US economy is near the top of the business cycle, and macroeconomists believe that a recession is coming in 2023. This information leads me to believe that DHI’s current operating margins of ~23% are unsustainable. To test this theory, I compiled data from every current publicly traded company in this industry which has been operating for more than 20 years.

Author Created from SEC Filings

As is shown, the industry average has increased steadily over time and has generally operated much lower than DHI’s current margins. Bullish analysts of DHI may suggest that the increase in their margins is due to the company creating great efficiencies through economies of scale.

Although DHI has historically operated with slightly higher margins than the industry, this data suggests that it’s more likely that the industry as a whole has performed well in the last 10 years rather than DHI having created tremendous economies of scale or any type of competitive advantage.

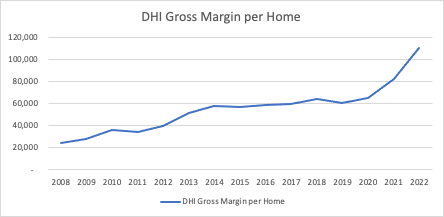

Further analysis of a comparison between home prices and costs of production shows a similar story.

Author Created from SEC EDGAR Financial Statements

As shown in the chart above, DHI’s gross margin per home has risen rapidly in the last 2 years. Historically, DHI’s gross margin has held near 20% but has now grown to almost 30%. This shows that prices have significantly outpaced the costs associated with building homes, creating abnormally high profits and operating margins. As interest rates increase and home buying slows, I would expect gross margins and operating margins to regress back to the historical mean of 20% and 12%, respectively.

Valuation

Story

Let’s summarize the DHI story as I have told it above and bring in the numbers to get value for the business.

DHI is a homebuilder which is facing some macro headwinds (High interest rates, high home prices, and a possible recession). These factors will decrease demand and will lead to poor performance for the current year. When these macro headwinds subside, the company will benefit from the macro tailwind of a housing shortage. DHI will continue to be one of the leading companies in the industry and benefit in the form of revenue growth. But seeing that the industry is highly competitive and capital intensive, DHI will only have moderate growth. DHI will also see its operating margins shrink due to the cyclical nature of the business and competition.

Numbers

Based on this story, I have built a 10 year DCF model, with the major inputs being as follows.

-

DHI’s revenue will decline 5% next year, increase by 5% each year in years 2-5, and level off to 3%.

-

I have fixed operating margins at 12% (DHI’s average from 2008 until today).

Author’s Work

Using all those inputs, I get a value for DHI at $97.94/share. As the company is trading near this price, I believe that the stock is fairly valued.

Risks

- Macro Risk

The homebuilding industry is cyclical and heavily influenced by macroeconomic factors. Any major change this the macro environment could impact DHI significantly.

2. Valuation Main Assumptions

My research indicates that the homebuilding industry will grow in the long run. But if this does not come to fruition, my valuation will be inaccurate and will need to be revised.

3. Market Share

DHI could lose market share due to the high level of competition in the industry. This could lead to lower growth rates or total revenues for the company.

4. Operating Margins

I built in the DHI’s operating margins at their 10-year historical average. But it is possible that DHI actually has more or less competitive advantages than I have perceived, which would change the margins that the company would be able to obtain.

Conclusion

DHI has built a great business and has created significant growth over the last 10 years due to its strategy of focusing on operations in the Top 50 cities in the US. But as the economy is near the top of the business cycle, DHI’s margins will shrink even with growth from a housing shortage tailwind.

DHI’s current PE ratio of 6 indicates value. But as much value as this indicator suggests, my research shows that the market got this one right. I’m placing a hold rating on the stock.

Be the first to comment