demaerre

CuriosityStream (NASDAQ:CURI) is a micro-cap company in the highly competitive streaming content industry. There are a variety of factors that make CURI one of the more interesting plays in the space compared to streaming peers in my view. For instance, CuriosityStream has a very niche offering as it is completely focused on growing and distributing a library of informative, non-fiction documentary-style content.

While the platform lacks the variety that consumers can get on more popular applications offered by Netflix (NFLX) or Disney (DIS), it does have one of the more competitive prices that I can recall seeing in sVOD with a $30 annual commitment – this represents a 50% mark down from the $4.99 monthly subscription for the HD package tier. This approach has helped CURI create a single digit churn rate as 85% of the company’s direct to consumer subscriber base is on the annual plan.

Public via SPAC

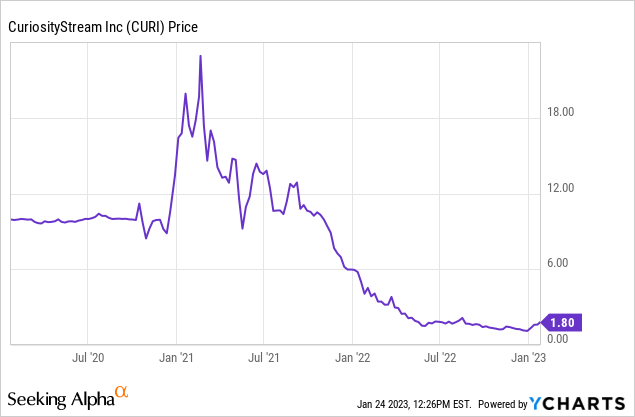

There isn’t much trading history for CuriosityStream as the company went public during the SPAC craze from 2020 and 2021. Shortly following CuriosityStream’s SPAC closure, the stock was caught up in a speculative hype that saw an enormous rally in many tech stocks at the time. At one point in early 2021, CURI shares traded as high as $24 dollars.

From February 2021 to January 2023, the peak to trough selloff has been an astounding 95.4%. Since the $1.10 low earlier this month, the stock has since rallied up to $1.95 as of article submission.

Revenue and Key Metrics

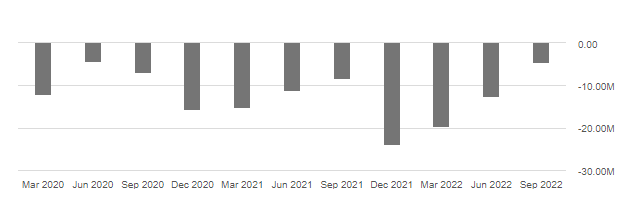

Since CuriosityStream is one of the more niche streaming offerings, it’s unlikely to ever scale to the degree that a platform like Netflix has scaled to but that doesn’t mean the company can’t still operate a much smaller but potentially profitable business. During the last earnings call in November, the company reported $23.6 million in revenue, $10 million in gross profit, and a $4.4 million operating loss.

CURI Operating Income (Seeking Alpha)

Even though the company isn’t currently profitable, CuriosityStream has noticeably improved operating loss in three consecutive quarters having decreased the operating loss from $23.5 million in Q4-21 to $4.4 million in Q3-22. A big part of this improvement in the company’s performance is attributable to less spend on expenses like marketing and administration. From the last quarterly call, CEO Clint Stinchcomb:

When we told you last quarter we would continue to take a hard look at all of our spending for marketing the content to G&A in order to reduce our cost base and improve our overall economics. These efforts drove a greater than $7 million reduction in noncore operating expenses between the second and third quarters.

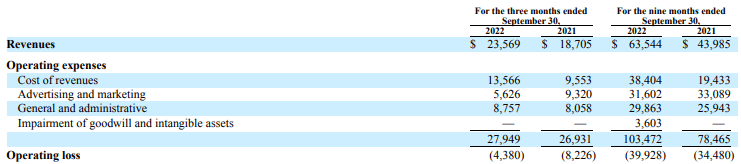

Per CuriosityStream’s last 10-Q, the reduction in advertising in the last quarter was $3.7 million year over year from $9.3 million down to $5.6 million:

CURI Earnings (Q3-22 Filing)

As I noted earlier, the operating loss improved considerably in Q3 but it should be noted the company’s operating loss for the nine months ended September 30th was still roughly 15% higher in 2022 compared to 2021. From a revenue perspective, the company has grown 44% year to date from $44 million to $63.5 million.

CURI Earnings (Q3-22 Filing)

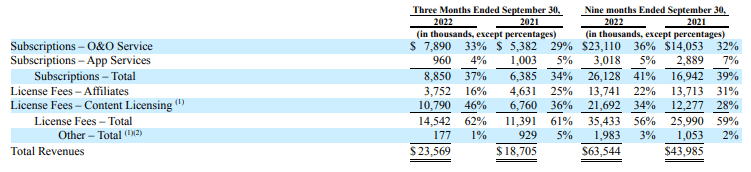

One thing that I think is worth pointing out is only 41% of CuriosityStream’s year to date revenue has come from subscriptions. 56% of the total revenue comes from licensing fees. I think this is notable because it shows a willingness to monetize the company’s owned content in ways that aren’t just limited to direct to consumer products.

Valuation Comparison

Another streaming name that I know fairly well is Chicken Soup for the Soul Entertainment (CSSE)(CSSEP). Even though CURI has an sVOD approach and CSSE has an aVOD approach, they’re both providing streaming products that offer economic alternatives at the consumer end. I think this is important in a streaming subscription landscape that has quickly become very saturated.

From an investment perspective, they’re both micro-cap growth ideas that I’d classify as closer to streaming ‘pure plays’ since so many other media companies with popular streaming platforms are still highly reliant on cable or traditional broadcast networks as revenue sources; Disney possibly being the biggest example. Based on price to book and enterprise value to sales, CURI has the more attractive valuation between the two.

| Trailing Twelve Months | CURI | CSSE |

|---|---|---|

| Price/Sales | 1.09 | 0.53 |

| EV/Sales | 0.44 | 3.25 |

| Price to Book | 0.76 | 0.96 |

Source: Seeking Alpha

While CSSE has faster revenue growth, it has done so through acquisitions and the recent purchase of Red Box has added a debt load to CSSE’s balance sheet that CURI simply doesn’t have:

| CURI | CSSE | |

|---|---|---|

| Total Cash | $63,773,000 | $32,203,799 |

| Total Cash Per Share | $0.89 | $1.54 |

| Total Debt | $4,735,000 | $482,941,984 |

| Net Debt | -$59,038,000 | $450,738,179 |

| Total Debt to Equity | 3.63% | 385.43% |

Source: Seeking Alpha

With just a 3.6% debt to equity position and $63.7 million in cash and investments, CURI is in a much better financial situation than many of the micro-cap growth media stocks. If the company can continue cutting costs and growing subscribers through what is likely an impending recession, I think CURI has one of the better risk/reward setups in the communications sector.

Risks

At this point, I think the biggest risk to CuriosityStream is that management could simply fail to execute the profitability plan. On the last call Stinchcomb said the company would “leave no stone unturned” to create cost efficiencies but to this point, CuriosityStream is still a company that is burning money to grow. Guidance for fourth quarter was not terribly enthusiastic as CFO Peter Westley indicated the final quarter of 2022 wouldn’t produce the kind of revenue growth that may have been expected from previous years:

we’re seeing a wide range of potential outcomes for the quarter and we do not anticipate the kind of Q4 sequential revenue growth that we’ve experienced in the past

He went on to say $2.6 million of Q4 revenue from last year came from a licensing deal that the company did not renew. Noting the unpredictability of the current economic environment, Westley did guide for at least $50 million in cash and investments to close 2022. If management can’t achieve profitability, CuriosityStream may ultimately need to raise cash. In that case, the company would either be taking on debt or CURI shareholders would have to deal with dilution down the line.

Summary

Streaming is a highly competitive space to be in and consumers are currently in the driver’s seat as they have numerous options and can take advantage of promotional offerings. The fight for eyeballs is intense and niche platforms like CuriosityStream may have a harder time scaling than the more well-known platforms that offer a wider variety of content. All that said, I think CuriosityStream has a pretty favorable risk/reward setup down here.

The company seems to be a very low bankruptcy risk and has a low churn rate. In in the event of a recession, the lower tier bundle is so attractively priced at just $30 for a full year, I don’t believe CuriosityStream’s product offering is the first that gets cut in any theoretical household budget belt-tightening at the consumer level. As I said earlier in the note, CURI may never become an industry leader based on raw subscriber numbers. But the company has low-cost, evergreen content a stock price that is probably too cheap at $1.86.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment