The Jacksonville-FL, based CSX Corporation (NASDAQ:CSX) is the last American Class I railroad to release its fourth-quarter earnings. Going into these earnings, a few things were crystal clear: the pressure on shipment volumes is rising, and operating expenses are still an issue. It’s a toxic mix that hurt both Union Pacific (UNP) and Norfolk Southern (NSC) this week. The good news is that CSX beat both revenue and EPS estimates. Unfortunately, the operating ratio increased due to outperforming expenses. The good news is that despite a poor outlook, operating challenges, and a high chance of more downside, I’m looking forward to buying more railroad exposure on weakness. As I often say, dividend growth investors in cyclical stocks like CSX should embrace situations like these. After all, that’s when most of the money is made.

Hence, we’ll also look into the many qualities that make CSX a top-tier stock that will (likely) end up generating above average returns the moment demand expectations bottom.

So, let’s get to it!

Why Don’t I Own CSX

I cover CSX a lot, yet I don’t own it. The reason I don’t own CSX is my already large industrial and railroad exposure. I have close to 50% industrial exposure in my dividend growth portfolio. This exposure consists of three railroad stocks. I own Union Pacific because of its “high” yield and exposure in the Western part of the United States. I own Norfolk Southern because of its intermodal exposure and footprint in the East (it’s CSX’s largest competitor), and I own Canadian Pacific (CP) due to its fast-growing business and high likelihood of connecting Canada, the US, and Mexico after the KSU merger.

In other words, I do have exposure in CSX’s territory, I do have railroad exposure with high dividend growth and a low yield, and I do have exposure in coal and related.

So, while I don’t own CSX, I do not prefer any of the stocks I own over CSX. In other words, it’s not a worse pick.

What Happened In 4Q? And Why Does It Matter?

If you have read my other railroad articles this week, you know what I’m going to say next. There are at least two good reasons to follow CSX news, even if one does not have CSX exposure.

It’s always good to know what CSX is up to, as it is one of the best and most consistent dividend growth outperformers on the market.

CSX is America’s second-largest railroad. Its comments and numbers tell us a lot about the state of the US economy and its many supply chains.

CSX Corp. (The Pan Am network in New England is excluded)

With that said, my expectations were very low. Both Union Pacific and Norfolk Southern reported poor numbers, as we’re simply in a very unfavorable environment for railroads. Economic growth is slowing, hurting freight demand, inflation remains high, and higher investments are needed to improve network fluidity. After all, due to the pandemic, railroads had to bring back a lot of equipment and employees to deal with rebounding demand. Now, they are dealing with the rebound in demand, and a high likelihood of falling shipments in the future, due to cyclical weakness.

This is the kind of environment where railroads can prove how well they can deal with challenges.

Shipments, Pricing, And RPU

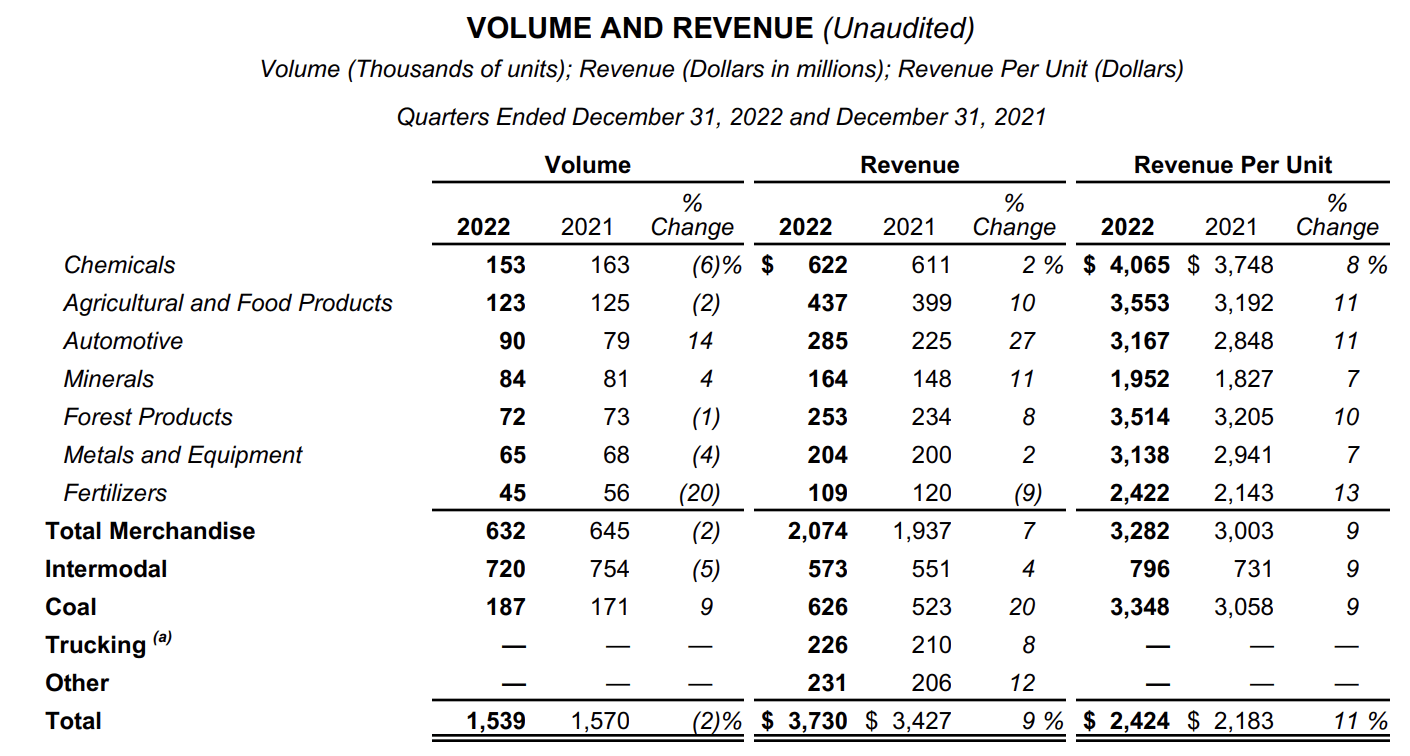

As usual, we start at the very top. In 4Q22, CSX shipped 1.5 million units (intermodal, cars, hoppers, you name it). That’s 2% less compared to 4Q21 as a result of weakness in chemicals, agriculture, forest products, metals, and fertilizers.

CSX Corp.

The company spent surprisingly little time discussing these developments. In its earnings call, nobody mentioned fertilizers, agriculture, or agriculture.

However, that’s fine, as one doesn’t need a Ph.D. to figure out what happened here. Especially not because CSX follows the economic trend quite well.

Chemicals are weak as a result of plummeting economic activity. The same goes for metals and equipment. Forest products were weak due to a soft housing market. Intermodal was weak due to weak consumer sentiment and de-stocking efforts on a retail level. Also, the trucking market has become very soft, which means that highway competition has increased.

I’m sure that agriculture is down due to droughts. Fertilizers are just a minor segment. CSX is the main railroad of its Florida peer Mosaic (MOS), which is one of the world’s largest potash producers. If anything, this seems to be a timing issue instead of a cyclical decline. Given my intel in the industry, this segment should see a meaningful rebound in the first half of this year.

With that said, the stars of the quarter were coal and automotive. Coal benefited from low inventories and high export demand. Plant closures were more than offset by higher demand in other areas. Automotive demand came back due to easing supply chain bottlenecks. Car producers are finally able to turn their backlog into finished products.

When incorporating pricing, CSX turned 2% fewer shipments into 9% higher revenue. Only the fertilizer segment failed to grow revenues. Automotive revenue improved by 27%. Coal was up 20%.

As this example shows, railroads are great at using pricing to their advantage. That’s important as everyone knows that long-term growth in total shipments is slow. Total shipments are tied to real economic output. Outperforming pricing gains are where the magic happens, so to speak. Well, that and higher operating efficiencies, which I will get to in a moment.

For now, it is important to mention that CSX remains in a terrific spot when it comes to pricing. According to President/CEO Joe Hinrichs:

[…] the pricing environment remains favorable for us. Our customers have experienced substantial inflation and understand that we face our own cost pressures, including the effects of the recent labor agreements. This transparency has helped us as we renew our pricing agreements, which will support our top line performance.

Moreover, a favorable mix caused revenue per unit to rise by 11%. In that case, even fertilizers contributed to these gains.

So far, I’m very happy with what I see.

Unfortunately, this was just a small part of the big picture.

Cost Pressures (Somewhat) Ruin The Quarter

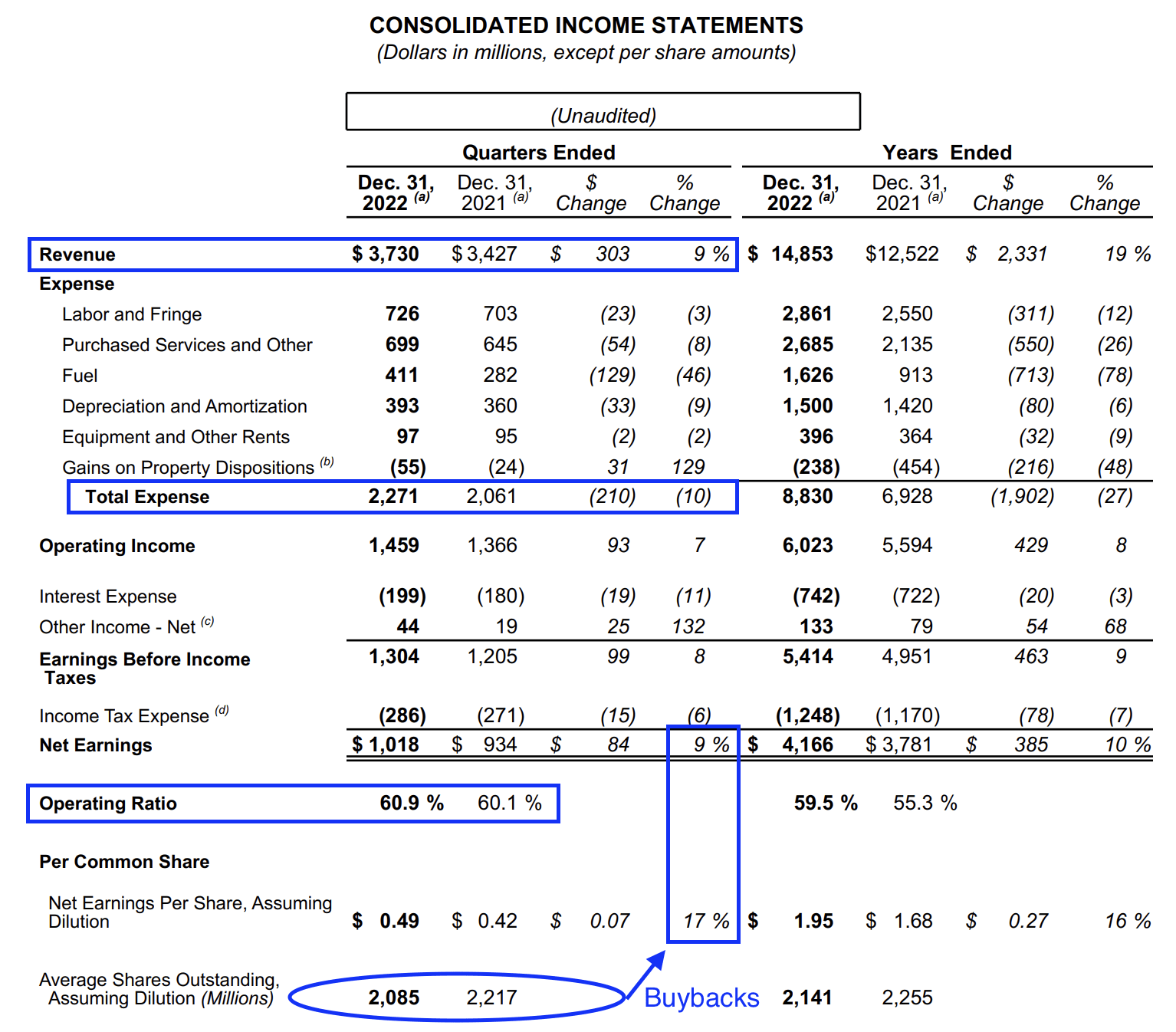

This part was going to be the bottleneck of the earnings release, as railroads have been struggling with high costs for at least a few quarters. As the overview below shows, the company had 9% higher revenues. Unfortunately, total expenses rose by 10%.

First of all, I am positively surprised. Expenses are outperforming by just 100 basis points, which is a good result given the circumstances. Moreover, the only segment that outperformed revenue growth was fuel (+46%). Labor costs were up due to wage inflation and a higher headcount. Again, I’m glad to see that CSX managed to keep the increase to 3%. That’s impressive.

CSX Corp. (Author Annotations)

Unfortunately, it still didn’t keep the operating ratio from rising to 60.9%.

On a full-year basis, the OR is 59.5%.

I like that number. While it is high and a move in the wrong direction (the lower, the better), it needs to be said that the acquisition of Quality Carriers (a trucking company) in 2021 added 250 basis points to the OR. Bear in mind that trucking companies are nowhere near as efficient as railroads. Adjusted for that number, the OR would have been close to 57.5%, which is a terrific number.

Related to this, we need to discuss rapidly improving operating efficiencies, positively impacting network fluidity.

The Railroad Is Back On Track

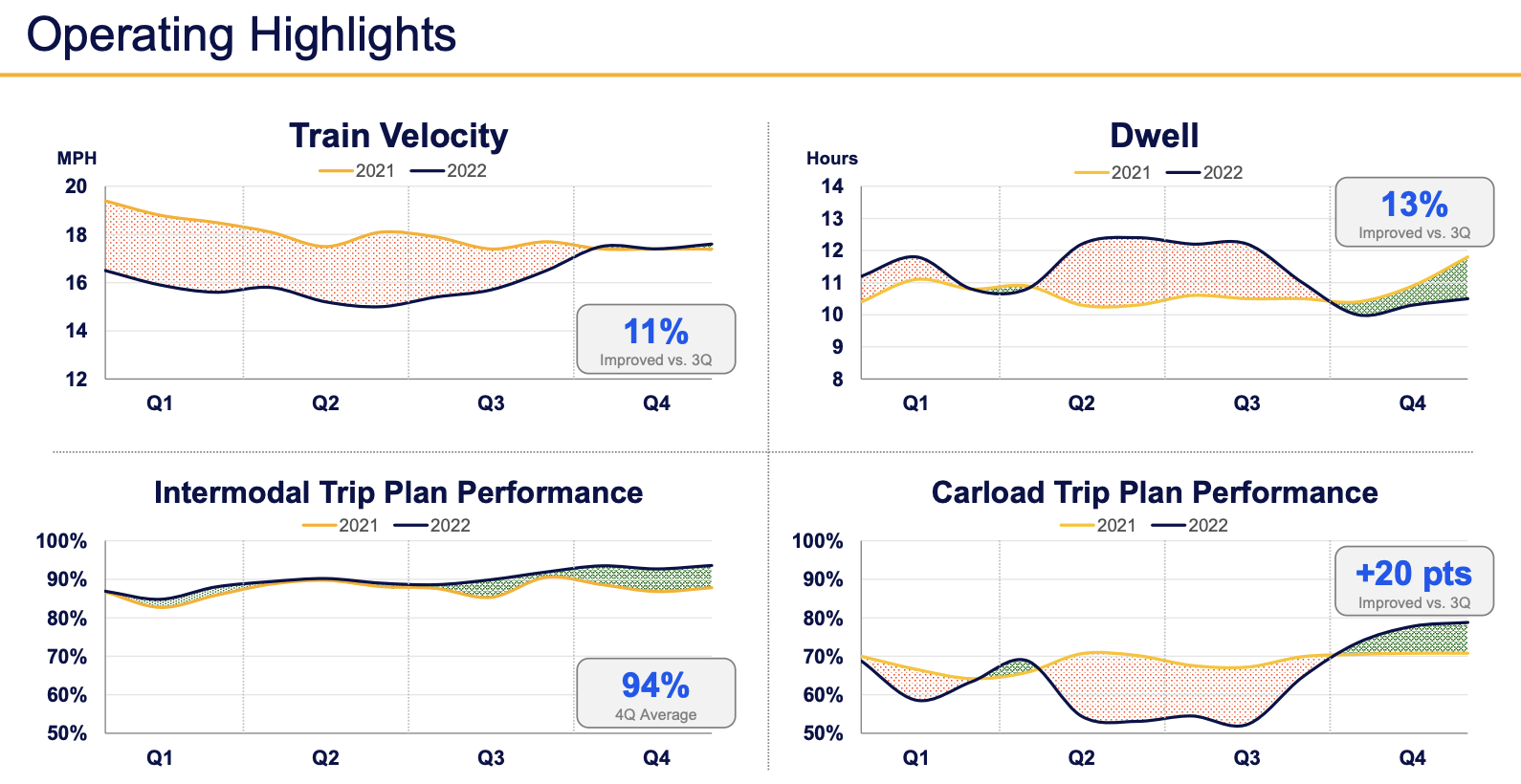

In light of the aforementioned post-pandemic operating difficulties, I’m glad to report that CSX is seeing tremendous operating improvements.

Despite weather-related headwinds, the company improved train velocity by 11% (sequentially), improved dwell time by 13%, and it saw higher intermodal trip plan performance. Carload trip plan performance rose by 20 points.

CSX Corp.

Even more important, the railroad is about to see pre-pandemic levels in network fluidity.

This progress has not stopped as we crossed into 2023 with our service metrics continuing to trend towards pre-pandemic high water levels of late 2019 and early 2020. Our team is focused on improving network fluidity and delivering a consistent, reliable service that will encourage our customers to shift business onto our network, and the data shows that we are well on our way.

Hiring is also going smoothly. The company ended the year with roughly 6,900 active train and engine employees. That’s up from 6,400 in 4Q21. It has 780 employees in training (up from 436), and it promoted close to 370 new conductors in the fourth quarter.

It also helps that the ONE CSX concept is bearing fruit.

CSX has been tremendously successful over the last several years as the Company has undergone its transformation. In my view, we’ve done particularly well across the first three of these scale railroading principles. The opportunity for us now is to focus on getting to even better balance with those last two. We will redouble our efforts in serving our customers and ensuring that our employees, the people who are delivering that service to our customers, feel valued, appreciated, and included. To address this and bring out the best of this operating model can deliver, we are building a ONE CSX culture that prioritizes our relationships and leverages our common goals.

Cash Flows, Dividends, And Buybacks

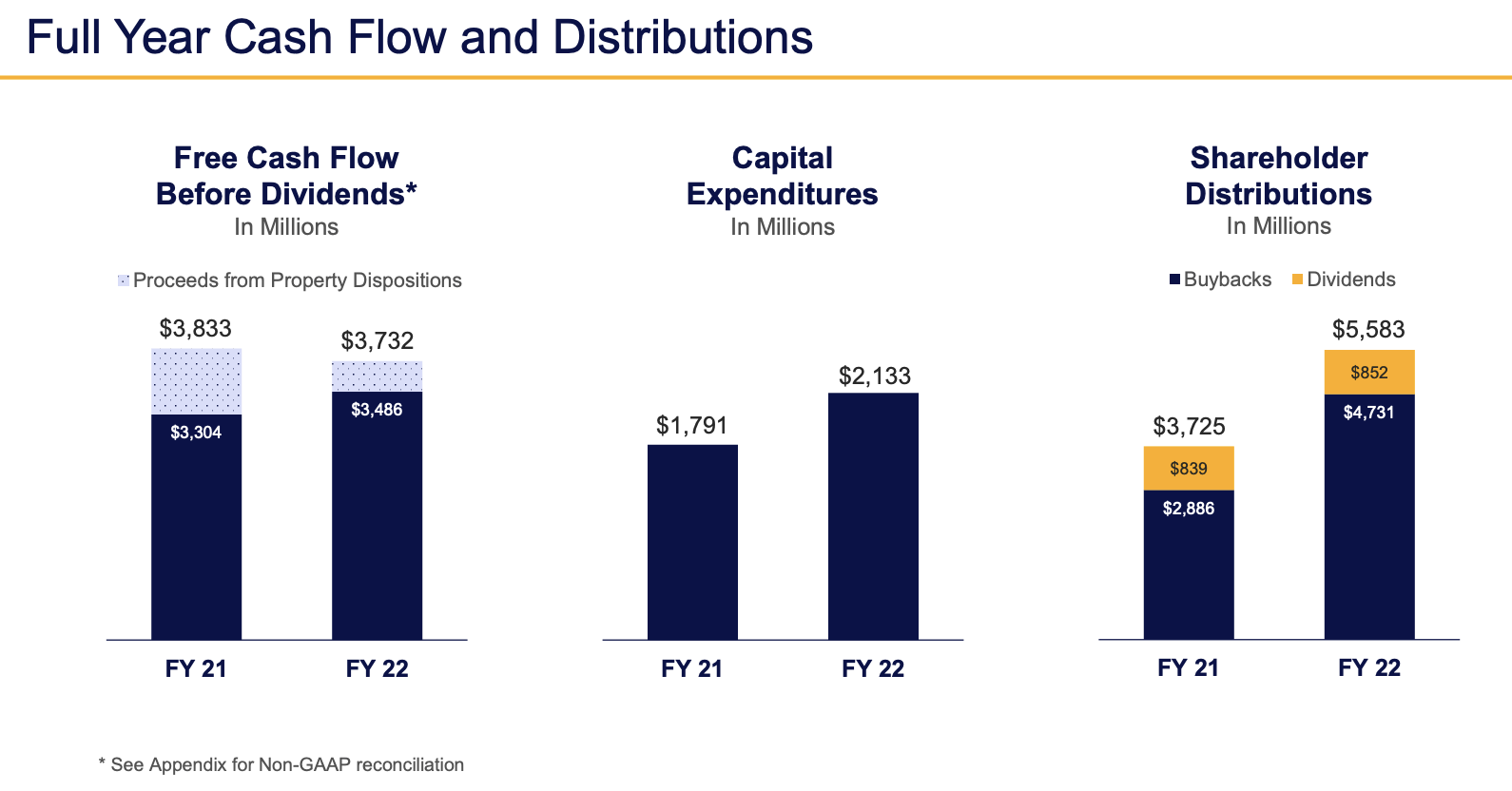

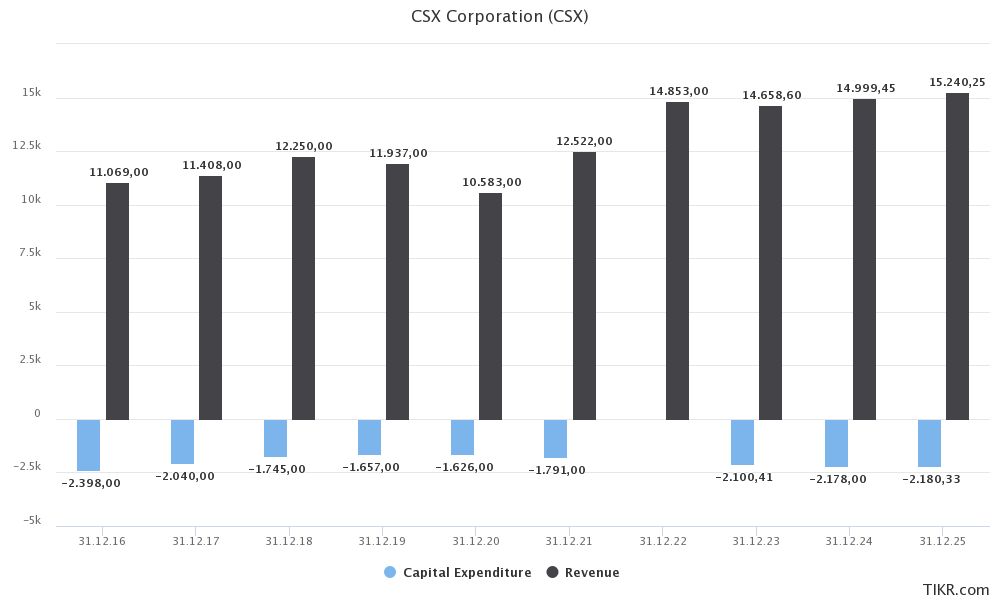

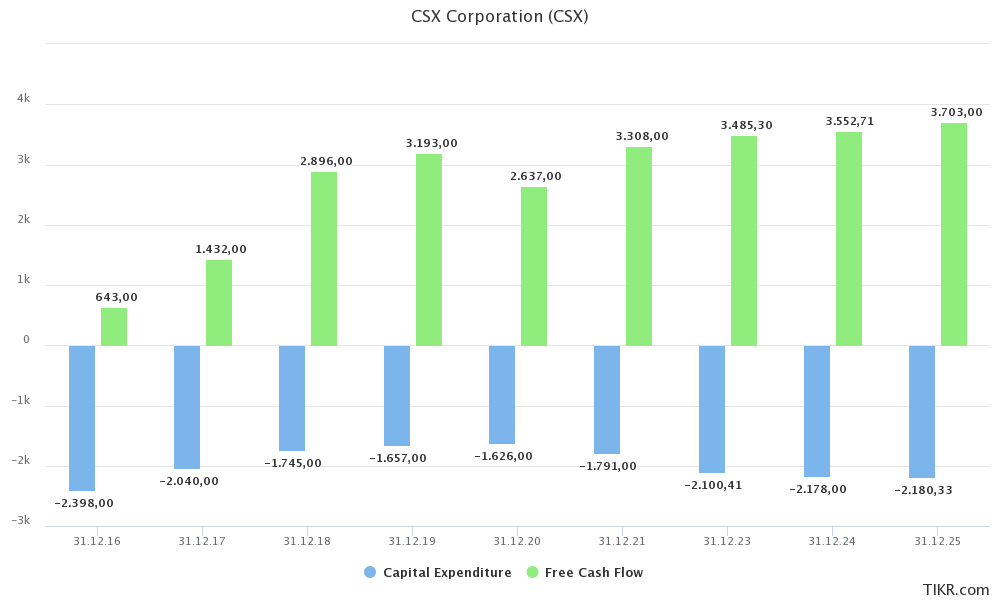

In 2022, CSX generated $3.7 billion in free cash flow. Adjusted for the sale of property, that number is $3.4 billion. Last year, free cash flow was $3.3 billion. CapEx increased to $2.1 billion (from $1.8 billion), which is 14% of total revenue. The surge in CapEx is the result of higher inflation, material requirements, and the acquisitions of Quality Carriers and the Pan Am railroad.

The company boosted shareholder distributions to $5.6 billion, which mainly consisted of buybacks.

CSX Corp.

These massive buybacks are also the reason why the company turned 9% net income growth into 17% earnings per share growth, which I highlighted in one of the tables in this article.

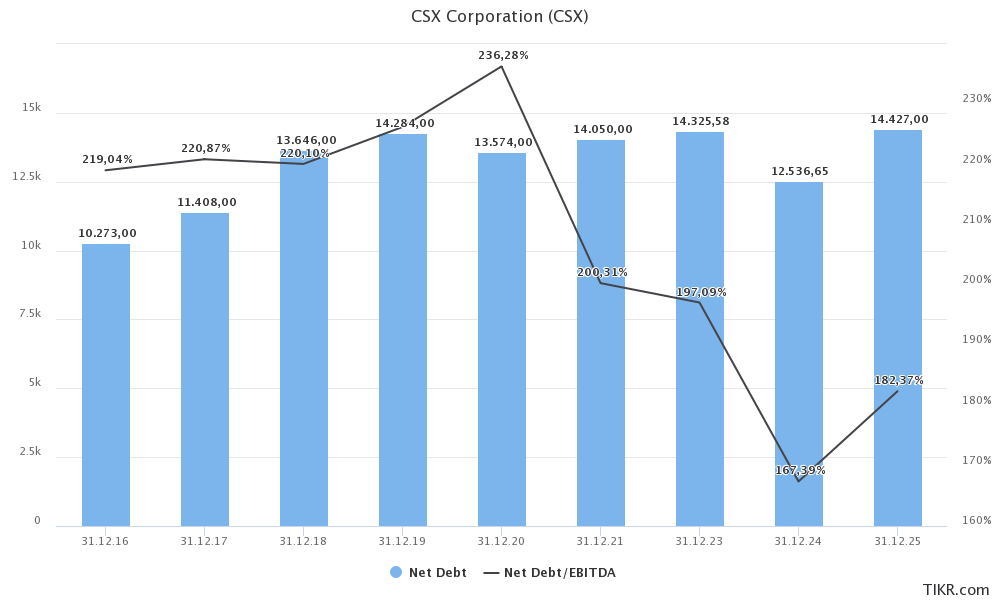

Moreover, while CSX spent more on buybacks and dividends than it generated in free cash flow, it continues to maintain a healthy balance sheet. Net debt ended the year at $14.0 billion, which is 2.0x EBITDA. The company has a BBB+ credit rating with an A2 short-term credit rating.

TIKR.com

So far, so good. Now, what?

Outlook – A Mild Recession?

Railroads have become extremely careful when it comes to telling the world what to expect going into 2023. Railroads aren’t giving volume targets, they are not issuing operating ratio targets, and analyst questions regarding the outlook are somewhat ignored.

I cannot blame them, as the economic environment is highly unpredictable. If I were CSX, I also wouldn’t try to fit slowing economic growth, persistent inflation, geopolitical issues, secular business trends, and an aggressive Fed into a detailed outlook.

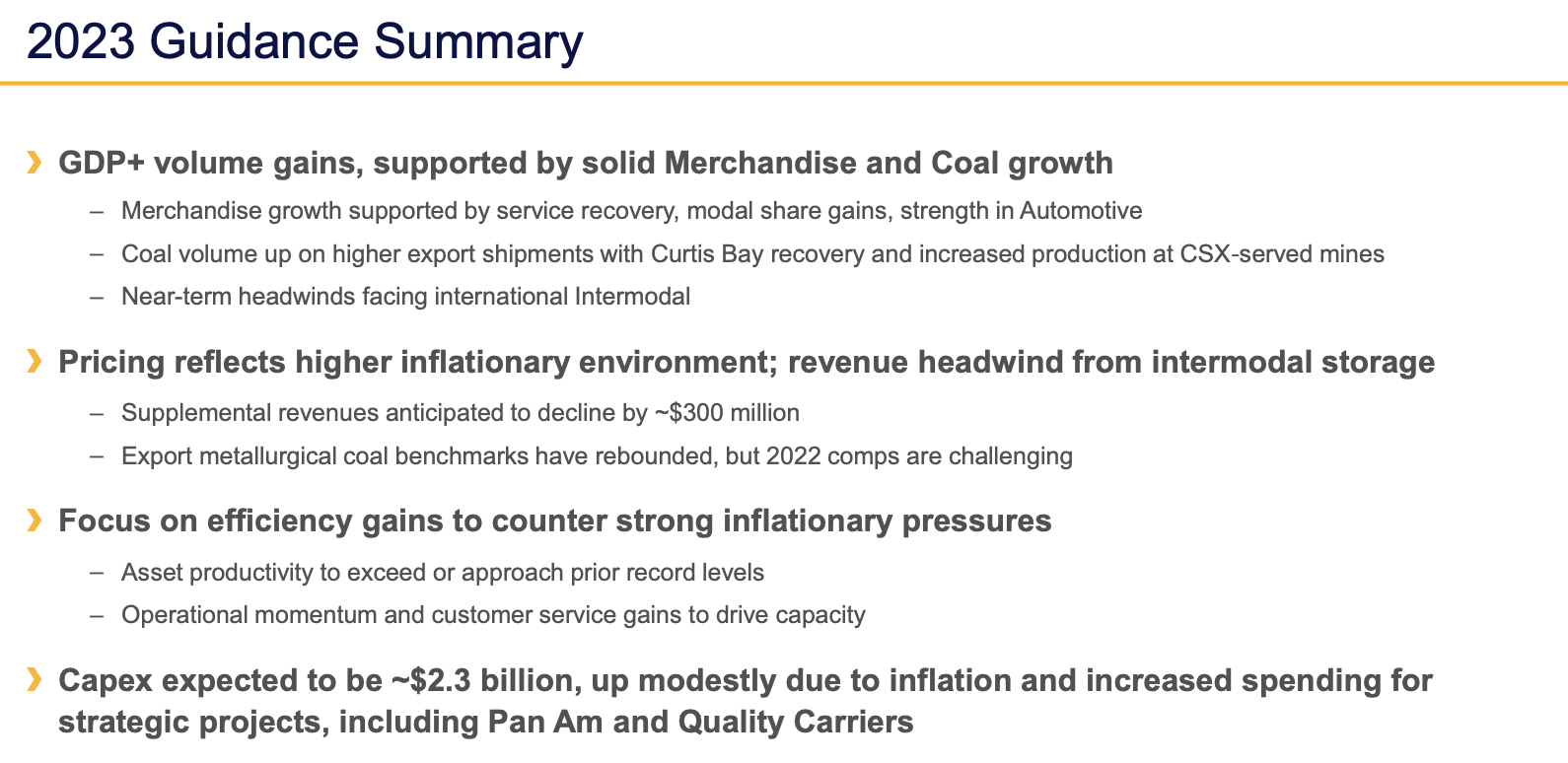

That said, there’s something we can work with. For starters, the company expects that its volumes will outperform GDP growth, supported by solid merchandise and coal. As the sheet below shows, this is based on the service recovery, modal share gains, and automotive strength. Coal should see the benefits of the Curtis Bay recovery. Curtis Bay is a massive coal export facility in Baltimore-MD.

CSX Corp.

According to the company:

[…] we do believe that international intermodal volume is likely to be soft, particularly over the first half of the year, as imports have slowed and retailer inventory levels have recovered.

[…] we will face cost pressures in 2023, but we know that we can get better operationally.

[…] In the end, our margin performance will largely depend on our success in driving more volume through our network and realizing potential operating leverage.

When looking at analyst estimates, we see that expectations were that CapEx would be $2.2 billion in 2023. The new $2.3 billion number implies a CapEx/revenue ratio of 15.3%, which is slightly higher than I would like it to be. However, it’s due to the aforementioned acquisitions. Moreover, that ratio is coming down again, so no worries there.

TIKR.com

Moreover, analysts expect free cash flow to remain strong. While growth rates are expected to drop, we shouldn’t expect a decline in free cash flow – according to these numbers. Moreover, using 2024E free cash flow of $3.6 billion, we’re dealing with an implied free cash flow yield of 5.5%. That’s a good number.

TIKR.com

Unfortunately, I’m not a big fan of a moderate outlook.

The Macro Outlook

While CSX did not mention it, a lot of railroad outlooks are based on a soft-landing scenario. Using Wells Fargo numbers, the consensus seems to be a mild recession in the last two quarters of 2023, which could lower full-year GDP growth to 0.5%.

Wells Fargo

I am not a big fan of this soft-landing approach, as I wrote in prior articles.

I’m assuming that a soft landing will be hard to achieve. I don’t see how the Fed can reduce inflation to 2% and keep it at 2% without hurting economic demand. After all, the only way to get sticky inflation down is to do some serious damage.

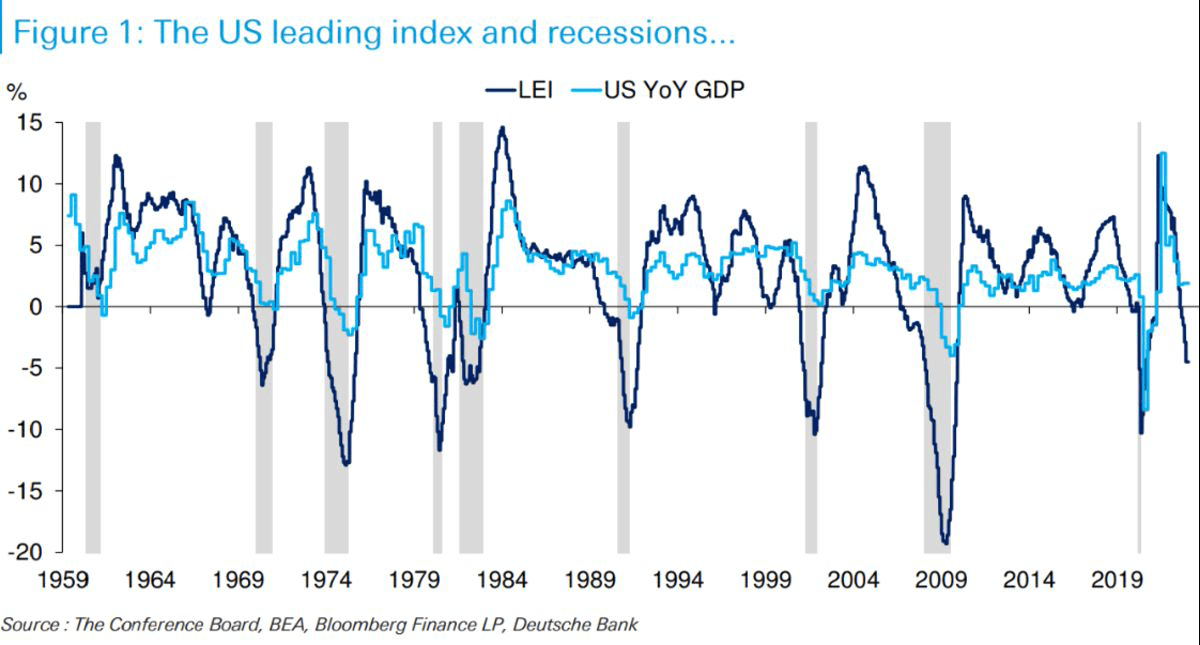

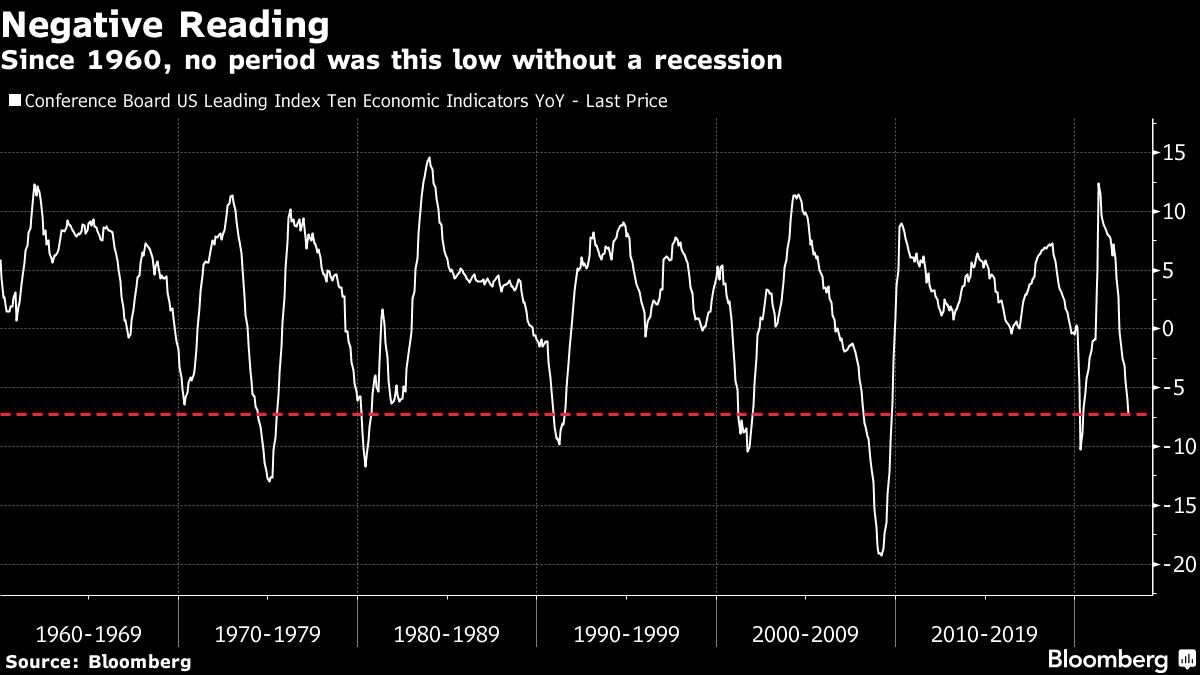

For now, leading indicators like the Conference Board’s LEI indicate a very high likelihood of a recession.

All the points below the dashed red lines were moments of extreme distress for the US: the Yom Kippur War and the oil embargo in the early 1970s, Iran–Iraq war in 1980, Gulf War in 1990-91, dot-com bubble in 2000, the Great Financial Crisis and then Covid-19. Those aside, December’s reading was weaker than more than 92% of all data-points since 1960, Bespoke noted. This may be a lagging indicator, but it doesn’t lag by all that much, and it seems dangerous to ignore it or try to explain it away.

Bloomberg

Hence, I believe a scenario is likely where volumes experience more downside pressure than the company assumes. This will make it harder (impossible) to grow revenues.

Valuation

I’m zero percent worried when it comes to the impact of my economic thesis on railroads – or any of my other holdings.

If anything, I believe that weakness offers opportunities.

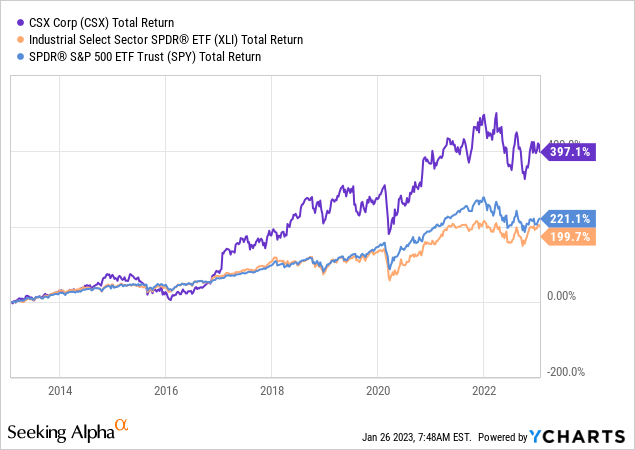

Over the past ten years, CSX has consistently outperformed both the market and the industrial sector.

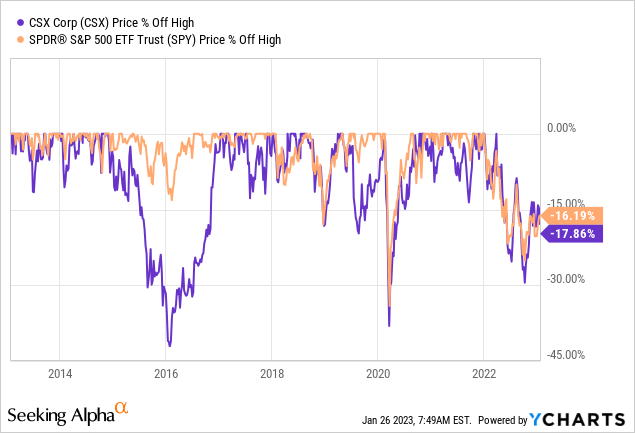

I don’t know how bad the current sell-off might get, but I expect that we could see another attempt to -30%, which implies a drop to the $25-$26 area.

My assumption comes with a risk. One major risk in the stock market is losing money. That one is obvious.

Another risk is missing long-term uptrends. After all, putting money to work is what it’s all about. And time in the market usually beats timing the market.

It also doesn’t help that CSX is attractively valued using current estimates.

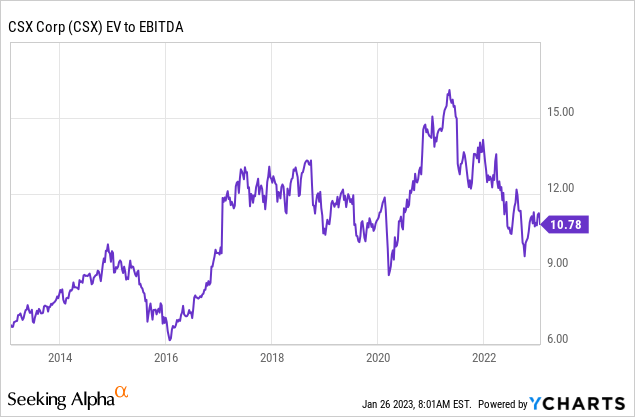

CSX is trading at 10.9x 2023E EBITDA, which is a very fair valuation.

If we were in an economic upswing, I would be buying railroads with both hands.

However, given the circumstances, I’m looking for a bit more weakness, as I believe that the outlook will be adjusted in the weeks ahead.

Takeaway

In this article, we discussed CSX’s 4Q22 earnings. The company did a good job in a tough environment. It grew revenue thanks to strong pricing, was able to keep expenses growth to 10%, and reported an operating ratio in the 60% range, despite two major acquisitions since 2021.

CSX is also restoring network fluidity at a rapid pace, which could see pre-pandemic levels in 2023.

However, the outlook remains highly uncertain, as economic developments are going in the wrong direction.

As much as I like CSX’s valuation, I think the stock is poised to drop a bit more in 2023, especially if the market starts to price in something worse than a soft landing.

I have no shorts and 90% of my net worth is invested in stocks. I believe that stocks like CSX are terrific buys on weakness. Investors who bought during prior recessions are in a very good spot. Hence, I’m embracing weakness.

Needless to say, feel free to disagree with my economic view. My goal is to discuss quarterly earnings and to give you my view on the economy, incorporating as many variables as possible.

I do not want to keep you from buying CSX. There’s a chance I’m wrong.

Don’t hesitate to use the comment section down below to share your view on recent developments. What’s your outlook? Do you agree with me?

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment