Justin Sullivan

What Happened?

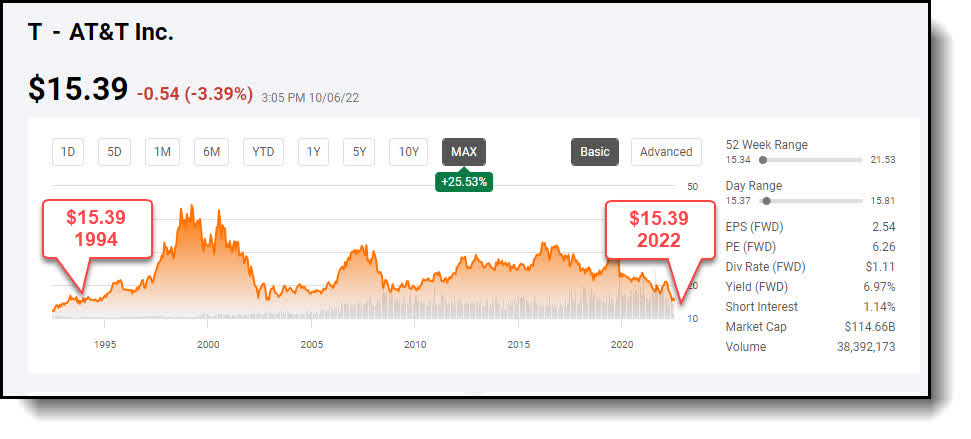

AT&T’s (NYSE:T) stock has fallen below $16 for the first time since 1994.

Current Long-term Chart

Seeking Alpha

The stock is down substantially in just the last quarter.

One Year Chart

Finviz

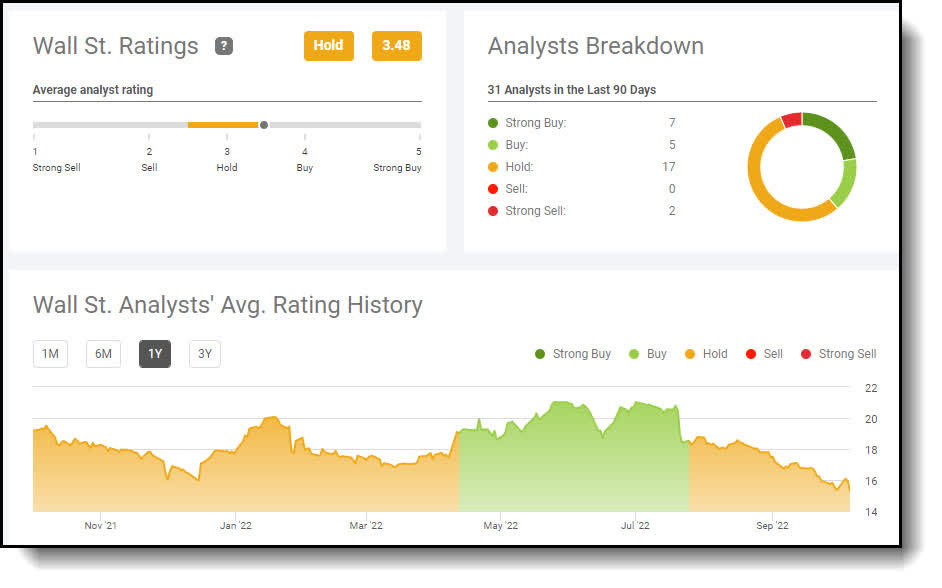

The stock has crashed 25% since reporting earnings last quarter. What’s more, many are still advocating current shareholders throw in the towel and sell out and prospective investors should avoid the stock. A majority of analysts have recently downgraded the stock and have a hold or sell rating at present.

Seeking Alpha

The funny thing is – I see this as a sign a major buying opportunity has presented itself. There’s definitely blood in the streets as far as AT&T’s stock is concerned. You have to ask yourself the question – are you playing chess or checkers? Let me explain.

Are you playing chess or checkers?

I see those selling out now as classic cases of first-level thinking. A first level thinker sells stocks as they fall and buys stocks when things are going well. The fact of the matter is in order to be truly successful, you have to do the exact opposite. Think of first-level thinking as checkers, second-level thinking as chess. Warren Buffett’s quote “Be fearful when others are greedy and greedy when others are fearful” is a classic example of second level thinking.

The contrarian’s code

Times of market turmoil often present the best buying opportunities for savvy dividend and income investors. Contrarians find their best investment opportunities during times of market duress while others are panic selling. Nonetheless, the underlying stock needs to have a solid growth story and strong fundamentals. AT&T fits the bill of the baby being thrown out with the bathwater. I see AT&T stock recovering next couple of years. Here’s why.

Why Now Is An Ideal Time To Buy AT&T

The following are the primary reasons I feel now may be an ideal time to start or increase your position in AT&T. The fact of the matter is, AT&T is actually growing at present. Furthermore, with a 7% yield to boot, the stock presents a fantastic buying opportunity for prospective dividend and income investors looking to lock in a superior and safe yield.

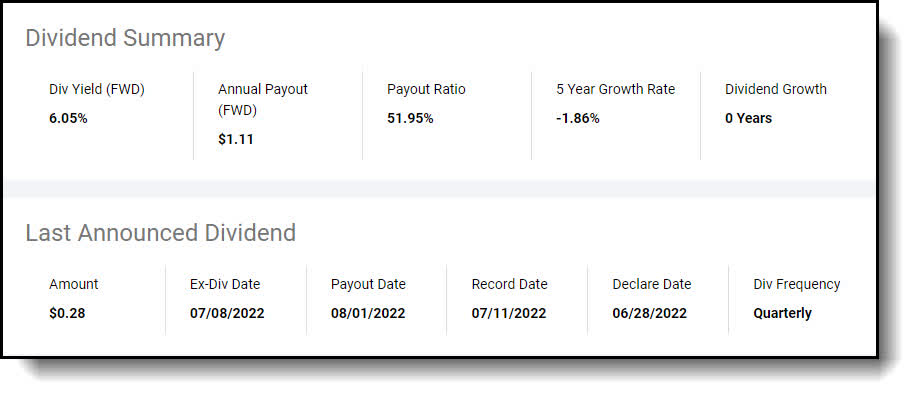

Seeking Alpha

The current quarterly dividend per share is $0.2775. The quarterly free cash flow required to cover dividend is approximately $2 billion. Come hell or high water, AT&T will pay the dividend, as we say in Texas. The current payout ratio is 66%.

AT&T’s 7% yield is well covered

AT&T is a mature high-yield income play with the potential for substantial capital appreciation. It you’re looking for dividend growth, this stock isn’t for you. This is a stock for those looking to boost their current income levels.

Think of AT&T as a giant mature oak tree that has been growing for years. It has grown into a majestic tree with a large canopy (7% dividend yield) that creates substantial shade (income) for you to enjoy during your golden years.

What’s more, AT&T is actually growing at present, taking share from Verizon (VZ) this last quarter. The company’s subscribers actually grew last quarter by 800,000. Let’s take a closer look at the latest results.

AT&T Has Strong Growth Potential

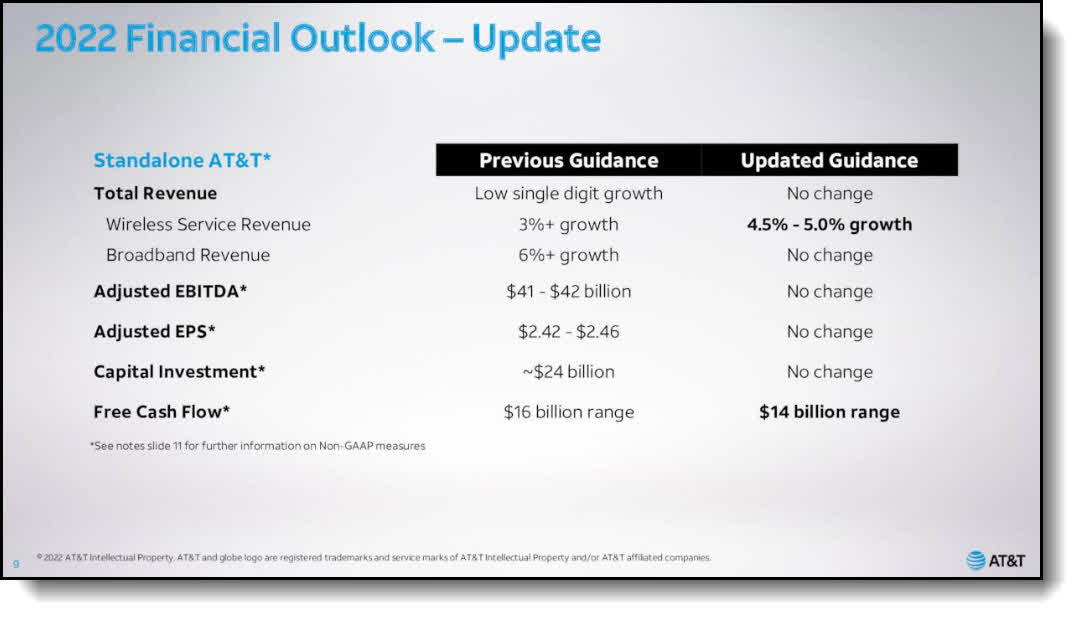

The selloff in AT&T began after last quarter’s earnings announcement. AT&T beat on the top and bottom line, yet lowered free cash flow guidance going forward by $2 billion. The lowering of free cash flow guidance was definitely the culprit for the recent selloff.

AT&T.com

Given the combination of elevated success-based investment, the potential for further extension of payments by customers, inflation and the more challenging environment facing the company’s Business Wireline unit, AT&T’s management made the prudent decision. They took a more conservative stance on free cash flow for the remainder of the year by lowering the estimated free cash flow guidance from $16 billion to $14 billion.

My take

I actually like this approach. It’s the “under promise to over deliver” method. Lowering the bar is never a bad idea under current market conditions. What’s more, the 25% drop in the stock just gave savvy income investors the chance to lock in a safe 7% yield.

AT&T.com

The company is basically a utility at this point, with our phones becoming a vital part of our daily lives. My primary focus is on the income provided by the substantial dividend. Nevertheless, with the major selloff, I submit most if not all of the bad news has been priced in. The stock is oversold and undervalued at present. Moreover, the earnings report really wasn’t all that bad. The following are some of the second quarter highlights from the company”

Second Quarter Highlights

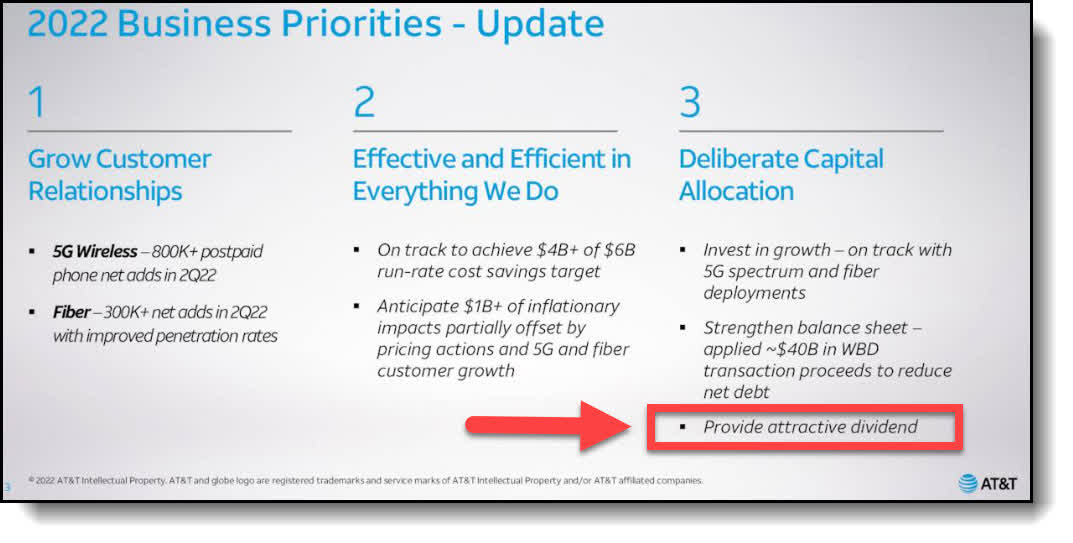

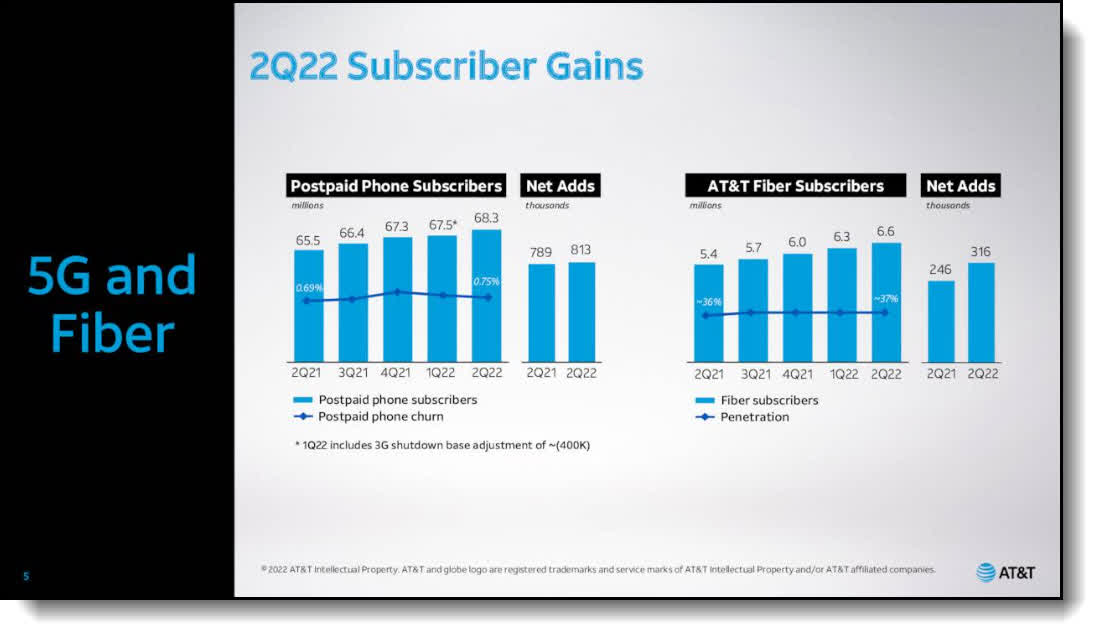

- MOBILITY: AT&T continues to see record levels of customer additions, including the best second quarter postpaid phone net adds in more than a decade and more than 6.1 million postpaid phone net adds over the past two years. We have already achieved our end-of-year target of covering 70 million people with mid-band 5G spectrum and are on track to approach 100 million people with mid-band 5G spectrum by the end of the year.

- AT&T FIBER: AT&T delivered subscriber growth near second quarter record levels with 316,000 AT&T Fiber net adds. This brings total net additions over the past two years to nearly 2.3 million, including 10 straight quarters of more than 200,000 net adds. We now have the ability to serve 18 million customer locations in more than 100 U.S. metro areas with AT&T Fiber.

- TRANSFORMATION: AT&T has confidence in its ability to achieve more than $4 billion of its $6 billion run-rate cost savings target by the end of the year.

Here are some key quotes from CEO Stankey on the conference call:

“We’re finding success in serving more customers in new and existing markets, with what we believe is the best wired Internet offering available. This is evidenced by our more than 300,000 second quarter AT&T Fiber net adds, marking our 10th straight quarter with more than 200,000 Fiber net adds.

Over the last eight quarters, we’ve achieved an industry-best 6 million postpaid phone net adds, while adding nearly 2.3 million AT&T Fiber customers, increasing our Fiber subscriber base by more than 50%. In the quarter, we had a remarkable 813,000 postpaid phone net adds, our best second quarter in more than a decade.

We have strong visibility on achieving more than $4 billion of our $6 billion transformation cost savings run rate target by the end of this year. As we shared before, we’ve initially reinvested these savings to fuel growth in our core connectivity businesses. However, as we enter the back half of this year, we expect these savings to start to contribute to the bottom line.”

AT&T.com

Let’s next review the current fundamental statistics related to valuation to gain a perspective on just how cheap the stock has gotten.

AT&T current valuation analysis

Finviz

AT&T is trading for multi-decade low valuation. The stock is trading for less than book value with a ratio of 0.97. Book value per share is actually $16.43. Forward P/E ratio stands at 6.35 and the stock is trading at less than one times sales at 0.82. These statistics mean two things to me. First, the stock is definitely oversold and unvalued. And most importantly, most of not all the bad news is presently priced in. Now let’s wrap this up.

Key Investor Takeaways

AT&T is a mature high yield income generator with a 7% yield and substantial upside. You’re buying AT&T for the abundant income its superior dividend yield provides. What’s more, the company has more than paid the price, with a 25% drop over the last quarter, for continuing to invest in the growth of its fiber and 5G businesses.

Nevertheless, AT&T is taking market share from Verizon. At some point in the future, the tide will turn, and you will want to be long on that day. AT&T shareholders will be richly rewarded with an excellent total return opportunity, and paid 7% while they wait. You can’t beat that deal.

My 12-month price target is $20 providing 30% upside from the time of this writing. There’s strong support at this level, which substantially increases your margin of safety. The stock is trading for a 30-year low valuation with a 7% yield attached. Finally, high yield dividend buying opportunities are often created by situations such as these. Remember, the time to buy is when the stock is out of favor, not when everyone is in love with it. One of my favorite quotes from investing icon Sir John Templeton is the following:

“Invest at the point of maximum pessimism.”

Templeton is known as a contrarian investor. He referred to his investment philosophy as “bargain hunting.” Templeton’s guiding principle was:

“Search for companies that offered low prices and an excellent long-term outlook.”

I feel this statement perfectly illustrates where AT&T’s stock is at this time. The reward far outweighed the risk with the stock yielding 7%. Our innate instincts encourage us to depart a sinking ship. This survival tactic impacts the way we invest. The herd running for the door is what creates the opportunity to buy a fundamentally solid company like AT&T with sound prospects at a discount. Hopefully, you have some dry powder and a long-term time horizon and take advantage. Those are my thoughts on the matter. I look forward to reading yours.

Your Input Is Required!

The true value of my articles is provided by the prescient remarks from Seeking Alpha members in the comments section below. Do you think AT&T is a Buy at current levels? Why or why not? Thank you in advance for your participation.

Be the first to comment