shaunl

U.S. Xpress Enterprises, Inc. (NYSE:USX) operates in a highly cyclical market landscape. Market volatility and softening of freight demand are evident. The company stays hammered as cost pressures overwhelm its revenue growth. Indeed, it can hardly maintain the balance between growth and viability. I am also worried about its fundamental stability. Liquidity appears problematic, which puts USX in a weak position against macroeconomic headwinds. Despite this, tables may turn as it increases their capacity and the inflation lull continues. But right now, it must get through near-term headwinds to show its potential. Meanwhile, the downward momentum of the stock price continues. It is consistent with fundamentals, but it appears too cheap to reflect its intrinsic value.

Company Performance

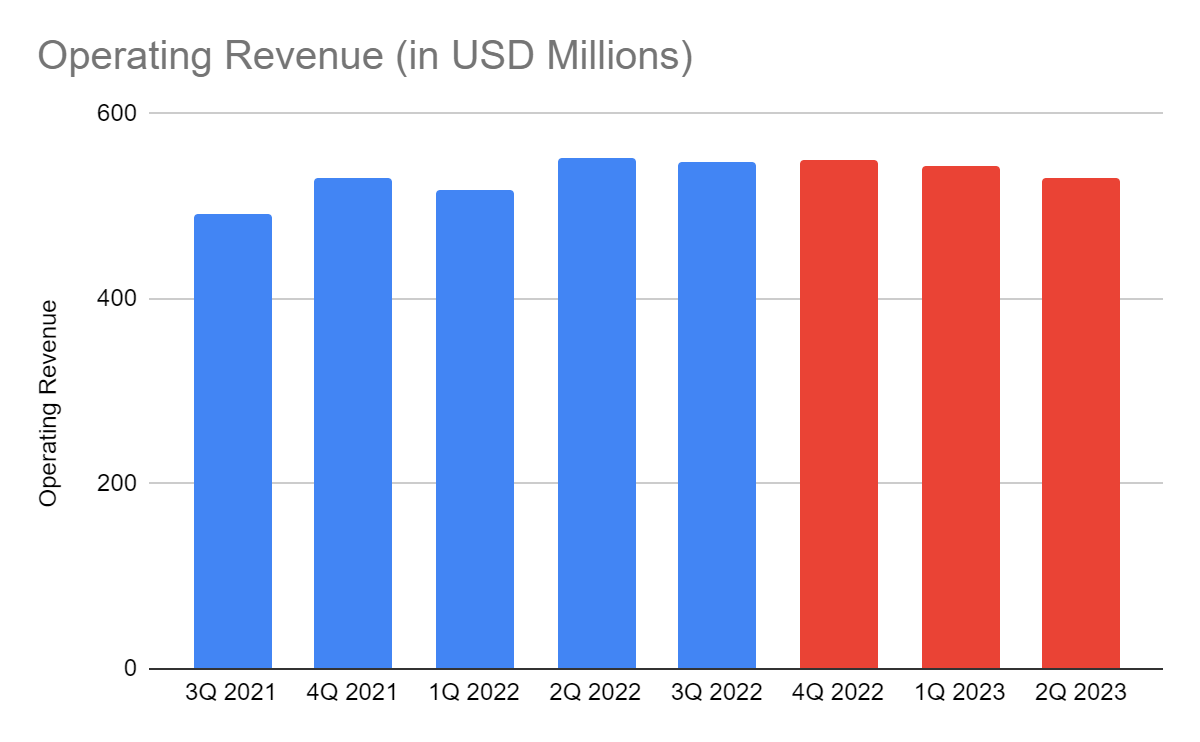

The trucking industry sees moderating freight demand amidst the potential recession. Although inflation accelerates, the purchasing power has not bounced back completely yet. Thankfully, U.S. Xpress Enterprises, Inc. demonstrates its ability to capitalize on the high-inflation environment. However, it is having a hard time stabilizing its core operations stable as cost pressures overwhelm revenue upsides. Currently, its operating revenue of nearly $550 million is quite impressive, given the 12% year-over-year growth. This decent growth can be attributed to several factors.

Operating Revenue (MarketWatch And Author Estimation)

One of the primary drivers is its continued expansion to increase its operating capacity and market visibility. It continues to increase its overall fleet size, allowing it to cater to more customers in a crowded freight brokerage market. One manifestation of its expansion is the continued increase in the number of tractors. After the additional 12% tractors, the company now has 6,400 tractors and 13,600 trailers. About 20% of tractors are provided by independent contractors. Indeed, it is one of the most prolific truckload companies, especially in the eastern part of the US. It is no wonder it has access to a massive network capacity. This aspect is crucial as supply chains start to improve. Note that many industries are now approaching the end of the backlog. As such, its truckloads are crucial for better inventory management.

Another driving force is its strategic pricing to offset increased fuel and equipment prices. It also allows USX to cope with the lower demand. Also, revenues will remain in an uptrend even if we exclude the impact of fuel surcharges. It shows decent growth of 5.7%. The combination of additional tractors and fuel surcharges helps the company increase its average truckload rate per mile by almost 10%. As such, its revenue strategies pay off. It succeeds in sustaining year-over-year growth amidst inflationary headwinds.

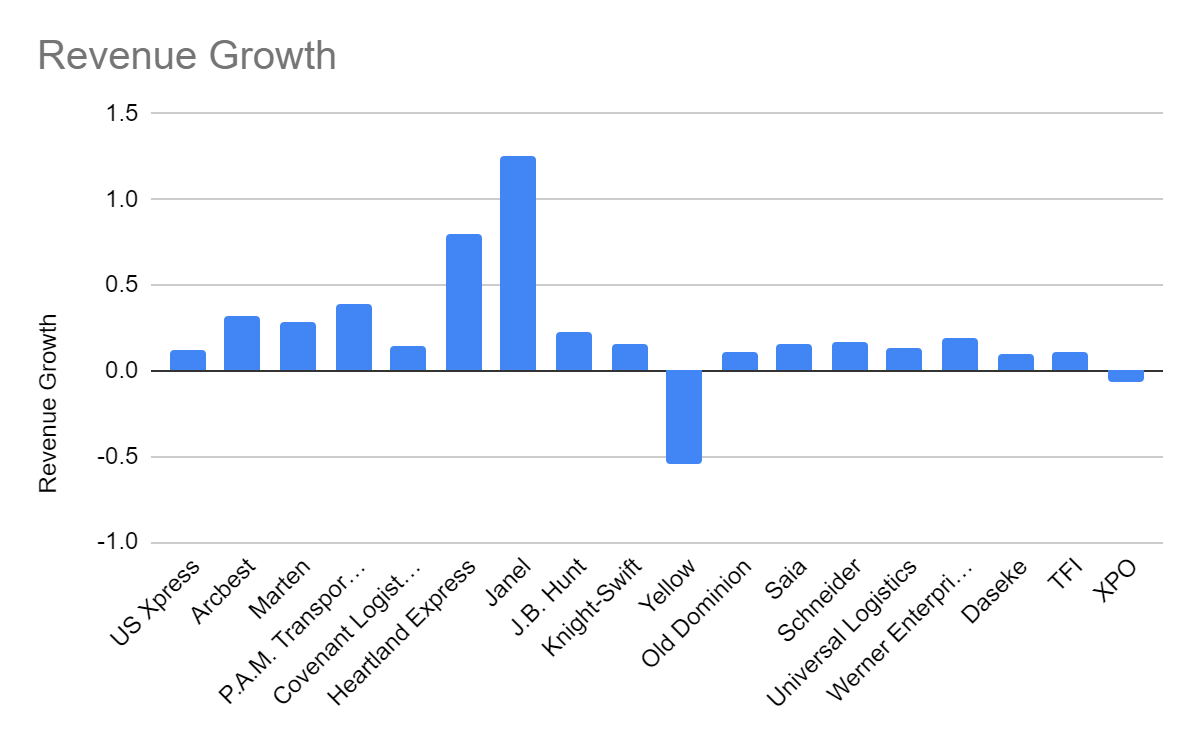

With regard to peers, U.S. Xpress remains a dwarf relative to many truckload and LTL giants. But its current performance appears better than the peer average. It holds a market share of 2.6% compared to 2.4% in the comparative quarter. Meanwhile, its revenue growth is lower than the market average of 22%. But it’s better than many larger peers, such as Yellow (YELL), Old Dominion (ODFL), XPO (XPO), and TFI (TFI).

Market Share (MarketWatch)

Revenue Growth (MarketWatch)

Likewise, costs and expenses are in a sharp uptrend. Cost pressures are evident, mainly from skyrocketing fuel prices, labor expenses, and purchased equipment. Currently, it navigates a tough environment while having to ensure the consistency of supply chain improvement. Even more noticeable is the massive increase in insurance claims. It more than doubled in just a year. Although it is barely 10% of operating expenses, its massive change is worth noting. It is because insurance claims are not part of the usual course of a truckload company. It is due to the development of file claims in an accident it got involved in a few years earlier. With that, margins are hammered at -4%. If we exclude the massive increase in insurance claims, the operating income will increase by $25.7 million. Despite this, margins will stay lower at 0.56% versus 1.04% and 1.1% in 3Q 2021 and 3Q 2022. It affirms the fact that inflation-driven costs and expenses, matched with the softened demand overwhelm revenues.

This year, USX must brace for a further downtrend in the first half. It may still be due to the softening freight market demand and the potential recession. I said it in many of my previous articles. I’m not so worried about the recession, but when it comes to trucking, things may be different. The movement of goods is crucial. Given the moderating demand and high inventory levels, the picture is quite different from 2021 and 2022. Even if a full-blown recession won’t take place, there may be some sort of economic slowdown. Given this, it may have to reduce its current volume and pricing.

On a lighter note, the return to normality and seasonality may help the industry become much more right-sized after a period of overwhelming freight demand. It may also help stabilize driver shortages. We hope that the impact of inflation will start to help stabilize costs and expenses. After all, the inflation lull has become faster, landing at 6.5%. But I expect it to materialize at least in the second half. With improved supply chains and lower fuel prices, it may be easier for the company to improve its capacity utilization. Of course, I expect near-term headwinds to impact the company. Operating revenues may decrease some more, but costs and expenses may start improving. As such, margins may stay low but may become more manageable.

Operating Margin (MarketWatch And Author Estimation)

How U.S. Xpress Enterprises, Inc. May Fare This Year

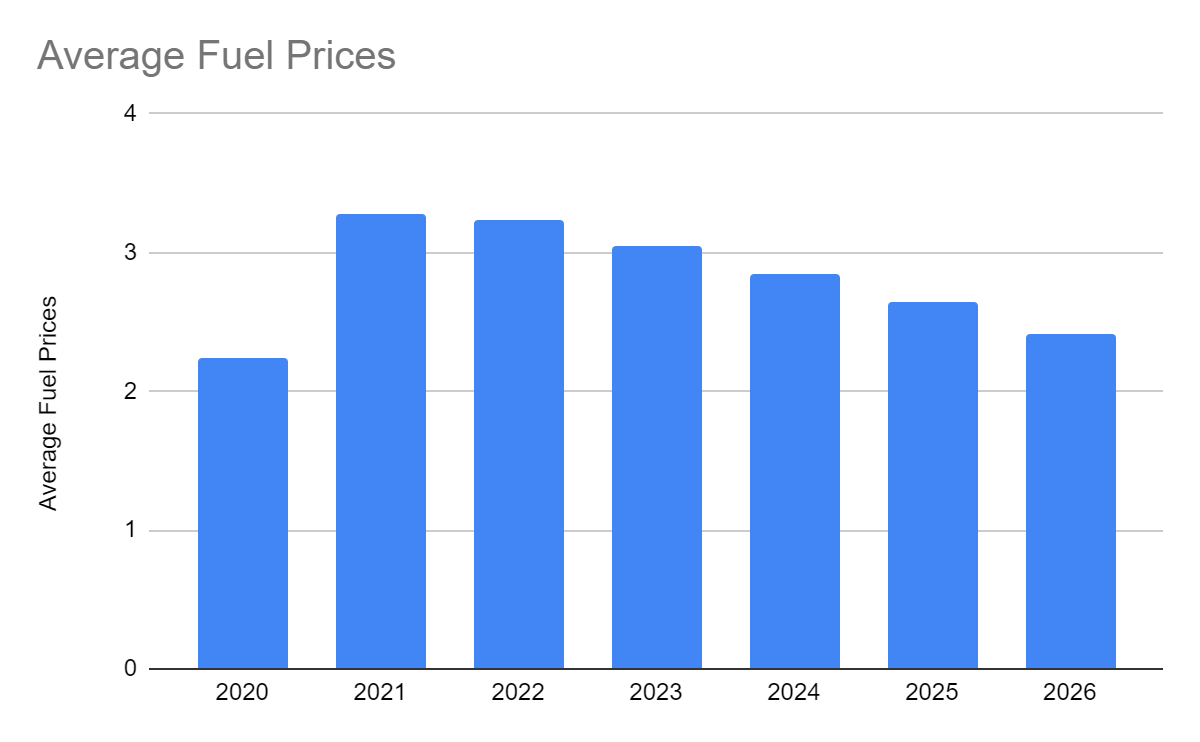

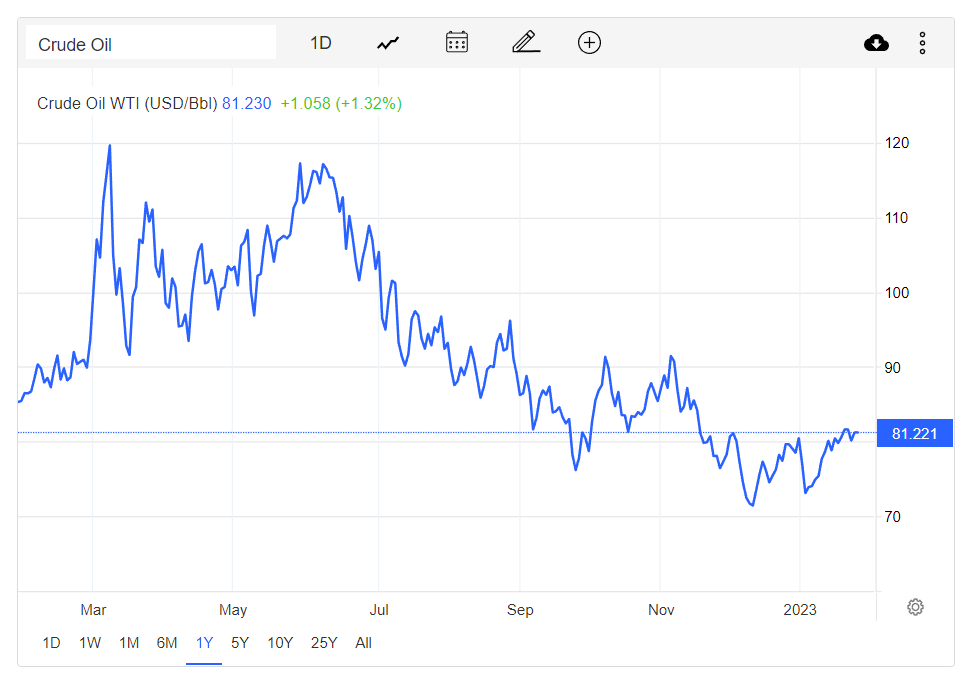

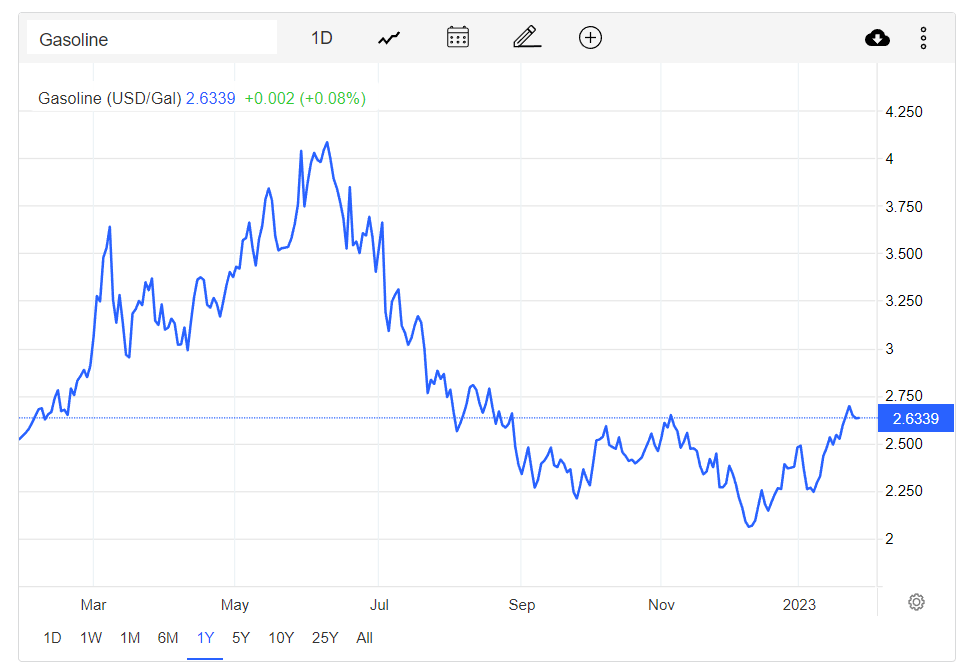

Softening freight demand and market slowdown are the primary concerns of the trucking industry this year. Even I, myself, adhere to the industry performance projections. Despite all these, I am not pessimistic at all. I still look forward to some boons taking place and giving decent prospects. Of course, we may not see it in the first half since near-term performance may show adjustments to the market trend. But sprinkles of hope may help USX cushion more blows and cope with them. First, the inflation lull has accelerated and dropped further than expected. At its current rate, it has already been cut by nearly 30% in six months. As such, it is logical to expect fuel and equipment prices to stabilize. After all, prices are now way lower than their peak in the first half of 2022, as shown in the charts below.

Average Fuel Prices (ST. LOUIS FED And Author Estimation)

Daily Crude Oil Prices (Trading Economics)

Daily Gasoline Prices (Trading Economics)

USX must also watch out for potential interest rate hikes. The combination of demand slowdown and rising interest rates may hammer its near-term performance. I expect interest rates to peak in the first half. Increments may slow down in the second half, so the company must withstand market pressures and find ways to bounce back. Despite this, I don’t buy overpessimistic market sentiment. There may be a slowdown at some point, but I don’t think it will lead to a deep recession due to several reasons. First, the inflation lull has sped up. Although the Fed must still be conservative, interest rate increments may be more relaxed than expected. I expect it at 4.5-4.8% versus the 5-5.25 market estimates. Second, inflation is more of a demand-pull than a cost-push. Third, labor market conditions are still a far cry from the situation during the Global Financial Crisis. Fourth, business activities may eventually bounce back once both demand and interest rate normalization stabilizes. Lastly, the government may help the industry rebound with its potential spending on the infrastructure law’s investment program. The transportation and logistics industry may play a crucial role in the movement of materials and labor.

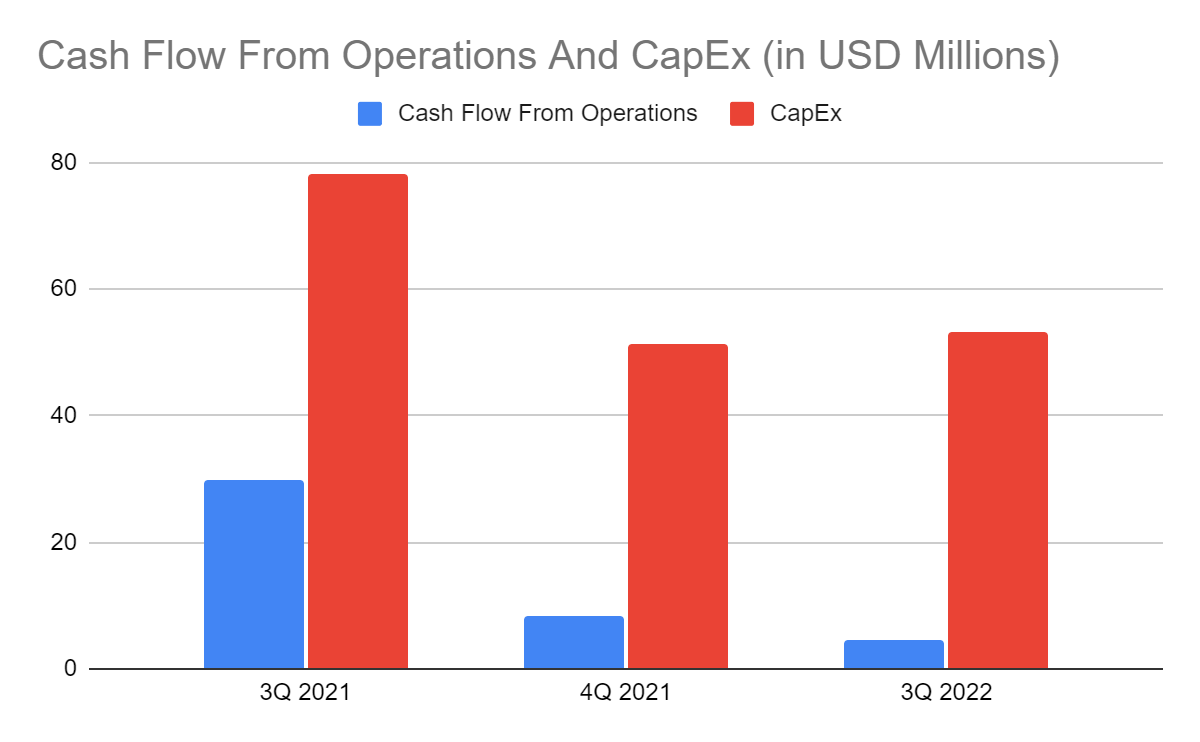

Despite this, USX must be more careful with its liquidity. It is a capital-intensive company so liquidity is king. The sad thing is that liquid assets, especially cash, remain very low. Its value of $1.4 million is about four times lower than in 2021. Cash burns may be understandable since the company has to cover its spending on fleet expansion and insurance claims. But the rate appears worrisome. It can be confirmed by its cash flow from operations, which has dropped from $30 million to $5 million. Even worse, borrowings have increased by over 20% in only a year. It is now 700 times higher than cash. Aside from interest rate hikes, the company can hardly sustain its current capacity. In turn, it has to raise its financial leverage. Its Net Debt/EBITDA Ratio is 13x, which is about thrice the maximum acceptable range of 3.5-4.5x. It is very risky since USX is a capital-intensive company. It needs a huge amount of cash to cover its operations. The way I see it using cash and borrowings alone, USX is heavily reliant on borrowings to sustain its current operating capacity. If this persists, there may be more cash burns. It may have to forego a portion of its operations to avoid burning more cash or raising financial leverage. It is a crucial concern since interest rates keep increasing, making the cost of borrowing more expensive. It may have a hard time keeping up with maturities despite its potential rebound. It is also difficult since the increase in revenues is offset by operating expenses. With that, the company appears to be earning way lower than it should cover borrowings. Cash inflows cannot also cover CapEx, leading to a negative FCF. It proves the continued cash burn of the company. Currently, it has a weak financial positioning to cushion the blow of macroeconomic volatility. On a lighter note, the company maintains a stable tangible book value. The company maintains enough capital, but again it has to improve liquidity.

Cash And Cash Equivalents And Borrowings (MarketWatch)

Cash Flow From Operations And CapEx (MarketWatch)

Stock Price Assessment

The stock price of US Xpress Enterprises, Inc. has been hammered in the last year. It remains consistent with fundamentals, making the downtrend reasonable. At $1.90, its value has already dropped by 59% in only a year. Despite this, it appears that the decrease has been too much to reflect its intrinsic value. Put simply, the stock price appears undervalued relative to its fundamentals. We can see it in its tangible book value. Its current TBVPS is 3.28, showing it has remained well-capitalized despite lacking liquid assets. It is only lower than the average in recent years at 3.39. But its value exceeds the stock price. The current PTBV of 0.98 shows that the current stock price downtrend is reasonable. But the relative valuation of 2019-2021 values appears very low. If we use the average PTBV of 1.57 to value the company, the target price will be $5.14, a 270% potential upside. We can confirm it using the EV Model. ($887 M – $780M) / 51,400,000 shares = $2.08. The derived value shows a 9% upside potential.

Bottomline

U.S. Xpress Enterprises, Inc. has been a hard time stabilizing revenue growth and balancing it with viability. I am still troubled with its liquidity, although it remains well-capitalized. Meanwhile, the stock price stays consistent with the fundamentals. But it’s too cheap to reflect its intrinsic value. Even so, it appears that as earnings stay hammered, so does the stock price. While relative valuation appears attractive, extra caution must be done before making a position. The recommendation, for now, is that U.S. Xpress Enterprises, Inc. is a hold.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment