6381380/iStock Editorial via Getty Images

Introduction

Here we are, once again, with another episode of the ongoing coverage of North-American Class-1 railroads. We will look at CSX Corporation (NASDAQ:CSX).

For those who are reading an article of this series for the first time, I would like to point out that we are doing here something a bit different from a simply analysis. In fact, what inspired me to initiate my coverage was studying and understanding what made Mr. Warren Buffett invest in a railroad and make it one of his favorite bets over time.

Summary of previous coverage

We have learned to consider a few key metrics Buffett looks at to assess a railroad. These are earning power, efficiency (operating margin and fuel efficiency), and use of capital (return on invested capital, capex, dividends and buybacks).

A company’s earning power is calculated as pre-tax earnings over interest. At the time of my first article, before Q3, CSX scored a 6.2. Then, the ratio moved upwards to 8, which made the company look more solid.

After Q3. CSX’s fuel efficiency worsened a bit, climbing upwards to 0.99 U.S. gallons of fuel consumed per 1,000 GTMs. In my article, I pointed out that it is not a given that when train velocity increases so does fuel consumption. In fact, the example of Canadian National (CNI) goes in the exact opposite direction, with the company achieving both higher speed and better fuel efficiency.

Regarding ROIC, CSX unfortunately does not disclose it. Therefore, I calculate it using the formula (NOPAT/invested capital). After the first half of 2022, the company was at a 15.4%. With the TTM data available after Q3, CSX’s ROIC decreased to 10.7%.

This made me state that, even though CSX is my favorite pick on the eastern side of the U.S., at the moment the company’s key metrics are not moving in the direction Mr. Buffett wants to see. This is why I wrote these words:

While I think the company is doing fine, I can’t say that, according to what I have learned from Mr. Buffett, it is improving its key metrics. This is an interesting case where if we look at a report with a different perspective from revenues, margins and EPS we may come across a picture that is a bit different from what we would think at first glance.

Q4 Results

Let’s look at most recent report to see what is going on with CXS and to understand whether or not Q3 was an accident or is part of a larger – and maybe concerning – trend.

Overall, the company showed it has pricing power, as most railroads do. In fact, while volumes decreased 1% YoY, revenues for the whole fiscal year were up 19%. Chemicals were down as a results of slowing industrial activity, and forest products were down too, a consequence of slowing housing construction. Automotive’s volume was up 14% for the quarter and 6% for the year, and this was largely expected due to easing supply chain constraints. However, other peers performed much better than this.

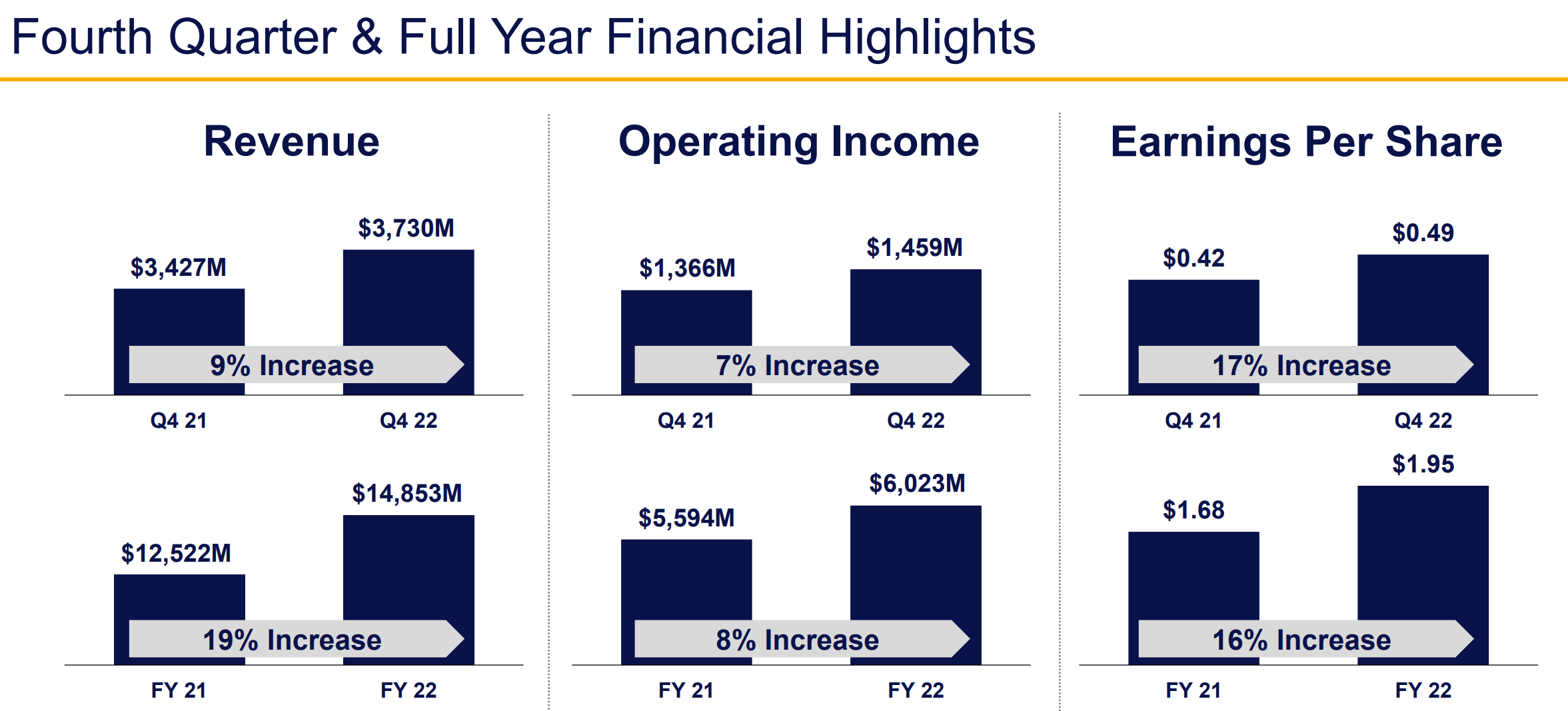

Now, by looking at the slide below showing the financial highlights, I see an elephant in the room.

CSX Q4 Results Presentation

Let’s consider the full year results. We look at revenue and we see a 19% increase YoY. Then we move to the operating income and we see just an 8% increase. Then we move to EPS and we are back to a double-digit increase of 16%. What is going on? Usually, a mature and well-managed company should see its revenue increase less than its operating income which should, on its turn, increase less than its EPS. In other words, the better a company is managed, the more each dollar of revenue is worth, generating more income and earnings through scale and operating efficiency. Here we are on a roller coaster. This means that CSX wasn’t efficient and that each dollar or increased revenue generated less income than usual. Not a good sign for a railroad, especially in an environment where other companies are performing better than this.

What made EPS spike up 16% when the OI was up just by 8%? The answer is easily found below.

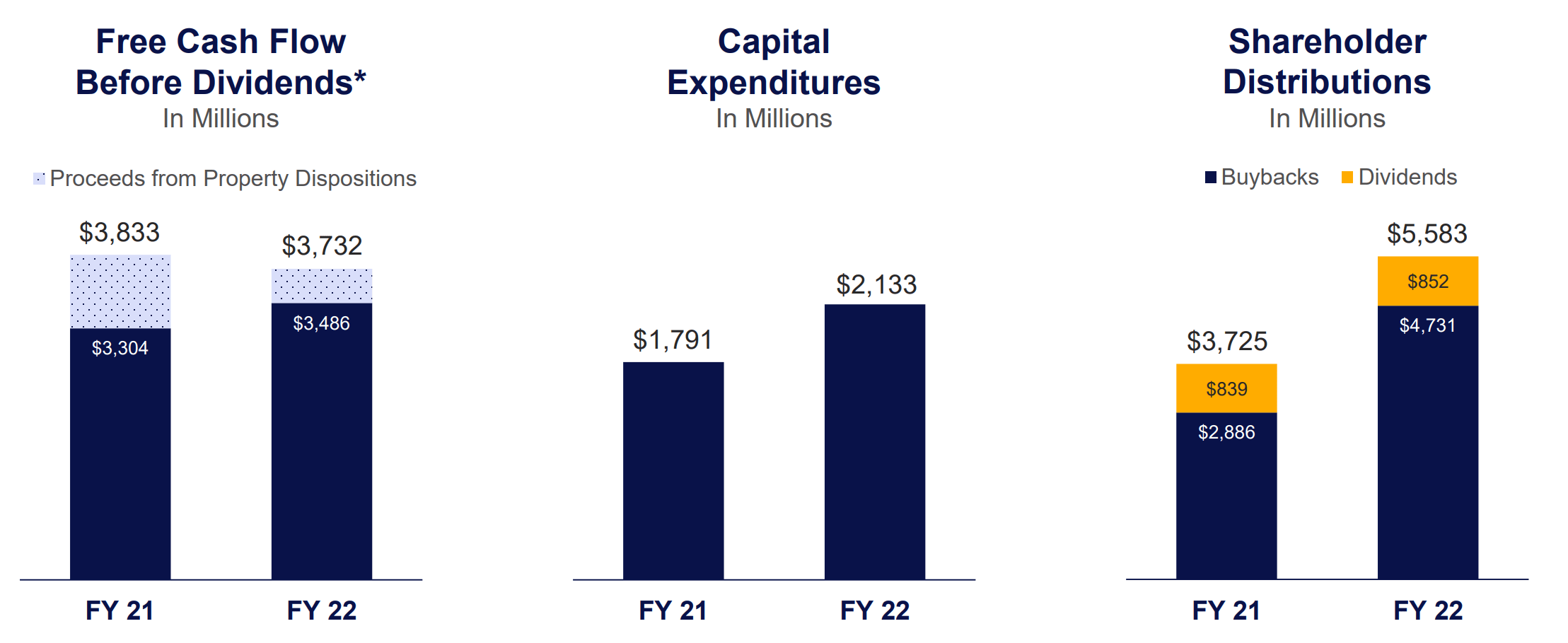

CSX Q4 Results Presentation

During 2022, CSX generated $3.49 billion of free cash flow. However, the company spent $4.73 billion on buybacks, coupled with another $852 million returned as dividends. No way I am going to like such a move, where shareholder returns are higher than the free cash flow generated by the company.

If we consider that the amount spent on buybacks is more or less 7% of the current market cap, we are close to understanding how an 8% operating income increase can turn into a 16% increase in earnings per share.

However, I don’t like this situation, as I think it endangers the company’s financials. In fact, if we look at the cash flow statement, we see that the company issued exactly $2 billion of long-term debt, which is more or less the difference between free cash flow generated of $3.49 billion and the $5.58 billion returned to the shareholders.

CSX now trades at $31.57 per share. With an average cost per share repurchased of $31.25 for 2022 and $31.91 for 2021 the company hardly created any value for its shareholder aside from decreasing the number of outstanding shares and thus changing the denominator of the EPS ratio.

The real thought I can make about this situation is that the company considers excess cash the cash it has on its balance sheet, which is currently $2 billion. I am not saying the company’s balance sheet is now in danger, but I think shareholder should we aware that this buyback pace is not sustainable.

With these considerations, we have already seen something about two aspects Mr. Buffett cares about:

1. Operating efficiency wasn’t good. In fact, the operating ratio for Q4 was above 60 and it came in precisely at 60.9%. For the year, it was 59.5% versus. 55.3% in 2021, a significant deterioration of 420 bps. True, the Quality Carriers trucking business adds about 250 points to the operating ratio, but, even if we facto this in, we are still before a bad result.

2. Use of capital wasn’t conservative and the company didn’t return just part of its excess capital, but it actually returned capital it didn’t generate during the year.

Let’s now look at some other aspects and let’s begin with earning power. Using the FY results, we have a 7.3 which is in the low range of railroads. Just to get an idea, Canadian National achieved a 12.34 for 2022.

Regarding fuel efficiency, CSX performed negatively with a 1% increase YoY in Q4 and a 3% increase if we look at the full year results. Currently, the company scores a 1, while it was able to improve just by 1% its train velocity (now at 17.5 mph) for the quarter, whereas it had a 10% deterioration for the same metric if we look at the whole past year.

Regarding the use of capital, we have already seen what I think could be a problem. Regarding capex, the company didn’t disclose much it is quarterly report and I am waiting to read the annual report to see if we will have further information, especially about network enhancement investments.

As we know, CSX doesn’t disclose its ROIC. However, we can calculate it and it is now at 10.8%, just 0.1 percentage point above where it was at the end of Q3. It is not a return that makes me astonished.

Conclusion

Overall, the last earnings report didn’t offer me any reason to revise my rating nor any data to think CSX Corporation should achieve impressive results during 2023. This is why I stick to my hold rating, considering the company around fair value, while not showing signs of being able to improve significantly its upcoming cash flows, a major point of interest for Mr. Buffett.

Overall, I think the words of Kevin Boone, CSX EVP, Sales & Marketing, during the last earnings call show something of how the company conceives itself at the moment: “we don’t pay — we don’t spend a lot of time thinking about the other Class 1 railroads.” I don’t want to give excess weight to these words, which may have also been said to show extreme confidence it the company’s own means. But if CSX Corporation looked a bit more at its peers, it could be stirred to increase its efficiency to the benefit of many.

Be the first to comment