Chinnachart Martmoh/iStock via Getty Images

We have previously covered CrowdStrike (NASDAQ:CRWD) here as a pre-earnings article in November 2022. CHPT’s elevated P/E valuation was discussed in comparison to its cloud/software/security peers, indicating the risk of a drastic correction at the slightest sign of slowing growth. We further analyzed its historical and projected performance through FY2025, with the conclusion that the company remains well-positioned through the worsening macroeconomics due to its robust balance sheet.

For this article, we have compared CRWD’s FQ3’23 performance with its peers. Despite tightened corporate spending during a period of worsening macroeconomic outlook, the market-wide demand for cybersecurity products has exceeded expectations indeed. It was also competent of the management to restructure their contracts accordingly to increase their odds of success during the elongated sales cycle. Combined with its accelerated forward top/ bottom line growth against its peers, it is no surprise that CRWD continues to trade with a notable baked-in premium.

Investment Thesis – Global Cybersecurity Demand Remains Robust

The CRWD stock is sorely understood indeed, since the company executed brilliantly with FQ3’23 EPS of $0.40 against estimates of $0.32. By the latest quarter, CRWD boasted a deferred revenue of $1.48B and a backlog (invoice prior to subscription commencement) of $782.2M, growing impressively QoQ by 8.82%/18.21% and YoY by 52.57%/19.47%, respectively. Its ARR also grew excellently by 9.34% QoQ and 56% YoY to $2.34B, despite the tougher YoY comparison. These numbers indicate that the company exceeded consensus expectations indeed.

In addition, CRWD grew its customer net retention rate across multiple modules remarkably. By FQ3’23, the company reported impressive subscription customers with five-or-more at 60%, six at 36%, and seven at 21%, respectively. These indicate an impressive 55%, 66%, and 81% YoY growth, respectively.

In the meantime, other cybersecurity companies have also performed well, with Zscaler (ZS) reporting YoY revenue growth of 54% and FQ1’23 EPS of $0.29. Okta (OKTA) similarly recorded revenue growth of 38% YoY and Remaining Performance Obligations (RPO) of 21% to $2.85B, with SentinelOne (S) also growing its ARR by 106% YoY to $487.4M. Considering the ongoing digital transformation post-reopening, we may infer that demand for cybersecurity products proves to be robust, with expanded multi-pillar contracts across the board.

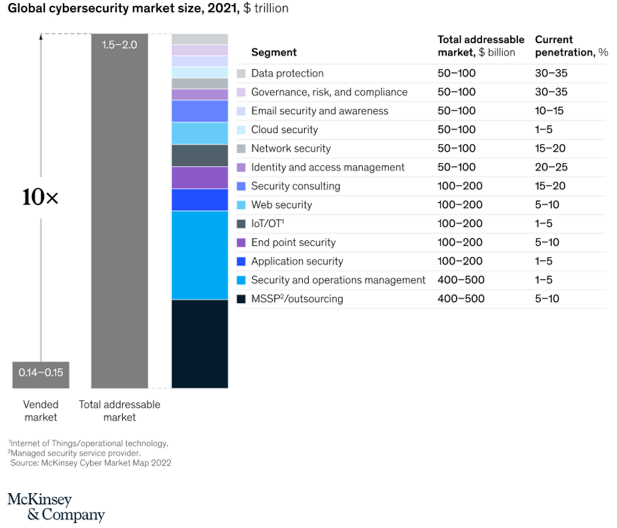

Global cybersecurity market size

McKinsey

With an addressable market of up to $2T through the next decade, it is apparent that there is a massive untapped potential for CRWD, since only $150B of global cybersecurity expenditure was reported in 2021. The global cybersecurity market is also expected to further expand to $900B, at a CAGR of 16.23% through 2032. These indicate the massive potential for growth and adoption once the macroeconomic normalizes and the market sentiments improve. Opportunistic investors only need to dollar cost average on the CRWD stock and stay patient through the worst of storms.

Why CRWD Deserves Its Premium P/E Valuations Against Its Peers

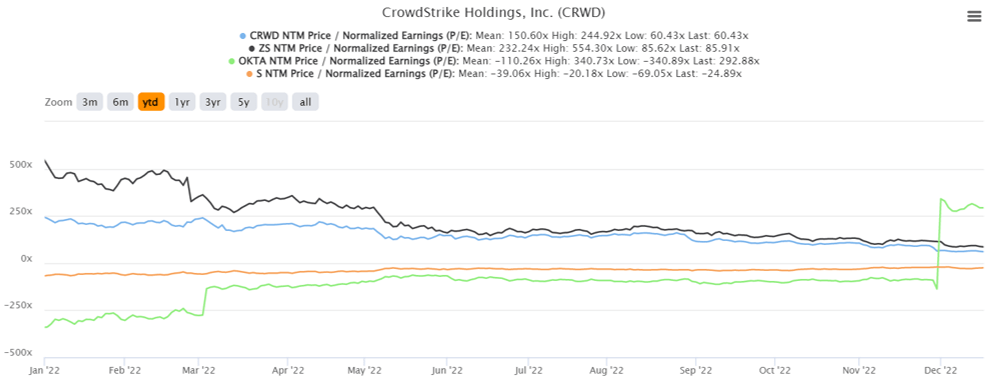

CRWD YTD P/E Valuations

S&P Capital IQ

CRWD is currently trading at an NTM P/E of 60.43x, lower than its YTD mean of 150.60x or relatively in line with its 3Y P/E mean of 59.81x. Its valuations are not overly exaggerated in comparison to its peers as well, such as Zscaler at NTM P/E of 85.91x, Okta at 292.88x, and SentinelOne at -24.89x. This is because market analysts expect CRWD to deliver an impressive revenue CAGR of 38.9% and an EPS CAGR of 62.5% through FY2025. These numbers naturally merit a certain premium against Zscaler at an EPS CAGR of 48.6%, with Okta likely achieving normalized profitability from FY2024 onwards, and SentinelOne from FY2025 onwards.

Based on CRWD’s FY2025 EPS of $2.88 and current P/E valuations, we are looking at an aggressive price target of $174.03. This number is not too far from the consensus bullish estimates of $170.06 indeed, indicating a notable 60.39% upside from current levels. However, we must also highlight the folly of market estimates, since CRWD has been effectively downgraded by -26.16% since the previous price target of $230 in early November. Odd indeed, since CRWD’s elongated sales cycle is a natural phenomenon during these uncertain economic conditions, with Zscaler and SentinelOne similarly reporting so in their recent earnings call:

Consistent with many other software companies and even our competitors, we are seeing higher cost consciousness and prudence around IT budgets. That’s leading to elongated sales cycles and limited budget availability. These factors are most pronounced in larger deals and they require higher level of evaluations and approvals. (SentinelOne – Seeking Alpha)

While there have been some headwinds in CRWD’s capability to land multiyear contracts recently, we are not concerned since the management is prudent in offering the option of a yearly deal instead. In addition, it went further in presenting flexible payment terms with multi-phase subscription start dates, which delays its ARR recognition into future quarters. These increase its rate of contract success during these uncertain macroeconomics indeed. These headwinds are only attributed to companies temporarily tightening their belts. As a result, Mr. Market only overreacted to the lower-than-expected forward guidance, since the management remains confident about its ~30% growth rate through FY2024, no matter the soft landing or recession.

In the meantime, CRWD continues to expand its partnership in the public sector as well, with up to 40 US state governments already on its Falcon platform. While the company does not break down its revenue segments by commercial and government end-market accordingly, we are strongly encouraged by this positive development in FQ3’23. Commercial sectors are more likely to be impacted by the ongoing macroeconomic, pointing to the current extreme pessimism levels due to market-wide spending and job cuts.

However, government agencies tend to be better insulated, as evidenced by Palantir’s (PLTR) performance thus far. The latter continues to report $1.02B of government revenues accounting for 55.73% of its revenue over the last twelve months, against 58.19% in FY2021. These contracts grew at an accelerated rate of 26% in FQ3’22 as well, against the 17% reported for the commercial segment. Combined with CRWD’s existing Impact Level 4 (IL-4) Authorization, we expect the company to remain well-positioned through these uncertainties, significantly aided by the “bread and butter” segment over the next few quarters.

Declines Are Also Attributed To The Pessimistic Market Sentiments

CRWD YTD Stock Price

{kind=link}

In the meantime, Mr. Market has been testing CRWD’s support level along with many stocks, due to the continued corrections thus far. At the time of writing, the stock has fallen by -21.67% since its recent earnings call. Otherwise, by a tragic -62.01% since its peak of $284.58 in November 2021, compared to Zscaler at -69.29%, Okta at -75.64%, and SentinelOne at -82.36%.

Perhaps, the worsening macroeconomic had something to do with CRWD’s decline, since the Feds are also poised to keep raising until a terminal rates of 5.1%, higher than the previous projection of 4.6%. Furthermore, China’s unexpected reopening cadence has thrown more uncertainties in the short term, due to the immense pent-up demand over the past three years of lockdown. Assuming a similar supply-demand imbalance as previously witnessed during the reopening cadence in 2021, global inflation may persist longer than expected through 2024 instead.

The prolonged elevated interest rates may also lead to a sustained reduction in company spending over the next two years, further affecting CRWD’s short-term performance. The employment market is relatively imbalanced as well, with aggressive job cuts in the tech sector while the labor market remains tight by November 2022. There is a reason why the S&P 500 Index has been trading sideways with a -20.41% plunge YTD, despite the upbeat November CPI and the Fed’s recent 50 basis points hike.

Then again, we are not overly worried, since this pain is only temporal, triggered by the projected soft landing after the hyper-growth post-COVID-reopening cadence. Therefore, we continue to rate the CRWD stock as a Buy, especially made sweeter by this deep correction.

We reckon a great entry point would be in the high double digits. Bottom-fishing investors may potentially wait for an $80 entry point for an improved margin of safety. However, our price target already looks attractive enough for long-term portfolio growth and investing. Do not make the folly of missing these attractive levels, since we expect the stock to perform well through the next decade.

Be the first to comment